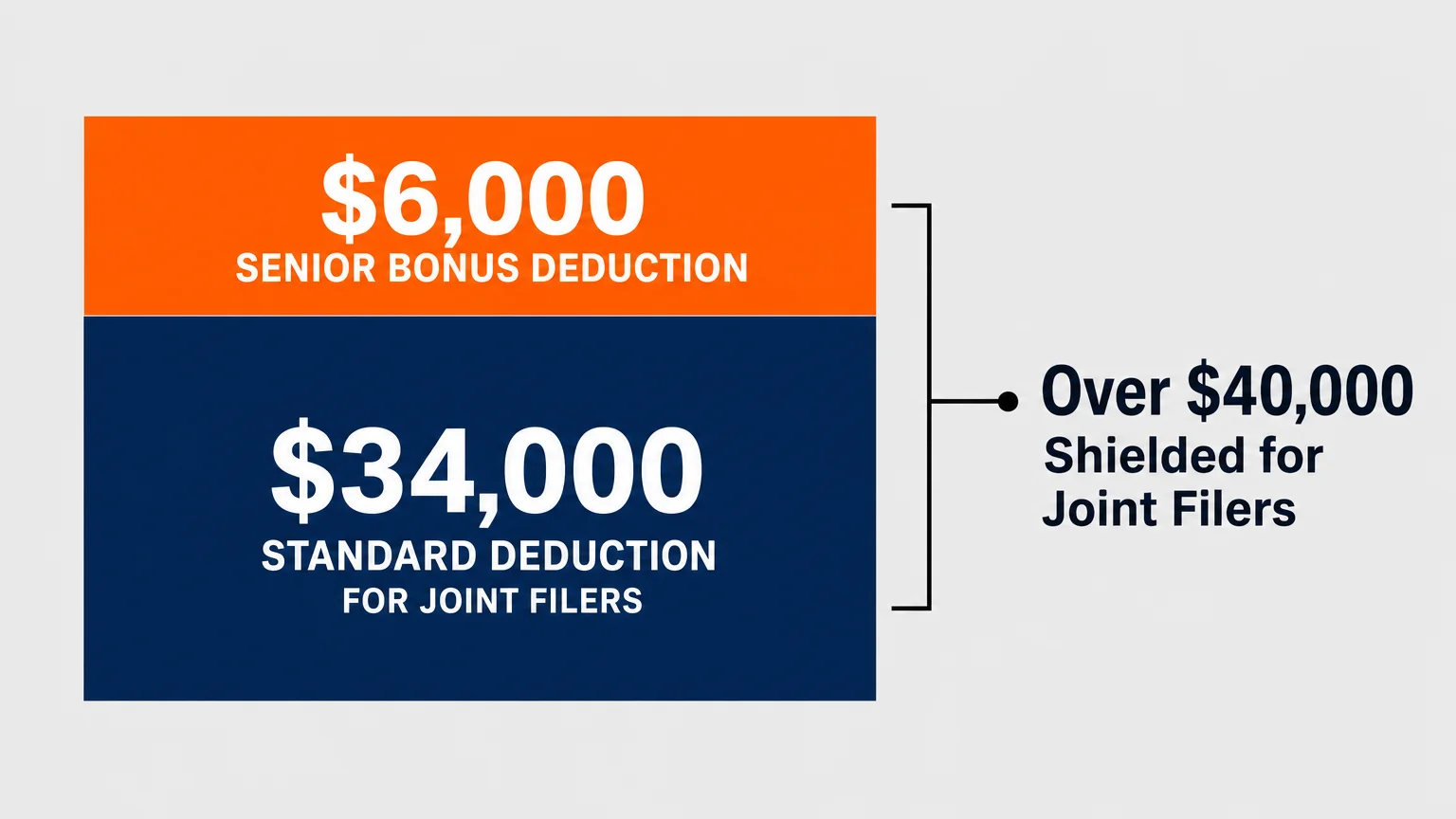

For the 2026 tax year, seniors have a major opportunity to lower their tax bills thanks to a newly expanded standard deduction and a unique bonus deduction. If you are 65 or older, the IRS now allows you to claim a $6,000 Senior Bonus Deduction on top of your regular standard deduction—even if you do not itemize your expenses. This change means a married couple filing jointly could shelter more than $40,000 of income from federal taxes this year. Understanding how these adjustments interact with your Social Security benefits, Medicare premiums, and retirement account withdrawals is essential for keeping more of your hard-earned money. Navigating these rules properly can dramatically reduce what you owe by April.

