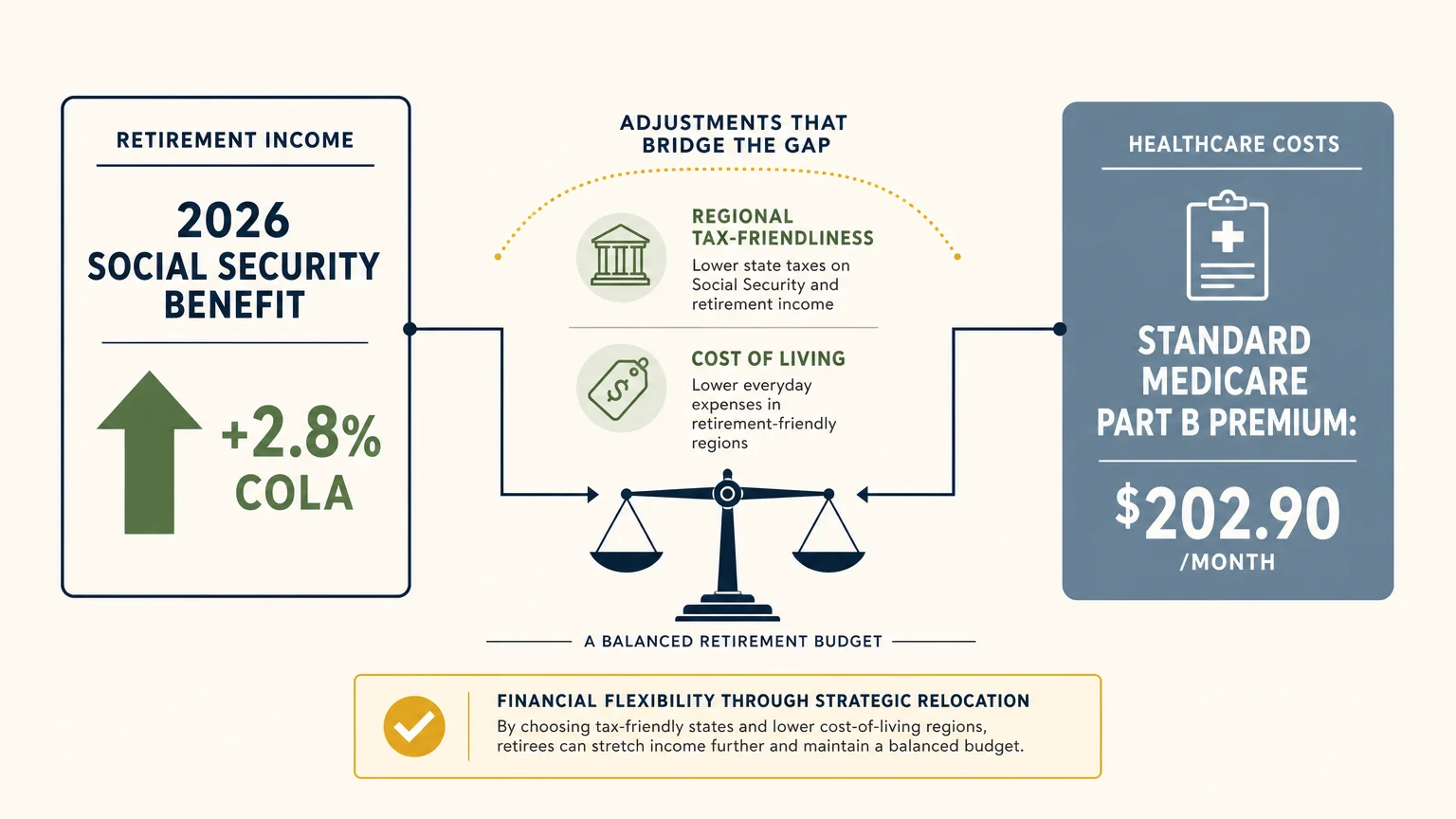

Finding the perfect retirement town means looking beyond sunny skies to balance everyday affordability with top-tier healthcare and community engagement. Where you choose to live impacts how far your 2026 Social Security benefit stretches—especially with the 2.8% cost-of-living adjustment and the standard $202.90 monthly Medicare Part B premium. High life satisfaction in retirement requires tax-friendly policies, accessible medical networks, and a built-in social infrastructure. From the tax advantages of the Sun Belt to the excellent hospital systems of the Midwest, we evaluated destinations where older adults report the highest levels of well-being. Explore these twelve towns that perfectly blend financial stability with an exceptional quality of life.

What Drives Retiree Happiness?

