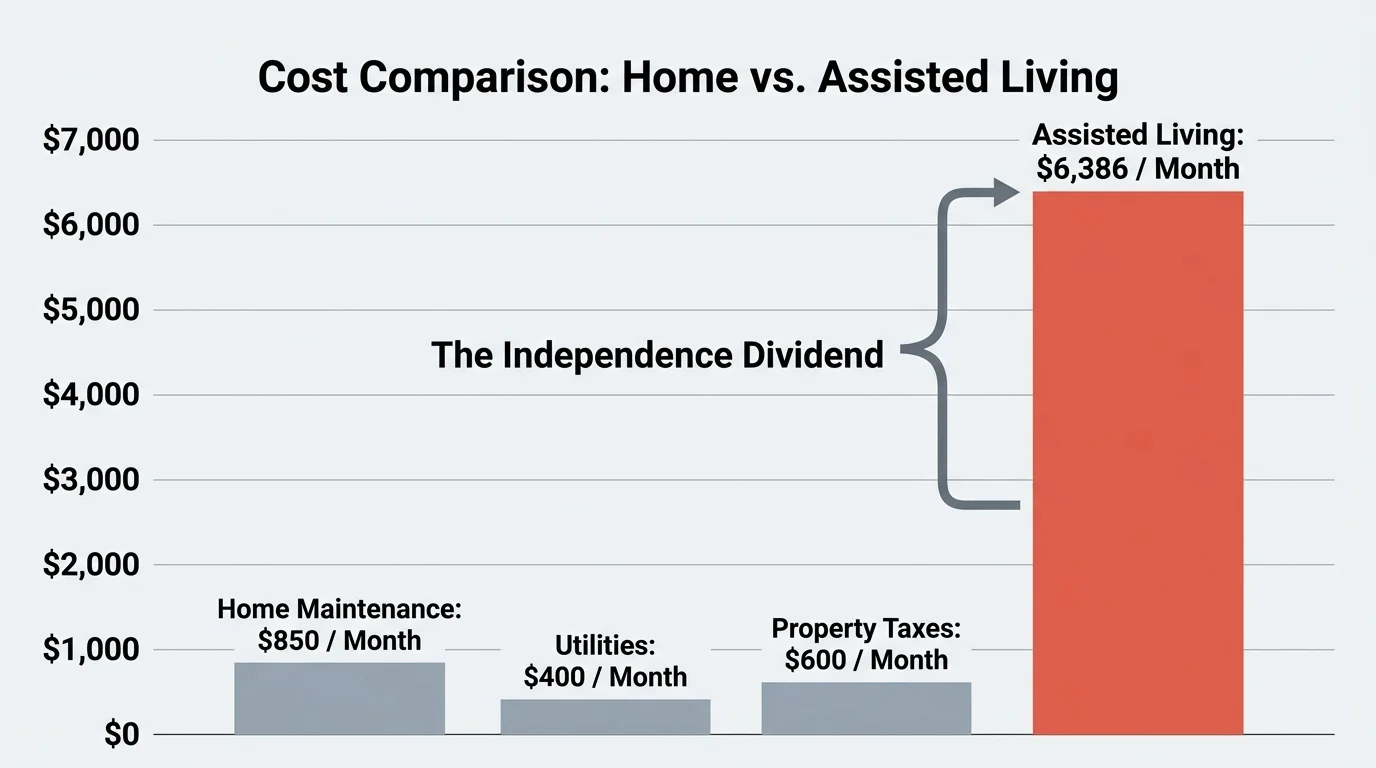

Staying in your own home and living on your own terms isn’t just about physical comfort; it is a massive financial decision. With the national average cost of an assisted living facility climbing to roughly $6,386 per month in 2026, preserving your physical health and financial stability is the ultimate wealth-protection strategy. Independence is a muscle that requires daily exercise—both in how you move your body and how you manage your money.

Building a secure retirement doesn’t always require sweeping, dramatic changes. Often, the difference between outliving your money and enjoying a comfortable, autonomous lifestyle comes down to small, repeatable actions. By weaving the right financial, physical, and administrative habits into your daily routine, you create a safety net that protects your savings and your freedom.

