Many retirees dream of escaping city traffic for the quiet charm of a secluded mountain village or a desert arts enclave. But choosing a retirement destination strictly for its scenery can mask hidden financial and practical challenges that become apparent only after you unpack. Relocating to a heavily isolated town often means facing steep travel expenses for medical care, limited in-network Medicare providers, and higher daily living costs due to supply chain distances. Before you sell your home and head for the hills, you need to look beyond the postcards. We rounded up eight picturesque small towns that look perfect on paper but might leave you feeling stranded, disconnected, or financially strained in your later years.

The Hidden Financial Costs of Moving Too Far Out

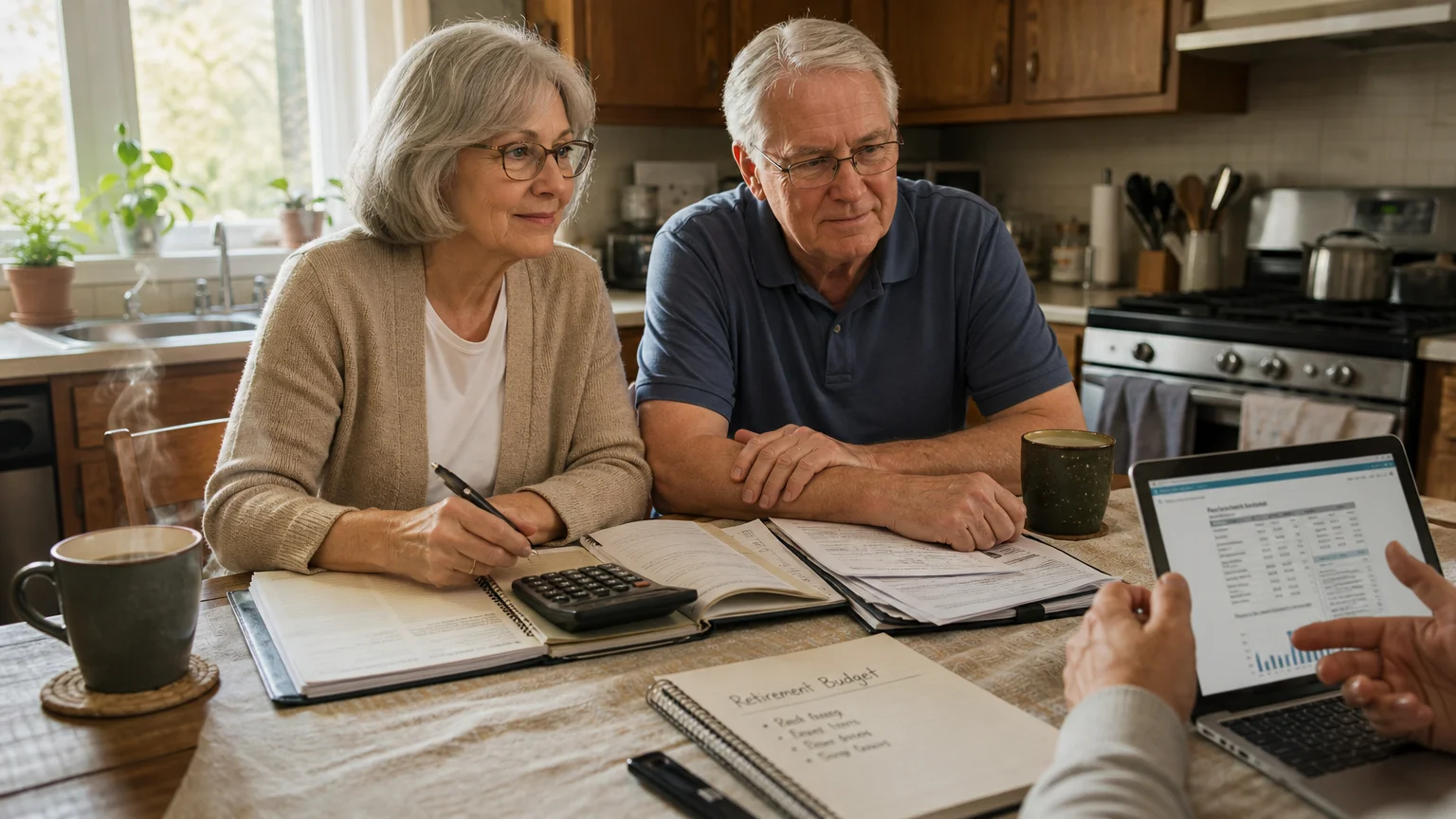

Retirement relocation involves much more than comparing median home prices. When you move to a remote town, the lack of local infrastructure shifts many hidden costs directly onto your personal budget. You might save on property taxes or escape the stress of city traffic, but you will likely pay significantly more for daily essentials and specialized services.