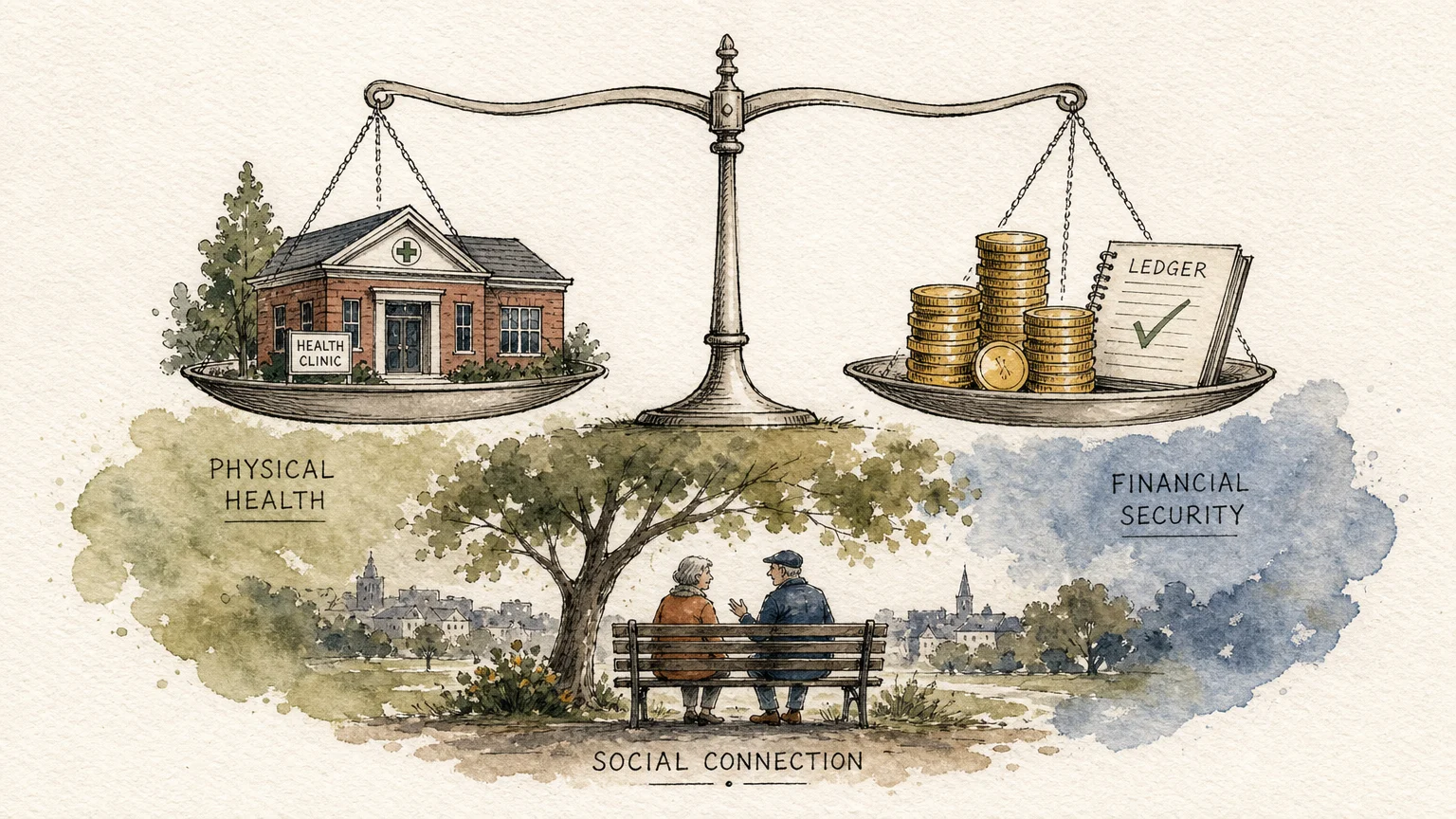

When you leave the workforce, your priorities naturally shift. While you might have previously chosen a city based on job markets or school districts, retirement planning requires a completely different set of metrics. Studies consistently show that retirees with the highest life satisfaction scores live in communities that support their financial security, physical health, and social connection.

Healthcare access stands out as the most critical factor. As you age, proximity to high-quality medical facilities becomes non-negotiable. Top-rated retirement towns boast robust local hospital systems and a high concentration of specialists who accept Medicare. Furthermore, financial stability plays a massive role in reducing stress. States that do not tax Social Security benefits or offer generous exclusions for pension and IRA withdrawals allow you to keep more of your hard-earned money.

“A good retirement isn’t just about the money you’ve saved; it’s about the life you’ve built and the community you choose to surround yourself with.” — Jean Chatzky, Financial Editor and Author

Finally, community infrastructure determines your daily joy. Walkable neighborhoods, accessible public transportation, continuing education opportunities, and recreational facilities prevent isolation. Towns that score highly for retiree well-being intentionally design spaces where older adults can safely and easily engage with their neighbors.

12 Towns With the Highest Retiree Life Satisfaction

Based on comprehensive data evaluating cost of living, healthcare quality, tax burden, and overall well-being indices, here are twelve exceptional towns where older adults report thriving in retirement.

1. Sarasota, Florida