1. Prioritize Preventive Health to Protect Your Wealth

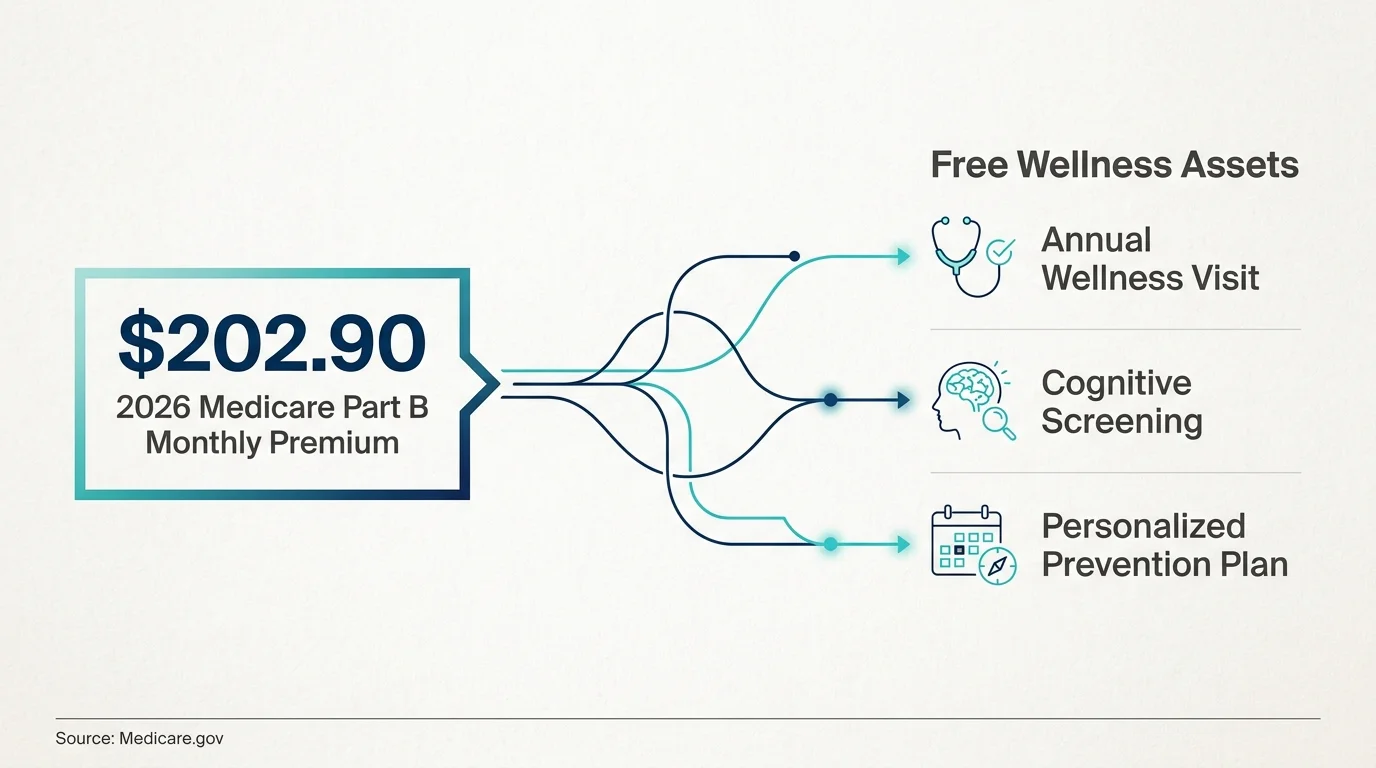

Medical expenses are the silent drain on retirement savings. Cultivating a daily habit of monitoring your health directly impacts your bottom line. For 2026, the standard Medicare Part B premium is $202.90 per month. Because you are paying this premium out of your Social Security check, you should absolutely maximize the benefits it provides.

Make it a habit to schedule and prepare for your Medicare Annual Wellness Visit. This is not a standard physical, but rather a comprehensive conversation about your health risks, cognitive function, and personalized prevention plan. Catching a condition early through a free screening can prevent thousands of dollars in future out-of-pocket costs and hospital co-pays.

2. Master the “Micro-Budget” to Outpace Inflation

According to the Social Security Administration, the cost-of-living adjustment (COLA) for 2026 is 2.8%, bringing the average monthly benefit to about $2,071. While this boost helps, everyday expenses like groceries, property taxes, and utilities often rise faster than fixed incomes.

Instead of a stressful monthly budget overhaul, adopt a daily “micro-budgeting” habit. Spend five minutes each morning reviewing your checking account and the previous day’s spending. This simple daily touchpoint prevents overdraft fees, alerts you immediately to fraudulent charges, and keeps you acutely aware of where your money goes. If your monthly benefit is $2,071, knowing exactly how much of that is spoken for by fixed costs allows you to spend the rest without guilt or anxiety.

