When international conflicts erupt, the financial shockwaves reach far beyond the battlefield—right into your retirement accounts and monthly budget. A war involving major energy producers like Iran directly threatens global oil supplies, driving up energy costs and accelerating inflation almost overnight. For retirees living on fixed incomes, this sudden spike in everyday expenses can feel overwhelming. While higher inflation eventually pushes your Social Security Cost-of-Living Adjustment (COLA) upward, these benefit bumps rarely keep pace with the real-time surge at the gas pump or grocery store. Geopolitical uncertainty also triggers sudden stock market volatility, threatening your hard-earned retirement balances. Understanding these immediate ripple effects is the first step toward shielding your finances from global instability.

The Direct Link Between Middle East Tensions and Living Costs

When a major geopolitical conflict involves a central oil producer, the global energy market reacts immediately. The Middle East controls a massive portion of the world’s daily oil supply, with millions of barrels passing through vital shipping lanes like the Strait of Hormuz. Any military action or blockade in this region creates an instant supply shortage. Financial markets price in this risk instantly, causing crude oil prices to spike.

For you, the retiree, this global event lands squarely on your monthly budget. Higher crude oil prices mean higher prices at the local gas pump. However, the damage rarely stops at transportation. Almost everything you purchase at the grocery store arrives via diesel-powered trucks. When shipping companies pay more for fuel, they pass those expenses onto the consumer. Within weeks of an overseas conflict, you will notice higher prices for fresh produce, packaged goods, and essential medical supplies. Heating oil and electricity rates also climb, forcing you to redirect funds from your savings or discretionary budget just to keep your home comfortable. This rapid inflation erodes the purchasing power of your fixed income, making careful budgeting more critical than ever.