Florida remains a perennial favorite for retirees, and Sarasota consistently ranks at the top for life satisfaction. Beyond the obvious draw of pristine Gulf Coast beaches and warm weather, Sarasota offers a highly regarded medical network anchored by the Sarasota Memorial Health Care System. Financially, Florida residents benefit from zero state income tax, meaning your Social Security benefits, pension payouts, and IRA withdrawals are entirely yours to keep. The city also features a rich cultural scene, including the Sarasota Opera and numerous art galleries, keeping residents intellectually engaged.

2. Winchester, Virginia

If you prefer a four-season climate without the extreme winters of the Northeast, Winchester is an outstanding choice. Located in the beautiful Shenandoah Valley, this historic town of about 27,000 residents offers a cost of living roughly 8% below the national average. Housing remains relatively affordable, with median home prices sitting comfortably below coastal city averages. Virginia offers a very decent retiree tax climate; the state does not tax Social Security benefits, and residents enjoy excellent air quality and a highly walkable downtown area.

3. Lancaster, Pennsylvania

Lancaster seamlessly blends picturesque farmland with a vibrant, easily navigable downtown. Pennsylvania is one of the most tax-friendly states for retirees; the state completely exempts Social Security benefits, and eligible pensions and distributions from 401(k)s or IRAs are generally tax-free after age 59 and a half. Lancaster offers top-tier medical facilities and a lower cost of living than nearby major metros like Philadelphia or New York, allowing your fixed income to cover a highly comfortable lifestyle.

4. Ann Arbor, Michigan

Retirees who value lifelong learning and world-class healthcare flock to Ann Arbor. Home to the University of Michigan, the city provides unmatched access to one of the nation’s premier hospital systems. While the winters require preparation, the community compensates with a robust infrastructure of senior services, cultural events, and continuing education programs. Michigan recently rolled back taxes on retirement income, implementing a phased-in exemption that provides significant relief for older adults drawing from pensions and 401(k) accounts.

