Building a successful retirement takes more than simply matching your guaranteed income to your current monthly bills. The real threat to your savings usually comes from hidden costs that sneak into your budget years after you stop working. From Medicare premium surcharges tied to your previous income to the harsh reality of long-term care, couples frequently overlook expenses that can drain a healthy nest egg. You need a proactive strategy that accounts for out-of-pocket medical needs, sudden tax bracket shifts, and the compounding effects of inflation. By understanding exactly what these nine stealthy expenses are, you can adjust your withdrawals and protect your financial independence throughout your golden years.

Quick Summary

- Healthcare goes beyond standard premiums: Medicare surcharges, out-of-pocket deductibles, and routine care exclusions can easily add thousands of dollars to your annual budget.

- Long-term care is largely your responsibility: Medicare severely limits skilled nursing coverage, leaving you to shoulder the burden of expensive custodial care.

- Taxes can disrupt your income: Losing a spouse triggers a tax bracket shift, and up to 85% of your Social Security benefits may become taxable if your combined income exceeds outdated thresholds.

- Family and lifestyle choices add up: Financial support for adult children and heavy travel spending in early retirement require intentional boundaries and planning.

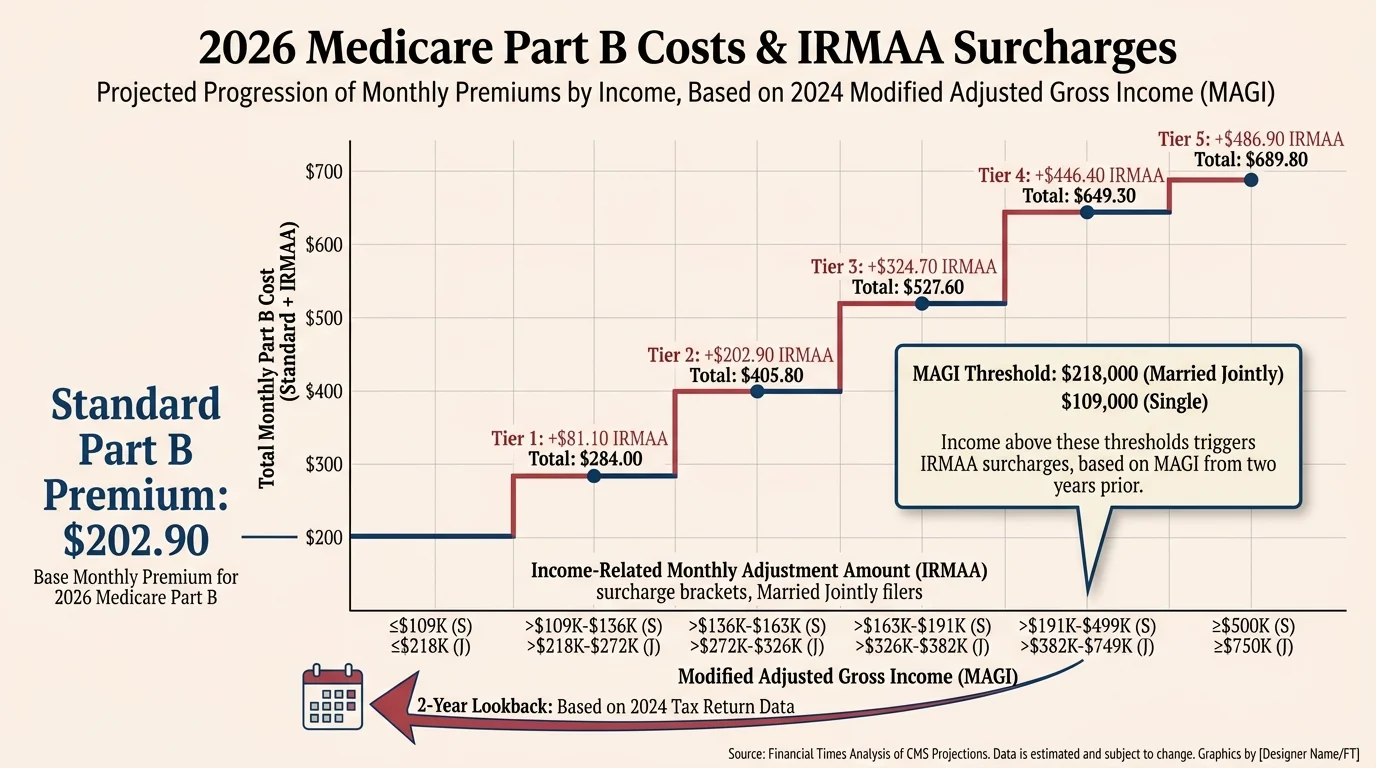

1. Medicare Premiums and IRMAA Surcharges

Many couples entering retirement mistakenly assume healthcare is entirely covered by the government once they turn 65. While Medicare Part A is usually premium-free, Medicare Part B comes with a mandatory monthly cost. For 2026, the standard Medicare Part B premium is $202.90 per month, reflecting an increase of nearly 10% from the previous year. The annual Part B deductible also rose to $283. Over a twelve-month period, a married couple pays nearly $4,870 just for standard Part B coverage before even seeing a doctor.

The situation becomes more expensive if you saved aggressively during your working years. If your income exceeds specific thresholds, you must pay an Income-Related Monthly Adjustment Amount (IRMAA). For 2026, IRMAA surcharges for married couples filing jointly begin at a Modified Adjusted Gross Income (MAGI) of $218,000, while single filers face surcharges starting at $109,000.

The trap most couples fail to recognize is the two-year lookback period. The Social Security Administration bases your 2026 IRMAA on your 2024 tax return. If you sold a rental property, executed a massive Roth conversion, or took a large portfolio withdrawal two years prior, that single taxable event can push you into a higher IRMAA bracket. This can unexpectedly add hundreds of dollars per person to your monthly Medicare bill.