The Baseline: 2026 Standard Deduction Amounts

Before diving into the special breaks reserved exclusively for older adults, you need to understand the foundation of your federal tax return. The standard deduction is a flat, predetermined amount that the Internal Revenue Service (IRS) allows you to subtract from your income before applying any income tax rates. It effectively acts as a zero-percent tax bracket. Any income that falls below your standard deduction is completely shielded from federal taxation.

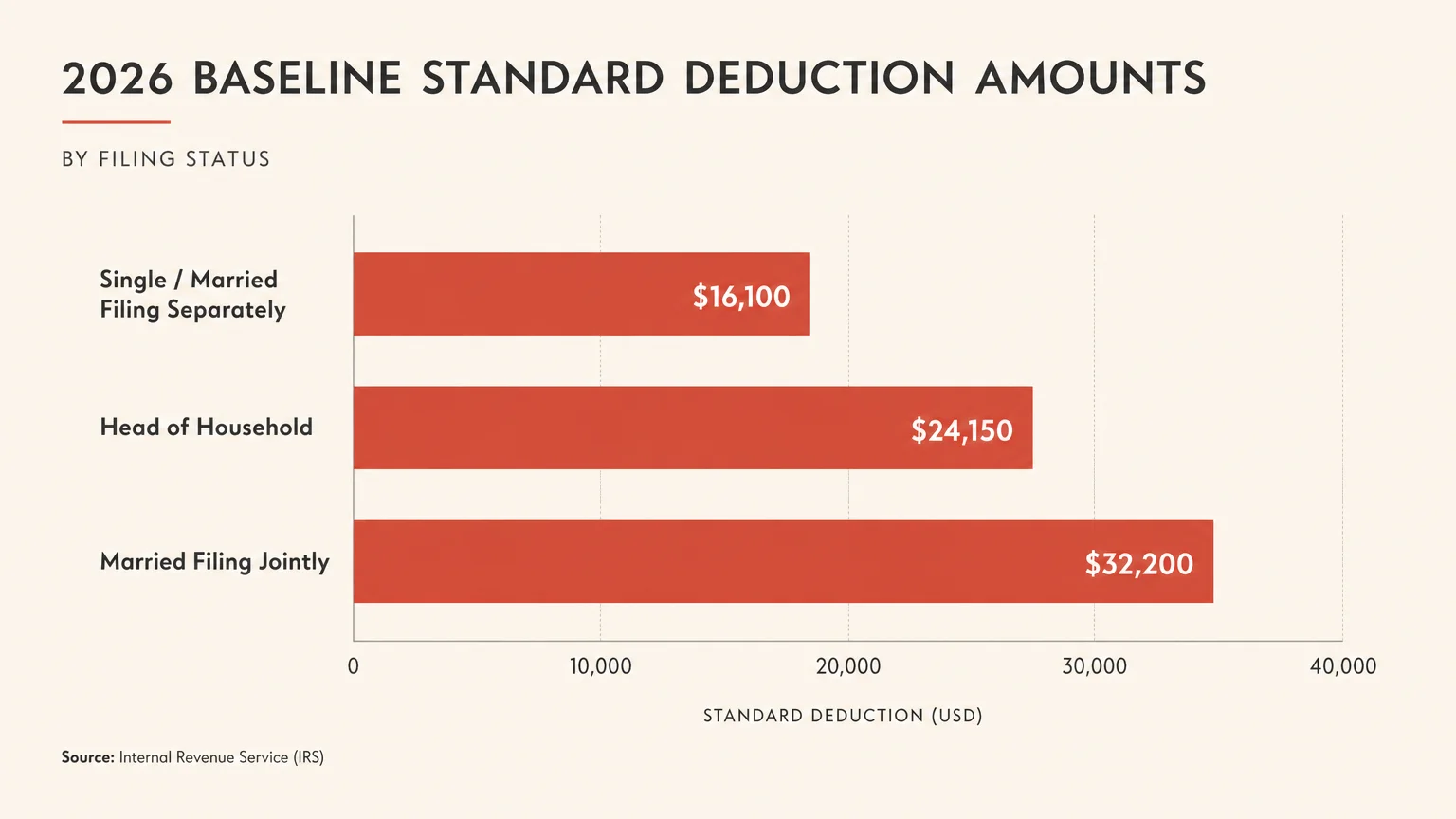

Due to inflation adjustments, the baseline standard deduction amounts have increased significantly for the 2026 tax year. For single filers and married individuals filing separately, the base standard deduction is $16,100. If you are married and filing jointly, your base deduction climbs to $32,200. Heads of household will see a base standard deduction of $24,150. These generous starting points mean that the vast majority of taxpayers will simply take the standard deduction rather than deal with the hassle of tracking every charitable receipt, medical bill, and property tax payment.

