Tax season doesn’t have to be a source of stress if you make strategic money moves long before the filing deadline. By organizing your documents, maximizing your retirement contributions, and managing your taxable income right now, you can lower your final tax bill and keep more of your hard-earned money. For seniors in 2026, shifting tax brackets and newly adjusted standard deductions present both hidden traps and valuable opportunities to shield your wealth from the IRS. This guide breaks down six practical, actionable steps you can take today to protect your retirement income. From navigating the new Medicare IRMAA limits to optimizing your IRA catch-up contributions, executing these strategies mid-year puts you in total control.

1. Maximize Your 2026 Catch-Up Contributions

One of the most effective ways to lower your taxable income—or build a reservoir of tax-free wealth for the future—is to take full advantage of IRS catch-up contributions. Once you turn 50, the government allows you to set aside extra money in your retirement accounts beyond the standard limits. If you have not reviewed your contribution amounts recently, mid-year is the perfect time to adjust your automated deposits.

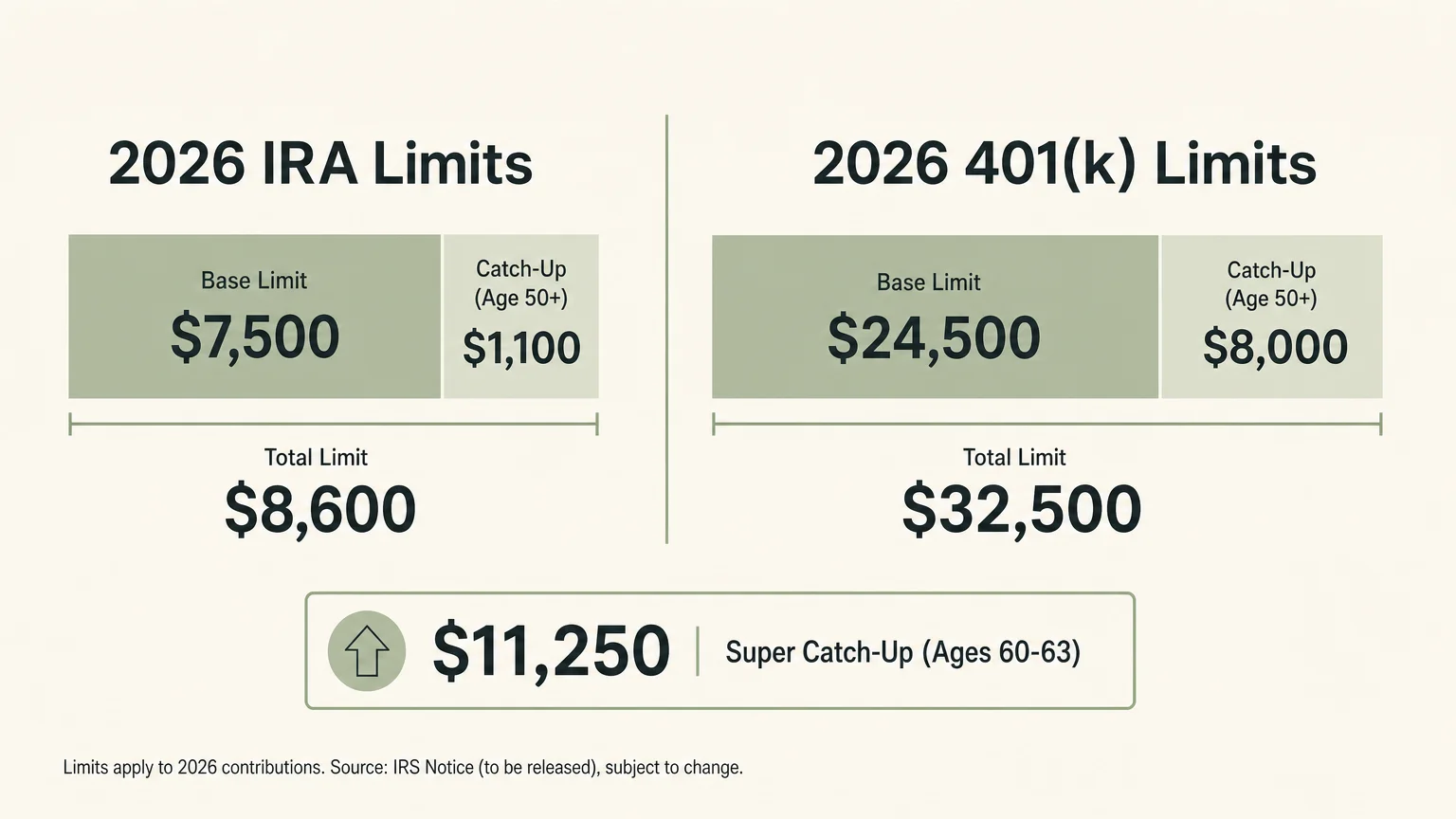

For the 2026 tax year, the Internal Revenue Service has adjusted several contribution limits to account for inflation. The standard limit for Individual Retirement Accounts (IRAs) is $7,500. However, if you are 50 or older, you are eligible for an additional $1,100 catch-up contribution, bringing your total allowable IRA contribution to $8,600 for the year.

If you are still working and have access to an employer-sponsored plan like a 401(k), 403(b), or TSP, the opportunity is even larger. The base 401(k) contribution limit for 2026 is $24,500. Workers aged 50 and older can add an $8,000 catch-up contribution, allowing for a total of $32,500. Furthermore, under recent legislation, there is a special “super catch-up” provision for individuals aged 60 through 63, permitting a catch-up limit of $11,250.

How you apply these contributions depends on your tax strategy:

- Traditional Accounts: Contributions lower your Adjusted Gross Income (AGI) for the current year, providing immediate tax relief. You will pay taxes on this money when you withdraw it in retirement.

- Roth Accounts: Contributions are made with after-tax dollars, meaning they will not lower your 2026 tax bill. However, the money grows completely tax-free, and you will not owe any federal income tax upon withdrawal.

If you are already retired but your spouse is still working, look into a Spousal IRA. As long as your household files a joint return and your spouse has enough earned income to cover the deposit, you can fund an IRA in your name to double your family’s tax-advantaged savings.

