Saving for retirement can feel like trying to hit a moving target, especially when living costs keep rising. If you have been doing your best to set money aside, you are about to get some significant help. Starting January 1, 2027, the federal government will begin depositing up to $1,000 directly into eligible retirement accounts through a new program called the Saver’s Match. Unlike complicated tax deductions that only help high earners, this initiative is designed specifically to boost the savings of low- and moderate-income Americans. By understanding the rules right now, you can position your finances this year to capture this guaranteed matching money as soon as the program goes live.

What Exactly Is the Saver’s Match?

The SECURE 2.0 Act, passed by Congress in 2022, introduced sweeping changes to how Americans plan for their golden years. One of the most impactful provisions is the creation of the Saver’s Match, which officially takes effect on January 1, 2027. This program represents a fundamental shift in how the federal government rewards working citizens who prioritize their retirement.

For decades, the government offered a tax break known as the Saver’s Credit. It was meant to incentivize lower- and middle-income workers to put money into their retirement accounts. However, because it was a nonrefundable tax credit, it only benefited people who actually owed federal income taxes. If your income was low enough that you did not owe any federal tax—a common scenario for part-time workers and semi-retirees—the credit provided exactly zero value to you.

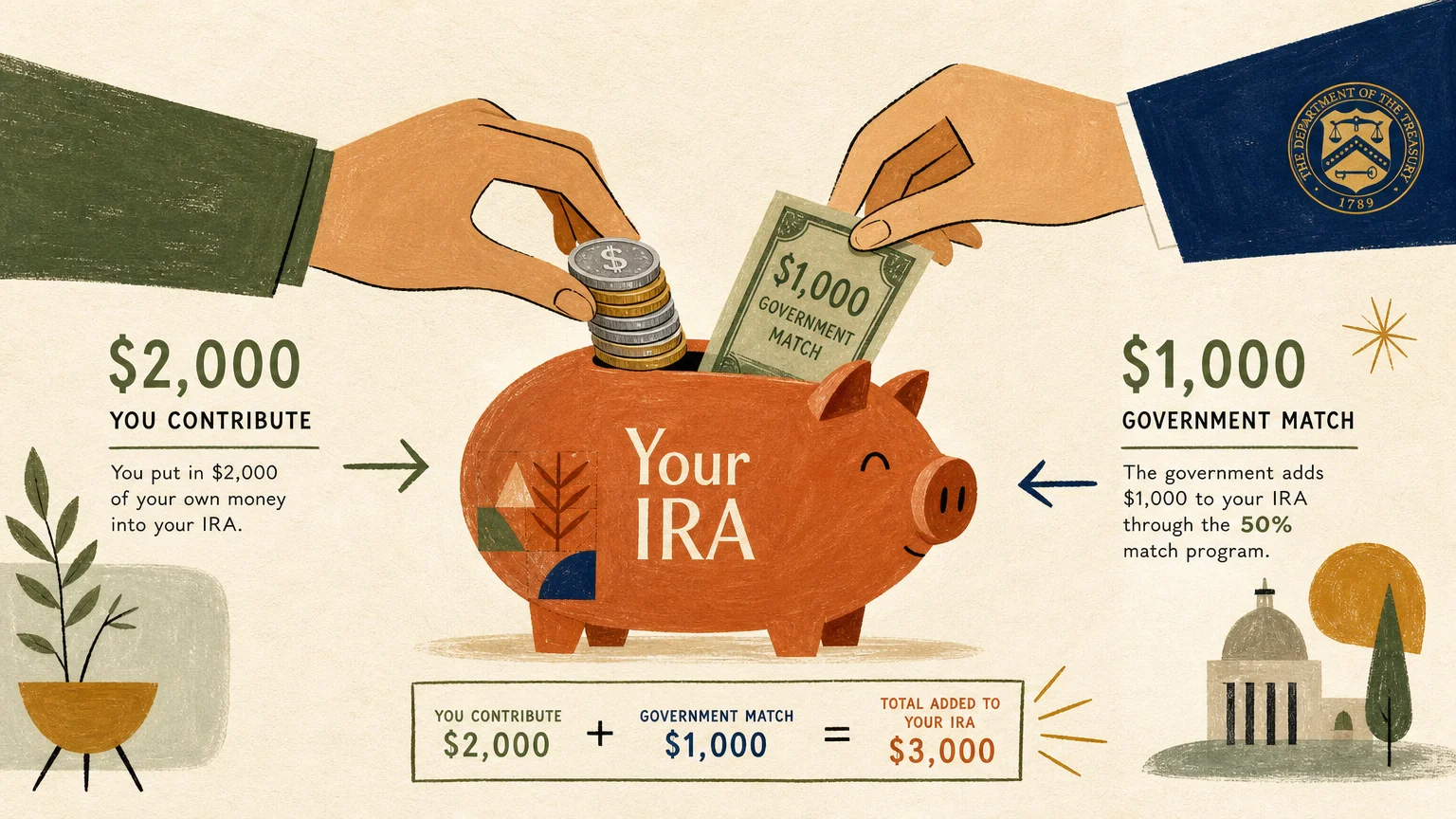

The Saver’s Match completely rewrites this rule. Starting in 2027, the federal government will offer a 50% matching contribution on the first $2,000 you save in an eligible retirement account. This means if you contribute $2,000 over the course of the year, the Treasury will deposit an additional $1,000 directly into your Individual Retirement Account (IRA) or workplace 401(k).

This is effectively free money from the government, designed to boost your long-term compounding interest. Even if you only manage to save $500 in a given year, the government will step in and add $250. Because the match is fully refundable, you will receive this deposit regardless of whether you owe federal income taxes. For many Americans, this will be the first meaningful federal retirement benefit they have ever qualified to receive.

Do You Qualify for the Government Match?

The new Saver’s Match is heavily targeted toward low- and moderate-income earners. This makes it particularly valuable for seniors who are working part-time, those transitioning into retirement, or individuals living on a fixed income who still generate a small amount of taxable wages.