However, these baseline numbers only tell part of the story. If you or your spouse are 65 or older by the end of the tax year, the IRS layers additional deductions on top of these base figures. To truly optimize your retirement tax strategy, you must stack these benefits correctly.

The Traditional Age 65 and Older Deduction

For decades, the tax code has provided a little extra help to older Americans through an additional standard deduction. This traditional benefit applies automatically as long as you check the correct box indicating your age on your Form 1040. If you are blind, you receive another identical deduction on top of the age-based one.

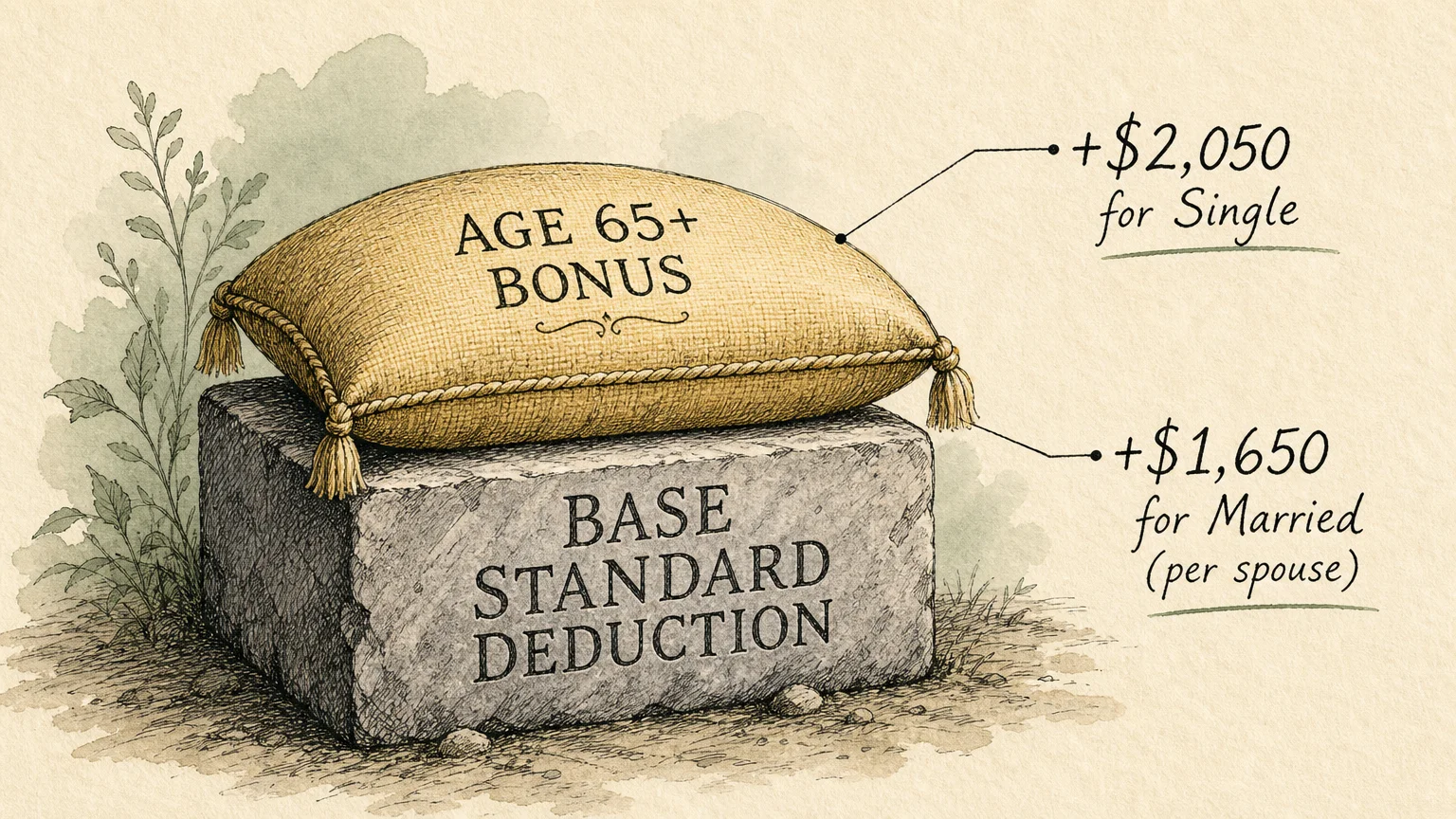

For 2026, the traditional age 65-plus standard deduction adds a substantial cushion to your tax return. If you file as Single or Head of Household, you get an extra $2,050 added to your base standard deduction. If you are Married Filing Jointly, the IRS grants an extra $1,650 for each qualifying spouse. This means if both you and your spouse are 65 or older, you add $3,300 to your combined standard deduction right out of the gate.

