Retiring today means aiming at a moving financial target. Healthcare, housing, and insurance costs are rising faster than the general inflation rate, eating into fixed incomes before you even budget for groceries. While the Social Security Administration’s 2026 cost-of-living adjustment of 2.8% offers some relief, it often falls short of covering the real-world expenses seniors face. Understanding which budget categories are growing the fastest allows you to adjust your withdrawal strategies and avoid draining your nest egg prematurely. By actively managing these specific cost centers—from Medicare premiums to property taxes—you can protect your wealth and maintain the lifestyle you worked so hard to build.

The Accelerating Cost of Healthcare

Healthcare predictably consumes a large portion of any senior’s budget, but the rate at which these costs accelerate often catches new retirees off guard. Unlike standard consumer goods, medical inflation typically outpaces general economic inflation. When you transition to a fixed income, even marginal increases in premiums, deductibles, and prescription out-of-pocket costs can force you to rethink your monthly spending limits.

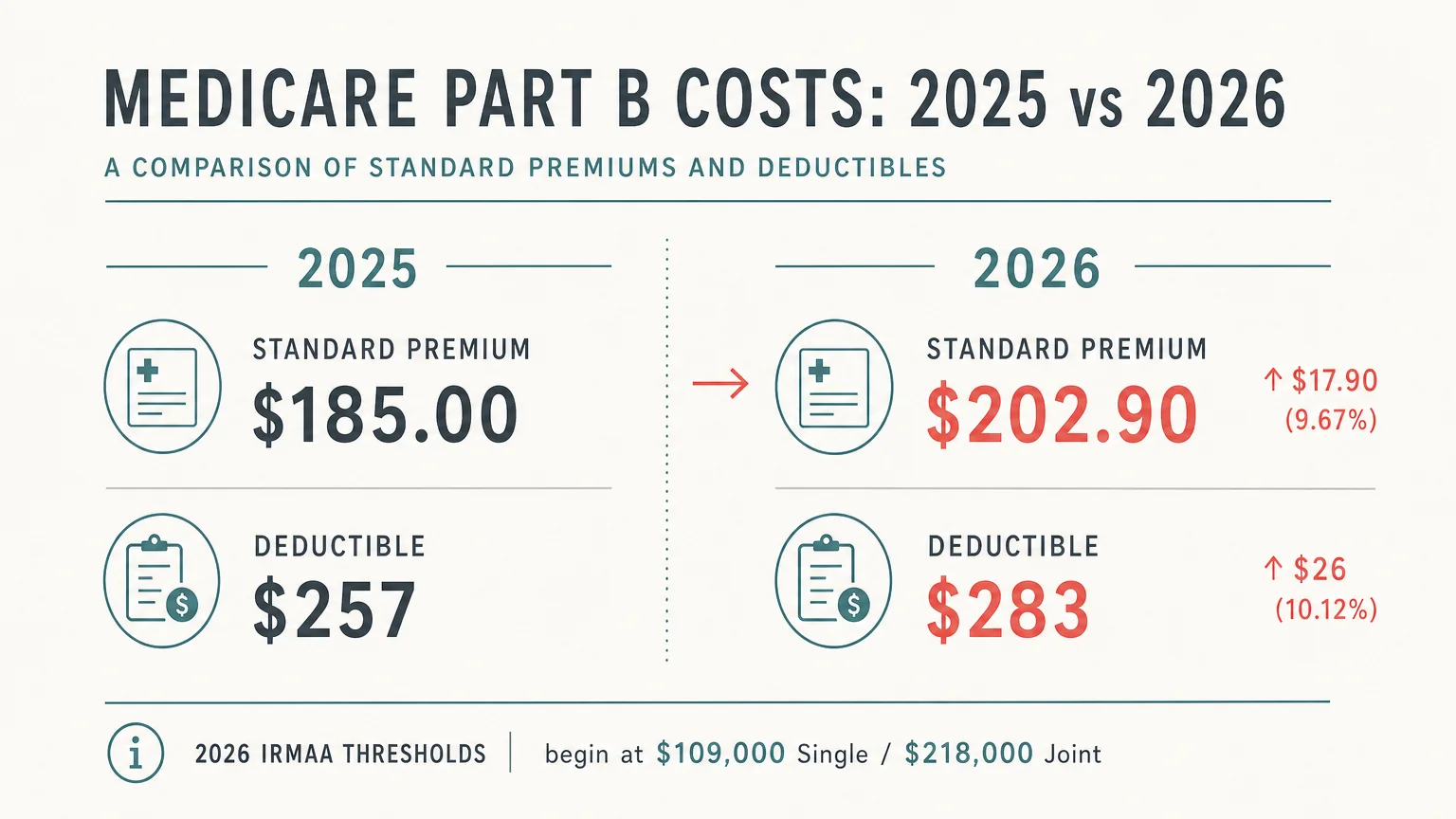

The standard Medicare Part B premium for 2026 is $202.90 per month, a noticeable jump from the $185.00 charged in 2025. Furthermore, the annual Part B deductible rose from $257 to $283. Because Part B premiums are automatically deducted from your Social Security payments, these increases effectively shrink your net income before the money ever reaches your checking account.

