Securing a U.S. green card unlocks profound financial and healthcare advantages for older adults, transforming how you plan and fund your retirement. As a lawful permanent resident, you gain access to critical safety nets, from Social Security retirement benefits to comprehensive Medicare coverage, effectively leveling the playing field between immigrants and U.S. citizens. Whether you are aiming to work a flexible consulting job without visa restrictions, sponsor your loved ones, or claim substantial senior tax deductions, a green card provides permanent stability. Understanding these ten powerful benefits ensures you maximize your financial security, avoid costly healthcare mistakes, and confidently navigate the rights afforded to you in your golden years.

1. Full Access to Social Security Retirement Benefits

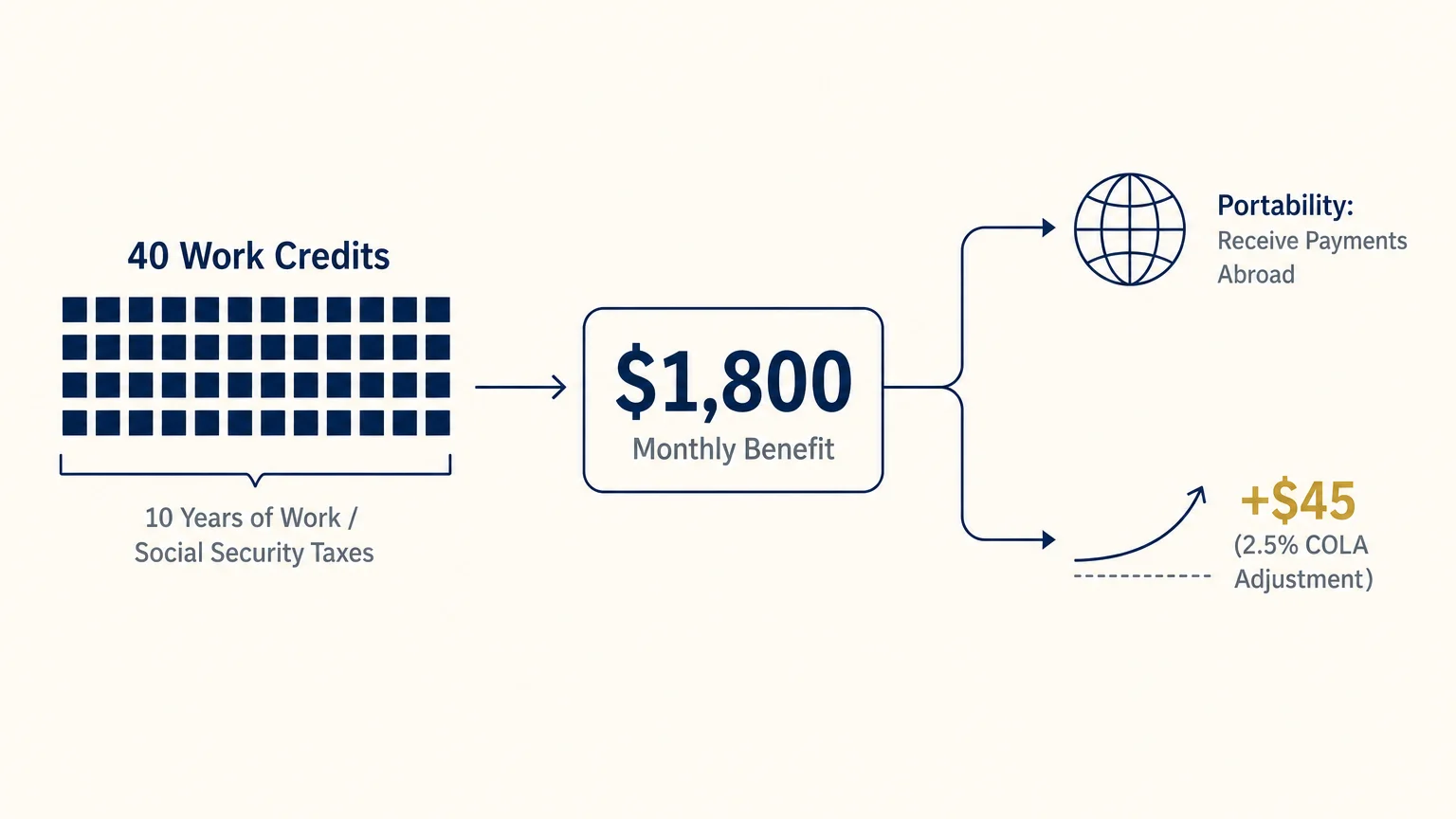

Once you secure your permanent resident status, you participate in the U.S. Social Security system exactly like a citizen. To qualify for retirement benefits, you must accumulate 40 work credits, which generally translates to 10 years of working and paying Social Security taxes. Your benefit amount is calculated based on your highest 35 years of earnings, providing a reliable stream of income that lasts for the rest of your life.

