Retiring on a fixed income forces you to weigh every dollar against the lifestyle you actually want. Finding a destination that balances true affordability with access to top-tier healthcare, vibrant culture, and comfortable weather requires looking beyond famous luxury enclaves. As Social Security and Medicare costs fluctuate—with the 2026 cost-of-living adjustment adding 2.8% while standard Medicare Part B premiums rose to $202.90—stretching your monthly budget in the right location has never been more critical. The ten towns below offer a proven mix of reasonable housing costs, favorable state tax policies, and the daily amenities you need to thrive. Relocating to a carefully chosen mid-sized city allows you to protect your savings without sacrificing your long-term comfort.

Why Your Zip Code Dictates Your Retirement Budget

Where you live directly controls your two largest expenses in retirement: housing and taxes. A move across state lines can instantly increase your take-home pay by eliminating state income taxes on your pensions or Social Security benefits. Conversely, moving to a state with a high sales tax or aggressive property tax reassessments can slowly drain the savings you worked decades to build.

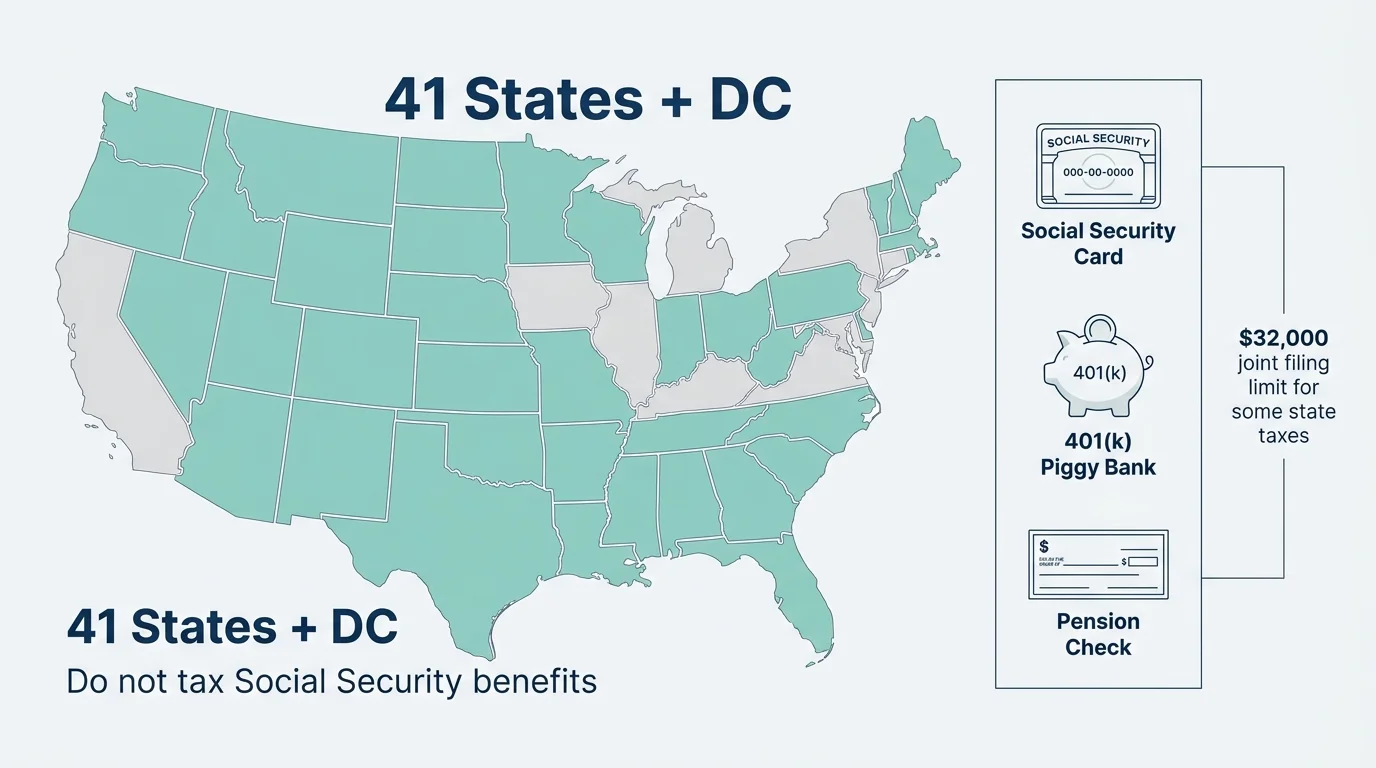

At the federal level, the Internal Revenue Service (IRS) mandates that you must pay taxes on up to 85% of your Social Security benefits if you file a joint return and your combined income exceeds $32,000. However, state taxation varies wildly. Today, 41 states and the District of Columbia do not tax your Social Security benefits. Navigating these local tax codes while simultaneously looking for quality hospitals and a welcoming community requires careful research.

