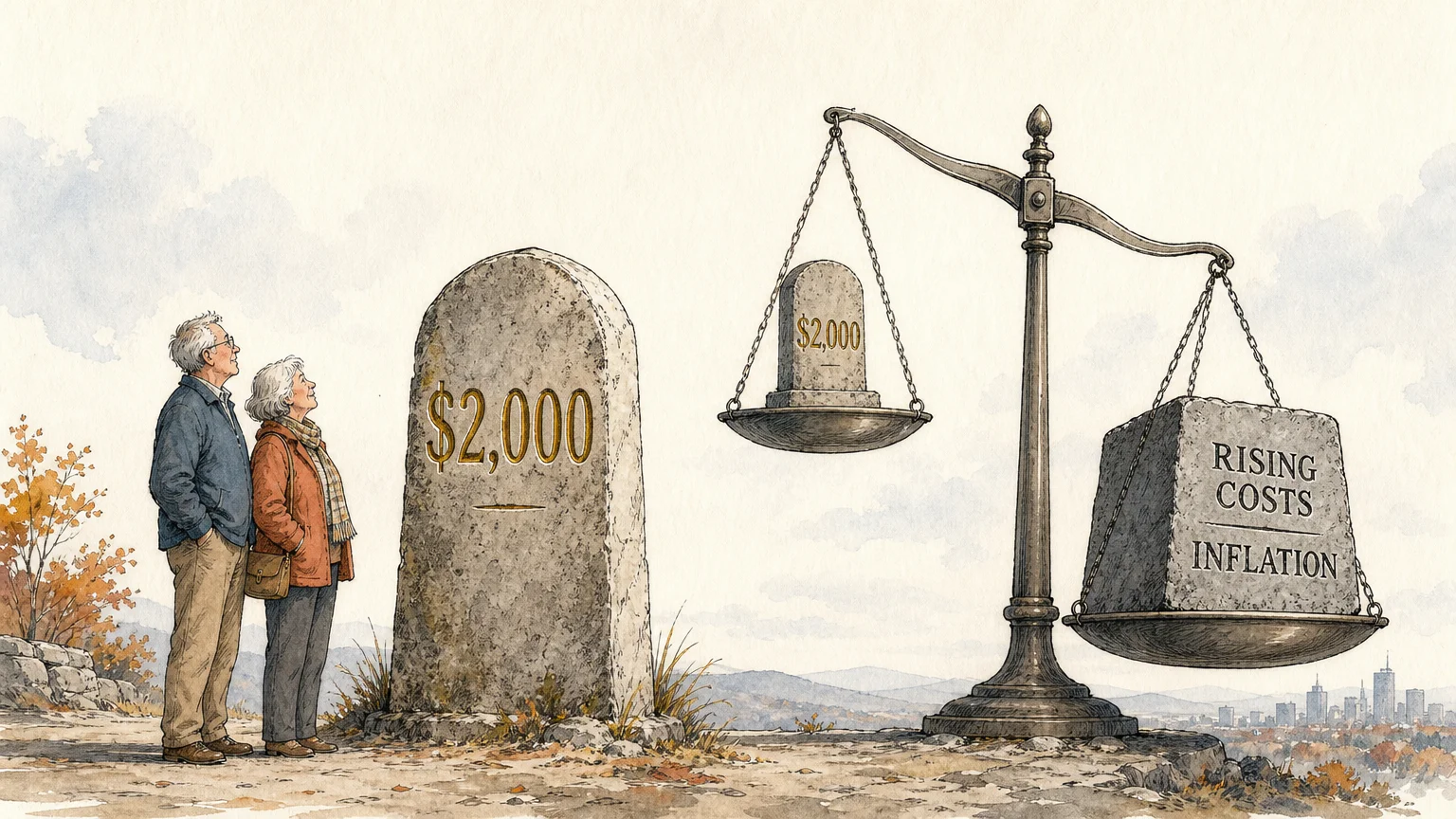

Social Security reached a historic milestone in 2026, with the average monthly benefit finally crossing the $2,000 threshold for retired workers. This boost provides a crucial lifeline if you are facing higher everyday living costs. However, banking on this temporary high-water mark could jeopardize your financial security. Unprecedented shifts are approaching in 2027, including soaring Medicare Part B premiums that threaten to consume your cost-of-living adjustments. Furthermore, the full retirement age officially finalizes its shift to 67, while the countdown toward the program’s trust fund depletion accelerates at an alarming rate. Understanding these impending policy changes and funding shortfalls is the only way to protect your hard-earned benefits from shrinking exactly when you rely on them most.

