The newly announced 2026 Medicare Part B premium of $202.90 per month is rapidly wiping out this year’s 2.8% Social Security cost-of-living adjustment. To protect your monthly cash flow, you need practical strategies to offset these rising healthcare expenses immediately. The $17.90 monthly increase in Part B costs and the new $283 annual deductible feel daunting, but you have options to fight back. By strategically adjusting your coverage, challenging unwarranted income-related surcharges, and utilizing federal assistance programs, you can reclaim hundreds of dollars annually. Let’s explore four actionable budget hacks designed to help you navigate the 2026 Medicare landscape and keep your hard-earned retirement money exactly where it belongs: securely in your own pocket.

The Real Math Behind Your 2026 Social Security Check

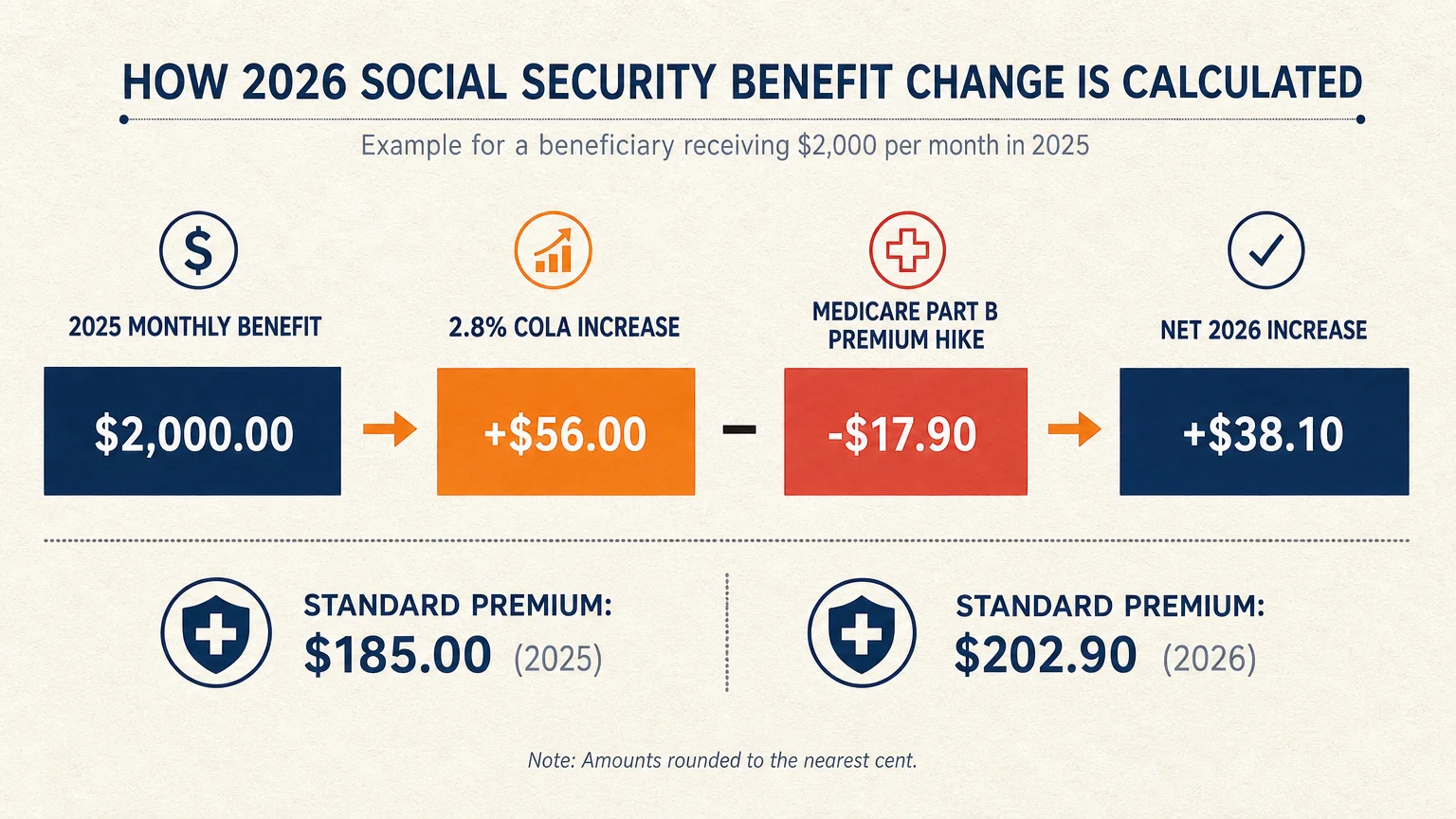

Each fall, retirees eagerly await the official Social Security cost-of-living adjustment (COLA). For 2026, the Social Security Administration (SSA) set the COLA at 2.8%. While any increase provides relief, the reality of your net check tells a much different story once your Medicare premiums take their cut.