2. Project Your Income to Avoid the IRMAA Trap

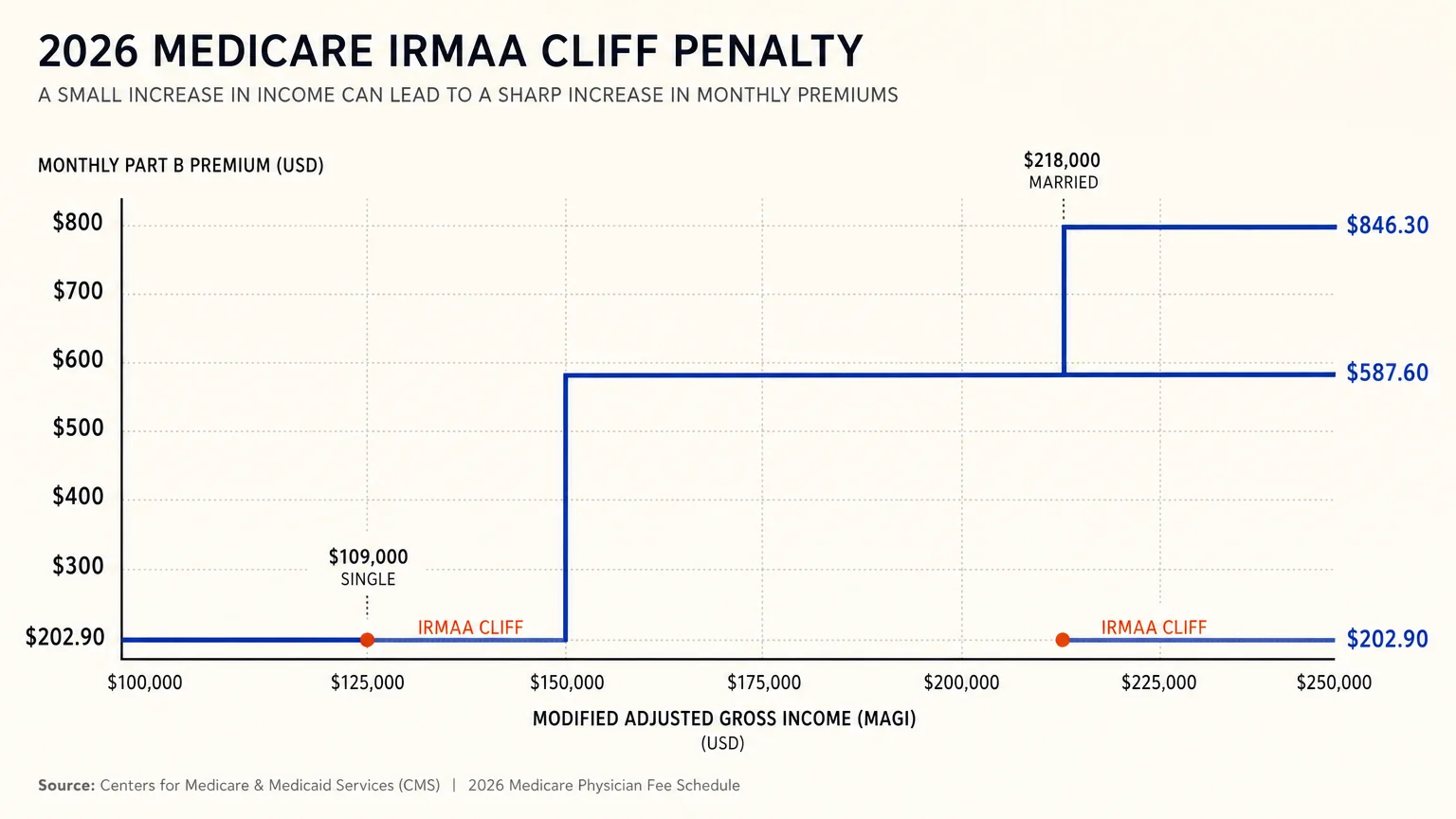

Many seniors are blindsided during tax season not by the IRS, but by Medicare. The Income-Related Monthly Adjustment Amount—commonly known as IRMAA—is a surcharge added to your Medicare Part B and Part D premiums if your income exceeds certain thresholds. Because Medicare looks at your tax return from two years prior, the financial moves you make in 2026 will dictate your Medicare premiums in 2028.

For 2026, the standard Medicare Part B premium has increased to $202.90 per month. However, if your Modified Adjusted Gross Income (MAGI) crosses specific lines, you could pay significantly more. The 2026 IRMAA brackets start when MAGI exceeds $109,000 for single filers or $218,000 for married couples filing jointly.

IRMAA operates as a “cliff” penalty. If a married couple’s MAGI is $217,900, they pay the standard Part B premium. But if a surprise capital gain pushes their income to $218,010—just $10 over the limit—they are vaulted into the first IRMAA tier, forcing them to pay $284.10 per month, per person. Over the course of a year, that slight income bump costs the couple an extra $1,948 in Medicare premiums.

To avoid triggering IRMAA, you need to project your 2026 income right now. Add up your expected Social Security benefits, pension payouts, taxable IRA withdrawals, dividends, and interest. If you are hovering near a threshold, you can take defensive measures. You might delay selling a profitable stock, hold off on a large IRA withdrawal, or direct your required distributions to charity to keep them off your tax return entirely.