How the Average Benefit Crossed the $2,000 Threshold

For decades, seniors built their retirement plans around relatively modest government checks. Thanks to consecutive years of inflation-driven cost-of-living adjustments (COLAs)—including the 2.5 percent bump in 2025 and the subsequent 2.8 percent adjustment announced for 2026—the average retired worker now receives approximately $2,026 per month. Reaching this $2,000 milestone represents a massive shift in nominal payout amounts compared to just a decade ago.

Higher checks look great on paper, but you must evaluate this income through the lens of purchasing power. The cost of groceries, housing, utilities, and prescription medications has climbed aggressively alongside these benefit increases. The Social Security Administration (SSA) designs the annual COLA strictly to keep pace with inflation, not to provide a true raise in your standard of living. If your monthly check increased by $50 but your essential household expenses rose by $75, your household budget effectively runs at a deficit despite the historic benefit average.

You also need to understand the difference between gross benefits and net benefits. The celebrated $2,000 average reflects the gross amount calculated by the government before any necessary deductions take place. By the time that money hits your bank account, several automatic subtractions alter the final deposit. The most significant of these deductions comes directly from the healthcare sector.

The Hidden Squeeze: Surging Medicare Part B Premiums

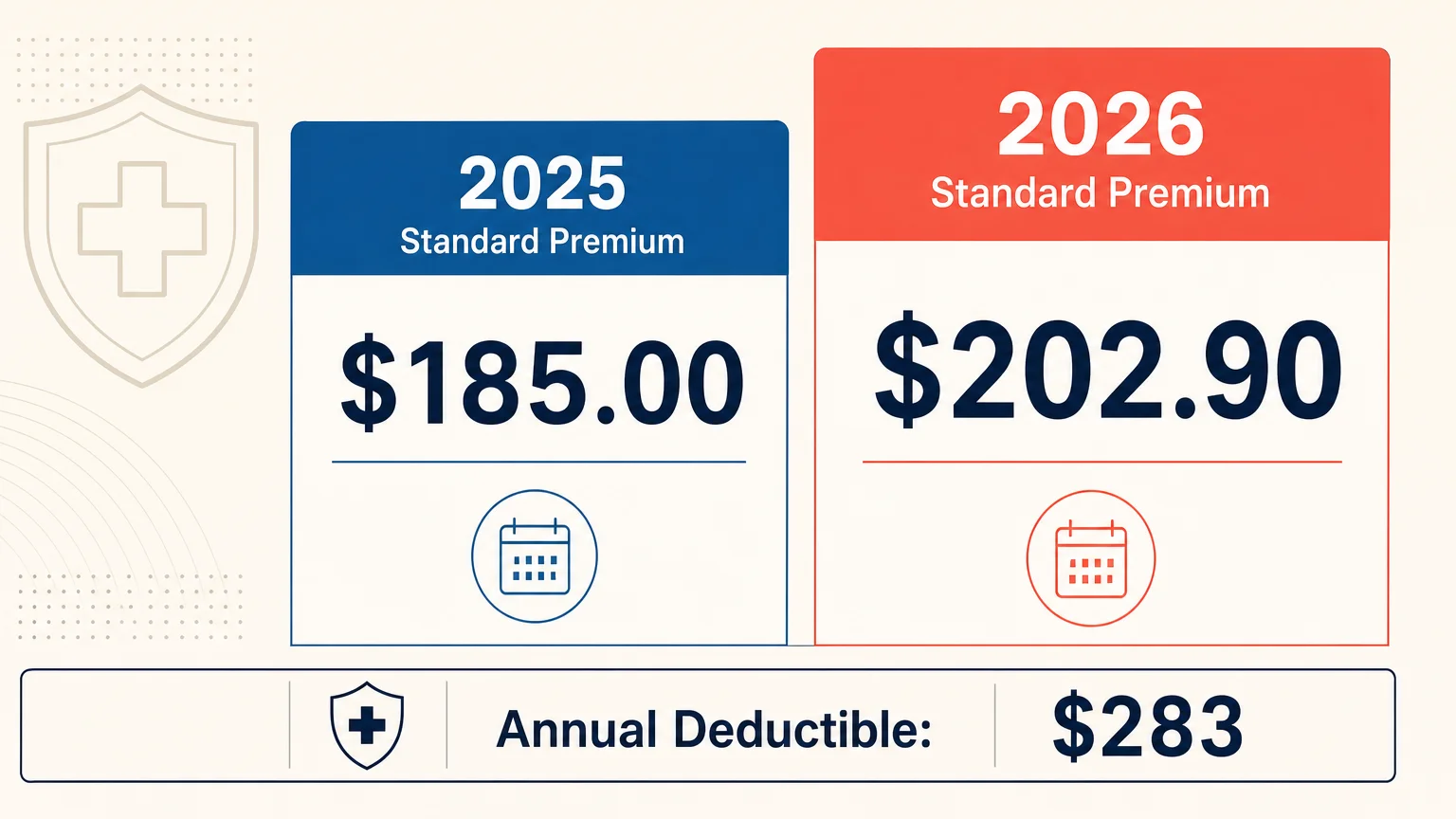

As you plan your budget for 2027, you must factor in the rising cost of healthcare. Medicare Part B covers your outpatient care, doctor visits, and preventive services. Unlike Medicare Part A, which is generally premium-free if you paid Medicare taxes during your working years, Part B carries a monthly cost that the government deducts directly from your Social Security check.

In 2026, the standard Medicare Part B premium jumped to $202.90 per month, a stark increase from the $185.00 rate in 2025. The annual Part B deductible also climbed to $283. When Medicare premiums increase at a faster percentage rate than the Social Security COLA, healthcare costs quietly cannibalize your raise. If healthcare inflation continues on its current trajectory, projections indicate that 2027 could bring another aggressive premium hike.

For higher-income retirees, the situation becomes even more complicated due to the Income-Related Monthly Adjustment Amount (IRMAA). If your Modified Adjusted Gross Income (MAGI) from two years prior exceeds specific IRS limits, you pay a surcharge on top of the standard Part B premium. This means your 2027 Medicare premiums will be determined by the income you reported on your 2025 tax return. Selling a home, converting a traditional IRA to a Roth IRA, or taking a large portfolio withdrawal can unexpectedly trigger IRMAA, shrinking your net Social Security benefit just when you expected a COLA increase. Always check current premium brackets at Medicare.gov to avoid costly surprises.