For retirees with higher incomes, the cost is even steeper. The Medicare Income-Related Monthly Adjustment Amount (IRMAA) acts as a surcharge on top of your standard Part B and Part D premiums. For 2026, the IRMAA threshold begins at $109,000 for single filers and $218,000 for couples filing jointly. If your income from two years prior exceeds these thresholds by even one dollar, your monthly healthcare costs will multiply.

To combat rising healthcare expenses, consider the following strategies:

- Review your coverage annually: During the Medicare Open Enrollment Period (October 15 to December 7), compare your current Part D or Advantage plan against new offerings on Medicare.gov. Formularies change every year; the plan that covered your prescriptions cheaply last year might not be the most cost-effective option this year.

- File an IRMAA appeal: If you experienced a “life-changing event”—such as retirement, divorce, or the death of a spouse—that reduced your income, file Form SSA-44 with the Social Security Administration. You can request that they use your current, lower income to calculate your premiums rather than your older, higher income.

- Utilize preventive care: Medicare Part B covers a wide array of preventive services, including annual wellness visits, cancer screenings, and vaccinations, completely free of charge. Catching a condition early is the most reliable way to reduce long-term medical spending.

Housing, Property Taxes, and Maintenance

Many seniors enter retirement with the peace of mind that comes from a paid-off mortgage. However, homeownership costs do not disappear once the loan is satisfied. Property taxes, homeowners insurance, and general maintenance are among the fastest-growing budget categories for retirees today.

As real estate values climb, local tax assessors adjust property appraisals upward. A home purchased thirty years ago for $150,000 may now be assessed at over $500,000, triggering a massive property tax bill that does not align with your fixed income. Simultaneously, the cost of homeowners insurance has skyrocketed in regions prone to natural disasters, and general home maintenance costs have surged due to elevated labor and material prices.

Protecting your housing budget requires a proactive approach:

- Apply for property tax relief: Many states and local municipalities offer property tax freezes, deferrals, or substantial exemptions specifically for seniors. Eligibility usually depends on your age and income. Contact your local county tax assessor’s office to find out what relief programs you qualify for.

- Increase your insurance deductibles: If your homeowners insurance premium has jumped, raising your deductible from $1,000 to $2,500 can significantly lower your monthly rate. Just ensure you keep the deductible amount securely set aside in a high-yield savings account for emergencies.

- Evaluate downsizing objectively: Moving to a smaller home or a less expensive state can free up equity and lower your tax burden. However, you must carefully calculate the transaction costs—such as realtor fees, moving expenses, and current mortgage interest rates if you need to finance a portion of the new purchase.

Auto Insurance and Transportation

Auto insurance presents a uniquely frustrating challenge for older adults. You might drive less frequently, obey all speed limits, and maintain a spotless driving record, yet still see your premiums rise. Auto insurance rates spiked significantly through the post-pandemic years, and while the national average saw a slight dip in 2025, rates remain elevated; several states are still projecting moderate increases for 2026.

Insurers heavily weigh age when calculating risk. Statistically, older drivers are more likely to be involved in accidents and are more susceptible to severe injuries when accidents occur. As you cross into your 70s, you will likely notice your auto insurance premiums creeping upward simply because you moved into a new demographic risk bracket.

You do not have to accept these automatic rate hikes passively. Take action to force your premiums back down:

- Take a defensive driving course: Many states mandate that insurance companies offer a multi-year discount to seniors who complete an approved accident prevention course. Organizations like AARP offer these classes online for a nominal fee.

- Report reduced mileage: If you no longer commute to work, your annual mileage has likely plummeted. Call your insurance agent and update your mileage bracket; driving under 5,000 miles a year qualifies you for a low-mileage discount with most carriers.

- Reassess comprehensive coverage: If your vehicle is over ten years old and its market value has significantly depreciated, it might be time to drop collision and comprehensive coverage. If the annual cost of the coverage exceeds 10% of the vehicle’s replacement value, you are likely overpaying.