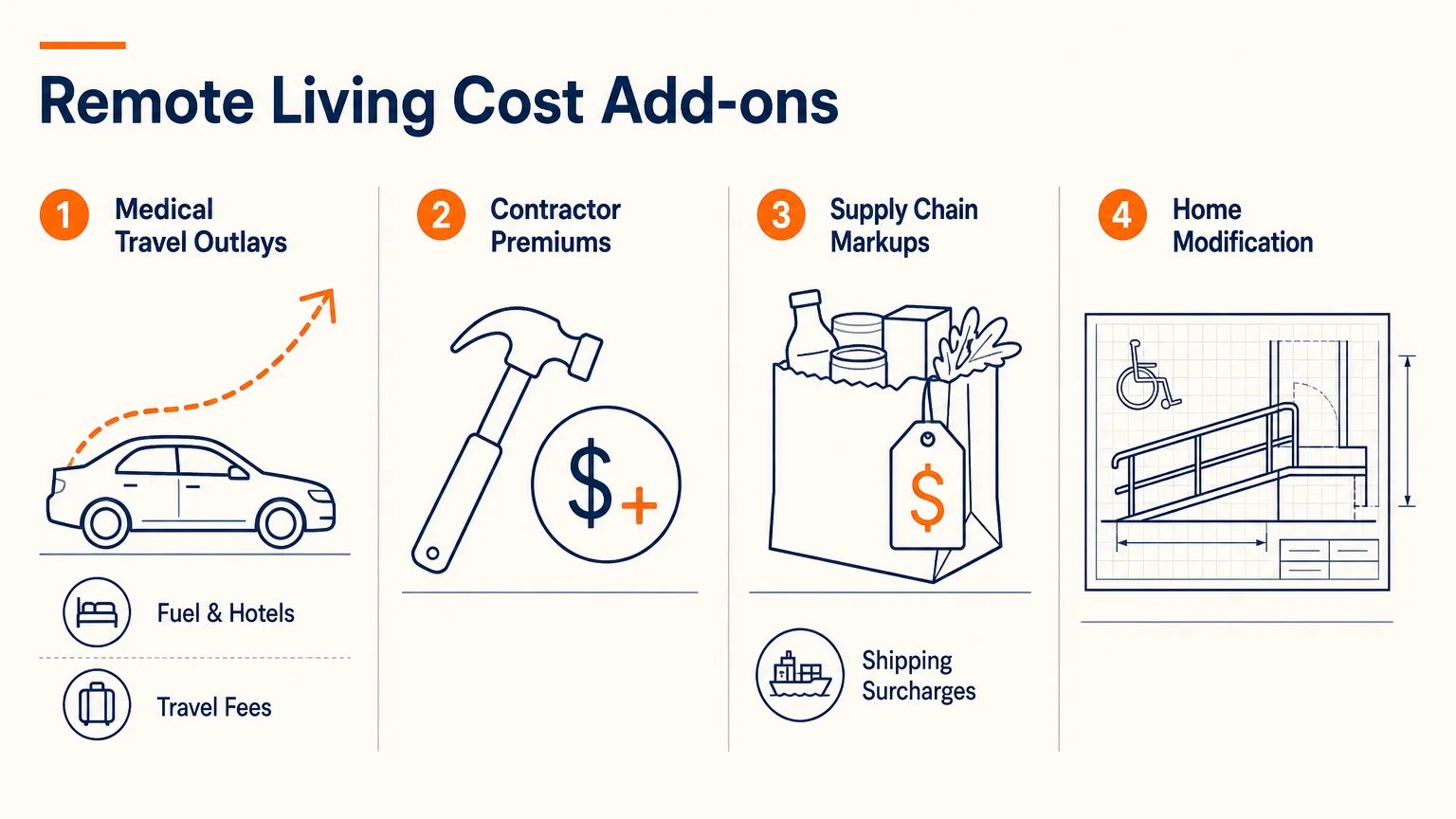

Expect to face these specific financial hurdles in isolated communities:

- Medical Travel Outlays: Driving two hours to see a cardiologist means spending heavily on gas, vehicle wear, and overnight hotel stays for early morning procedures.

- Contractor Premiums: If your roof leaks or your furnace fails, securing a plumber or electrician in a town of 2,000 people often requires paying steep travel fees for a professional to drive in from the nearest major city.

- Supply Chain Markups: Remote grocery stores and hardware shops lack the volume discounts of large retailers. You will pay premium prices for everyday goods, and shipping heavy items to a rural address often incurs extra freight surcharges.

- Home Modification Expenses: Retrofitting historic or mountain homes with wheelchair ramps, walk-in tubs, or stairlifts is notoriously expensive in areas with limited specialized labor. According to the National Council on Aging (NCOA), modifying a multi-story home for aging in place can easily cost tens of thousands of dollars.