One of the most powerful features of this benefit is portability. If you decide to spend your golden years retiring in your home country or traveling the world, the Social Security Administration (SSA) allows permanent residents to continue receiving payments abroad in most nations. While a 30% federal withholding tax might apply depending on your destination and existing tax treaties, your hard-earned benefits remain yours. For example, if your calculated monthly benefit is $1,800, a standard 2.5% Cost-of-Living Adjustment (COLA) would add $45 to your monthly check, ensuring your purchasing power keeps pace with inflation regardless of where you live.

2. Comprehensive Medicare Eligibility at Age 65

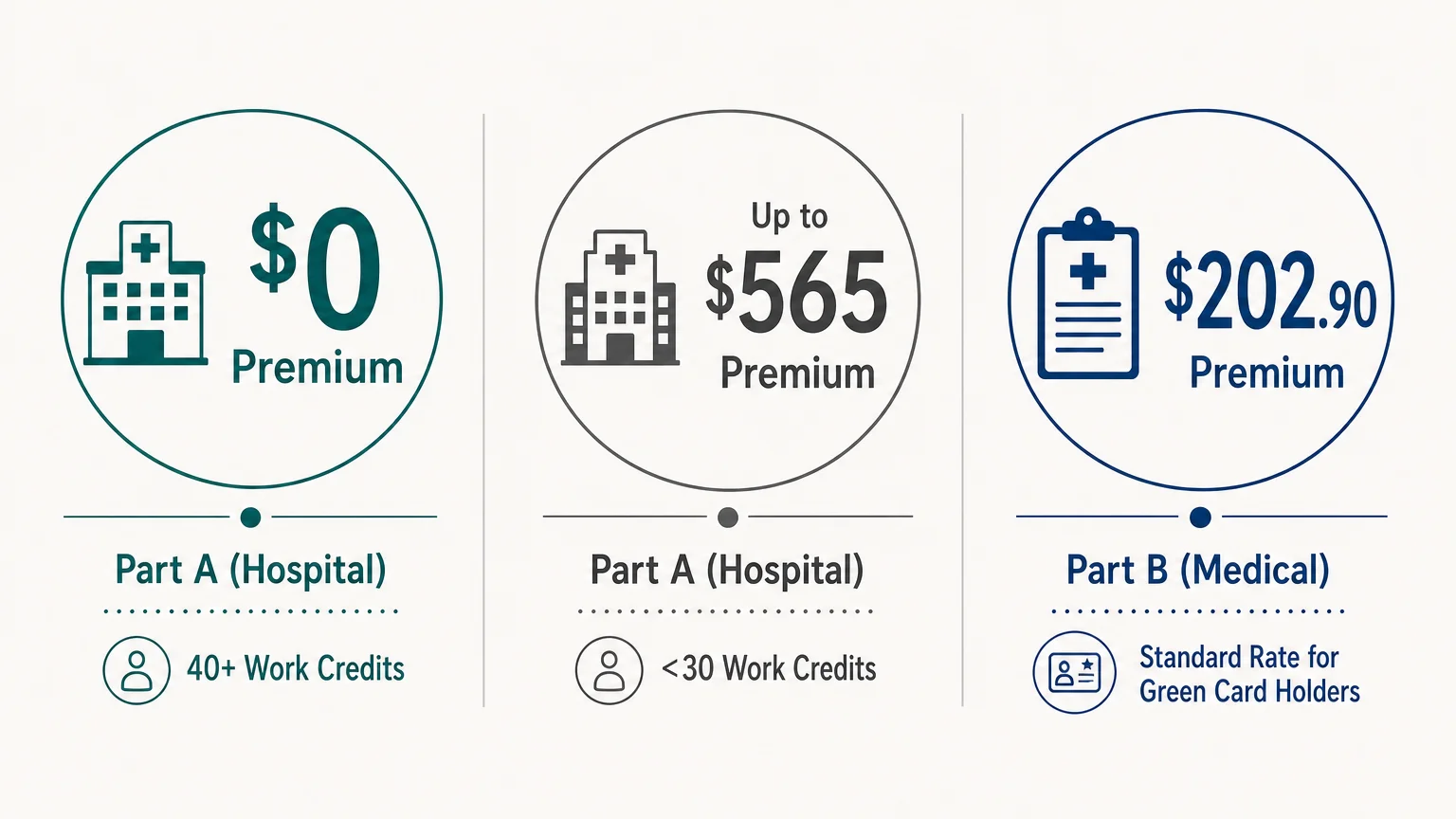

Healthcare costs routinely rank as the number one financial concern for older adults. Fortunately, your green card provides a direct pathway to Medicare. If you have earned 40 work credits, you qualify for premium-free Part A (Hospital Insurance) when you turn 65.

Even if you immigrated later in life and do not have the required 10-year work history, you are not locked out of the system. Green card holders can buy into Medicare, provided they have lived in the United States continuously for five years right before the month they apply. This is a massive advantage that protects you from the notoriously expensive private health insurance market.

| Medicare Coverage | 2026 Monthly Premium | Who Qualifies at This Rate? |

|---|---|---|

| Part A (Hospital) | $0 | Green card holders with 40+ work credits |

| Part A (Hospital) | Up to $565 | Green card holders with fewer than 30 work credits |

