Waiting to claim Social Security until age 70 guarantees the highest possible monthly check, adding up to 24% to your standard retirement benefit. This strategy maximizes your lifetime income and builds a durable shield against inflation, but the decision involves much more than a larger bank deposit. Behind the scenes, claiming at 70 triggers a chain reaction that directly impacts your taxes, Medicare premiums, and spousal survivor benefits. By delaying your claim, you capture valuable delayed retirement credits and establish a higher baseline for all future cost-of-living adjustments. Understanding the financial mechanics of a delayed claim allows you to optimize your retirement timeline and keep more of the wealth you spent decades building.

The Math Behind the Age 70 Payraise

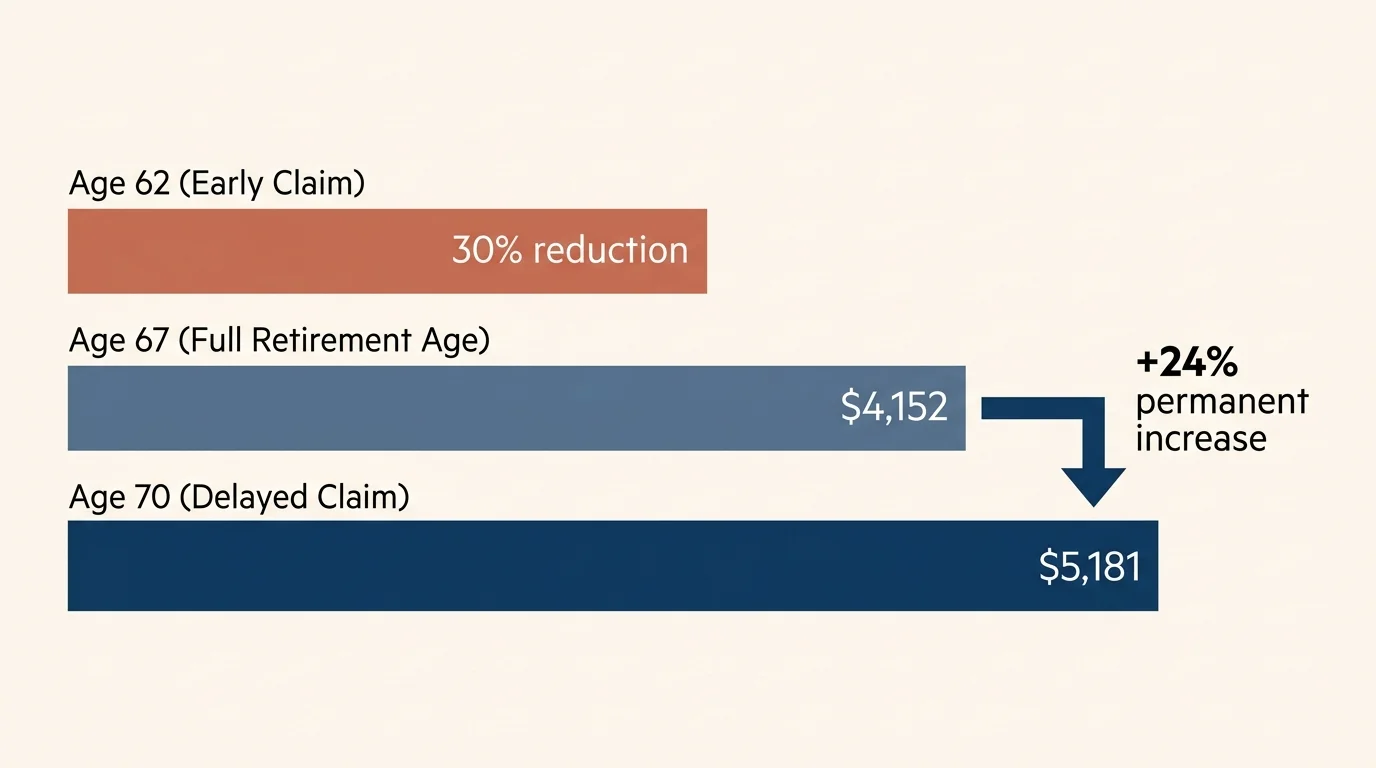

Your Full Retirement Age (FRA) is the exact point when you are entitled to 100% of the benefit you earned during your working years. For anyone born in 1960 or later, that age is officially 67. You are legally allowed to claim as early as age 62, but doing so permanently slashes your monthly check by up to 30%. However, if you have the financial flexibility to wait past your FRA, the Social Security Administration (SSA) rewards you generously with Delayed Retirement Credits.