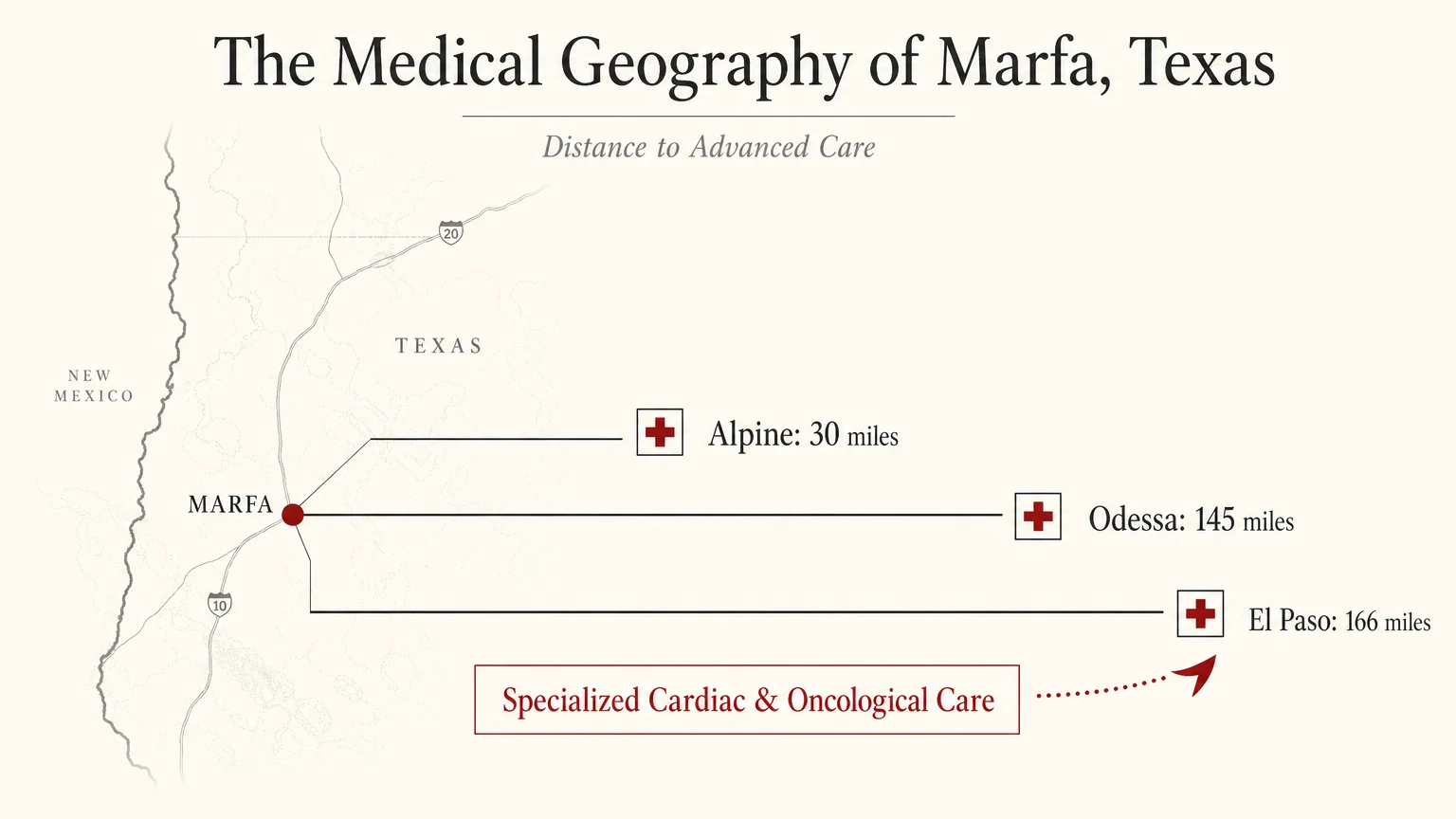

1. Marfa, Texas

Marfa is famous worldwide for its minimalist art installations, historic architecture, and vast, starry desert skies. For a creative retiree, it feels like an intellectual oasis. Texas also boasts no state income tax, meaning your pension withdrawals and Social Security benefits stay entirely in your pocket.

However, the financial trade-off comes in the form of extreme isolation. The nearest full-service hospital is in Alpine, about 30 miles away. For serious medical emergencies or specialized cardiac and oncological care, residents often must travel to Odessa (145 miles) or El Paso (nearly 166 miles). If you require frequent specialist visits, the out-of-pocket travel costs and the physical toll of long highway drives across the desert will quickly erode any tax savings you gained by moving to Texas.

2. Forks, Washington

Surrounded by the lush Olympic National Forest and famous as the setting for the Twilight series, Forks offers stunning coastal scenery and a relatively low cost of living compared to the booming Seattle metropolitan area. Washington is another tax-friendly state that does not levy a state income tax, making it highly attractive for budget-conscious seniors.

The primary drawbacks are healthcare access and harsh weather conditions. Forks Community Hospital is a critical access facility; it is equipped for basic medical needs and emergencies but lacks extensive specialized departments. Seeing a specialist usually requires a winding, three-and-a-half-hour drive