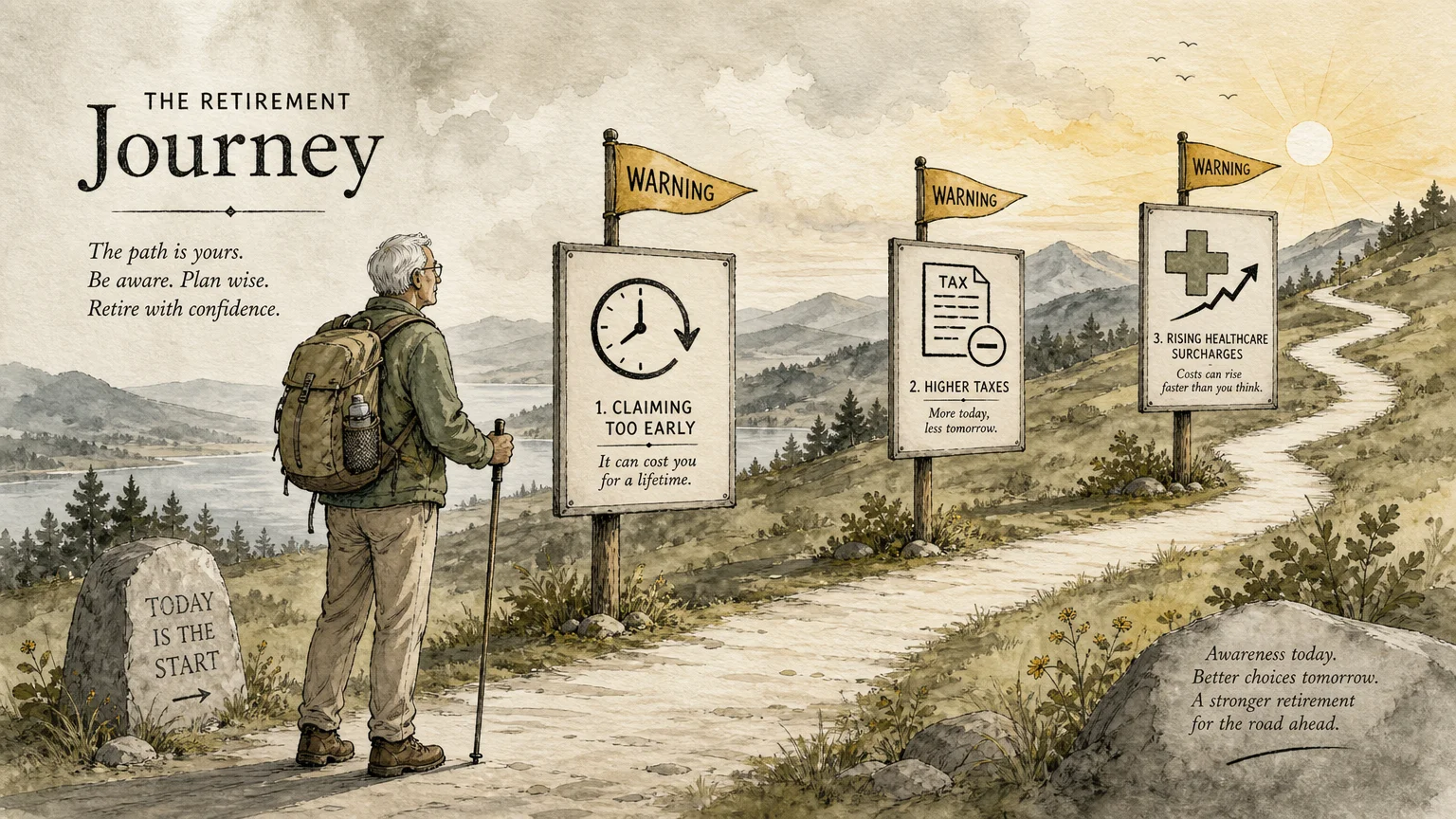

The Full Retirement Age Finishes Its Long Transition

The rules governing when you can claim your full benefits have undergone a massive transformation, and 2027 marks the final chapter of this shift. For decades, the Full Retirement Age (FRA)—the exact age at which you qualify for 100 percent of your primary insurance amount—was 65. In 1983, Congress amended the law to gradually increase the FRA to account for longer life expectancies.

If you were born between 1943 and 1954, your FRA was 66. For every birth year from 1955 to 1959, the age threshold increased by two months. If you were born in 1960, you turn 67 in 2027. This demographic milestone means the gradual phase-in is completely finished; for anyone born in 1960 or later, the Full Retirement Age is firmly and permanently set at 67.

This policy change effectively acts as a benefit cut for anyone who wishes to retire early. You still possess the right to claim Social Security as early as age 62, but doing so now triggers the maximum possible permanent penalty. Filing at 62 reduces your monthly check by 30 percent compared to waiting for your Full Retirement Age. If your full benefit at age 67 would be $2,000, claiming at 62 drops that lifetime monthly payment to just $1,400. Once you lock in this reduced rate, you cannot reset it simply by reaching age 67 later on.