For every single year you delay claiming your benefit between your FRA and age 70, your payout increases by a guaranteed 8%. If you wait the full three years from 67 to 70, you lock in a 24% permanent payraise. To put the real dollars into perspective, the maximum Social Security benefit at full retirement age in 2026 is $4,152 per month. If a high-earning worker waits until age 70, that maximum benefit leaps to $5,181 per month. Over a year, that translates to over $12,000 in additional guaranteed income.

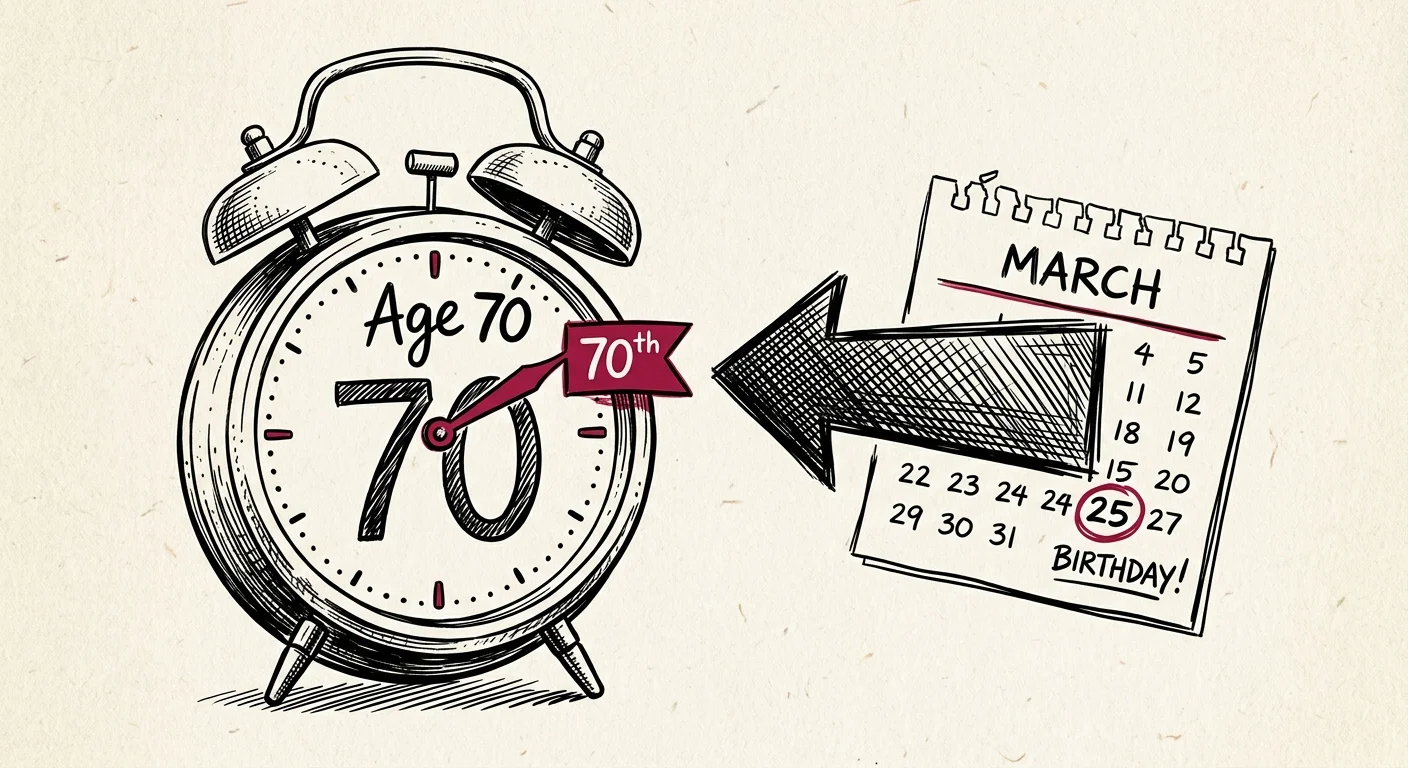

Once you reach age 70, these delayed retirement credits stop accumulating. There is zero financial incentive to delay your claim past your 70th birthday.