What Geopolitical Turmoil Means for Your Social Security COLA

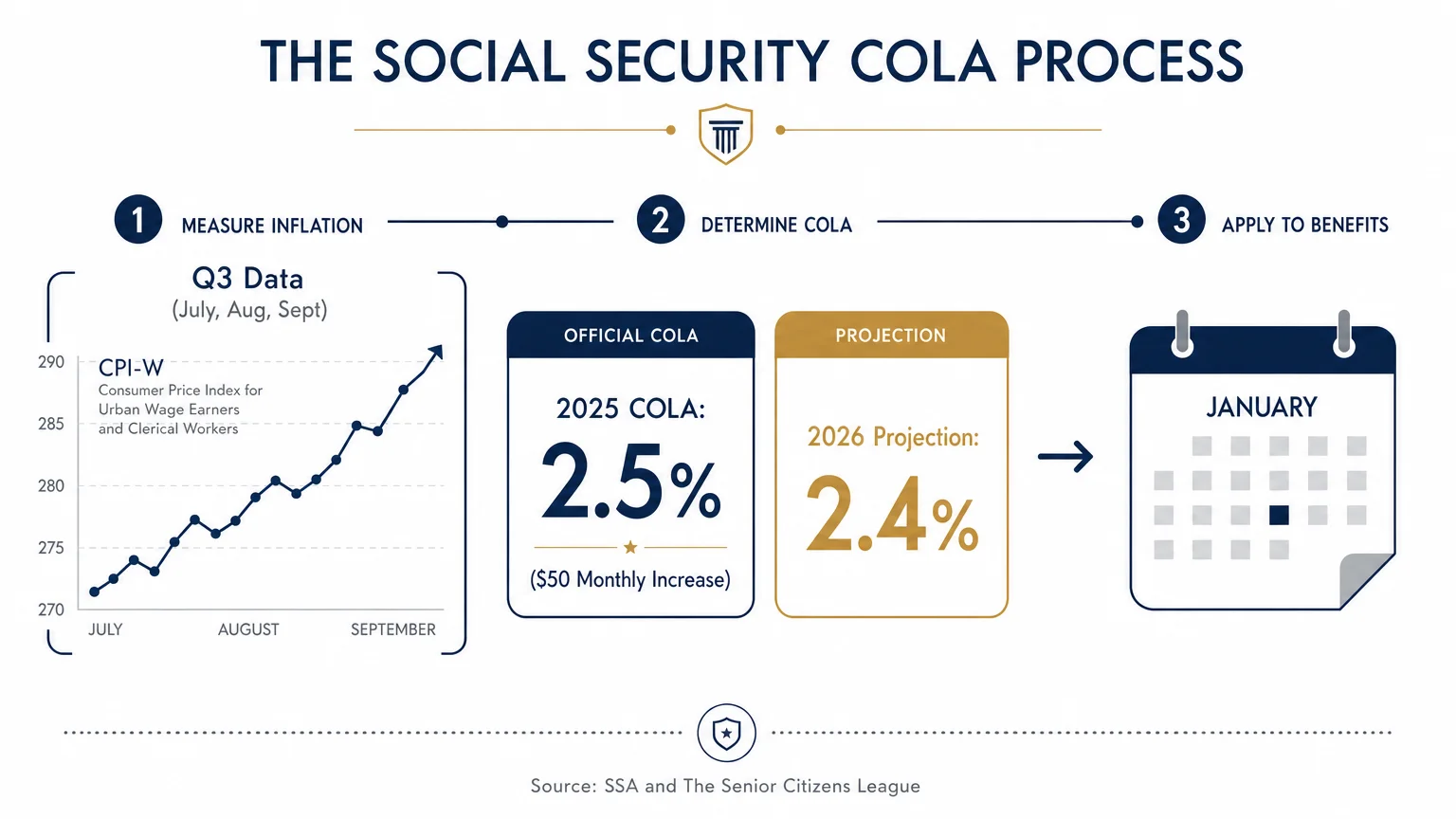

The Social Security Administration relies on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) to determine your annual Cost-of-Living Adjustment (COLA). The government measures this inflation data specifically during the third quarter of the year—July, August, and September. If a war drives up energy and consumer prices during these crucial months, the resulting data will likely trigger a higher COLA for the following year.

For historical context, as inflation cooled slightly, the Social Security Administration announced a 2.5% COLA for 2025, which provided an average monthly increase of about $50 for retirees. Before geopolitical tensions escalated further, early estimates from analysts like The Senior Citizens League projected a relatively modest 2026 COLA of approximately 2.4%.

However, a sudden wartime spike in the cost of living disrupts these projections. If prices surge, your future benefit adjustments will eventually reflect the new reality. The primary challenge you face is the lag time. If energy costs skyrocket in April, you must absorb those out-of-pocket expenses for the remainder of the year. The government will not adjust your Social Security check until the following January. During this gap, you must rely on your personal savings to bridge the difference.

Navigating Higher Medicare Costs During Inflationary Periods

Medical care requires massive energy consumption and complex supply chains. When global conflicts drive up baseline inflation, healthcare delivery costs naturally follow suit. The Centers for Medicare and Medicaid Services (CMS) evaluates these rising costs annually and adjusts premiums accordingly.

In 2025, the standard Medicare Part B premium increased by roughly 6% to $185.00 per month. Additionally, the annual Part B deductible rose to $257. Because the government automatically deducts Medicare Part B premiums from your Social Security payments, these rising healthcare costs directly reduce the net amount deposited into your bank account. You can verify your specific Medicare costs and current deductibles at Medicare.gov.

If war-driven inflation accelerates, you can expect future Medicare premiums to climb even faster. For seniors with higher incomes, the Income-Related Monthly Adjustment Amount (IRMAA) poses an additional risk. If you are forced to withdraw larger amounts from your tax-deferred retirement accounts just to cover wartime inflation, you might accidentally push your modified adjusted gross income into a higher bracket, triggering steep IRMAA surcharges on your Medicare premiums.

Market Volatility and Your Retirement Savings

Financial markets despise uncertainty. The outbreak of war, especially one threatening global energy supplies, frequently triggers immediate stock market sell-offs. Institutional investors panic, moving capital out of equities and into perceived safe havens. For a young worker, a temporary market dip represents a chance to buy stocks at a discount. For a senior actively withdrawing from a 401(k) or Individual Retirement Account (IRA), this volatility introduces severe “sequence of returns risk.”

Sequence of returns risk occurs when you are forced to sell investments during a market downturn to fund your daily living expenses. Selling stocks while prices are low locks in those losses permanently. Your portfolio loses the shares needed to recover when the market eventually stabilizes.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett, Investing Expert

Maintaining patience during wartime headlines protects your hard-earned wealth. Historical data shows that while geopolitical shocks cause sharp, sudden market drops, equities generally recover once the initial uncertainty passes. Reacting emotionally to breaking news and liquidating your portfolio at the bottom is one of the fastest ways to deplete your retirement savings.

Actionable Strategies to Protect Your Portfolio

You cannot control international relations, but you can control your financial posture. Implementing defensive strategies ensures your retirement plan survives global turbulence.

- Build a robust cash buffer: Maintain enough liquid cash in high-yield savings accounts or money market funds to cover 12 to 24 months of living expenses. This buffer allows you to pause portfolio withdrawals during wartime market dips, protecting your invested assets until the market recovers.

- Review your fixed-income allocations: Ensure your portfolio contains a well-structured bond ladder, utilizing Treasury bills or Certificates of Deposit (CDs). These predictable, fixed-income vehicles provide reliable yields without the daily price swings associated with the stock market.

- Maximize your tax deductions: Shielding your income from taxes leaves more money in your pocket to fight inflation. The Internal Revenue Service (IRS) offers higher standard deductions for older Americans. For the 2025 tax year, the standard deduction for a single filer aged 65 or older is $17,750. For a married couple filing jointly, where both spouses are 65 or older, the maximum standard deduction reaches up to $34,700. Taking full advantage of these limits helps stretch your budget.