Comparing Benefit Amounts by Claiming Age

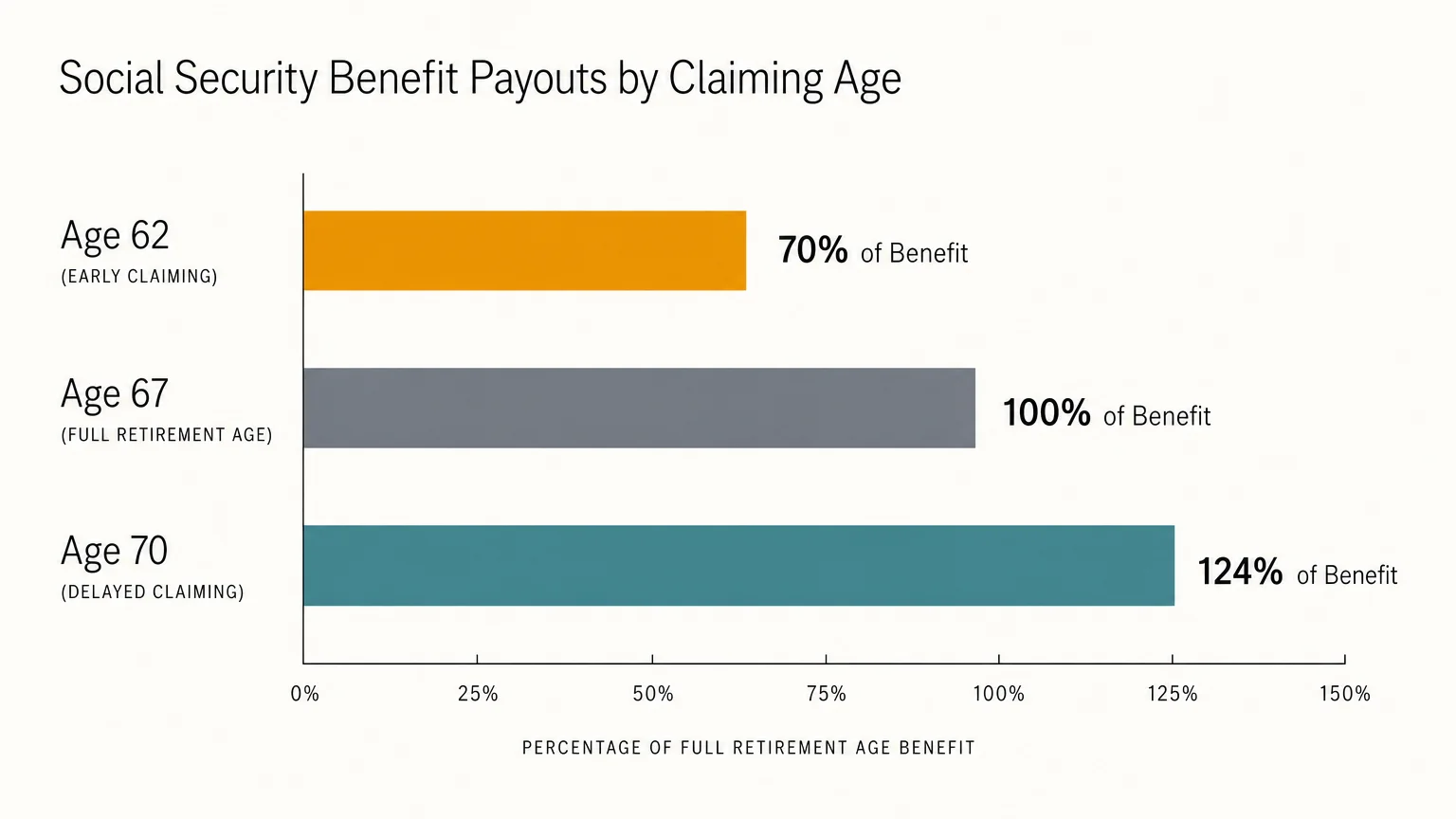

Understanding the mathematical impact of your claiming age is critical for maximizing your lifetime income. The government rewards patience. For every year you delay claiming past your Full Retirement Age up to age 70, you earn delayed retirement credits that increase your benefit by 8 percent annually.

The table below illustrates how filing age drastically alters your monthly income. This example assumes a worker born in 1960 or later, with a primary insurance amount (PIA) of exactly $2,000 at a Full Retirement Age of 67.

| Claiming Age | Percentage of Full Benefit | Estimated Monthly Payment | Financial Impact |

|---|---|---|---|

| Age 62 | 70% | $1,400 | Maximum permanent reduction; locked in for life. |

| Age 65 | 86.6% | $1,733 | Partial reduction; you still lose over 13% of your base benefit. |

| Age 67 (FRA) | 100% | $2,000 | You receive your standard primary insurance amount. |

| Age 70 | 124% | $2,480 | Maximum delayed credits; ensures the highest possible survivor benefit. |

Waiting until age 70 secures a guaranteed 24 percent boost above your baseline benefit. Very few traditional investments offer a guaranteed, risk-free 8 percent annual return, making delayed claiming one of the most powerful financial strategies available to healthy pre-retirees.