3. Invest 30 Minutes Daily in Low-Impact Movement

Physical independence and financial independence are deeply connected. A single fall can lead to an expensive hospital stay, physical therapy, and the sudden need for paid in-home care or an assisted living facility. Taking 30 minutes a day to engage in low-impact exercises—like brisk walking, tai chi, or water aerobics—improves your balance and joint health.

Many Medicare Advantage plans and Medicare Supplement plans offer free gym memberships through programs like SilverSneakers. Making daily movement a non-negotiable habit is one of the most effective ways to delay or completely avoid the devastating costs of long-term custodial care.

4. Automate Financial Duties to Prevent Costly Penalties

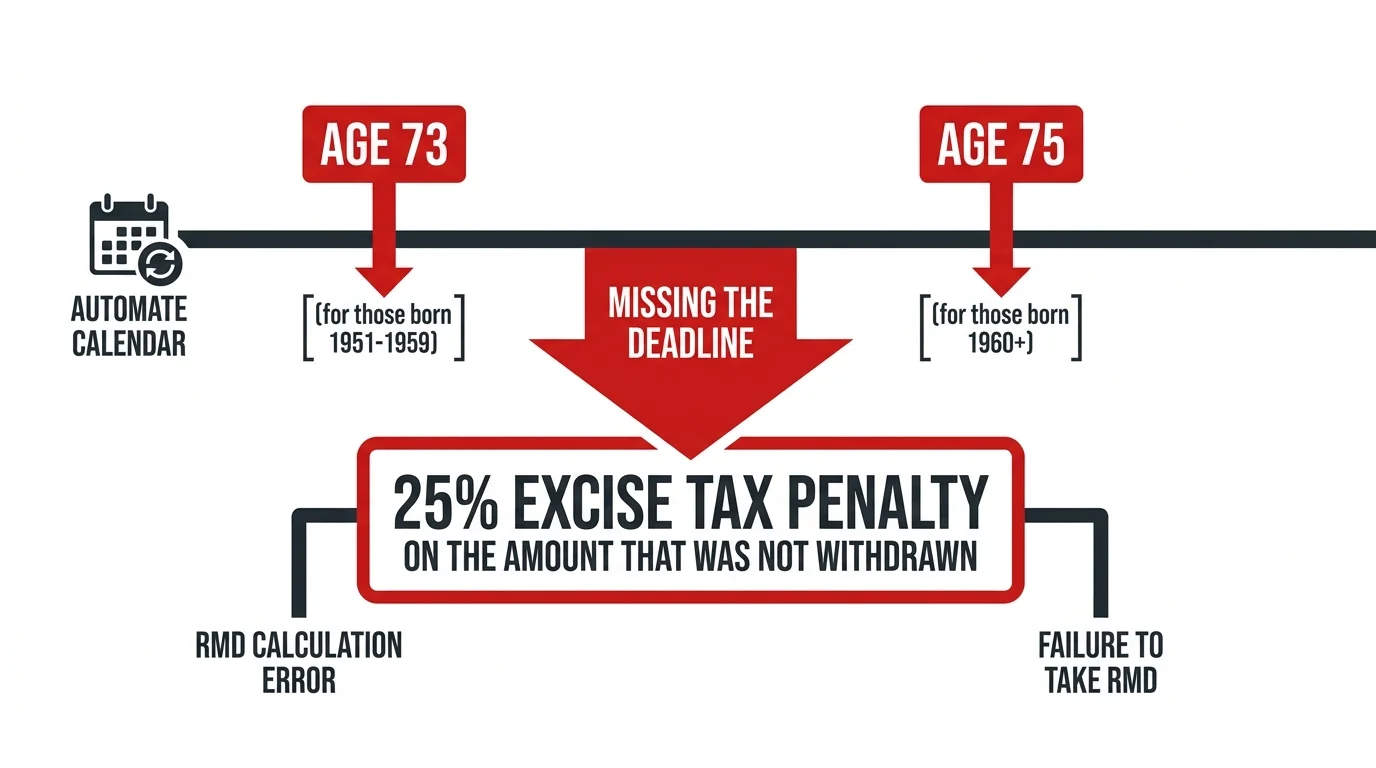

Memory lapses happen to everyone, but in retirement, forgetting a financial deadline can trigger massive penalties. If you have tax-deferred retirement accounts like a Traditional IRA or a 401(k), the IRS mandates that you take Required Minimum Distributions (RMDs) starting at age 73 (or age 75 if you were born in 1960 or later).

