You worked hard to build your retirement, yet glancing at the latest financial headlines is enough to make anyone second-guess their security. The core pillars of American retirement face mounting pressures that directly impact your bottom line. With the 2026 Social Security cost-of-living adjustment coming in at 2.8 percent while Medicare Part B premiums simultaneously jump to $202.90 per month, many seniors find their actual take-home pay barely budges. Add in recent government reports projecting the depletion of the Social Security retirement trust fund by 2032, and it is entirely natural to feel anxious. Fortunately, understanding these specific changes is the first step toward regaining control, cutting through the noise, and effectively protecting your fixed income from unexpected legislative shortfalls.

The Social Security Squeeze: 2026 COLA vs. Real Costs

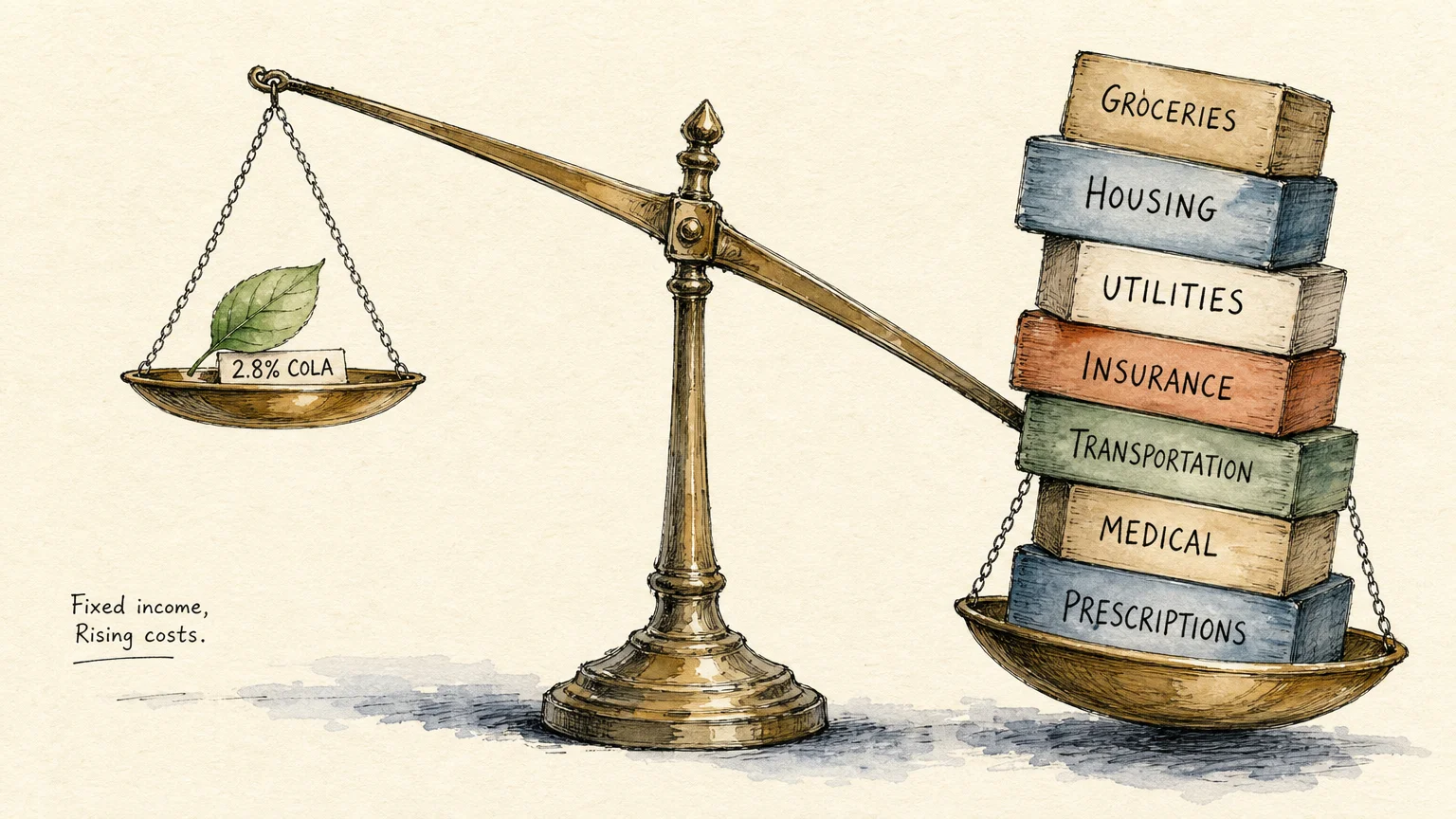

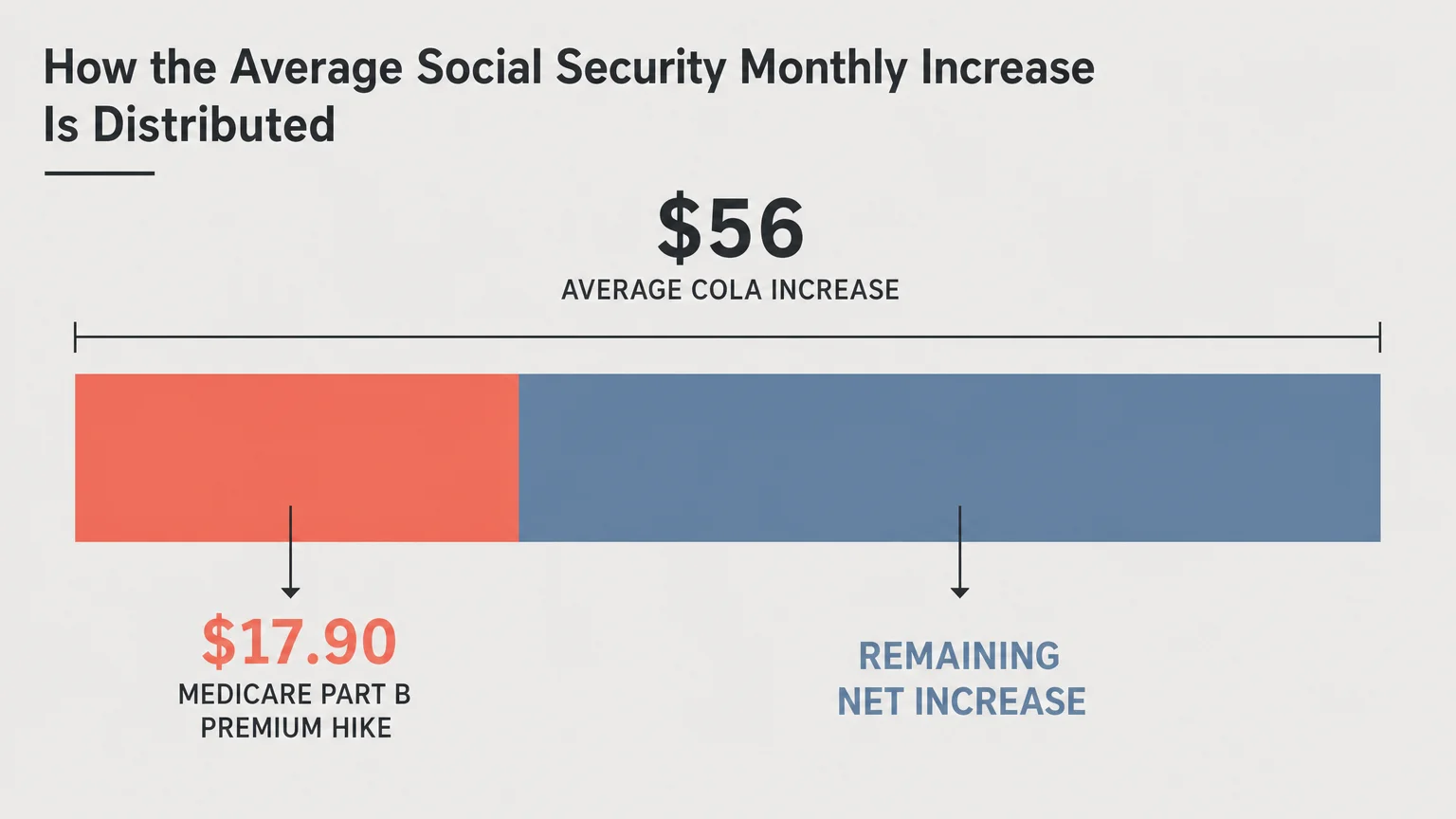

Every October, the Social Security Administration announces the cost-of-living adjustment (COLA) for the upcoming year. For 2026, the official COLA is 2.8 percent. On paper, this translates to an average increase of about $56 per month for the typical retiree, pushing average monthly checks slightly higher to help offset the creeping costs of groceries, housing, and utilities.

However, the reality of living on a fixed income often feels disconnected from federal inflation metrics. The COLA is calculated using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While this index tracks broad economic inflation, it heavily weights expenses like gasoline and electronics while underrepresenting the categories where seniors spend the most money—specifically, healthcare and housing.

When your grocery bill rises, property taxes increase, and home insurance premiums skyrocket, a 2.8 percent raise can quickly evaporate. More than 71 million Americans rely on these benefits, and for many, Social Security represents over half of their retirement income. Understanding exactly how much you will keep after mandatory deductions is crucial for balancing your monthly budget.

Rising Medicare Premiums Eating Your Raise

One of the primary reasons retirees feel pessimistic about future benefits is the aggressive rate at which healthcare costs consume their annual COLA. For the vast majority of seniors, Medicare Part B premiums are deducted directly from their Social Security checks before the money ever hits their bank account.