Taxes: The Stealth Expense

“Taxes will be the single biggest factor that separates people who keep their retirement money from those who lose it.” — Ed Slott, CPA and Retirement Tax Expert

Many people assume their tax burden will plummet the day they stop working. While your earned income drops, your taxable income can actually rise depending on how you structure your withdrawals. Taxes represent a rapidly growing category for retirees who fail to plan for Required Minimum Distributions (RMDs) and the taxability of their Social Security benefits.

If your combined income—which the IRS calculates as your Adjusted Gross Income (AGI) plus nontaxable interest plus half of your Social Security benefits—exceeds certain thresholds, up to 85% of your Social Security benefits become taxable. Because these thresholds have not been adjusted for inflation in decades, a growing number of middle-class seniors find themselves caught in this tax trap every year.

Fortunately, the IRS provides powerful tools to help seniors shield their income. The 2026 standard deduction is highly favorable for retirees. For 2026, the basic standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. Additionally, if you are 65 or older, you are entitled to an extra standard deduction of $2,050 for singles and $1,650 per qualifying person for joint filers.

Even more impactful is a new temporary provision available from 2025 through 2028. Eligible seniors can claim an enhanced deduction of up to $6,000 per person ($12,000 for married couples filing jointly), subject to income phase-outs starting at a modified adjusted gross income of $75,000 for singles and $150,000 for joint filers. Check directly with the IRS or your tax professional to ensure you claim every dollar you are entitled to.