to Seattle. Additionally, the region receives massive amounts of annual rainfall. The constant dampness accelerates wear and tear on roofs, siding, and home foundations, forcing you to budget significantly more for ongoing property maintenance.

3. Ely, Minnesota

Nestled near the spectacular Boundary Waters Canoe Area Wilderness, Ely is a paradise for seniors who love fishing, canoeing, and pristine wilderness. The housing market is generally affordable, and the small-town community is tightly knit and supportive.

Financially, Ely presents two major challenges. First, as of 2026, Minnesota is one of only eight states that still taxes Social Security benefits. While generous exemptions exist if your adjusted gross income falls below certain thresholds, higher-income retirees will face a tax hit. If your monthly Social Security benefit is $2,000, state taxes can take a noticeable bite out of your annual income. Second, the true cost of Ely lies in its brutal, isolating winters. Heating an older home through months of sub-zero temperatures requires a massive utility budget. When heavy snow restricts mobility, accessing major medical facilities requires a two-hour drive to Duluth, which can become dangerous or entirely impossible during winter storms.

4. Eureka Springs, Arkansas

Eureka Springs boasts beautifully preserved Victorian architecture nestled tightly into the rolling Ozark Mountains. Arkansas is highly tax-friendly for retirees, fully exempting Social Security benefits and offering deductions for other types of retirement income.