If your income recently dropped due to retirement, divorce, or the death of a spouse, you do not have to wait two years for Medicare to notice. You can file Form SSA-44 with the Social Security Administration to request an immediate premium reduction based on a life-changing event.

3. Evaluate Whether to Take the Standard Deduction or Itemize

Deciding between the standard deduction and itemizing your expenses is the foundational choice of your tax return. The IRS allows you to choose whichever option reduces your taxable income the most. Because the standard deduction has grown significantly over the past decade, the vast majority of seniors now claim it. However, assuming you should take the standard deduction without running the numbers is a costly mistake.

The standard deduction is particularly generous for seniors. If you are 65 or older, the IRS grants you an extra deduction amount on top of the base figures. For the 2026 tax year, the base standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. The extra deduction for age 65 or older adds $2,050 for unmarried individuals, or $1,650 per qualifying spouse for married couples.

| Filing Status | 2026 Base Deduction | Senior Add-on (65+) | Total 2026 Standard Deduction |

|---|---|---|---|

| Single (Age 65+) | $16,100 | $2,050 | $18,150 |

| Married Filing Jointly (One spouse 65+) | $32,200 | $1,650 | $33,850 |

| Married Filing Jointly (Both spouses 65+) | $32,200 | $3,300 ($1,650 each) | $35,500 |

With a $35,500 hurdle for a married senior couple, itemizing only makes sense if you have massive deductible expenses. The most common itemized deductions for seniors include state and local taxes (capped at $10,000), mortgage interest, charitable donations, and out-of-pocket medical expenses.