| Part B (Medical) | $202.90 | Most green card holders (standard rate) |

3. Access to Vital Safety Nets Like Medicaid and SSI

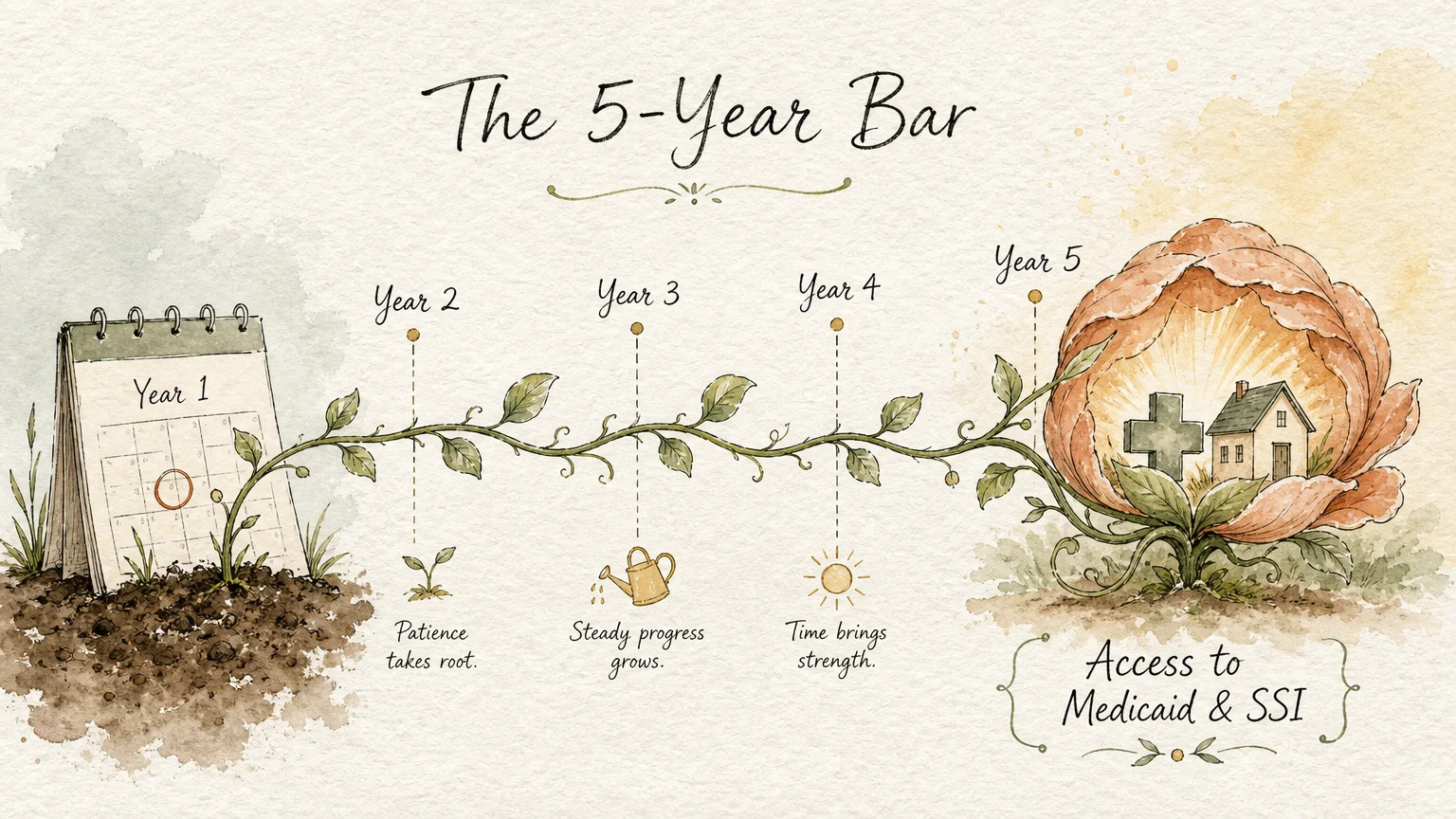

Financial hardships can occur unexpectedly in retirement. If your savings are depleted or you require expensive long-term care, holding a green card grants you access to federally funded safety net programs. However, federal law imposes a waiting period known as the “five-year bar”.

After you have held your green card for five years, you become eligible to apply for Medicaid (which can cover nursing home costs and out-of-pocket medical expenses) and Supplemental Security Income (SSI) for basic living assistance. Furthermore, many individual states use their own funds to waive this five-year waiting period, providing immediate access to certain state-level health benefits for low-income permanent residents. You can check state-specific programs through Benefits.gov.

4. Favorable Tax Treatment and New Senior Deductions

The IRS treats green card holders as U.S. tax residents. While this means you must declare your worldwide income, it also entitles you to the exact same lucrative tax deductions as U.S. citizens. For older adults, these deductions are substantial and can drastically reduce your tax burden.

When you file your taxes, you qualify for the standard deduction, plus the additional standard deduction for being age 65 or older. Furthermore, sweeping tax legislation has created massive opportunities. For instance, beginning in 2025, the Enhanced Senior Deduction offers an additional $6,000 deduction per eligible person age 65 or older.

“Your retirement savings are only as good as the amount you actually get to keep after taxes.” — Ed Slott, Retirement Tax Expert

If you are a married couple filing jointly and both spouses are 65 or older, combining the baseline standard deduction, the age 65 addition, and the new Enhanced Senior Deduction can shelter tens of thousands of dollars from federal income tax.

5. Total Employment Freedom for Your Second Act

Many older adults do not want to fully stop working at age 65. You might want to pivot to a part-time consulting role, turn a hobby into a small business, or sit on a corporate board. Temporary work visas tightly restrict who you can work for and how many hours you can log. A green card eliminates these barriers entirely.