5. Boulder, Colorado

For the highly active retiree, Boulder is frequently cited as one of the healthiest cities in America. The local culture prioritizes outdoor recreation, wellness, and environmental consciousness. While housing costs in Boulder run higher than the national average, Colorado offers generous state tax deductions for retirement income. Residents aged 65 and older can generally exclude a significant portion of their pension and annuity income, helping to offset the premium cost of living in this mountain-adjacent haven.

6. Naples, Florida

When measuring pure longevity, Naples stands out; residents here boast an average life expectancy of over 84 years, one of the highest in the nation. This affluent Gulf Coast city caters extensively to an older demographic, meaning healthcare services, recreational facilities, and community layouts are heavily optimized for seniors. The lack of state income tax maximizes your spending power, though you must carefully budget for higher real estate prices and coastal property insurance premiums.

7. Barnstable, Massachusetts

Located on Cape Cod, Barnstable frequently tops wellness surveys for its incredibly high community well-being scores. It features a massive network of fellow retirees, minimizing the risk of social isolation. While Massachusetts does have a state income tax, it does not tax Social Security benefits, and it exempts income from certain government pensions. The area offers incredible summer weather, beautiful coastal scenery, and a surprisingly robust localized healthcare system tailored to an aging population.

8. Raleigh, North Carolina

Part of the famous Research Triangle, Raleigh attracts retirees who want moderate weather, a booming economy, and exceptional medical care. The proximity to Duke University Hospital and UNC Medical Center ensures you will never have to travel far for specialized treatments. North Carolina features a flat state income tax rate and exempts all Social Security benefits. The cost of living remains reasonable compared to northern coastal cities, making it a financial sweet spot for many relocators.

9. Midland, Michigan

Midland is gaining rapid attention as a hidden gem for budget-conscious retirees. With median home prices significantly below the national average, relocating to Midland allows you to downsize and potentially eliminate your mortgage entirely. The town is highly rated for its safety, walkability, and access to nature. If you are looking to maximize the purchasing power of your Social Security Administration benefits while still enjoying a strong sense of community, Midland requires serious consideration.

10. Georgetown, Texas

Georgetown regularly ranks as one of the fastest-growing cities in the country, largely driven by retirees seeking a warm climate and favorable tax environment. Texas levies no state income tax, making it a powerful wealth-preservation state. The town is famous for its beautiful Victorian town square and massive master-planned active adult communities. You also benefit from being just a short drive from Austin, providing access to major airport hubs and specialized medical centers.

11. Carmel-by-the-Sea, California

If you have a robust retirement portfolio and dream of a premium coastal lifestyle, Carmel-by-the-Sea offers unparalleled beauty and a deeply engaged community. California is notoriously expensive and heavily taxes most forms of retirement income; however, it notably does not tax Social Security benefits. For those who can afford the high housing costs, Carmel provides a magical, pedestrian-friendly village atmosphere, incredible weather, and a fiercely protective community spirit.

12. Fort Collins, Colorado

Rounding out the list is Fort Collins, a city that offers a slightly more affordable alternative to Boulder while delivering the same active, outdoor-centric lifestyle. Situated at the foothills of the Rocky Mountains, the city features miles of paved biking trails, excellent local healthcare, and a vibrant downtown. The strong community resources dedicated to older adults make it easy to transition into the area and build a new social circle.