To put this into perspective, let us look at the math for a single 66-year-old retiree. They start with the $16,100 base deduction and add the $2,050 traditional senior deduction. Before any newly introduced tax laws apply, this individual already enjoys $18,150 of tax-free income. If their primary source of income is a modest pension alongside Social Security, they might owe absolutely nothing to the federal government.

The Game Changer: The New $6,000 Senior Bonus Deduction

While the traditional deductions are helpful, the most significant shift for retiree taxes in 2026 comes from recent legislative updates. Under the newly implemented tax packages, older adults gain access to a powerful new tool: a $6,000 Senior Bonus Deduction. This is an entirely separate line item from the traditional age-based deduction discussed above.

This deduction is uniquely flexible. Historically, taxpayers had to choose between taking the standard deduction or itemizing their expenses; they could never do both. The new $6,000 Senior Bonus Deduction breaks this rule. It is available to you whether you take the massive 2026 standard deduction or choose to itemize your heavy medical and local tax expenses. The IRS grants this $6,000 deduction per qualifying taxpayer, meaning a married couple where both spouses are 65 or older can claim an astonishing $12,000 bonus deduction.

When you combine all three layers—the base standard deduction, the traditional senior extra, and the new Senior Bonus—the resulting tax shield is remarkable. A married couple filing jointly with both spouses over 65 can shelter up to $47,500 of their income from federal taxes ($32,200 base + $3,300 traditional extra + $12,000 bonus). For many middle-income retirees, this effectively eliminates their federal income tax liability entirely, allowing them to keep more money in their pockets to cover rising costs of living.

“Your retirement savings are only as good as the amount you actually get to keep after taxes.” — Ed Slott, CPA and Retirement Tax Expert