You do not need an employer to sponsor you, and you do not have to worry about losing your visa if you decide to quit a stressful job. This employment freedom empowers you to structure your “second act” in retirement exactly how you see fit, generating supplemental income on your own terms.

6. The Ability to Sponsor Your Family Members

Retirement is meant to be shared with loved ones. As a lawful permanent resident, you have the legal right to sponsor specific family members for their own green cards. You can file Form I-130 to petition for your spouse and your unmarried children to join you in the United States.

While the process involves wait times based on visa availability categories, having the ability to initiate family reunification provides immense emotional relief. It ensures that you can build a multi-generational support system during your retirement years.

7. Freedom to Travel and Retire Internationally

Having a green card affords you tremendous flexibility to travel. If you want to spend the winter months in a warmer country or visit family overseas for an extended period, you can easily do so. You do not need to apply for temporary visas to re-enter the United States; your green card serves as your primary entry document.

There is a critical caveat to this freedom: your travel must be temporary. If you plan to remain outside the United States for a continuous year or more, you must apply for a Reentry Permit (Form I-131) before you leave. This document signals to the government that you are not abandoning your permanent U.S. residence, allowing you to enjoy long international stays without risking your immigration status.

8. Unrestricted Access to Property Ownership and Exemptions

Owning a home is a cornerstone of a secure retirement. Green card holders face no restrictions when buying real estate in the United States. In fact, government-backed mortgage entities like Fannie Mae and Freddie Mac treat lawful permanent residents exactly the same as U.S. citizens, meaning you have access to the same favorable interest rates and loan terms.