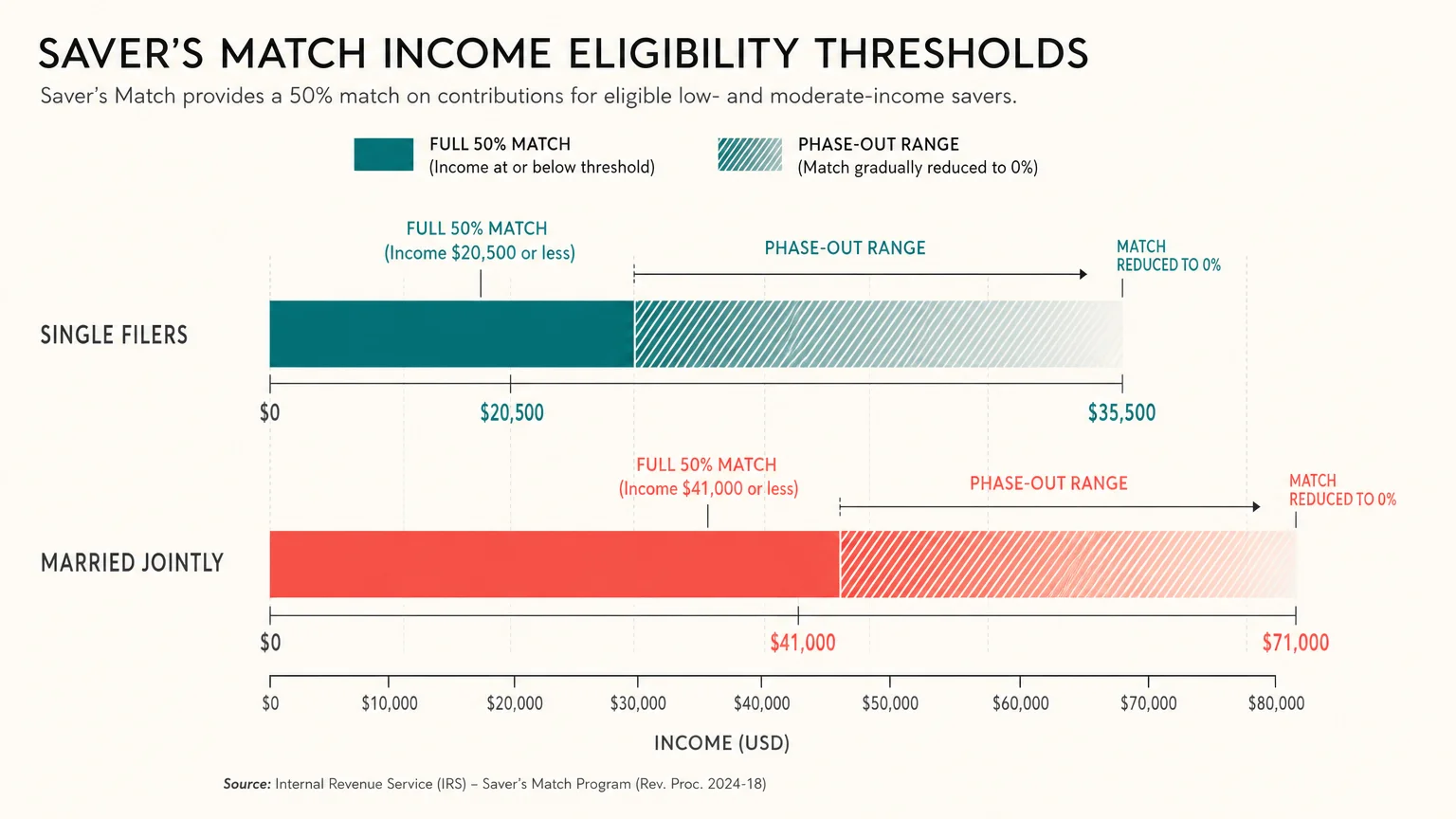

Eligibility is based entirely on your tax filing status and your Modified Adjusted Gross Income (MAGI). While the exact figures for 2027 will eventually be adjusted for inflation, the baseline income thresholds established by the SECURE 2.0 Act are as follows:

- Single Filers and Married Filing Separately: You receive the full 50% match if your income is $20,500 or less. The match percentage gradually phases out as you earn more, dropping to zero once your income reaches $35,500.

- Married Couples Filing Jointly: You receive the full 50% match if your joint household income is $41,000 or less. The benefit phases out completely when your joint income hits $71,000.

- Heads of Household: You receive the full match if your income is $30,750 or less, with the phase-out range ending completely at $53,250.

If you are married and filing jointly, both you and your spouse can claim the match independently, as long as you both have eligible income and make contributions. That means a qualifying married couple could theoretically receive up to $2,000 in combined matching funds from the government every single year.

It is crucial to note that you must have “earned income” to contribute to an IRA and qualify for the match. Pensions, Social Security benefits, and passive investment dividends do not count as earned income. However, if you have a part-time job, consulting income, or freelance wages, those earnings allow you to participate and claim the government funds.