Navigating the Senior Bonus Phase-Out Rules

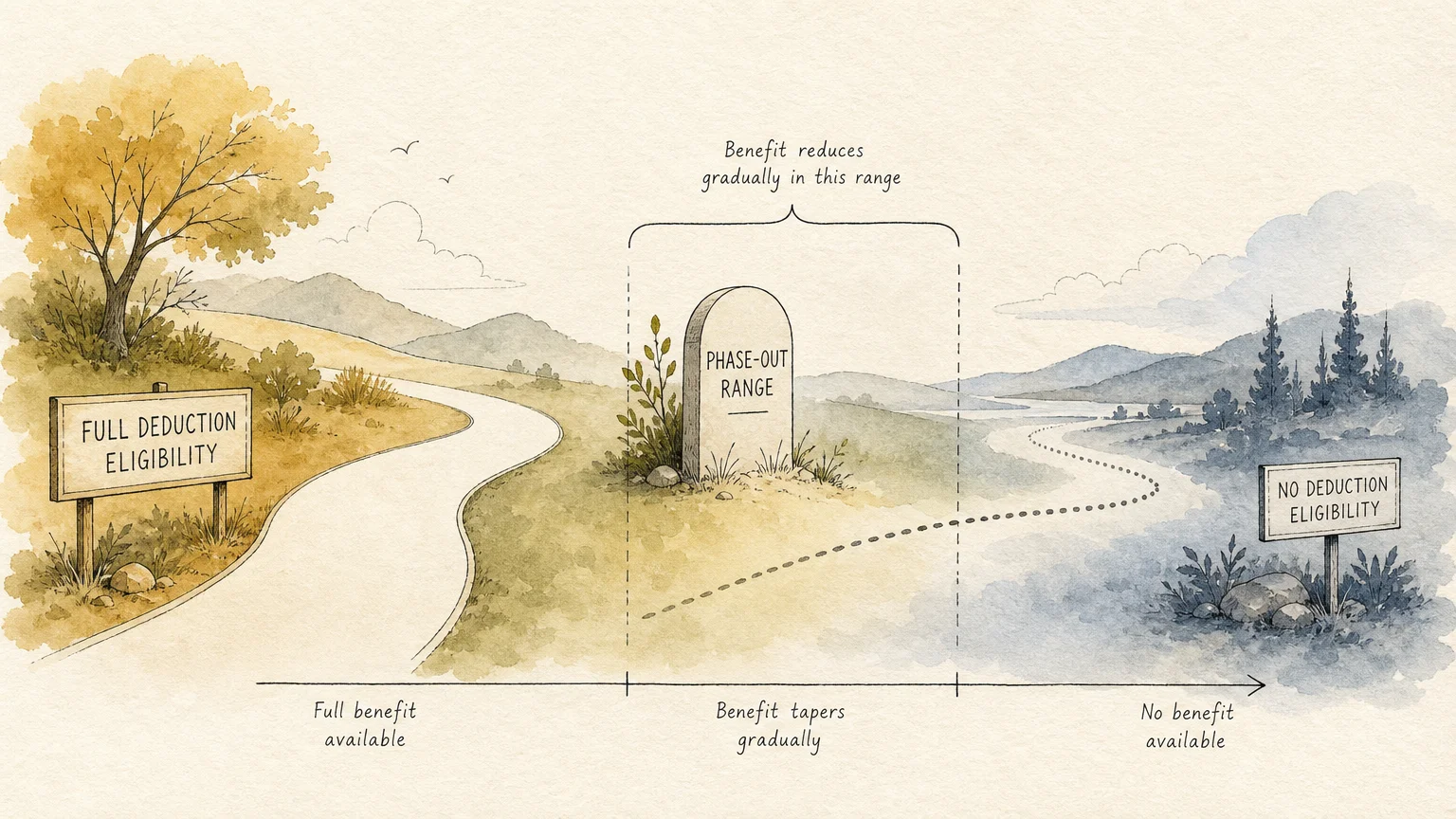

As with many generous tax provisions, the new $6,000 Senior Bonus Deduction is targeted primarily at low- and middle-income retirees. If you have substantial income from pensions, required minimum distributions (RMDs), or part-time consulting work, you need to pay close attention to the phase-out thresholds. The government slowly reduces your bonus deduction if your Adjusted Gross Income (AGI) crosses a certain line.

For 2026, the phase-out begins when your AGI reaches $75,000 as a single filer, or $150,000 for married couples filing jointly. The deduction phases down at a rate of 6 percent for every dollar you earn over the limit. This means the benefit completely disappears once a single filer reaches $175,000 in income, or $250,000 for a married couple.

Let us walk through a practical example to clarify how this math works in real life. Suppose you are a single filer aged 67, and your total AGI for the year is $80,000. Because your income is $5,000 over the $75,000 limit, you must calculate a 6 percent reduction on that excess amount. Six percent of $5,000 is $300. You subtract that $300 from your $6,000 bonus, leaving you with a final Senior Bonus Deduction of $5,700. You still receive the vast majority of the benefit; it simply requires an extra step of math on your tax return. Managing your retirement withdrawals strategically to stay under these phase-out limits is now a critical part of year-end tax planning.