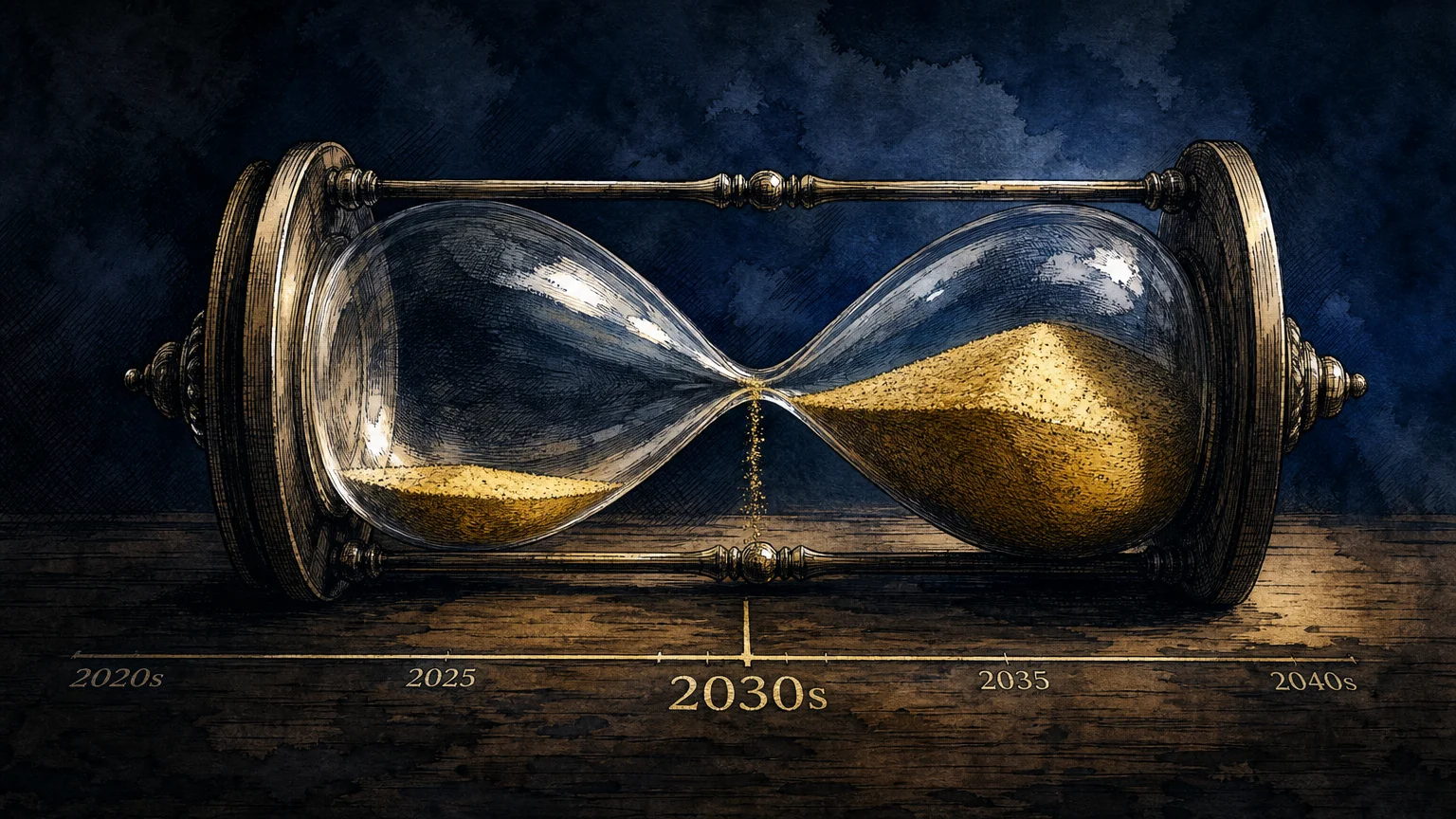

The Approaching Trust Fund Cliff in the 2030s

While navigating the rules for 2027 requires careful planning, a much larger storm gathers on the horizon. Social Security operates as a pay-as-you-go system; the payroll taxes collected from today’s workers fund the benefits distributed to today’s retirees. Because the massive Baby Boomer generation is retiring and birth rates have declined, the ratio of workers to beneficiaries has dropped significantly.

To bridge the gap between tax revenues and benefit payouts, the SSA relies on surplus reserves held in the Old-Age and Survivors Insurance (OASI) Trust Fund. The 2026 Trustees Report issued a stark warning: the trust fund is currently on pace to deplete its reserves by late 2032 or early 2033.

Trust fund depletion does not mean Social Security goes bankrupt or stops paying benefits entirely. The system will continue to collect ongoing payroll taxes. However, once the reserve dries up, those incoming taxes are projected to cover only about 78 percent of scheduled benefits. If Congress fails to pass legislative reforms before this deadline, you could face an automatic, across-the-board benefit cut of approximately 22 percent.

This looming 2032 deadline creates immense anxiety for seniors mapping out their 2027 finances. Fear of these cuts drives many healthy individuals to claim early at age 62, hoping to secure what they can before the system changes. Unfortunately, panic-filing locks in a permanent 30 percent reduction right now. If an additional 22 percent cut occurs in the 2030s, an already reduced early benefit will shrink to a level that may push vulnerable seniors into poverty.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

The Taxation Trap: Why Your Net Income Might Shrink

Another profound threat to your 2027 retirement budget lies in the United States tax code. Many seniors falsely assume their Social Security benefits are entirely tax-free. In reality, whether the Internal Revenue Service (IRS) taxes your benefits depends on a specific calculation known as “Provisional Income.”