If you fail to take the exact required amount by the deadline, the Internal Revenue Service imposes a steep 25% excise tax on the amount you failed to withdraw. While this drops to 10% if you correct the error within two years, it is still a painful loss of your hard-earned money. Make it a habit to automate your essential financial duties. Set up automatic bill pay for your utilities and Medicare premiums, and work with your brokerage to automate your annual RMDs so you never hand over a quarter of your retirement income to the IRS unnecessarily.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Investor and Philanthropist

5. Claim the Tax Breaks You Have Earned

Taxes do not stop when your paycheck does. However, the tax code offers specific provisions to help older Americans keep more of their money. Cultivate a habit of neatly filing your medical receipts, property tax bills, and charitable donation records into a designated folder throughout the year.

When tax season arrives, this habit pays off. For the 2025/2026 tax years, the IRS grants an additional standard deduction for taxpayers aged 65 and older. Single filers receive an extra $2,000 on top of their base standard deduction, and married couples filing jointly receive an extra $1,600 per qualifying spouse. Furthermore, recent legislative changes have expanded bonus deductions for qualifying seniors. By staying organized daily, you ensure you never miss out on deductions that lower your taxable income.

6. Build a “Scam Defense” Routine

Seniors lose billions of dollars annually to sophisticated financial fraud. Protecting your assets is paramount to maintaining your independence. Develop a daily habit of healthy skepticism.

- Never answer calls from unknown numbers; let them go to voicemail.

- Do not click on links in text messages claiming a package delivery failed or your bank account is locked.

- If you receive an alarming message about your Social Security or Medicare, ignore the message and log directly into your official my Social Security account to verify its legitimacy.

Taking just two seconds to pause and verify a request can save your entire life savings from cybercriminals.