How Deductions Impact Social Security and Medicare

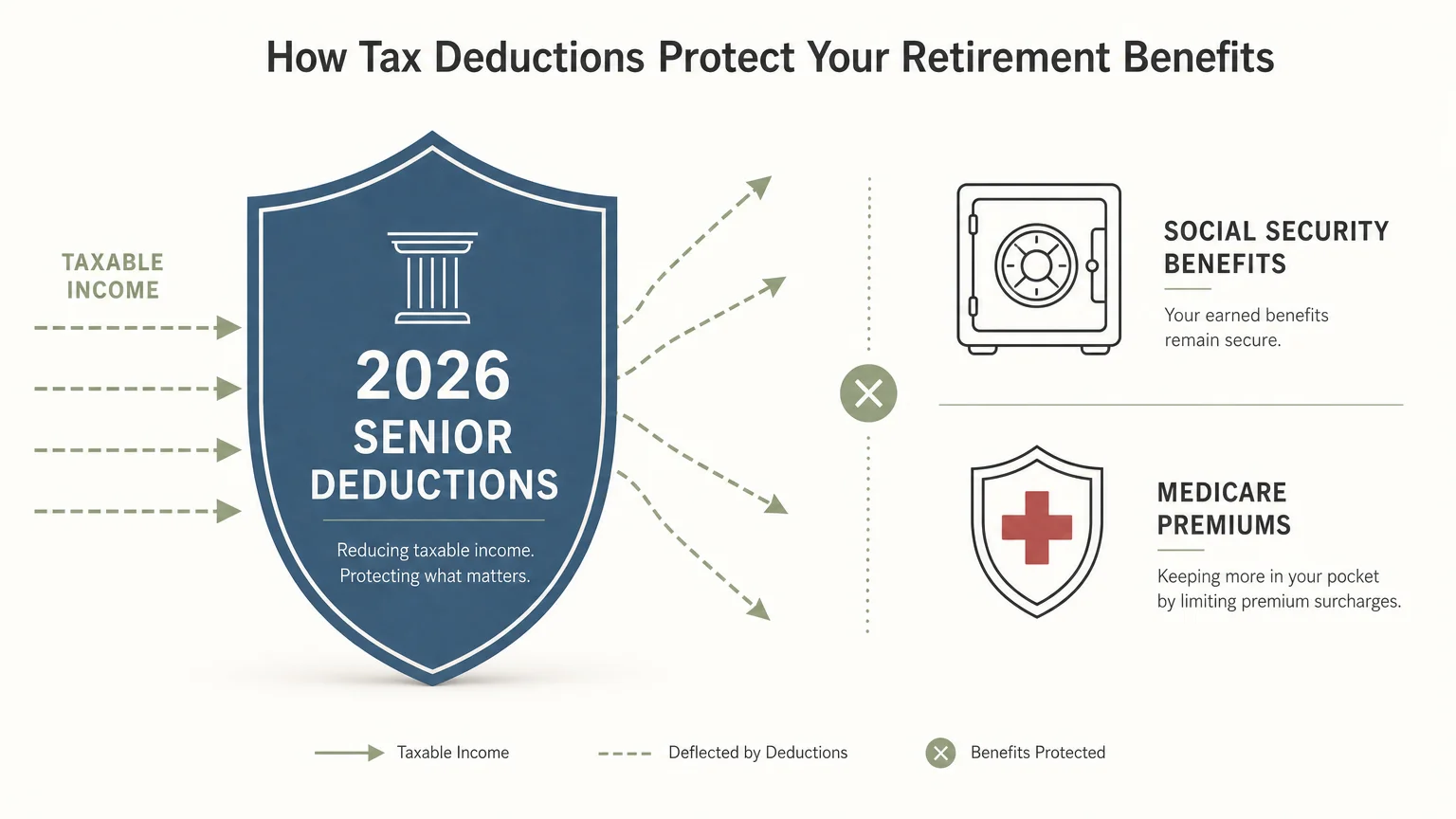

When planning your taxes, it is crucial to understand how your deductions interact with your government benefits. The Social Security Administration (SSA) announced a 2.8 percent Cost-of-Living Adjustment (COLA) for 2026. While a larger monthly check is always welcome, this extra income can push your Adjusted Gross Income higher, potentially exposing more of your Social Security benefits to taxation.

This is where understanding the mechanics of the tax code becomes essential. Your standard and bonus deductions reduce your taxable income—the final number used to calculate the tax you owe. However, these deductions do not reduce your provisional income, which is the formula the IRS uses to determine if your Social Security benefits are taxable in the first place. Similarly, these deductions do not lower your Modified Adjusted Gross Income (MAGI) when calculating Medicare premiums.

For 2026, the standard Medicare Part B premium is set at $202.90 per month. If your MAGI from two years prior exceeds certain thresholds, you will be hit with an Income-Related Monthly Adjustment Amount (IRMAA) surcharge. Taking a massive $47,500 standard deduction will beautifully wipe out your federal income tax, but it will not save you from a Medicare premium surcharge if your gross income remains high. You must manage your gross income proactively—perhaps by utilizing Qualified Charitable Distributions (QCDs) from your IRA—if you want to keep your Medicare costs down.