Beyond the purchase, establishing permanent residency qualifies you for valuable state-level senior property tax exemptions. Many states offer a “homestead exemption” or a “senior freeze” that locks in your property tax rate or drastically reduces the assessed value of your home. These programs almost always require the homeowner to be a legal permanent resident of the state.

9. Protection of Your Permanent Status

Immigration insecurity causes significant stress. A green card effectively ends that anxiety. While the physical card itself must be renewed every 10 years, your actual status as a lawful permanent resident does not expire. Unless you formally abandon your residency or commit a serious deportable offense, your right to live and retire in the United States is permanent.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

10. A Direct Pathway to U.S. Citizenship

Perhaps the most significant advantage of holding a green card is that it represents the final stepping stone to full U.S. citizenship. After maintaining continuous residence for five years (or three years if you are married to a U.S. citizen), you become eligible to apply for naturalization.

Becoming a citizen unlocks the right to vote, access to a U.S. passport, and absolute protection against deportation. It also removes all restrictions on international travel duration and exempts you from the estate tax limitations that apply to non-citizen spouses. Your green card is the master key that opens this final door.

Pitfalls to Watch For

While a green card provides incredible advantages, certain mistakes can jeopardize your finances or your legal status. Watch out for these common traps:

- Abandoning your status accidentally: If you retire abroad and spend more than 365 continuous days outside the U.S. without obtaining a Reentry Permit, Customs and Border Protection may determine you have abandoned your residency.

- Failing to report global income: Because you are a U.S. tax resident, the Internal Revenue Service (IRS) requires you to report all income earned globally. You must also file an FBAR (Foreign Bank and Financial Accounts Report) if the aggregate value of your foreign accounts exceeds $10,000 at any point in the year. Failing to do so carries steep penalties.

- Missing Medicare enrollment windows: Even if you do not have 40 work credits and have to pay for Part A and Part B out of pocket, you must sign up during your Initial Enrollment Period around your 65th birthday. Missing this window can result in permanent late enrollment penalties.

- Confusing the card with the status: Your physical green card expires every 10 years and must be renewed using Form I-90. However, letting the card expire does not mean you lose your permanent resident status—it just makes it very difficult to prove your right to work or re-enter the country.

Getting Expert Help

Managing the intersection of immigration status, international taxation, and retirement benefits can be complex. Consider consulting professionals in these specific scenarios:

- If you plan to retire abroad: Work with a Certified Public Accountant (CPA) who specializes in expatriate taxes. They can help you navigate foreign tax credits and ensure your global assets are reported correctly.

- If you need healthcare guidance: Navigating the 5-year continuous residence rule for Medicare.gov buy-in can be tricky. Reach out to your local State Health Insurance Assistance Program (SHIP) for free, unbiased counseling on Medicare eligibility.

- If you are approaching the 5-year mark: Consult an immigration attorney to review your travel history and prepare your naturalization application (Form N-400) to ensure a smooth transition to citizenship.

Frequently Asked Questions

Do I get Medicare for free as a green card holder?

Not automatically. You receive premium-free Part A (Hospital Insurance) only if you or your spouse have accumulated 40 work credits (roughly 10 years of work) in the U.S. Everyone, including citizens, pays a monthly premium for Part B (Medical Insurance). If you lack the work history, you can buy into Part A after living in the U.S. continuously for five years.

Can I receive Social Security if I move back to my home country?

Yes, in most cases. Permanent residents who have earned their 40 work credits can receive their Social Security retirement checks in dozens of countries worldwide. However, you should verify with the SSA, as some countries face U.S. Treasury payment restrictions, and non-citizens may be subject to a 30% withholding tax depending on international treaties.

Does the five-year bar apply to all government assistance?

The five-year bar generally applies to federal means-tested benefits like Medicaid, SSI, and SNAP (food stamps). However, there are exceptions for refugees, asylees, and military veterans. Additionally, some states use their own funding to provide emergency medical assistance or nutritional support to permanent residents before the five years have passed.

As you navigate your retirement years, your green card serves as a powerful tool for financial stability and personal freedom. By understanding the rules surrounding Medicare, Social Security, and taxes, you can build a secure, comfortable life without fear of losing your legal footing.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.