2. Long-Term Care (Beyond the 100-Day Mark)

There is a dangerous misconception that Medicare acts as a safety net for nursing home care. The reality is far less forgiving. Original Medicare only covers short-term, skilled nursing care for up to 100 days following a qualifying inpatient hospital stay. Even during that brief window, coverage is not completely free; for days 21 through 100 in the 2026 calendar year, you are responsible for a daily coinsurance payment of $217.

Once you require custodial care—assistance with daily living activities like bathing, dressing, and eating—Medicare stops paying entirely. At this stage, the financial burden falls squarely on your personal savings. According to current data from the Genworth Cost of Care Survey, a private room in a nursing facility now carries a median monthly cost of roughly $10,025. This translates to over $120,000 per year for a single spouse.

Couples must actively plan for this exposure. Relying entirely on out-of-pocket payments can rapidly deplete an investment portfolio, leaving the healthy spouse with inadequate funds to maintain their lifestyle. You need to explore hybrid long-term care insurance policies, life insurance with long-term care riders, or specific Medicaid asset-protection strategies well before cognitive or physical decline begins.

3. The Widow’s Penalty and Shifting Tax Brackets

Retirement planning is often done under the assumption that both spouses will live to the exact same age. However, when one spouse passes away, the surviving partner faces a sudden and severe financial disruption frequently referred to as the widow’s penalty.

First, the household experiences a reduction in guaranteed income. When a spouse dies, the surviving spouse retains the larger of the two Social Security checks, but the smaller check disappears forever. Despite this drop in income, household expenses rarely decrease by half. Property taxes, home maintenance, utility bills, and insurance premiums largely remain the same.

Second, and often more damaging, is the shift in tax status. The surviving spouse must begin filing federal taxes as a single individual in the year following their partner’s death. Because the income brackets for single filers are significantly narrower than those for married couples filing jointly, the surviving spouse may end up paying higher taxes on a lower total income. This bracket compression forces many widows and widowers to withdraw even more money from their traditional retirement accounts just to cover the tax bill.