- Audit your discretionary spending: Separate your essential expenses from your discretionary wants. If energy prices surge due to overseas conflicts, temporarily reducing travel or dining out provides the extra cash flow needed to cover inflated grocery and utility bills.

Comparing Pre-War vs. Conflict-Era Financial Strategies

Adapting your approach during times of global instability requires a deliberate shift in mindset. Review the table below to see how standard retirement strategies pivot during conflict-driven economies.

| Financial Area | Standard Retirement Strategy | Conflict-Era Defensive Strategy |

|---|---|---|

| Emergency Funds | Holding 3 to 6 months of living expenses in a standard savings account. | Holding 12 to 24 months of expenses in high-yield accounts to outlast market dips. |

| Portfolio Withdrawals | Automated monthly sales of stocks and bonds to generate consistent income. | Pausing stock sales; pulling necessary income only from cash reserves and mature bonds. |

| Budgeting | Reviewing expenses annually based on general inflation trends. | Auditing budgets monthly to adjust for rapid spikes in gas, heating, and grocery costs. |

| Tax Planning | Taking standard withdrawals to satisfy minimum income requirements. | Carefully managing withdrawals to avoid triggering Medicare IRMAA surcharges during inflation. |

Pitfalls to Watch For

Even experienced investors make emotional decisions when faced with alarming geopolitical news. Avoid these common mistakes to protect your financial security.

- Liquidating investments in a panic: Moving your entire retirement portfolio to cash after the market drops guarantees a permanent loss. Furthermore, cash loses its purchasing power rapidly during the exact inflationary periods caused by wartime energy spikes.

- Relying on the COLA to fix immediate problems: Assuming your upcoming Social Security adjustment will bail you out of a mid-year inflation spike leaves you vulnerable. You must have personal savings to survive the months between the initial price surges and the eventual January benefit increase.

- Falling for crisis-themed financial scams: Fraudsters thrive on fear. During international conflicts, you will likely encounter aggressive sales pitches for overpriced physical gold coins, bogus foreign currency investments, or unregistered cryptocurrency schemes promising safe haven returns. Always verify investment professionals and products through official channels like Investor.gov.

- Ignoring Required Minimum Distributions (RMDs): If you are of RMD age, the IRS still requires you to withdraw funds from your tax-deferred accounts, regardless of what the stock market is doing. Failing to take your RMD out of fear of selling low will result in severe tax penalties.

Getting Expert Help

Managing the intersection of global conflict, inflation, and retirement withdrawals requires precision. You do not have to navigate these complexities alone. Consider consulting a licensed, fee-only fiduciary financial advisor in the following scenarios:

- You are nearing RMD age during a market downturn: A professional can help you strategically select which assets to sell for your required distributions, minimizing the damage to your long-term growth potential.

- Your fixed income no longer covers essentials: If wartime inflation pushes your basic living expenses beyond your Social Security and pension income, an advisor can help safely restructure your portfolio to generate higher yields without taking on excessive risk.

- You want to execute a Roth conversion: A temporary market dip caused by geopolitical news actually presents a unique tax opportunity. Converting traditional IRA funds to a Roth IRA while asset prices are depressed lowers your immediate tax bill and allows the assets to grow tax-free during the eventual economic recovery.

Frequently Asked Questions

Will a war involving Iran halt my Social Security deposits?

No. The Social Security Administration pays benefits out of domestic trust funds, which are funded by payroll taxes collected from the current U.S. workforce. Overseas conflicts do not disrupt the federal government’s ability to process and deposit your monthly checks.

Does geopolitical conflict change how Medicare is funded?

Not directly. However, conflicts drive up baseline inflation and energy costs, which eventually increases the cost of domestic medical care. When healthcare becomes more expensive to provide, the Centers for Medicare and Medicaid Services typically raises future beneficiary premiums and deductibles to cover the difference.

Should I move my entire 401(k) to cash until the war ends?

Moving entirely to cash exposes you to severe inflation risk. While cash protects you from daily market swings, its purchasing power rapidly degrades when energy and food prices surge. A balanced portfolio containing equities, bonds, and a healthy cash buffer provides the best defense against both market drops and inflation.

How quickly does a spike in gas prices affect my Social Security check?

It does not happen immediately. The government measures the specific inflation data used for the Cost-of-Living Adjustment only during July, August, and September. Any adjustment based on that data does not take effect until your January payment. You must absorb any real-time price spikes using your own savings during the gap.

Global conflicts naturally create feelings of unease, especially when you are living on a fixed income and watching the markets react to breaking news. However, your financial security does not have to be a casualty of overseas turmoil. By maintaining a healthy cash buffer, strictly managing your discretionary budget, and avoiding emotional investment decisions, you can successfully insulate your retirement from the immediate shocks of war. Stay focused on the variables you can control, and remember that historically, the U.S. economy and markets have weathered numerous geopolitical crises and emerged resilient.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.