If you find that your itemized expenses fall just short of the standard deduction every year, consider a strategy called “bunching.” Instead of donating $8,000 to your favorite charity every year, you might combine three years’ worth of donations ($24,000) into a single tax year. This massive spike in expenses allows you to itemize and claim a larger deduction in year one, while comfortably taking the generous standard deduction in years two and three. The same strategy can be applied to elective medical procedures, like dental implants or hearing aids, which can be grouped into one calendar year to exceed the IRS threshold (medical expenses must exceed 7.5% of your AGI to be deductible).

4. Plan Your Required Minimum Distributions (RMDs) Carefully

If you have money in a Traditional IRA, a 401(k), or other tax-deferred retirement accounts, the IRS will not let those funds sit untaxed forever. Once you reach a certain age, you must withdraw a minimum amount every year and pay ordinary income tax on it. These are your Required Minimum Distributions (RMDs).

Current legislation mandates that RMDs begin at age 73 for anyone born between 1951 and 1959, and at age 75 for anyone born in 1960 or later. If you are subject to RMDs in 2026, waiting until December to figure out your strategy is dangerous. Failing to take your full distribution by December 31 triggers a hefty IRS penalty—typically 25% of the amount you failed to withdraw, which can be reduced to 10% if corrected in a timely manner.

If you do not actually need your RMD money to cover living expenses, you have a highly efficient alternative: the Qualified Charitable Distribution (QCD). A QCD allows you to transfer funds directly from your IRA to a qualified 501(c)(3) charity. The money counts toward satisfying your RMD for the year, but because it goes straight to the charity, it never shows up in your Adjusted Gross Income.

This maneuver is incredibly powerful. By keeping the distribution out of your AGI, you avoid inflating your tax bracket, protect your Social Security benefits from heavier taxation, and shield yourself from the Medicare IRMAA cliff discussed earlier. For 2026, the maximum QCD limit is indexed for inflation and exceeds $100,000 per person. Remember, the funds must be transferred directly by your IRA custodian to the charity; if you withdraw the money to your personal checking account first, the tax advantages are permanently lost.

5. Harvest Investment Losses to Offset Capital Gains

If you hold investments in a standard, taxable brokerage account—not an IRA or 401(k)—you will pay taxes whenever you sell an asset for a profit. However, the IRS allows you to use your losing investments to cancel out the taxes on your winning ones. This strategy is known as tax-loss harvesting.

Mid-year is an excellent time to review your portfolio. If you have a mutual fund or stock that has dropped in value, you can sell it to lock in the loss. You can then apply that loss to offset any capital gains you have realized this year. If your losses exceed your gains, the IRS allows you to use up to $3,000 of the excess to offset your ordinary income, such as your pension or part-time wages. Any leftover losses beyond $3,000 can be carried forward indefinitely into future tax years.

“Taxes will be the single biggest expense in retirement. It’s not the market that will wipe out your savings—it’s the taxman.” — Ed Slott, CPA and Retirement Tax Expert

While tax-loss harvesting is brilliant, you must navigate the “wash-sale rule.” The IRS prohibits you from claiming a tax loss if you buy a “substantially identical” investment within 30 days before or after the sale. If you sell a specific S&P 500 index fund at a loss, you cannot buy that exact same fund back the next week. You can, however, remain invested in the market by purchasing a different kind of index fund, such as a total stock market fund, to maintain your portfolio’s balance while still securing your tax deduction.