“Social Security is the best annuity money can buy. It pays you until you die, and it keeps up with inflation.” — Jean Chatzky, Financial Editor and Retirement Expert

How the 2026 COLA Interacts With a Delayed Claim

A common and dangerous misconception is that you forfeit the annual Cost-of-Living Adjustment (COLA) if you choose to delay your claim. This is entirely false. Even while you wait to file, the SSA automatically applies every declared COLA directly to your underlying Primary Insurance Amount.

When you finally initiate your claim at 70, your benefit fully reflects years of compounded inflation protection. For instance, the Social Security COLA for 2026 is 2.8%. If you are currently in your delay period, that 2.8% increase is permanently baked into your baseline calculation. Once your 8% delayed retirement credits are stacked on top of that inflation-adjusted baseline, the compounding effect creates a fortress around your purchasing power.

The Hidden Tax Implications of a Larger Check

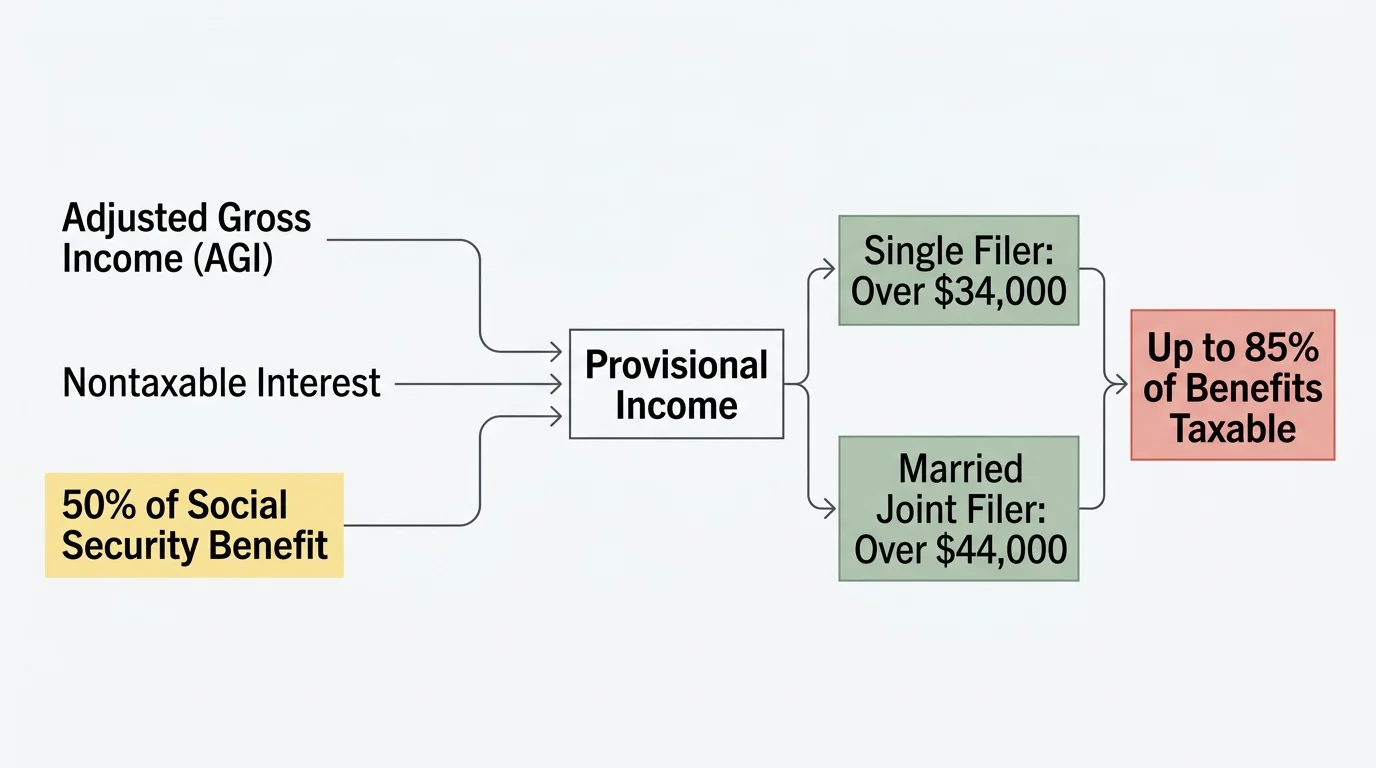

A substantially larger Social Security check sounds flawless on the surface; however, it can quietly alter your entire tax situation. Depending on your total income, up to 85% of your Social Security benefits can be subject to federal income taxes.