The town’s historic charm is also its biggest practical liability. Eureka Springs is built directly onto steep, winding hillsides, and many homes require navigating multiple flights of outdoor stairs just to reach the front door. As your mobility naturally declines with age, walking to town or retrofitting these historic, multi-level homes for accessibility becomes prohibitively expensive. Furthermore, if you develop complex health conditions, you face a long drive through the mountains to reach comprehensive medical networks in Fayetteville or Bentonville.

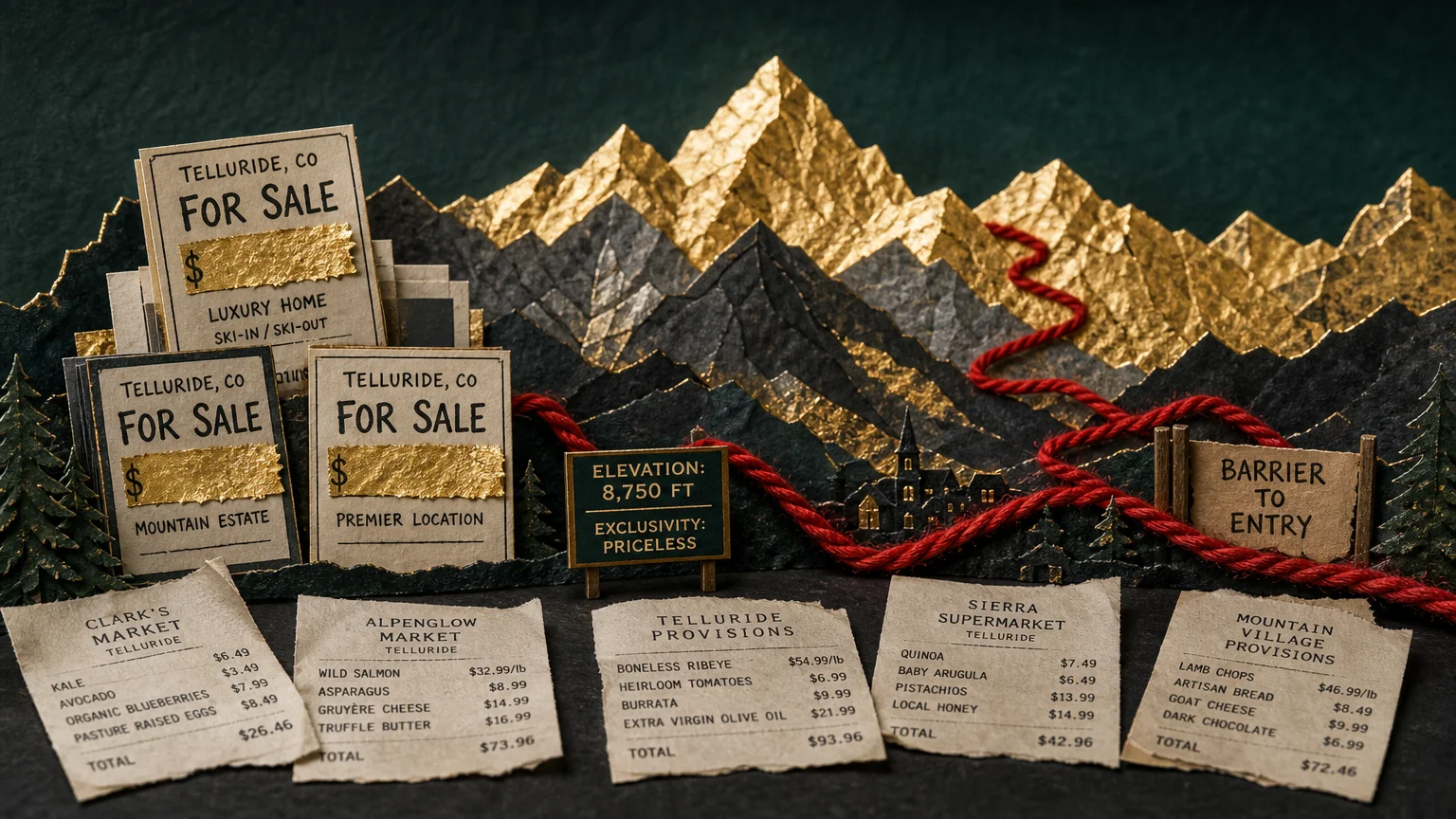

5. Telluride, Colorado

Telluride offers world-class skiing, vibrant summer festivals, and breathtaking alpine views. For the 2026 tax year, Colorado offers a generous full exemption on state taxes for Social Security benefits if you are 65 or older, creating a highly favorable tax environment.