You calculate your Provisional Income by adding together your Adjusted Gross Income (AGI), any nontaxable interest (like municipal bond interest), and exactly 50 percent of your total Social Security benefits. Once you have this number, you compare it to the federal threshold limits:

- Individual Filers: If your provisional income falls between $25,000 and $34,000, up to 50 percent of your benefits may be taxable. If it exceeds $34,000, up to 85 percent of your benefits become taxable.

- Married Filing Jointly: If your provisional income falls between $32,000 and $44,000, up to 50 percent of your benefits may be taxable. If it exceeds $44,000, up to 85 percent of your benefits become taxable.

Here is the critical problem for 2027: Congress established these tax thresholds in the 1980s and early 1990s, and they have never been indexed for inflation. As annual COLAs push the average benefit past the $2,000 mark, an increasing number of middle-class seniors find themselves pushed over the $25,000 or $32,000 provisional income thresholds. Without realizing it, you may face a larger federal tax bill simply because your government benefit increased.

Pitfalls to Watch For

Managing retirement income involves dodging invisible landmines. When preparing for 2027, be hyper-aware of these common mistakes that routinely cost seniors thousands of dollars.

Mistake 1: Ignoring the Earnings Test

If you claim Social Security before your Full Retirement Age and continue to work a job, you trigger the Retirement Earnings Test. The SSA limits how much you can earn before they start withholding your benefit checks. For example, if you exceed the annual limit in the years leading up to your FRA, the government withholds $1 in benefits for every $2 you earn above the threshold. While you eventually get this money back in the form of a recalculated benefit later in life, the immediate cash flow disruption can ruin your monthly budget. Once you reach FRA, the earnings test disappears entirely.

Mistake 2: Overlooking Spousal and Survivor Benefits

Married couples often make the mistake of evaluating their benefits in silos rather than as a joint household strategy. If your spouse had a significantly higher lifetime earnings record, you might be eligible for a spousal benefit that equals up to 50 percent of their Full Retirement Age amount. Furthermore, survivor benefits dictate that a widow or widower inherits the higher of the two household Social Security checks. When the higher-earning spouse delays claiming until age 70, they permanently maximize the survivor benefit left behind for their partner.

Mistake 3: Mismanaging Retirement Account Withdrawals

Pulling large sums from a traditional 401(k) or IRA increases your taxable income for the year. This elevated income can instantly push your provisional income over the IRS thresholds, causing up to 85 percent of your Social Security to become taxable. Additionally, as mentioned earlier, it can trigger Medicare IRMAA surcharges. Firing off random withdrawals without a tax strategy is a guaranteed way to bleed wealth.

Getting Expert Help

Navigating the complex interplay of Social Security rules, Medicare premiums, and IRS taxation often requires professional intervention. The stakes are too high to rely solely on guesswork. Consider consulting a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) in the following scenarios:

- You are coordinating a dual-income retirement: A professional can run break-even analyses to determine the precise months you and your spouse should file to maximize your combined lifetime payout.

- You face Required Minimum Distributions (RMDs): When you reach age 73, the IRS forces you to withdraw money from your traditional retirement accounts. A CPA can help you plan Roth conversions in your 60s to lower future RMDs and protect your Social Security from taxation.

- You are navigating the loss of a spouse: Filing for survivor benefits involves strict timing rules. An expert can guide you on whether to claim survivor benefits first while letting your own benefit grow, or vice versa.

You can find vetted, fee-only financial planners through resources like the Investor.gov (SEC) database or reputable organizations like the CFP Board. Additionally, the AARP provides excellent free calculators and advocacy information regarding your benefits.