The IRS determines this through a formula called “provisional income.” To calculate your provisional income, you add your Adjusted Gross Income (AGI), any nontaxable interest (like municipal bonds), and exactly 50% of your Social Security benefit. Because your age 70 check is 24% larger, half of that benefit is a larger number, which adds a heavier weight to the IRS formula. If your provisional income exceeds $34,000 as a single filer or $44,000 as a married couple filing jointly, up to 85% of your benefits become taxable.

Fortunately, the current tax code provides standard deductions to help shield this income. For 2026, the baseline standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. Additionally, taxpayers who are 65 and older receive an extra $2,050 (single) or $1,650 per qualifying spouse (joint). Thanks to recent legislation, eligible seniors age 65 and older can also claim a new temporary $6,000 senior bonus deduction in 2026. Proactive planning—such as drawing down taxable retirement accounts before age 70—can help you manage your provisional income before your maximized Social Security checks begin.

Navigating Medicare Premiums and IRMAA Surcharges

Once you are enrolled in Medicare, your Part B premiums are automatically deducted from your Social Security payments. For 2026, the standard Medicare Part B premium is $202.90 per month. If you choose to delay Social Security until 70 but enroll in Medicare at 65, you simply pay your Medicare premiums directly to the government until your benefits begin.

The real financial surprise hits high-income retirees through the Income-Related Monthly Adjustment Amount (IRMAA). Medicare reviews your tax return from exactly two years prior to determine your current premium. In 2026, if your modified adjusted gross income from 2024 exceeded $109,000 for single filers or $218,000 for joint filers, you are penalized with an IRMAA surcharge on top of the standard premium.

Because your age 70 Social Security check is maximized, and because you will likely be taking Required Minimum Distributions (RMDs) from your traditional 401(k) or IRA around the exact same time, your combined income can easily cross an IRMAA cliff. Crossing the threshold by just one single dollar triggers the full surcharge for that tier.

| 2024 MAGI (Single Filer) | 2024 MAGI (Joint Filer) | 2026 Total Part B Premium |

|---|---|---|

| $109,000 or less | $218,000 or less | $202.90 (Standard) |

| $109,001 to $137,000 | $218,001 to $274,000 | $284.10 (Tier 1 Surcharge) |

| $137,001 to $171,000 | $274,001 to $342,000 | $405.80 (Tier 2 Surcharge) |

The Impact on Spousal and Survivor Benefits

When you wait until 70 to claim, you are making a strategic decision that deeply protects your household—especially your spouse. Social Security offers two distinct types of family benefits, and delaying impacts them very differently.

Spousal Benefits: Delaying past your Full Retirement Age does not increase the spousal benefit while you are both alive. A spousal benefit maxes out at exactly 50% of your FRA amount. Waiting until 70 gives you a 24% boost on your own record, but your spouse’s benefit remains capped at the FRA level.

Survivor Benefits: This is where the age 70 strategy proves its immense worth. If you pass away before your spouse, your surviving spouse is legally entitled to 100% of the exact benefit you were receiving at the time of your death. By delaying to 70, you permanently lock in that 24% payraise for your surviving spouse. When one spouse dies, the household loses the smaller of the two Social Security checks, making that maximized survivor benefit crucial for paying ongoing living expenses.

How to Fund the Gap: The Bridge Strategy

If you retire at 62 or 65 but want to delay Social Security until 70, you must find a way to pay your bills during the “gap years.” This is where a bridge strategy becomes essential.

A bridge strategy involves purposefully drawing down your personal savings and investment accounts to replace the income Social Security would have provided. By spending down your traditional IRAs or 401(k)s during these early retirement years, you accomplish two massive financial goals. First, you allow your Social Security benefit to grow by 8% annually. Second, you actively reduce the balances in your tax-deferred accounts, which permanently shrinks your future Required Minimum Distributions (RMDs) and lowers your lifetime tax burden.