The downside is the astronomical cost of living and the severe physical toll of the mountain environment. Telluride sits at an elevation of 8,750 feet. The thin air places heavy, continuous stress on aging cardiovascular and respiratory systems. Many seniors who retire here are forced to relocate a second time when their health changes. Moving twice eats into your wealth rapidly. For example, selling a home and moving twice in a decade means paying real estate commissions of 5 to 6 percent twice—a process that can easily drain $50,000 to $100,000 from your nest egg. Furthermore, the nearest major medical hubs are hours away in Grand Junction or Montrose.

6. Bisbee, Arizona

Located in southern Arizona near the Mexican border, Bisbee is a quirky, historic former mining town with a vibrant arts community. Arizona is a massively popular retirement destination because it does not tax Social Security benefits, and property taxes are generally reasonable compared to coastal states.

Like Eureka Springs, Bisbee is built directly into the steep sides of a canyon. The town is famous for its outdoor staircases—a feature celebrated in local fitness events but punishing for seniors with joint pain or arthritis. Many of the historic homes lack modern insulation and central air conditioning, leading to exorbitant cooling costs during the intense desert summers. When you need specialized healthcare, you must commit to a nearly two-hour drive to Tucson.

1:Vibrant, 2:harbor, 3:imagery, 4:contrasts, 5:with, 6:a, 7:closed, 8:sign, 9:il

7. Bar Harbor, Maine

Bar Harbor is the idyllic gateway to Acadia National Park, offering cool coastal breezes, fresh seafood, and stunning ocean views. Maine does not tax Social Security benefits, providing a solid, predictable baseline for your monthly retirement income.

The financial shock of Bar Harbor arrives in the off-season. When the summer tourists leave, many local grocery stores, pharmacies, and service businesses close their doors entirely for the winter. This forces year-round residents to drive over an hour to Bangor for basic groceries, services, and medical appointments. Winterizing older coastal homes against fierce Atlantic storms is incredibly expensive, and reliance on heating oil can cause utility bills to spike unpredictably. The extreme isolation can also take a heavy toll on your mental health during the dark, freezing months.

8. Taos, New Mexico

Taos offers rich Native American history, distinct adobe architecture, and a thriving creative scene. The high desert landscape is stunning, but New Mexico is one of the few states that still taxes Social Security benefits in 2026. Fortunately, state lawmakers provide exemptions for single filers with an adjusted gross income below $100,000 and married couples below $150,000.

Sitting at nearly 7,000 feet in elevation, Taos presents similar altitude and respiratory challenges as Telluride. The local real estate market is highly competitive and expensive. For major surgical procedures or specialized senior care, residents frequently must travel an hour and a half to Santa Fe or two and a half hours to Albuquerque, adding significant travel costs and logistical stress to routine medical bills.