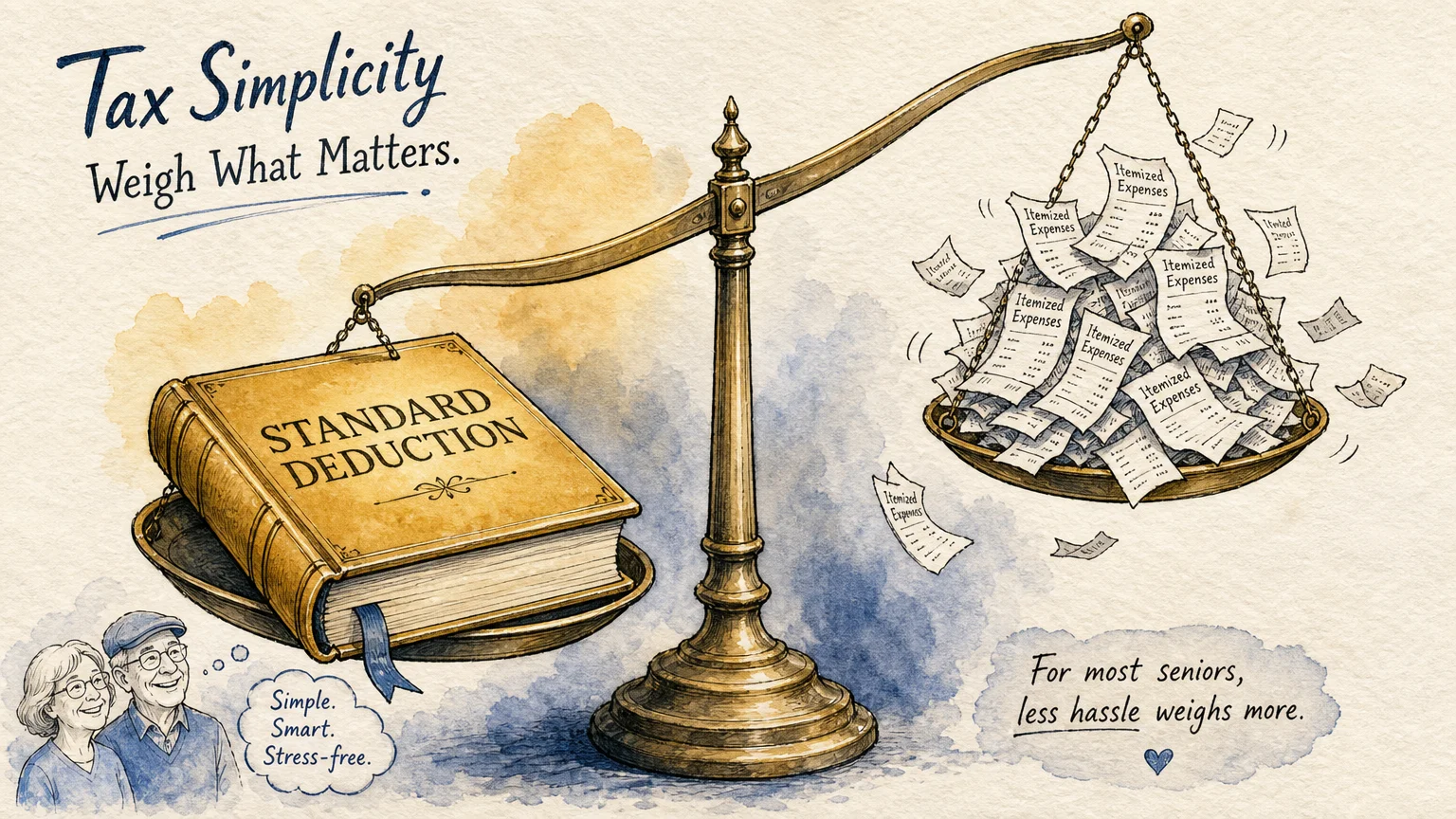

Itemizing vs. Taking the Standard Deduction in 2026

Given the sheer size of the combined standard deductions for seniors in 2026, itemizing expenses will make sense for very few older adults. Itemizing requires you to forgo the base standard deduction and the traditional senior deduction in favor of listing out specific deductible expenses. To win the math game, your individual expenses must add up to more than your guaranteed standard deduction.

For 2026, the State and Local Tax (SALT) deduction cap has been raised to $40,400, providing some relief for seniors living in high-tax states. You can also deduct medical expenses that exceed 7.5 percent of your Adjusted Gross Income. However, you must carefully weigh whether gathering all those receipts is worth the effort.

The table below illustrates the maximum potential deductions available in 2026 without the need to itemize a single expense.

| Deduction Type | Single Filer (Age 65+) | Married Filing Jointly (Both 65+) |

|---|---|---|

| Base 2026 Standard Deduction | $16,100 | $32,200 |

| Traditional Age 65+ Deduction | $2,050 | $3,300 ($1,650 per spouse) |

| New Senior Bonus Deduction | $6,000 (Subject to phase-out) | $12,000 (Subject to phase-out) |

| Total Potential Deduction | $24,150 | $47,500 |

If your total itemizable expenses—including state taxes, mortgage interest, and heavy medical bills—do not exceed the bolded numbers at the bottom of the table, taking the standard route is both financially superior and vastly simpler. Remember, the $6,000 Senior Bonus Deduction is unique because you can claim it even if you do choose to itemize, making it a win-win scenario.