4. Routine Dental, Vision, and Hearing Care

If you rely exclusively on Original Medicare, you must prepare to pay cash for routine sensory and dental maintenance. The program explicitly excludes coverage for routine dental cleanings, extractions, fillings, and dentures. It also does not pay for routine eye exams, prescription glasses, or hearing aids.

These are not minor expenses. A quality pair of prescription hearing aids can easily cost between $3,000 and $6,000, and they typically need to be replaced every five to seven years. Extensive restorative dental work—such as implants, crowns, or bridges—frequently results in out-of-pocket bills exceeding $5,000 per spouse.

To combat these costs, many couples choose to enroll in Medicare Advantage plans that bundle these benefits, or they purchase standalone dental and vision insurance policies. If you prefer to self-fund, you must intentionally build a healthcare cash buffer into your retirement savings specifically earmarked for these inevitable aging-related expenses.

5. Taxes on Your Social Security Benefits

Do not assume your Social Security checks are yours to keep free and clear. Up to 85% of your benefits may be subject to federal income tax if you cross specific income thresholds set by the Internal Revenue Service.

The IRS uses a formula called “Combined Income” to determine the taxability of your benefits. You calculate this by adding your Adjusted Gross Income (AGI), your nontaxable interest (such as municipal bonds), and one-half of your Social Security benefits.

| Filing Status | Up to 50% Taxable (Combined Income) | Up to 85% Taxable (Combined Income) |

|---|---|---|

| Single / Head of Household | $25,000 — $34,000 | Over $34,000 |

| Married Filing Jointly | $32,000 — $44,000 | Over $44,000 |

Because Congress established these thresholds decades ago and never indexed them for inflation, nearly half of all retirees now pay taxes on their benefits. If you and your spouse withdraw heavy amounts from a traditional IRA or 401(k), you artificially inflate your AGI, which in turn triggers higher taxes on your Social Security income. Managing your withdrawal sequence and utilizing Roth accounts can help you mitigate this stealth tax.

“Taxes will be the single biggest expense in retirement. It is not about what you make, it is about what you keep.” — Ed Slott, CPA and Retirement Tax Expert

6. Home Modifications for Aging in Place

Many couples declare they want to stay in their family home for the duration of their retirement. Aging in place sounds financially efficient because you avoid expensive monthly assisted living fees, but the physical reality of a declining body requires expensive structural modifications.

Homes built decades ago are rarely designed with senior mobility in mind. To make a home safe, you might need to widen doorways for wheelchair access, install a stairlift, replace an old bathtub with a zero-entry shower, add grab bars, and retrofit a first-floor room into a primary bedroom. A comprehensive accessible bathroom remodel alone can range from $15,000 to $25,000. If you plan to remain in your current property, you must allocate a dedicated portion of your savings to home renovations before a medical emergency forces your hand.

7. The Lag in Purchasing Power

Retirement can last three decades, giving inflation ample time to erode your purchasing power. While Social Security offers an annual Cost-of-Living Adjustment (COLA), the formula used to calculate it rarely captures the true spending habits of older Americans.

For 2026, the Social Security Administration announced a 2.8% COLA, resulting in a relatively modest monthly increase for the average beneficiary. However, the expenses that dominate a retiree’s budget—such as medical care, prescription drugs, property taxes, and homeowners insurance—historically rise at a much faster pace than the broader consumer price index. If your investment portfolio is entirely parked in conservative cash equivalents, your money is quietly losing value. You must maintain exposure to growth-oriented assets like equities to ensure your savings outpace long-term inflation.

8. Supporting Adult Children and Grandchildren

A surprising and highly variable drain on retirement portfolios comes from family dynamics. Many couples significantly underestimate how much financial support they will provide to their adult children and grandchildren. Whether it involves helping with a down payment on a house, funding a grandchild’s college tuition through a 529 plan, or stepping in to cover a child’s medical emergency, family bailouts can severely disrupt your safe withdrawal rate.

You must place your financial security first. You cannot borrow money to fund your retirement, but your children can secure loans for education or housing. Establish firm financial boundaries with your family early in your retirement to ensure your generosity does not jeopardize your long-term independence.