“Retirement is not an age; it’s a financial number.” — Jean Chatzky, Financial Expert

10 Retirement Towns That Actually Balance Cost and Comfort

We evaluated locations across the United States that deliver an exceptional quality of life without demanding a premium price tag. These towns consistently rate highly for their healthcare access, low tax burdens, and active senior communities.

1. Lancaster, Pennsylvania

Nestled in the heart of Pennsylvania Dutch Country, Lancaster consistently ranks as a top retirement destination. It provides a perfect blend of quiet rural landscapes and a thriving, walkable downtown filled with art galleries and farmers’ markets. From a financial perspective, Pennsylvania does not tax retirement income—including Social Security, 401(k) distributions, and pensions—for residents over age 59 and a half. You gain access to excellent regional medical centers while enjoying a cost of living that remains far below nearby East Coast metropolitan hubs.

2. Greenville, South Carolina

Greenville offers a picturesque downtown centered around a stunning waterfall and expansive park system. South Carolina is remarkably friendly to retirees, completely exempting Social Security benefits from state income tax. The state also offers generous income tax deductions for residents 65 and older. With mild winters and a booming culinary scene, Greenville gives you the cultural amenities of a much larger city while keeping housing costs incredibly manageable.

3. Huntsville, Alabama

Often referred to as the “Rocket City” due to its rich aerospace history, Huntsville boasts a highly educated population and a robust local economy. Alabama imposes very low property taxes and exempts all Social Security benefits and defined-benefit pensions from state income taxation. You will find top-rated medical facilities here, heavily supported by the city’s growing tech and engineering sectors, making it an intellectually stimulating and deeply affordable place to settle down.

4. Roanoke, Virginia

If you dream of retiring in the mountains but cannot stomach the price tags of resort towns, Roanoke delivers. Surrounded by the Blue Ridge Mountains, this city provides endless outdoor recreation, scenic drives, and a vibrant arts culture. Virginia does not tax Social Security benefits, and the state offers an age-based tax deduction that helps lower your overall burden. Healthcare is anchored by the Carilion Clinic system, ensuring you have access to specialists without traveling to a major coastal city.

5. Fort Wayne, Indiana

Fort Wayne frequently appears on lists of the most affordable places to live in the United States. Your housing dollar stretches remarkably far here, allowing you to purchase a comfortable, upgraded home for a fraction of the national average. Indiana has implemented tax policies that favor seniors, including the phase-out of taxes on military pensions. The city features a renowned minor league baseball stadium, miles of connected riverfront trails, and a highly accessible local healthcare network.

6. Pensacola, Florida

Florida remains a retirement staple because it levies zero state income tax on all retirement income, including pensions, IRA withdrawals, and Social Security. However, traditional South Florida destinations have become prohibitively expensive. Pensacola, located in the Florida Panhandle, offers the pristine white-sand beaches and tax benefits of the Sunshine State at a much more reasonable price point. The presence of a large military community also means the area is well-equipped with amenities and discounts for veterans.

7. Tucson, Arizona

For those who need a dry, warm climate to soothe joint pain, Tucson provides an excellent alternative to the sprawling and expensive Phoenix metro area. Arizona completely exempts Social Security benefits from state income tax. Tucson surrounds you with breathtaking desert landscapes, world-class golf courses, and the vibrant culture of a major university town. The University of Arizona ensures the region is staffed with top-tier medical professionals and cutting-edge healthcare facilities.

8. Winston-Salem, North Carolina

Winston-Salem marries historical charm with modern medical innovation. Home to Wake Forest University and its massive medical network, you will never have to worry about finding specialized healthcare. North Carolina does not tax Social Security benefits, and its relatively moderate flat income tax rate makes financial planning predictable. The city experiences all four seasons mildly, allowing you to enjoy a traditional autumn and spring without enduring brutal winter blizzards.

9. Augusta, Georgia

Famous for hosting the Masters golf tournament, Augusta is a paradise for active retirees. Georgia is exceptionally tax-friendly for seniors, offering a massive retirement income exclusion of up to $65,000 per person for residents aged 65 and older. This means a married couple can potentially exclude up to $130,000 of retirement income from state taxes. Between the low cost of housing, warm weather, and excellent regional hospitals, Augusta easily balances budget constraints with luxury living.