Most seniors have their Medicare Part B premiums deducted directly from their monthly Social Security benefits. Let’s break down the actual math. If your monthly benefit was $2,000 in 2025, a 2.8% COLA adds roughly $56 to your gross check. However, the standard Medicare Part B premium rose from $185.00 in 2025 to $202.90 in 2026. That single $17.90 increase instantly swallows nearly a third of your hard-earned raise before it ever reaches your bank account.

You cannot change the federally mandated standard premium, but you absolutely can control how you manage your overall healthcare and tax expenses. Using a few strategic adjustments, you can stop the financial bleeding and keep your retirement budget balanced.

1. Appeal the Medicare IRMAA Surcharge If Your Income Dropped

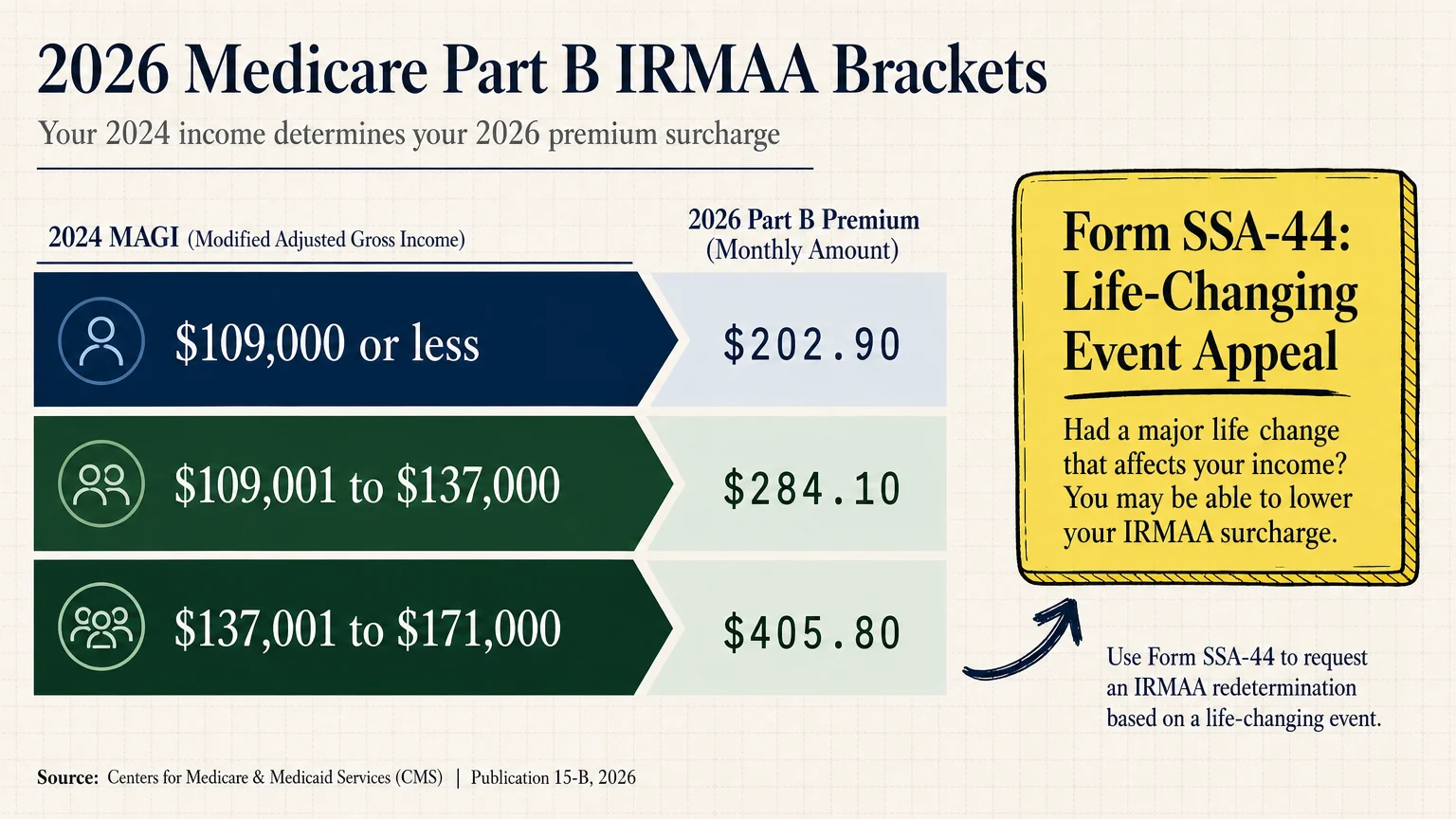

The $202.90 base premium is just the starting point; high earners face significant penalties. The Income-Related Monthly Adjustment Amount (IRMAA) is an extra charge added to your Part B and Part D premiums if your income exceeds certain limits. The government bases your 2026 premiums on your tax return from two years ago—specifically, your 2024 Modified Adjusted Gross Income (MAGI).

For 2026, if your 2024 MAGI was higher than $109,000 as an individual filer or $218,000 as a married couple filing jointly, you will pay an IRMAA surcharge. Depending on your exact bracket, your Part B premium could jump from $202.90 to anywhere between $284.10 and $689.80 per month.

| Individual Tax Return (MAGI) | Joint Tax Return (MAGI) | 2026 Monthly Part B Premium |

|---|---|---|

| $109,000 or less | $218,000 or less | $202.90 (Standard Rate) |

| $109,001 to $137,000 | $218,001 to $274,000 | $284.10 |

| $137,001 to $171,000 | $274,001 to $342,000 | $405.80 |

Here is the budget hack: If your income has dropped since 2024—perhaps due to retirement, a reduction in work hours, or the death of a spouse—you do not have to accept this surcharge. You can request a new initial determination by filing Form SSA-44 with the Social Security Administration.

To win your appeal, you must prove that your income decreased due to a recognized “life-changing event.” The SSA accepts eight specific events:

- Marriage, divorce, or annulment.

- Death of your spouse.

- Work stoppage or reduction in work hours.

- Loss of income-producing property due to a disaster or other event beyond your control.

- Loss of pension income.