9. The “Go-Go” Years Travel Boom

Financial planners often divide retirement into three phases: the go-go years, the slow-go years, and the no-go years. During the initial go-go phase, newly retired couples finally have the free time to pursue the travel and hobbies they delayed during their working careers.

This pent-up demand frequently results in spending that exceeds pre-retirement levels. Between booking international cruises, upgrading recreational vehicles, dining out frequently, and treating the family to vacation rentals, the first five to seven years of retirement can rapidly drain a portfolio if not carefully monitored. You should build a realistic “fun bucket” into your initial retirement budget, giving yourselves permission to enjoy the wealth you built while setting strict limits to preserve capital for your later years.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Chairman and CEO of Berkshire Hathaway

Costly Errors to Sidestep

Avoiding critical mistakes is just as important as picking the right investments. When couples fail to coordinate their strategies, they leave thousands of dollars on the table. Watch out for these three major pitfalls:

- Ignoring the Medicare initial enrollment window: Failing to enroll in Medicare Part B when you are first eligible (and not covered by creditable employer insurance) results in permanent late-enrollment penalties. These penalties are added to your monthly premium for the rest of your life.

- Filing for Social Security in a vacuum: When one spouse claims Social Security as early as age 62, they permanently lock in a reduced benefit. This decision also permanently reduces the survivor benefit available to the remaining spouse after a death. Couples must strategize their claiming ages together to maximize survivor protections.

- Keeping too much wealth in tax-deferred accounts: If your entire nest egg sits in traditional IRAs and 401(k)s, Required Minimum Distributions (RMDs) will eventually force you to withdraw large sums of money. This taxable income can trigger higher tax brackets, subject your Social Security to the 85% tax threshold, and incur steep IRMAA surcharges.

When DIY Isn’t Enough

Managing day-to-day budgeting is something most couples can handle on their own, but certain retirement transitions demand specialized expertise. You should seek out a fiduciary financial advisor or tax professional in these specific scenarios:

- Executing Roth Conversions: Moving money from a traditional IRA to a Roth IRA requires you to pay taxes upfront. A professional can help you calculate the exact amount to convert each year to fill up your current tax bracket without spilling over into higher rates or triggering IRMAA.

- Medicaid Spend-Down Strategies: If you are trying to protect your legacy from nursing home costs, navigating the Medicaid five-year lookback period is incredibly complex. An elder law attorney can assist you in establishing irrevocable trusts or executing legitimate asset transfers to meet state eligibility requirements.

- Navigating High-Net-Worth Estate Planning: If your estate is large enough to face federal or state inheritance taxes, you need proper legal structures to ensure your wealth transfers smoothly to your heirs and preferred charities rather than the government.

Frequently Asked Questions

What is the difference between Medicare and Medicaid for long-term care?

Medicare is a federal health insurance program based on age (65 and older) or disability, and it only covers short-term skilled nursing care. Medicaid is a joint federal and state program based on financial need; it is the primary government program that pays for long-term custodial nursing home care once your assets are depleted.

How can we avoid paying Medicare IRMAA surcharges?

The most effective way to avoid IRMAA is to manage your Modified Adjusted Gross Income (MAGI). You can do this by drawing income from tax-free sources like Roth IRAs, utilizing Qualified Charitable Distributions (QCDs) from your traditional IRA to satisfy your RMDs without adding to your taxable income, and carefully timing large capital gains.

At what age should couples start planning for long-term care?

The optimal time to investigate long-term care insurance or asset-protection strategies is during your mid-to-late 50s. At this age, you are still likely to pass the medical underwriting required for insurance policies, and premiums are generally more affordable than if you wait until your 60s or 70s.

A successful retirement requires you to look beyond the surface-level expenses of housing and groceries. By acknowledging the hidden costs of healthcare surcharges, shifting tax brackets, and long-term care, you can build a resilient financial plan. Take the time to sit down with your spouse, review your expected income sources, and run stress tests against these nine forgotten expenses to ensure your money lasts as long as you do.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: May 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.