10. Chattanooga, Tennessee

Known as the “Scenic City,” Chattanooga sits along the Tennessee River and is surrounded by mountains. Tennessee is one of the rare states that imposes zero income tax on all retirement income, meaning your Social Security and 401(k) withdrawals remain entirely yours. Furthermore, Chattanooga was the first U.S. city to roll out citywide gigabit internet, making it perfect for retirees who want to stay highly connected or manage remote investments. The downtown is highly walkable, clean, and filled with free community events.

State Tax Rules to Watch

Before packing your boxes, you must analyze how your new home state will tax your specific mix of income. A state with no income tax might compensate by charging heavy sales or property taxes. Use this quick comparison of four popular retirement states to understand the varying approaches to taxation.

| State | Social Security Tax | Pension & IRA Tax | General Financial Environment |

|---|---|---|---|

| Pennsylvania | Fully Exempt | Fully Exempt (for residents 59.5+) | High local property taxes in some counties; excellent income tax rules for retirees. |

| Florida | Fully Exempt | No State Income Tax | Zero income tax, but watch out for rising homeowner’s insurance premiums and high property taxes. |

| Tennessee | Fully Exempt | No State Income Tax | Zero income tax, but the state relies heavily on a high baseline sales tax (typically 7% plus local). |

| Illinois | Fully Exempt | Fully Exempt | Retirement income is safe from the state’s flat tax, though property taxes remain among the highest nationally. |

Costly Errors to Sidestep

Even the most meticulously planned relocation can drain your finances if you fall into common transition traps. Protect your nest egg by avoiding these major mistakes:

- Assuming your Medicare Advantage Plan travels with you: Original Medicare (Part A and Part B) travels with you anywhere in the U.S. However, Medicare Advantage (Part C) and Part D prescription plans are tethered to specific zip codes. If you move out of your plan’s service area, you must switch plans, which could alter your network of covered doctors and prescription copays. Always check plan availability at Medicare.gov before moving.

- Ignoring local property tax reassessment laws: In some states, a home’s taxable value is locked in for the previous owner but resets to the current market value the moment you buy it. This can result in a property tax bill that is double or triple what the real estate listing advertised.

- Moving solely for tax benefits: Saving $3,000 a year in state taxes is not worth it if you have to spend $5,000 a year traveling back home to see your grandchildren or if the local healthcare system cannot manage your specific medical conditions. Prioritize your support network and health above pure tax avoidance.

When DIY Isn’t Enough

While you can research property values and basic tax rates on your own, certain relocation scenarios demand professional guidance to prevent severe financial penalties. Consider hiring a fee-only fiduciary financial advisor and a specialized tax professional if you face the following situations:

- You plan to split your time between two states: Establishing legal domicile determines which state gets to tax your income. If you spend six months in New York and six months in Florida, both states may try to claim you as a resident. A professional can help you structure your time, voting registration, and property ownership to definitively establish your tax home.

- You are selling a highly appreciated primary residence: If you have lived in a high-cost area for decades, selling your home to downsize might trigger significant capital gains taxes. A tax advisor can help you properly utilize the Section 121 exclusion (which shields up to $500,000 of profit for married couples) and plan for any overflow.

- You are navigating Medicaid planning across state lines: If you anticipate needing long-term care, understand that Medicaid eligibility rules and look-back periods vary by state. Moving to a new state can disrupt your timeline and eligibility if not planned flawlessly.

Frequently Asked Questions

Which states impose zero income tax on all retirement income?

Currently, nine states impose no income tax on any retirement income, including pensions, 401(k) distributions, IRA withdrawals, and Social Security benefits. These states are Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Additionally, states like Illinois and Pennsylvania have an income tax but explicitly exempt retirement income.

How does a cost-of-living adjustment (COLA) affect my taxes?

When Social Security implements a COLA—such as the 2.8% increase for 2026—your monthly benefit increases. If this higher benefit pushes your combined income over the IRS thresholds ($25,000 for individuals; $32,000 for married filing jointly), a larger percentage of your Social Security benefits may become subject to federal income tax.

Does my standard Medicare Part B premium change based on where I live?

No. The standard Medicare Part B premium, which is $202.90 for 2026, is a federal baseline and does not change based on your zip code. However, higher-income earners are subject to the Income-Related Monthly Adjustment Amount (IRMAA), which increases your premium based on your tax returns from two years prior.

Finding the perfect retirement town requires balancing the spreadsheet with your soul. Your ideal destination should make you feel financially secure while providing the community, healthcare, and hobbies that make your golden years truly rewarding. Take the time to rent in a prospective city for a month during its worst weather season. If you still love the town when the weather is poor, and the math works in your favor, you have found your new home.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources such as the Social Security Administration, the IRS, and Eldercare Locator before making major relocation or financial decisions.

Last updated: May 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.

Leave a Reply