- An employer settlement payment from a closed or bankrupt company.

Filing this one piece of paperwork with your updated income estimates can instantly erase thousands of dollars in annual surcharges.

2. Tap Into Medicare Savings Programs and Extra Help

Many seniors struggle to pay their monthly premiums but mistakenly assume their income is too high to qualify for assistance. The reality is that federal and state governments offer robust programs designed specifically to defray the costs of Medicare.

The first lifeline is a Medicare Savings Program (MSP). Administered by your state’s Medicaid office, an MSP can completely cover your $202.90 Part B premium. Depending on your state’s specific income and asset limits, you might qualify for the Qualified Medicare Beneficiary (QMB) program, the Specified Low-Income Medicare Beneficiary (SLMB) program, or the Qualifying Individual (QI) program. By shifting the burden of the premium back to the state, you instantly add over $2,400 back to your yearly budget.

The second major resource is the Extra Help program, which lowers the costs of Medicare Part D prescription drug coverage. Thanks to recent expansions under the Inflation Reduction Act, far more seniors now qualify for full Extra Help benefits. If you qualify, this program pays your Part D premiums, your deductibles, and lowers your copayments for medications. You can apply for Extra Help directly through the Social Security Administration website.

3. Rethink Your Part D or Medicare Advantage Plan

Your health needs change from year to year; your Medicare coverage should adapt accordingly. Insurance companies routinely alter their plan structures, meaning the policy that saved you money in 2025 could be your biggest financial drain in 2026. Premium costs, provider networks, and drug formularies all shift annually.

“Putting your retirement healthcare on autopilot is a guaranteed way to overpay. Shopping your Medicare coverage annually is one of the highest-paying hourly jobs a retiree can take on.” — Jean Chatzky, Financial Editor and Author

During the Medicare Annual Enrollment Period (October 15 to December 7), you have the opportunity to switch your standalone Part D drug plan or your Medicare Advantage (Part C) plan. Use the official Medicare Plan Finder tool to input your current prescription drugs and preferred pharmacies. The tool automatically calculates the exact out-of-pocket costs for every plan available in your zip code.