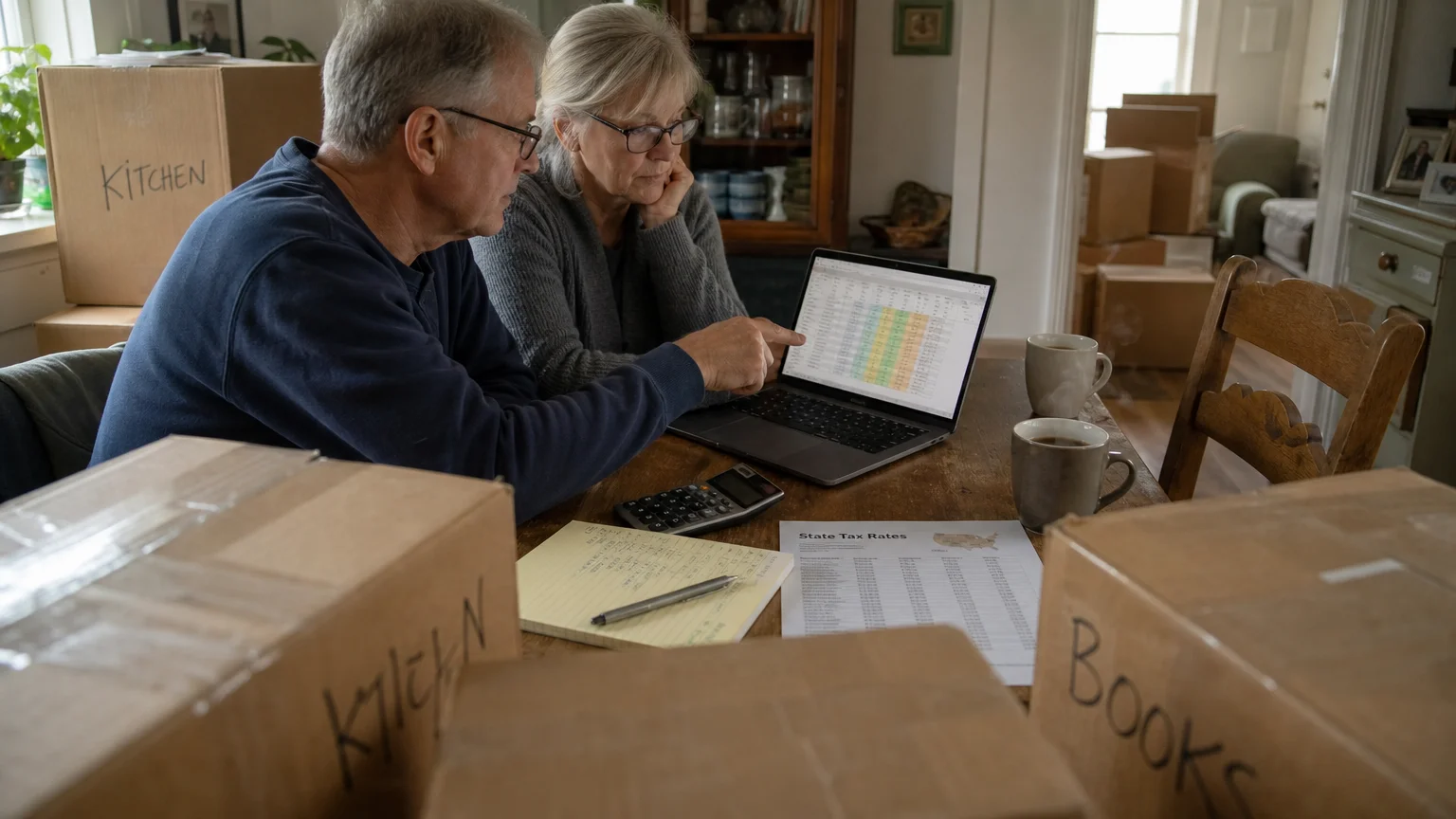

Evaluating the Financial Impact of Relocating

Before you pack your bags, you must perform a comprehensive financial analysis. A town with cheap housing might hide exorbitant property taxes, while a state with no income tax might have high sales taxes that quietly drain your budget. According to IRS.gov, your tax liability shifts dramatically the moment you establish residency in a new state.