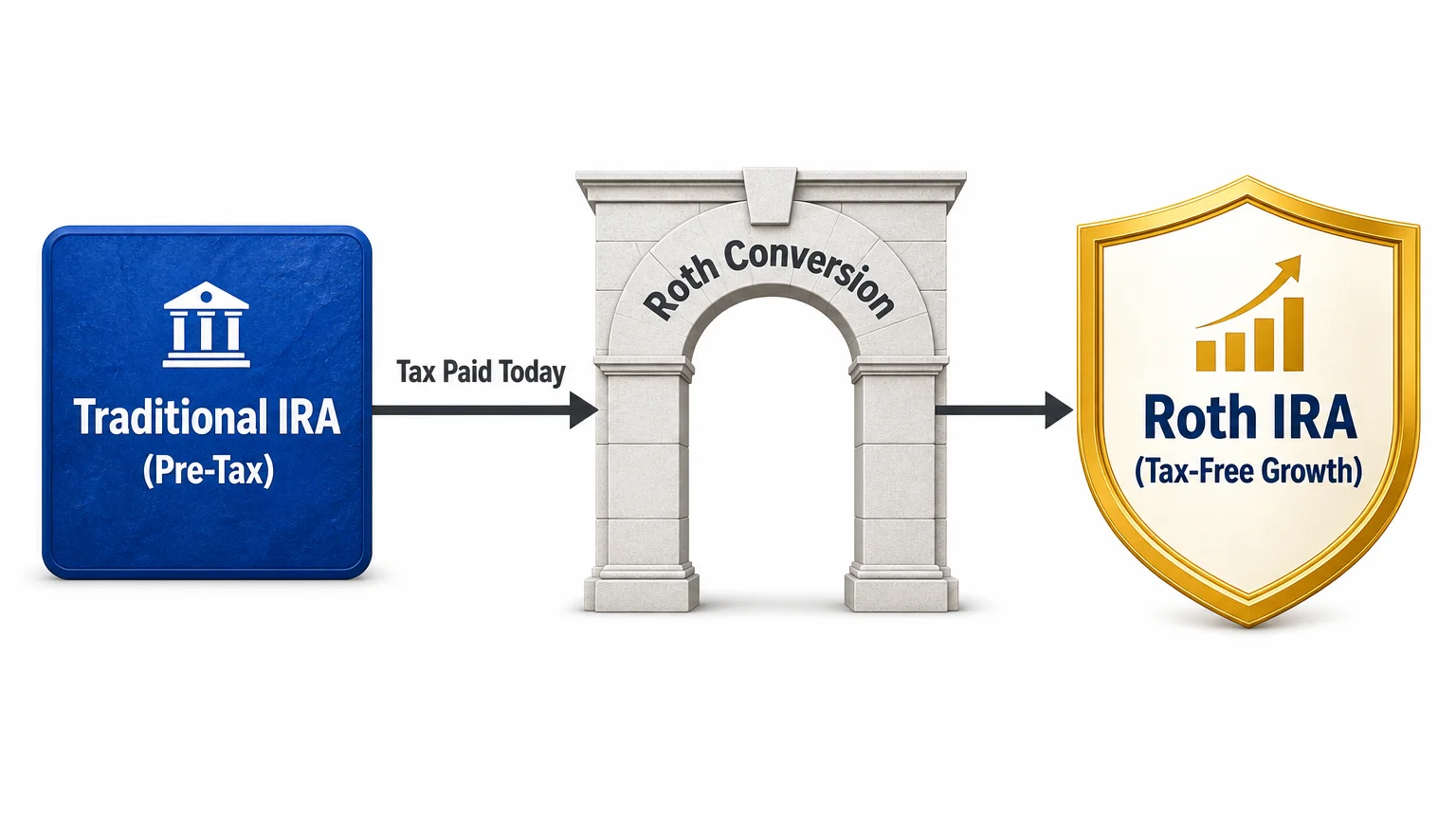

6. Consider a Roth Conversion Before Year-End

A Roth conversion involves moving money from your Traditional IRA into a Roth IRA. You must pay ordinary income tax on the amount you convert in the year you make the move. While paying voluntary taxes might sound unappealing, doing so strategically can save you tens of thousands of dollars over your retirement.

The logic is simple: you choose to pay taxes now while you are in a known, relatively low tax bracket, so you do not have to pay taxes later when rates might be higher. Once the money is in the Roth IRA, it grows tax-free forever. Furthermore, Roth IRAs are not subject to Required Minimum Distributions during your lifetime, giving you ultimate flexibility over how and when you use your money.

The best time to execute a Roth conversion is during the “gap years”—the period after you retire and stop earning a salary, but before you start claiming Social Security or taking RMDs. During these years, your taxable income naturally plummets, dropping you into a lower tax bracket.