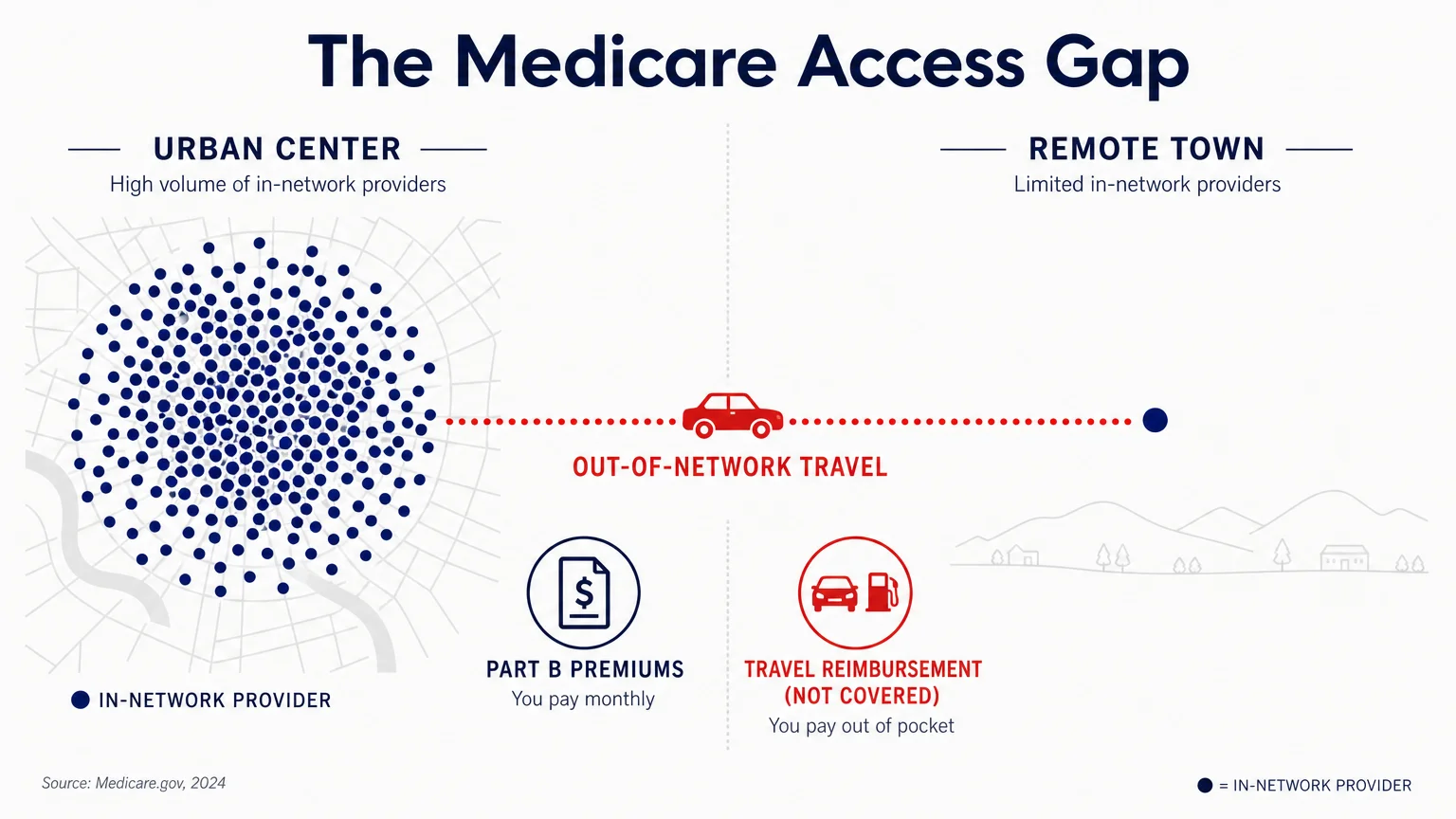

How Medicare Works in Remote Areas

Your choice of retirement town directly impacts the quality and availability of your healthcare coverage. The Medicare Advantage plan that worked perfectly in a major metropolitan suburb might leave you functionally uninsured in a remote village.

Rural hospitals operate on razor-thin margins. According to 2025 data from the American Hospital Association, Medicare Advantage plans reimburse rural hospitals at just 90.6 percent of traditional Medicare rates. Because of these low payouts and burdensome prior authorization requirements, an increasing number of rural hospitals and clinics are dropping out of Medicare Advantage networks entirely.