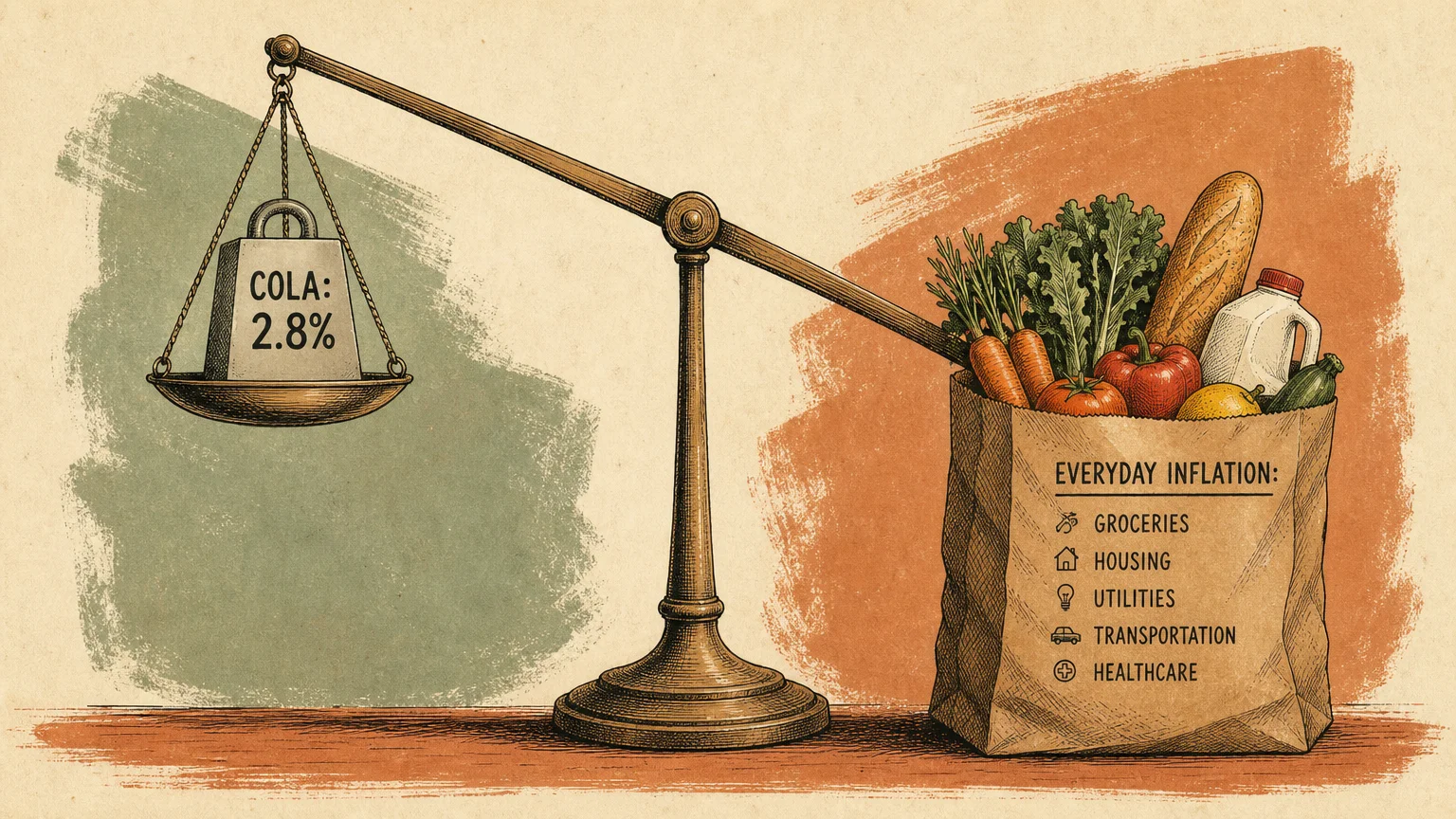

Everyday Essentials and the COLA Gap

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

To help retirees maintain their purchasing power, the Social Security Administration implements an annual Cost-of-Living Adjustment (COLA). The 2026 COLA was set at 2.8%. For the average retired worker receiving about $2,008 per month in late 2025, this adjustment adds roughly $56 to their monthly check, bringing the average benefit to $2,064 in 2026.

While any increase is welcome, the COLA often creates a false sense of security. The adjustment is calculated using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index measures the spending habits of younger, working-age individuals. Seniors, however, spend a vastly different proportion of their income on healthcare and housing—two categories that consistently inflate faster than general consumer goods. This structural mismatch creates the “COLA Gap,” where your official benefit increase fails to cover the actual rise in your grocery, utility, and medical bills.

Understanding this dynamic is crucial for setting realistic withdrawal rates from your personal savings.

| Financial Category | 2025 to 2026 Change | Impact on Your Budget |

|---|---|---|

| Social Security COLA | Increased by 2.8% | Adds roughly $56 to the average monthly check. |

| Medicare Part B Premium | Increased from $185.00 to $202.90 | Consumes a portion of your Social Security COLA before it hits your bank account. |

| IRS Standard Deduction (Single) | Increased from $15,750 to $16,100 | Lowers your taxable income, protecting more of your withdrawals from taxes. |

Pitfalls to Watch For

Managing a retirement budget is an active process. Avoiding common financial traps is just as important as generating good investment returns. Watch out for these frequent missteps:

- Putting Medicare on Autopilot: Automatically renewing your Medicare Advantage or Part D prescription drug plan without reviewing it is a costly mistake. Insurers tweak their covered drug lists, preferred pharmacy networks, and co-pays every year. Failing to compare plans can result in thousands of dollars in unnecessary out-of-pocket expenses.

- Ignoring the Senior Standard Deduction: Tax software has improved, but manual filers often overlook the extra standard deduction granted to taxpayers age 65 and older. Furthermore, missing out on the new $6,000 enhanced senior deduction (available through 2028) means handing the government money you are legally entitled to keep.

- Underestimating Longevity Risk: A budget that works perfectly at age 65 might collapse by age 85. Many retirees fail to account for the eventual cost of long-term care or home modifications. You must stress-test your budget to ensure your portfolio can withstand inflation over a three-decade horizon.

- Triggering Unnecessary IRMAA Surcharges: Liquidating a large stock position or executing a massive Roth IRA conversion can unexpectedly push your income over the Medicare IRMAA threshold. Always model the downstream Medicare consequences of any major financial move.

Getting Expert Help

You do not have to navigate the complexities of a retirement budget alone. While educating yourself is the best first step, certain financial crossroads require professional guidance. Consider hiring a fee-only, fiduciary financial planner or a certified tax professional in the following scenarios:

- Navigating RMDs and Tax Brackets: When you approach the age for Required Minimum Distributions, a tax professional can help you structure withdrawals across your traditional IRAs, Roth accounts, and taxable brokerages to keep you in the lowest possible tax bracket.

- Planning for Long-Term Care: If you are concerned about nursing home costs draining your estate, an elder law attorney or financial advisor can explain the nuances of Medicaid spend-down rules, long-term care insurance, and irrevocable trusts.

- Filing IRMAA Appeals: If you recently retired and your income dropped significantly, a professional can help you gather the necessary documentation to successfully petition the Social Security Administration for a reduction in your Medicare premiums.

Moving Forward with Confidence

Securing your retirement budget requires ongoing attention and a willingness to adapt. You cannot control macroeconomic inflation, Medicare premium hikes, or shifting tax laws, but you maintain complete control over how you respond to them. By actively managing your discretionary expenses, reviewing your insurance policies annually, and optimizing your tax strategy, you build a fortress around your hard-earned wealth. Take these adjustments one step at a time, focusing on the categories that impact your specific lifestyle the most.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.