The Old Saver’s Credit vs. The New Saver’s Match

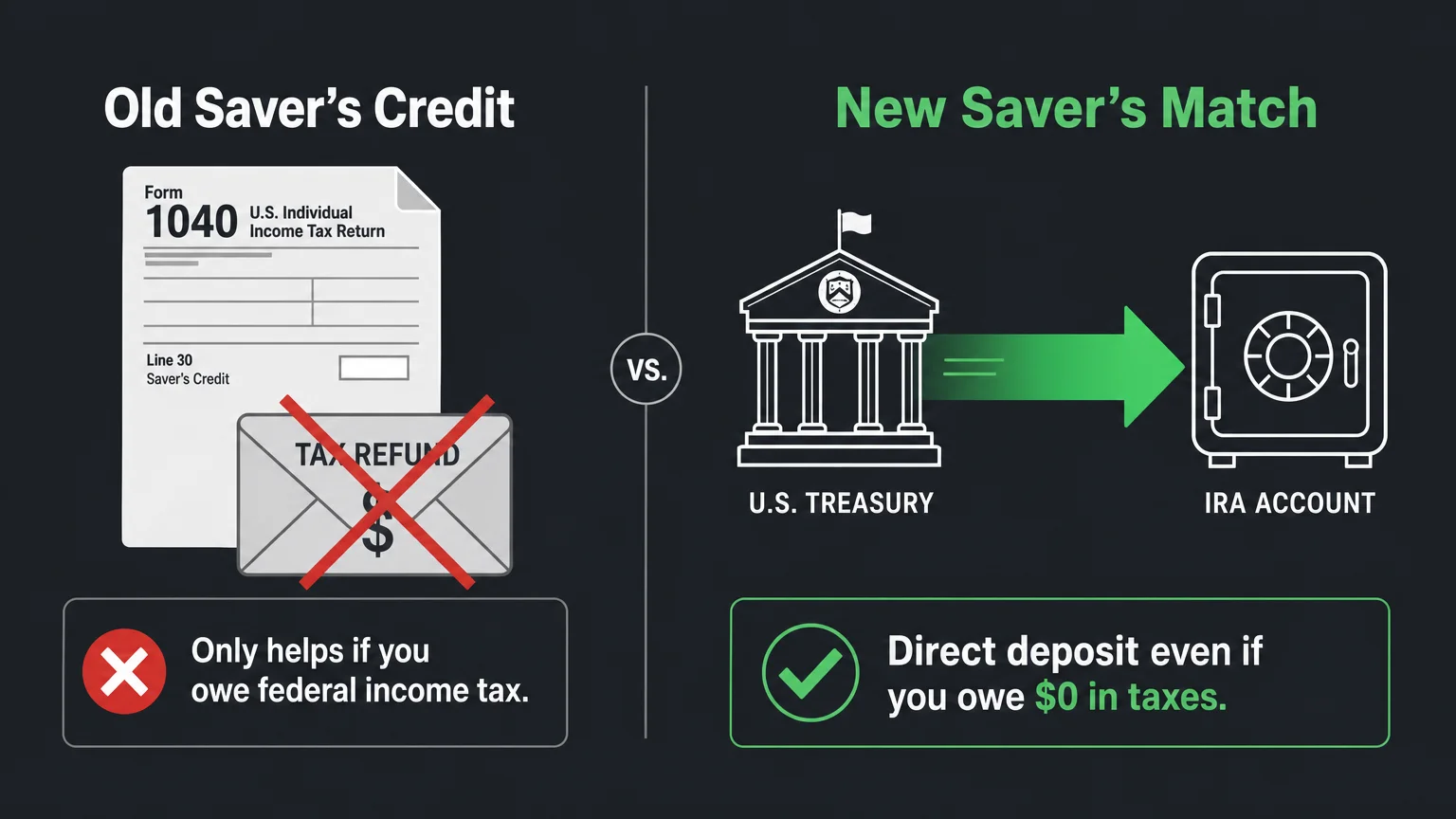

To truly understand why the Saver’s Match is a game-changer, it helps to look at the program it is replacing. The old Saver’s Credit was notoriously underutilized by the public. According to the Pew Charitable Trusts, only about 5.7% of eligible taxpayers claimed the old credit in 2021, receiving an average of just $191. The old system simply did not reach the people who needed it most.

Here is a direct breakdown of how the old rules compare to the upcoming 2027 guidelines:

| Feature | The Old Saver’s Credit (Ending 2026) | The New Saver’s Match (Starting 2027) |

|---|---|---|

| How You Receive It | A reduction in your calculated federal tax bill. | A direct cash deposit into your IRA or 401(k). |

| Refundability | Nonrefundable; if you owe $0 in taxes, you get $0. | Fully refundable; you receive the match even if you owe $0 in taxes. |

| Maximum Amount | Up to $1,000, but often much less due to low tax liability. | A guaranteed 50% match up to $1,000 per person. |

| Impact on Savings | Provides no direct impact on your retirement account balance. | Directly increases your invested retirement assets and compound interest. |

By shifting the benefit from a quiet tax reduction to a tangible direct deposit, the government ensures that the money goes exactly where it is needed: into your long-term investment portfolio.

How to Maximize Your IRA Contributions in 2026

While the Saver’s Match does not officially begin until 2027, the absolute best time to prepare your finances is right now. We are currently navigating the 2026 financial landscape, and the Internal Revenue Service (IRS) has increased contribution limits to help you save more aggressively.

For the 2026 tax year, you can contribute up to $7,500 to a Traditional or Roth IRA. If you are age 50 or older, you are eligible for an additional “catch-up” contribution of $1,100, bringing your total allowable IRA contribution to an impressive $8,600 for the year.

These higher limits are especially important considering the current economic climate seniors face. In 2026, the Social Security Administration (SSA) implemented a 2.8% Cost-of-Living Adjustment (COLA). While this bump provides helpful relief at the grocery store, seniors are simultaneously battling rising healthcare costs. The standard Medicare Part B premium increased to $202.90 per month for 2026.

With essential living expenses taking up a larger portion of your monthly budget, taking advantage of tax-advantaged accounts—and eventually the Saver’s Match—is critical for your financial stability.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Investor and Philanthropist

If you establish a solid savings habit in 2026, you will be perfectly positioned to easily redirect $2,000 into your IRA in 2027. By doing so, you can automatically capture the full $1,000 government match as soon as the program launches. Think of your 2026 contributions as a practice run for the free money available next year.