If you relocate to a highly remote town, enrolling in Traditional Medicare (Parts A and B) alongside a standardized Medigap policy and a standalone Part D prescription drug plan is often the safest and most reliable strategy. Traditional Medicare is accepted by nearly every doctor and hospital in the country that takes Medicare, giving you the absolute freedom to travel to distant cities for specialized care without worrying about restrictive local networks or out-of-network billing surprises.

| Coverage Feature | Traditional Medicare (Parts A & B) | Medicare Advantage (Part C) |

|---|---|---|

| Provider Network | Visit any doctor or hospital nationwide that accepts Medicare. | Restricted to a specific local or regional network of providers. |

| Rural Accessibility | Universally accepted by rural clinics and critical access hospitals. | Increasingly rejected by rural providers due to low reimbursement rates. |

| Prior Authorizations | Rarely required for medically necessary covered services. | Frequently required, which can severely delay urgent rural care. |

| Out-of-Pocket Limits | No built-in cap (requires purchasing a supplemental Medigap policy for protection). | Includes a yearly out-of-pocket maximum, but only for in-network care. |

What Can Go Wrong

Relocating without fully assessing a town’s long-term infrastructure can jeopardize your financial security. Avoid these common remote retirement mistakes:

- Buying Illiquid Real Estate: Remote housing markets move slowly. If you buy a quirky mountain cabin and later need to move to an assisted living facility closer to family, your home could sit on the market for months or years. This ties up the vital equity you need to pay for your ongoing care.

- Facing the Double Move: Relocating to a high-altitude or steep-terrain town often forces seniors into a second move when their mobility inevitably declines. Paying real estate commissions twice in one decade severely depletes your savings.

- Ignoring the New Tax Reality: Tax laws evolve rapidly. The IRS recently implemented a temporary $6,000 enhanced Senior Tax Deduction for tax years 2025 through 2028 under recent legislation, which drastically lowers federal burdens for those over 65. However, state tax laws vary wildly. Moving from a state that exempts pension income to one that taxes it can alter your monthly cash flow overnight. Verify your local standard deductions through the Internal Revenue Service (IRS).

- Underestimating Emergency Transport: If you suffer a stroke or heart attack in a town without a specialized cardiovascular center, you may require a life-flight helicopter to a major city. Even with excellent insurance, out-of-pocket costs for emergency air transport can be staggering.

“Dreaming about your future is one thing. But planning for it is an entirely different matter. One is about hopes and wishes, the other is about making smart decisions today that will give you the most secure and content tomorrows.” — Suze Orman, Personal Finance Expert

When to Consult a Professional

Retirement relocation involves complex tax, legal, and healthcare decisions. Consider seeking expert guidance in these specific scenarios:

- Before Purchasing Real Estate: Consult a fee-only Certified Financial Planner (CFP) to model how purchasing a home in a new state will impact your required minimum distributions (RMDs), property tax liabilities, and overall cash flow.

- During Medicare Open Enrollment: Work with an independent, locally licensed Medicare broker in your new destination. They can verify which local hospitals and regional specialists actually accept your coverage before you commit to a plan. You can also compare plan details directly at Medicare.gov.

- When Updating Your Estate Plan: Estate and inheritance tax laws vary heavily by state. Hire an elder law attorney in your new location to update your will, trusts, and advance healthcare directives to ensure they comply with local statutes.

Frequently Asked Questions

Do all states tax Social Security benefits?

No. As of 2026, only eight states tax Social Security benefits: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont. Many of these states offer generous exemptions based on your age and adjusted gross income. You can verify local rules through the Social Security Administration or your state’s department of revenue.

Can I keep my current Medicare Advantage plan if I move to another state?

Usually, no. Medicare Advantage plans are strictly tied to local county networks. When you move out of your current plan’s designated service area, you qualify for a Special Enrollment Period. This allows you to choose a new Advantage plan in your new town or revert to Traditional Medicare.

What exactly is a critical access hospital?

A critical access hospital is a small facility located in a designated rural area, typically limited to 25 beds or fewer. They provide 24/7 emergency care and basic outpatient services to stabilize patients, but they lack the specialized surgical, cardiac, or intensive care units found in major urban hospitals.

Retiring to a remote, scenic town is a beautiful goal, but it requires rigorous financial and logistical planning. You must account for elevated travel costs, healthcare limitations, and the practical realities of aging in an isolated environment. Take the time to rent a home in your desired town during its harshest season before committing to a permanent purchase. By testing the waters first, you can protect your retirement savings and ensure your new community truly supports your long-term well-being.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.