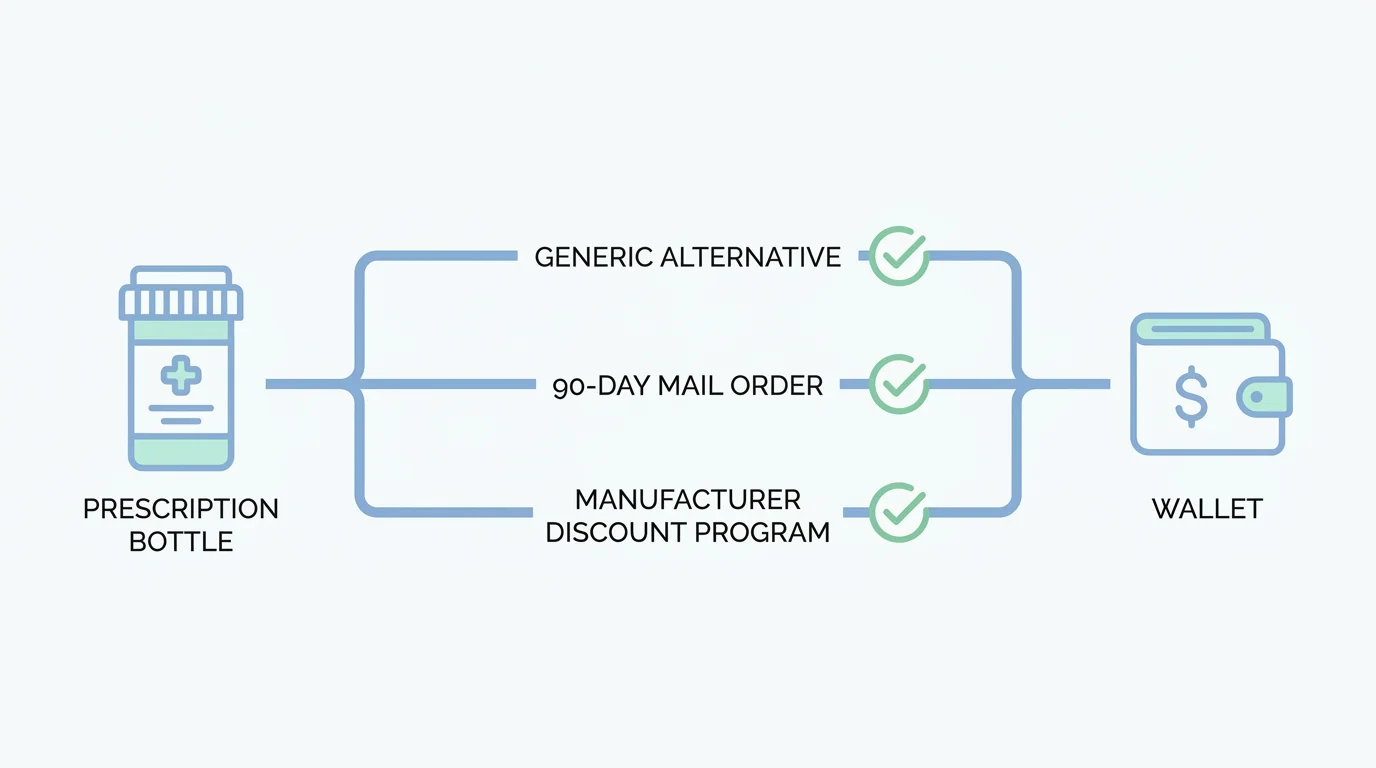

7. Audit Your Prescriptions and Seek Discounts

Prescription drug costs can eat up a massive portion of a fixed income. Make it a routine to regularly discuss your medication list with your doctor or pharmacist. Ask if there are generic alternatives or if you can safely stop taking a medication that is no longer necessary.

Beyond the pharmacy, make it a habit to seek out senior discounts everywhere you go. From grocery stores and restaurants to auto mechanics and cellular providers, asking “Do you offer a senior discount?” is a free, simple habit that can stretch your dollars significantly. Organizations like the National Council on Aging (NCOA) also offer excellent tools like BenefitsCheckUp to help you find local programs that assist with utility bills and property taxes.

8. Eat Brain-Healthy Foods on a Budget

Nutrition plays a massive role in cognitive longevity and energy levels. You do not need to buy expensive, trendy superfoods to eat well. Make a weekly habit of planning your meals around budget-friendly, nutrient-dense staples like beans, lentils, frozen vegetables, and canned fish (like sardines or salmon, which are rich in Omega-3s).

If your budget is exceptionally tight, do not let pride get in the way of using community resources. Millions of older adults utilize the Supplemental Nutrition Assistance Program (SNAP) to help cover grocery costs, freeing up cash for housing and medical needs.

9. Socialize With Purpose

It might seem surprising to list socializing as a financial and independence habit, but isolation is a documented health hazard. The physical deterioration caused by chronic loneliness is often compared to smoking 15 cigarettes a day. Health decline directly accelerates the need for paid medical intervention and facility care.

Call a friend daily, volunteer at a local charity, or join a community group. Staying socially engaged keeps your mind sharp, gives you a support network to lean on during difficult times, and significantly reduces the risk of cognitive decline.

Understanding the True Costs of Care

To fully grasp why these daily habits are so vital, it helps to look at the numbers. Medicare does not cover long-term custodial care (help with bathing, dressing, and eating). If you lose your independence, the out-of-pocket costs can be staggering.

| Care Type | Average 2026 Monthly Cost | Does Medicare Cover It? |

|---|---|---|

| Assisted Living Facility | $5,900 to $6,386 | No (Considered custodial care) |

| In-Home Care Aide (Part-time) | $4,500 to $5,500 | Rarely (Only short-term if medically necessary) |

| Nursing Home (Private Room) | $9,000+ | Only for short-term rehab (up to 100 days) |

Costly Errors to Sidestep

Even with great daily habits, large structural mistakes can derail your independence. Avoid these common pitfalls:

- Claiming Social Security without a plan: Claiming at age 62 locks in a permanent reduction of up to 30% of your benefit. If you have longevity in your family, delaying your claim can significantly boost your guaranteed monthly income.

- Assuming Medicare covers everything: From dental implants to hearing aids and long-term care, Medicare has strict limits. Budgeting for these out-of-pocket gaps is essential.

- Ignoring your estate plan: Not having a current will, advance healthcare directive, or durable power of attorney leaves your financial and medical decisions in the hands of the state if you become incapacitated.

When DIY Isn’t Enough

While daily habits empower you to manage most of your retirement life, certain situations require a professional touch. You should seek guidance from a fiduciary financial planner or a tax professional when:

- You inherit a retirement account, as the IRS rules for inherited IRAs are incredibly complex and subject to strict withdrawal timelines.

- Your income spikes due to selling a home or a large portfolio withdrawal, which could trigger an Income-Related Monthly Adjustment Amount (IRMAA) surcharge on your Medicare Part B and Part D premiums.

- You are trying to qualify for Medicaid to cover long-term care costs. Medicaid requires a strict look-back period for asset transfers, and applying without an elder law attorney can result in painful coverage delays.

Adopting these nine habits will not change your life overnight, but consistency compounds. By staying physically active, keeping a close eye on your cash flow, and proactively managing your taxes and healthcare, you build a fortress around your independence.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.