Below is a general comparison of how different popular retirement states treat your income:

| State | Taxes Social Security? | Taxes Pensions & 401(k)s? | General Cost of Living |

|---|---|---|---|

| Florida | No | No | Moderate to High (Insurance) |

| Pennsylvania | No | No (for most qualifying plans) | Moderate |

| Michigan | No | Partially Exempt | Low to Moderate |

| Colorado | No | Generous Deductions | High |

| North Carolina | No | Yes (Standard Rate) | Moderate |

“Pay taxes now — at historically low rates — so you can avoid paying more later.” — Ed Slott, CPA and Retirement Tax Expert

As Ed Slott points out, strategic tax planning is critical. If you are relocating to a state that taxes IRA withdrawals, you might want to consider executing Roth conversions before you move, depending on the tax brackets of your current state versus your destination.

Common Mistakes to Avoid When Relocating

Relocating in retirement is a major life event. Avoid these common financial and logistical missteps to ensure a smooth transition:

- Failing to verify Medicare Advantage networks: If you use a Medicare Advantage plan (Part C), your coverage is usually regional. Moving out of your plan’s service area requires you to enroll in a new plan. Check Medicare.gov to ensure your preferred doctors in the new town are in-network.

- Ignoring hidden housing costs: A cheaper mortgage can be quickly offset by steep property taxes, high homeowners association (HOA) fees, or extreme weather insurance premiums (especially in coastal areas like Florida or wildfire-prone zones).

- Moving solely for tax breaks: Choosing a town purely because it lacks an income tax can backfire if you find yourself isolated from family, friends, and the activities you love. Mental health and social connection carry intrinsic value that transcends tax savings.

- Not doing a trial run: Visiting a town for a week on vacation is entirely different from living there year-round. Rent an Airbnb for a month during the area’s worst weather season before committing to a permanent move.

Finding the Right Advisor

Relocating across state lines involves complex tax and estate planning. You should consider consulting a qualified financial professional if you face any of the following scenarios:

- Selling a primary residence: If you have lived in your home for decades, you may face significant capital gains. An advisor can help you navigate the IRS Section 121 exclusion to shield up to $500,000 (for married couples) of your home sale profit from taxes.

- Navigating state estate taxes: Even if your estate falls below the federal estate tax exemption, several states levy their own estate or inheritance taxes at much lower thresholds. An advisor can help you structure your assets to protect your heirs.

- Managing required minimum distributions (RMDs): If your relocation coincides with reaching your RMD age, a financial planner can help you time your withdrawals to minimize the tax hit in your new state.

Frequently Asked Questions

- How does moving to a new state affect my Social Security payments?

Moving to a new state does not change the gross amount of your federal Social Security benefit. However, it may change your net income. While the federal government taxes Social Security based on your combined income, only a small handful of states currently tax Social Security at the state level. Moving from a state that taxes these benefits to one that does not will increase your take-home pay. - Will my Medicare coverage follow me if I move?

Original Medicare (Part A and Part B) is a federal program and is accepted by participating providers anywhere in the United States. However, if you have a Medicare Advantage plan or a standalone Part D prescription drug plan, you will likely need to switch plans because these are tied to specific geographic service areas. - What happens to my standard deduction if I move?

Your federal standard deduction remains the same regardless of where you live in the U.S. (For 2026, seniors aged 65 and older continue to enjoy an additional standard deduction amount on top of the base federal standard deduction). However, state-level standard deductions and personal exemptions vary wildly. You must check the specific tax code of your new resident state.

Choosing the best town for your retirement involves blending your lifestyle desires with cold, hard financial realities. Whether you prioritize the tax-free sunshine of Florida or the intellectual stimulation and healthcare infrastructure of a university town in Michigan, the key to life satisfaction is preparation. Take the time to run the numbers, visit the communities, and envision your daily life in these top-rated destinations.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.