Pitfalls to Watch For

While the Saver’s Match is an incredible wealth-building opportunity, the government has established strict rules you must follow. A simple clerical error or misunderstanding could cost you the entire match. Here are the most common pitfalls seniors need to avoid:

- Assuming the Match Is Automatic: The Treasury will not simply look at your bank account and blindly send you a check. You must officially claim the Saver’s Match by filing your federal tax return. Even if your income is so low that you are not typically required to file taxes, you will need to submit a return in 2028 (for the 2027 tax year) to trigger the government deposit.

- Withdrawing the Funds Too Early: The government is providing this money specifically for your long-term retirement security. If you withdraw the matched funds early, you will face severe penalties. The IRS has rules in place to claw back the match if you take an early distribution from your account before reaching the qualifying retirement age.

- Miscalculating Your Income: Because the match phases out at specific income thresholds, earning just a few extra dollars could significantly reduce your match percentage. If you are near the upper limit of the phase-out range (for example, approaching $35,500 as a single filer), be mindful of how additional part-time work or taxable account withdrawals might accidentally increase your MAGI.

- Not Having an Eligible Account Set Up: The government needs a designated place to deposit the funds. You must have an active, eligible retirement account—such as a Traditional IRA, Roth IRA, or a workplace 401(k)—ready to accept the transfer. The funds cannot be deposited into a standard checking or savings account.

Getting Expert Help

Navigating the transition from working full-time to relying on retirement income can be complex. You might find yourself juggling Social Security claims, Medicare enrollment, and IRA management all at once. Seeking professional guidance is often the smartest move to ensure you do not leave money on the table.

Consider consulting a fee-only fiduciary financial advisor or a Certified Public Accountant (CPA) in the following scenarios:

- You are planning your tax strategy: An expert can help you calculate your exact MAGI and ensure you fall safely within the income thresholds for the Saver’s Match.

- You are managing Required Minimum Distributions (RMDs): If you are over age 73 (or 75, depending on your birth year), withdrawing from traditional retirement accounts will increase your taxable income. A professional can help you manage these withdrawals so they do not push you out of the eligibility range for the match.

- You are setting up a new IRA: If you do not currently have an IRA, organizations like AARP and the Consumer Financial Protection Bureau (CFPB) offer educational resources, but a professional can personally help you choose a low-cost brokerage firm and explain the intricate differences between Traditional and Roth options.

Frequently Asked Questions

If I contribute to a Roth IRA, does the government match go into the Roth account?

Yes, the Saver’s Match can be deposited directly into a Roth IRA. However, under the current SECURE 2.0 guidelines, matching funds provided by the government are treated as pre-tax money. This means that while your own personal Roth contributions will remain tax-free upon withdrawal, the $1,000 government match (and its subsequent investment earnings) will likely be subject to ordinary income tax when you eventually withdraw it during retirement.

Can I get the match if I am already collecting Social Security?

Yes, but only if you also have “earned income” from a job or self-employment. Social Security benefits do not count as earned income for the purpose of making IRA contributions. If your absolute only source of income is your monthly Social Security check, you cannot contribute to an IRA or claim the Saver’s Match. If you work a part-time job while collecting Social Security, you can participate based strictly on your job earnings.

What if my spouse works, but I do not?

If you are married and file a joint tax return, you can utilize a “Spousal IRA.” This allows the non-working spouse to contribute to an IRA based entirely on the working spouse’s income. In this specific scenario, both spouses could potentially contribute $2,000 each to their respective accounts and receive a combined match of $2,000 from the government, provided their total joint income falls within the eligibility limits.

Is the $1,000 match counted toward my annual IRA contribution limit?

No. The government’s matching contribution does not count against your personal annual contribution limit. For example, if the IRA limit is $7,500, you are still legally allowed to contribute your full $7,500 out of pocket. The $1,000 government match will simply be added on top of your contribution, accelerating your account growth without penalizing your saving capacity.

The shift from the Saver’s Credit to the new Saver’s Match is a landmark change that will help millions of Americans secure a more comfortable future. By removing the strict requirement to owe federal taxes and providing a direct cash deposit into your IRA, the government is offering an unprecedented incentive to build your nest egg. You do not have to wait until 2027 to start preparing. Review your current budget, consider adjusting your part-time working hours to stay within the upcoming income limits, and establish a comfortable savings routine today.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.