Pitfalls to Watch For

Even with clear rules, tax season is fraught with opportunities for errors that can cost you thousands. Avoid these common mistakes when claiming your 2026 senior tax deductions:

- Forgetting to Check the Age 65 Box: Tax software usually handles this automatically based on your birthdate, but if you file paper forms or use an inexperienced preparer, skipping the simple checkbox on Form 1040 means you forfeit the traditional $2,050 or $1,650 age-based deduction entirely.

- Confusing AGI with Taxable Income: Many seniors wrongly assume that their massive standard deduction will protect them from Medicare IRMAA surcharges or the phase-out limits of the new Senior Bonus Deduction. Those limits are based on Adjusted Gross Income (AGI), which is calculated before your standard deduction is applied.

- Ignoring State Income Tax Differences: Federal tax laws and state tax laws do not always align. Your state might not recognize the new federal $6,000 Senior Bonus Deduction, and their state-level standard deduction might be quite low. You may still need to keep medical and property tax receipts for your state return even if you take the federal standard deduction.

- Failing to Adjust Tax Withholdings: If your total deduction limit jumps to $47,500 in 2026, you might be having far too much tax withheld from your pension or IRA distributions. Adjust your W-4P or W-4R forms so you can keep your money throughout the year instead of giving the IRS an interest-free loan until refund season.

Getting Expert Help

While the standard deduction simplifies tax filing for many, specific life events create complex tax webs that require professional intervention. Consider hiring a fiduciary financial planner or a Certified Public Accountant (CPA) if you fall into one of the following scenarios:

- You Have Large Required Minimum Distributions (RMDs): If you are 73 or older and hold significant funds in traditional IRAs or 401(k)s, your mandatory withdrawals can inflate your AGI. A professional can help you execute Qualified Charitable Distributions (QCDs) to keep your income below the $75,000 or $150,000 phase-out thresholds.

- You Are Navigating a Spouse’s Passing: In the year your spouse passes away, you are allowed to file as Married Filing Jointly, capturing the full $47,500 senior deduction combination. However, the following year, you typically revert to Single filing status, slashing your deductions and narrowing your tax brackets. This transition, often called the “widow’s penalty,” requires proactive tax planning.

- You Are Selling a Primary Residence: Downsizing is common in retirement. While federal law exempts up to $250,000 (single) or $500,000 (joint) of profit on the sale of a primary residence, any gain beyond that hits your AGI directly. A massive one-time influx of cash can trigger Medicare surcharges and wipe out your income-sensitive deductions for the year.

Frequently Asked Questions

What is the maximum standard deduction for a single person over 65 in 2026?

Assuming your income falls below the $75,000 phase-out limit, a single filer aged 65 or older can claim a total deduction of up to $24,150. This figure combines the $16,100 base standard deduction, the $2,050 traditional age 65-plus deduction, and the new $6,000 Senior Bonus Deduction.

Can I claim the new $6,000 Senior Bonus Deduction if I itemize my taxes?

Yes. Unlike the standard deduction, the new $6,000 Senior Bonus Deduction (introduced by recent legislative changes) applies whether you choose to itemize your deductions or take the standard route. It acts as an additional above-the-line reduction to your taxable income.

Does a larger standard deduction reduce my Medicare Part B premium?

No. Standard and itemized deductions lower your final taxable income, but Medicare bases its premium surcharges (IRMAA) on your Modified Adjusted Gross Income (MAGI). Deductions are subtracted after your MAGI is calculated, meaning a high standard deduction will not protect you from increased healthcare premiums.

Are Social Security benefits counted toward the $75,000 income limit for the new deduction phase-out?

Yes. Up to 85 percent of your Social Security benefits can be subject to federal income tax. The taxable portion of your Social Security is included in your Adjusted Gross Income, which is the exact figure used to determine if you hit the phase-out thresholds for the Senior Bonus Deduction.

Do I get an extra deduction if I am legally blind?

Yes. The IRS provides an additional standard deduction for blindness that mirrors the age 65 deduction. In 2026, if you are single, 65 or older, and legally blind, you receive two $2,050 additions to your base standard deduction, significantly increasing your tax-free income threshold.

Maximizing your 2026 tax deductions requires nothing more than understanding the rules and ensuring your tax software or preparer applies them correctly. Take the time to estimate your Adjusted Gross Income early in the year so you can make informed decisions about your retirement account withdrawals. By leveraging the expanded base standard deduction, the traditional age bonus, and the newly available Senior Bonus Deduction, you can build a highly efficient tax strategy that preserves your wealth. The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.