What Happens if You Work While Delaying?

Many active seniors choose to continue working through their late 60s. If you do, delaying your claim works completely to your advantage.

Because you are past your Full Retirement Age, the dreaded Social Security earnings test disappears completely. You can earn any amount of money from your job, and the SSA will not withhold a single penny of your benefits. Furthermore, your continued high earnings might actually increase your underlying base benefit. Social Security calculates your check based on your 35 highest-earning years. If your current salary replaces a low-earning year from early in your career, the SSA will automatically recalculate and adjust your benefit upward.

It is also worth noting that the Social Security payroll tax is capped. For 2026, the maximum taxable wage base is $184,500. Any income you earn from your job above that specific threshold is completely exempt from the 6.2% Social Security payroll tax.

“Someone’s sitting in the shade today because someone planted a tree a long time ago.” — Warren Buffett, Chairman and CEO of Berkshire Hathaway

Common Mistakes to Avoid

Waiting until 70 is mathematically superior for maximizing lifetime wealth, but poor execution can easily sabotage the strategy. Avoid these frequent missteps:

- Draining your portfolio recklessly: To delay claiming, you need bridge income to cover living expenses between retirement and age 70. If you drain your accounts too rapidly without a withdrawal sequence plan, you risk triggering massive tax bills and running out of money.

- Forgetting your Medicare enrollment: You do not have to claim Social Security to get Medicare. You must actively enroll in Medicare at age 65 (unless you have qualifying active employer coverage). Missing your initial enrollment window results in lifetime late-enrollment financial penalties.

- Ignoring life expectancy realities: It generally takes until your early 80s to “break even” on the money you passed up by not claiming at age 62. If you have severe health issues or a family history of short life expectancy, claiming earlier is likely the better financial move.

- Waiting past age 70: Delayed retirement credits stop exactly at age 70. There is no financial benefit to waiting until 70 and a half or 71. Apply for your benefits approximately three to four months before your 70th birthday.

Finding the Right Advisor

Deciding exactly when to claim involves coordinating your taxes, investment withdrawals, and health insurance. A specialized fiduciary financial advisor can help you navigate this complex web. Consider seeking professional guidance if:

- You hold significant assets in tax-deferred accounts and need a calculated withdrawal strategy to avoid Medicare IRMAA surcharges in the future.

- You are planning Roth IRA conversions during your gap years (between ages 60 and 70) to lower your future RMDs.

- You and your spouse have vastly different earnings histories and need to coordinate a maximized survivor benefit timeline.

- You intend to sell a business or primary residence, which could create a massive one-time tax spike that interferes with your retirement brackets.

Frequently Asked Questions

Does delaying my claim to age 70 increase my spousal benefit?

No. If your spouse is claiming a benefit based on your work record, their maximum spousal benefit is capped at 50% of your Full Retirement Age (FRA) amount. Your decision to wait until 70 increases your own benefit and the eventual survivor benefit, but it does not increase the spousal benefit.

What happens to my benefits if I die before reaching age 70?

If you pass away before claiming, your surviving spouse is entitled to survivor benefits based on the amount you were legally entitled to receive at the time of your death. The delayed retirement credits you earned up until your passing will be fully applied to their survivor check.

Do my benefits automatically start at age 70, or do I need to apply?

Social Security benefits do not start automatically unless you are already receiving disability benefits. You must actively submit an application to the Social Security Administration. It is highly recommended to apply three to four months before the month you want your benefits to begin.

Can I change my mind if I delay but suddenly need the money?

Yes. If you are past your Full Retirement Age and decide to claim before age 70, you can request up to six months of retroactive benefits. However, taking a retroactive lump sum will permanently reset your ongoing monthly benefit to the amount you were entitled to six months ago.

To further understand your individual benefits and Medicare responsibilities, you can visit the Social Security Administration (SSA), explore health coverage rules at Medicare.gov, or review the most current tax brackets at the Internal Revenue Service (IRS). For comprehensive aging resources, the National Council on Aging (NCOA) provides excellent guidance for navigating senior finances.

Optimizing your Social Security strategy is one of the most vital financial decisions of your retirement. By looking at the complete picture—taxes, Medicare, and spousal protection—you can confidently secure the wealth you have spent a lifetime building.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.

Leave a Reply