When reviewing plans, pay close attention to the new $2,000 out-of-pocket cap on prescription medications. Because insurance companies are now responsible for more of your drug costs once you hit that cap, many have raised their monthly premiums or shifted drugs to more expensive tiers. Take an hour to comparison shop—it is entirely possible to find a plan with a lower premium that still covers all your essential medications.

4. Maximize Senior Tax Deductions and HSA Funds

Strategic tax planning provides another excellent way to offset your rising healthcare costs. If you have a Health Savings Account (HSA) left over from your working years, you can use those pre-tax dollars to pay your Medicare premiums. While you cannot contribute to an HSA once you are enrolled in Medicare, you are legally allowed to spend down your existing balance tax-free to cover Part B, Part D, and Medicare Advantage premiums. (Note: You cannot use HSA funds to pay for Medicare Supplement/Medigap premiums.)

Additionally, take full advantage of the enhanced standard deduction for seniors. In 2026, the basic standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. On top of that base amount, taxpayers aged 65 and older receive an extra standard deduction. For 2026, this additional amount is $2,050 for single filers and $1,650 per qualifying spouse for joint filers.

This means a married couple, both over age 65, can shield $35,500 of their income from federal taxes entirely. If your out-of-pocket healthcare costs—including your Medicare premiums, dental work, and vision care—are exceptionally high, calculate whether itemizing your taxes makes sense. The IRS allows you to deduct qualified medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI). Shrinking your tax bill directly increases the amount of cash you have available to cover higher Medicare premiums.

When to Consult a Professional

Managing healthcare costs and retirement income often requires a highly personalized approach. Consider consulting a fee-only fiduciary financial advisor or a licensed Medicare broker if you encounter these specific situations:

- Experiencing a major life event: If you recently retired, sold a business, or lost a spouse, a professional can help you navigate the resulting tax implications and file your IRMAA appeal correctly.

- Choosing between Medigap and Medicare Advantage: A licensed, independent Medicare broker can assess your specific medical needs and preferred doctors to help you weigh the long-term costs and restrictions of both options.

- Planning Roth conversions: Converting traditional IRA funds to a Roth IRA creates taxable income that can inadvertently trigger Medicare premium surcharges. A tax professional can calculate the exact amount to convert without crossing an IRMAA threshold.

What Can Go Wrong: Costly Medicare Mistakes

Even with a solid budget, simple oversights can trigger lasting financial penalties. Avoid these common traps that routinely cost seniors thousands of dollars:

- Ignoring the Annual Notice of Change (ANOC): Medicare Advantage and Part D plans mail this document every September. Failing to review it means missing critical updates about premium hikes, new copays, or dropped medications for the upcoming year.

- Missing your Initial Enrollment Period: If you delay signing up for Part B or Part D without having creditable employer coverage, you will face permanent late enrollment penalties that increase your monthly premiums for the rest of your life.

- Assuming Medigap covers prescriptions: Medicare Supplement (Medigap) plans cover deductibles and copays for hospital and doctor visits, but they do not cover prescription drugs. You must purchase a standalone Part D plan to avoid out-of-pocket pharmacy disasters.

- Assuming your doctor is still in-network: Medicare Advantage networks change frequently. Always verify directly with your doctor’s billing office that they will continue to accept your specific plan in 2026.

Frequently Asked Questions

Can my Social Security check decrease if Medicare premiums go up?

Thanks to a rule called the hold-harmless provision, your net Social Security benefit typically will not decrease if the standard Medicare Part B premium increase is larger than your annual COLA. Under this provision, your premium increase is capped at the exact dollar amount of your COLA. However, this protection does not shield you from IRMAA surcharges or Part D premium hikes.

What is the Medicare Part B deductible for 2026?

The annual Medicare Part B deductible for 2026 is $283. You must pay this amount out-of-pocket before Original Medicare begins covering 80% of your approved medical services.

Are Medicare Part B premiums tax-deductible?

Yes. Medicare Part B, Part D, and Medigap premiums are considered deductible medical expenses by the IRS. You can deduct them if you choose to itemize your taxes and your total qualified medical expenses exceed 7.5% of your adjusted gross income for the year.

Rising healthcare expenses are an unavoidable reality of retirement, but you do not have to absorb every cost passively. By utilizing these strategies—appealing unfair surcharges, applying for available assistance, evaluating your coverage annually, and optimizing your tax deductions—you take active control of your financial well-being.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.