If you execute a conversion, it is crucial to pay the resulting tax bill with outside cash (such as from a savings account) rather than withholding taxes from the IRA distribution itself. Withholding taxes from the conversion reduces the amount of money growing tax-free in the Roth account and can trigger early withdrawal penalties if you are under age 59½.

What Can Go Wrong: 4 Common Senior Tax Mistakes

Even with the best intentions, the complexity of the U.S. tax code causes many retirees to stumble. Avoid these frequent missteps as you organize your finances this year:

- Misunderstanding Social Security Taxation: Many retirees assume their Social Security benefits are tax-free. In reality, up to 85% of your benefits can be taxed at the federal level if your “provisional income” (your AGI, plus non-taxable interest, plus half your Social Security) exceeds $25,000 for a single filer or $32,000 for a married couple. Always factor this into your withholding strategies.

- Ignoring State Tax Rules: Moving across state lines for retirement changes everything. Some states do not tax Social Security; others do. Some states offer massive exclusions for pension income, while others tax it fully. Do not base your financial plans solely on federal rules.

- Missing the Medicare Enrollment Window: If you are turning 65, failing to sign up for Medicare Part B on time can result in a lifetime late-enrollment penalty of 10% for every 12-month period you delayed. This directly impacts your monthly budget, compounding the sting of high healthcare costs.

- Violating the Pro-Rata Rule: When executing a “backdoor” Roth contribution, the IRS looks at all of your Traditional IRA balances combined. You cannot selectively convert only your non-deductible contributions. If you have significant pre-tax money in any IRA, a backdoor Roth will trigger unexpected taxes.

When to Consult a Professional

While many tax moves can be handled on your own, certain scenarios demand the trained eye of a fiduciary professional. You should strongly consider hiring a Certified Public Accountant (CPA) or a Certified Financial Planner (CFP®) if you encounter the following situations:

- Executing Large Roth Conversions: Moving significant sums of money requires precise tax bracket management to avoid spilling over into a higher rate or triggering IRMAA surcharges.

- Navigating the Death of a Spouse: The transition from “Married Filing Jointly” to “Single” filing status results in what is known as the “widow’s penalty”—your income may stay roughly the same, but your tax brackets compress drastically, resulting in higher taxes.

- Selling a Primary Home: If you are downsizing, a professional can help you ensure you meet the criteria for the Section 121 exclusion, which allows you to shield up to $250,000 (single) or $500,000 (married) of profit from capital gains tax.

- Inheriting an IRA: The SECURE Act dramatically changed the rules for inherited retirement accounts. Non-spouse beneficiaries typically must drain the account within 10 years, which can cause massive tax spikes if not planned properly.

Frequently Asked Questions

Do I have to pay taxes on my Social Security benefits?

Yes, it is possible. Depending on your total provisional income, the IRS can tax up to 85% of your Social Security benefits. If your only source of income is Social Security, your benefits are generally not taxed. If you have additional income from wages, pensions, or investments, you should review the IRS thresholds to see if you owe.

At what age do I get the extra standard deduction?

The IRS allows an additional standard deduction amount for the tax year in which you turn 65. If you are married and only one spouse is 65 or older, you get one additional amount. If both spouses are 65 or older, the additional deduction amount is doubled.

Can I still contribute to an IRA if I am fully retired?

You must have “earned income” (such as W-2 wages or self-employment income) to contribute to an IRA. Pensions, Social Security, and investment dividends do not count as earned income. However, if your spouse is still working, they can fund a Spousal IRA on your behalf.

What is the best resource to check my current tax brackets?

Always refer directly to the Internal Revenue Service for the most current, inflation-adjusted tax brackets, standard deduction amounts, and filing deadlines. Tax software and financial planners will also have these updated figures.

Your Next Steps

Getting ahead of tax season requires looking at your finances proactively rather than reacting when the filing deadline arrives. Start by logging into your investment accounts to check your current catch-up contributions and evaluate whether your anticipated income is inching dangerously close to a Medicare IRMAA threshold. By pulling your financial data together now, you give yourself the runway needed to make adjustments before December 31 closes the door on your options.

Taking control of your tax strategy can dramatically stretch the longevity of your portfolio. This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.