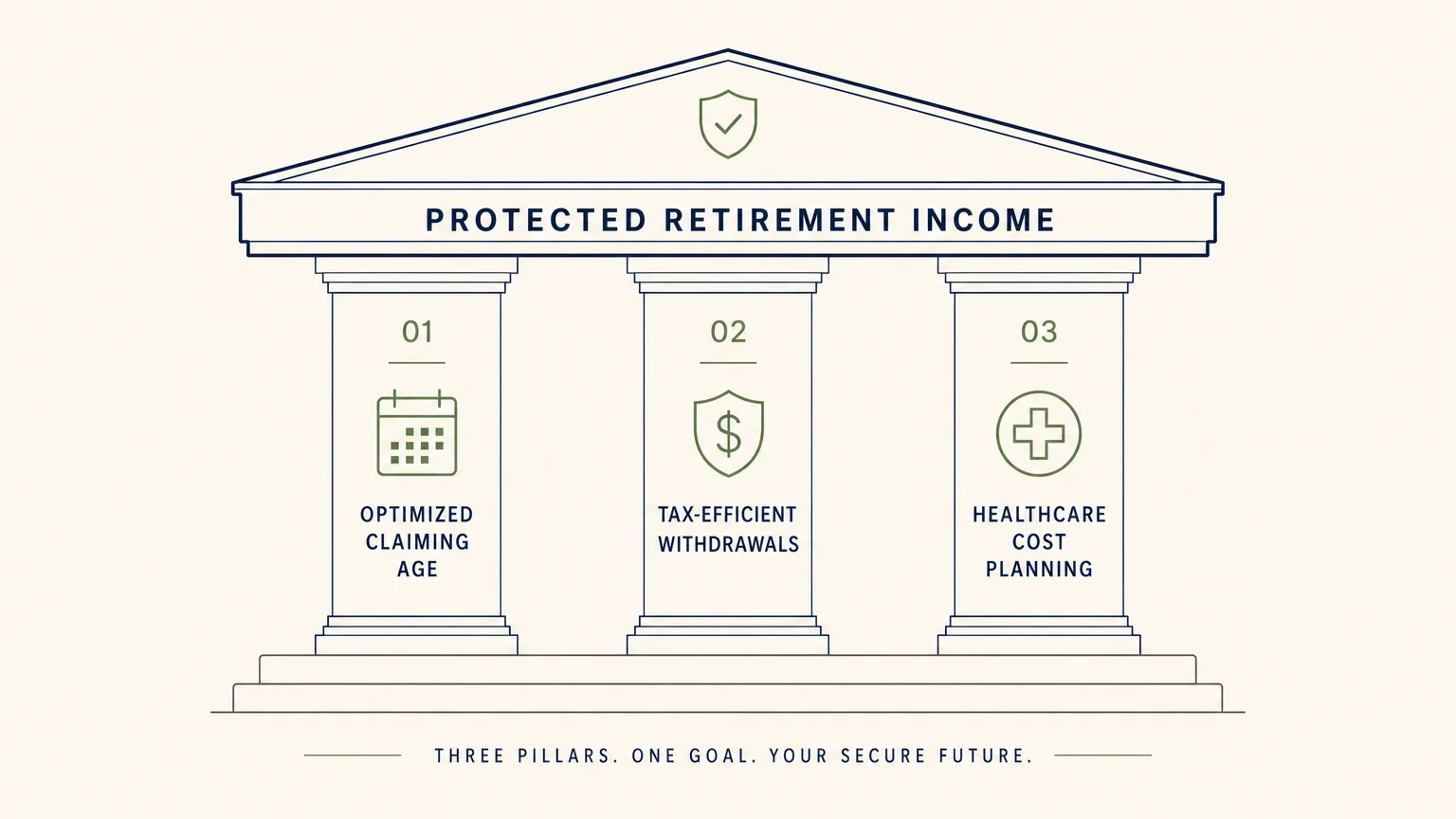

Strategies to Fortify Your Retirement Income

If the news regarding trust fund depletion and rising Medicare costs makes you anxious, take proactive steps now to secure your financial foundation. You possess more control over your retirement than you might realize.

First, diversify your income streams. Social Security was only ever designed to replace roughly 40 percent of the average worker’s pre-retirement income. It is a safety net, not a complete pension. Build secondary income through dividend-paying stocks, high-yield savings accounts, part-time consulting work, or rental income. The less reliant you are on the government’s monthly deposit, the less impact future policy changes will have on your lifestyle.

Second, manage your tax liabilities ruthlessly. Explore the benefits of Roth accounts. Withdrawals from a Roth IRA are tax-free and do not count toward the provisional income formula that taxes your Social Security. By strategically converting portions of your traditional IRA to a Roth IRA during lower-income years, you effectively insulate your future benefits from the IRS.

Finally, practice extreme patience with your claiming timeline. If your health is stable and you have sufficient savings to bridge the gap, delay your claim. Every month you wait between age 62 and age 70 increases your permanent baseline benefit. A larger baseline means larger nominal dollar amounts when annual COLAs are applied in the future. It acts as the ultimate hedge against both inflation and potential congressional benefit cuts.

2027 brings a finalized Full Retirement Age, escalating healthcare premiums, and a ticking clock on the trust fund. Do not let these shifts catch you off guard. Audit your spending, review your tax strategy, and build a comprehensive plan that protects your wealth well into your later years.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.