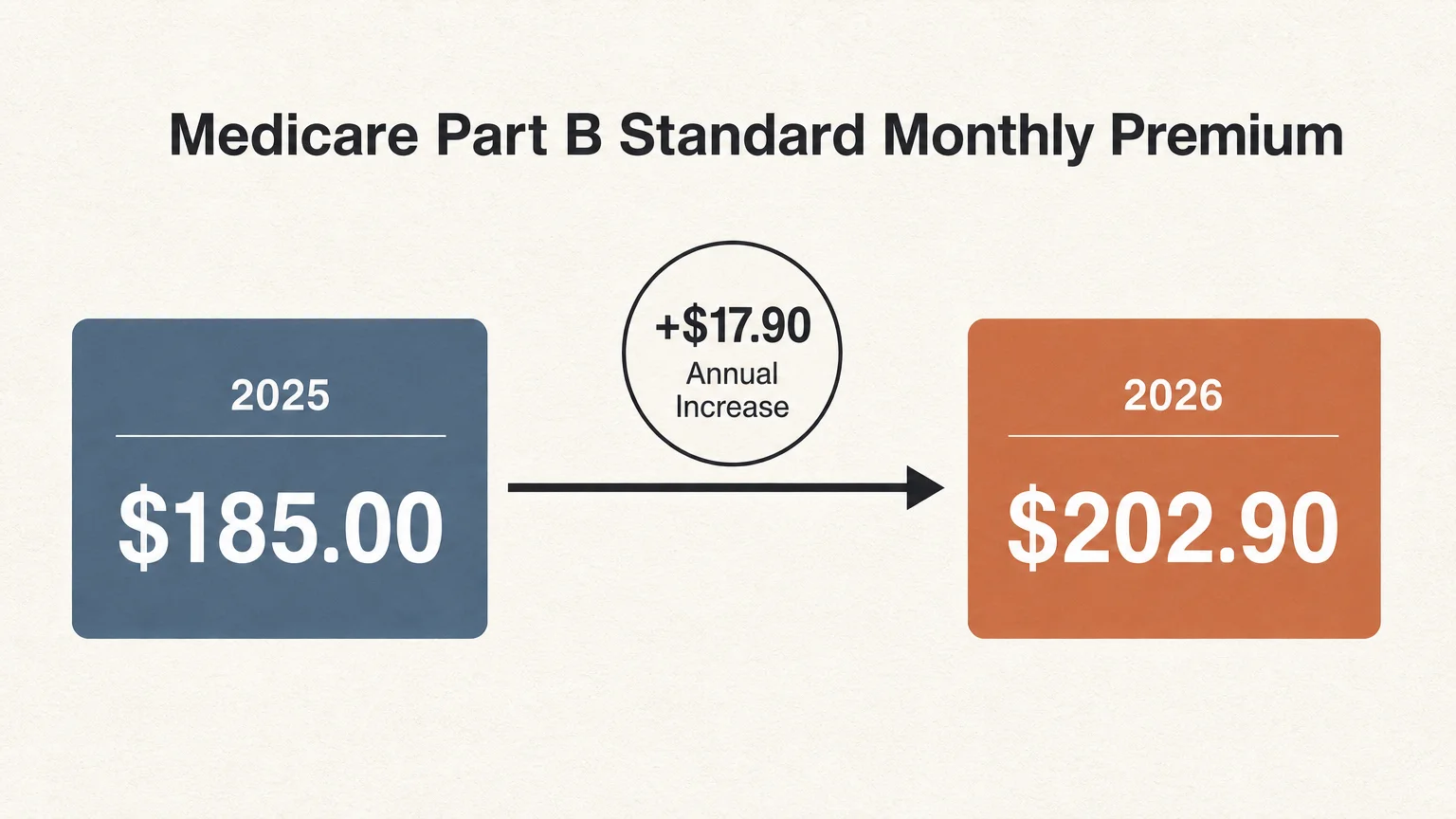

According to the Centers for Medicare & Medicaid Services (2026), the standard Medicare Part B premium increased to $202.90 per month for 2026. This represents a steep $17.90 monthly jump from the 2025 premium of $185.00. If your Social Security check only increases by an average of $56 per month, that nearly $18 Medicare hike immediately erases roughly one-third of your raise.

This dynamic creates a stagnant “net” benefit. Even if gross Social Security payouts increase, the net deposit into your checking account remains virtually flat. High-income earners face an even tougher headwind due to the Income-Related Monthly Adjustment Amount (IRMAA). If your modified adjusted gross income exceeds certain thresholds, your Part B and Part D premiums scale up significantly, putting further strain on your portfolio withdrawals.

Comparing Your 2026 Medicare Costs

When analyzing your future benefits, you must account for the out-of-pocket costs required to utilize your Medicare coverage. Deductibles and copays are rising alongside monthly premiums. The table below outlines the specific cost shifts from 2025 to 2026 based on official data from the Centers for Medicare & Medicaid Services:

| Medicare Cost Category | 2025 Amount | 2026 Amount | Annual Increase |

|---|---|---|---|

| Part B Standard Monthly Premium | $185.00 | $202.90 | +$17.90 |

| Part B Annual Deductible | $257.00 | $283.00 | +$26.00 |

| Part A Inpatient Hospital Deductible (per benefit period) | $1,676.00 | $1,736.00 | +$60.00 |

These increases are tied to projected price changes and higher utilization rates across the medical system. If you experience a hospitalization or require extensive outpatient care, these baseline costs must be factored into your emergency cash reserves.

The Looming 2032 Trust Fund Deadline

Perhaps the greatest source of retirement anxiety stems from the annual Social Security and Medicare Trustees Reports. The financial health of the Old-Age and Survivors Insurance (OASI) Trust Fund—the primary pool of money that pays retiree benefits—has been steadily declining due to demographic shifts. Birth rates have fallen, meaning fewer workers are paying payroll taxes, while the massive baby boomer generation continues to retire and draw benefits.

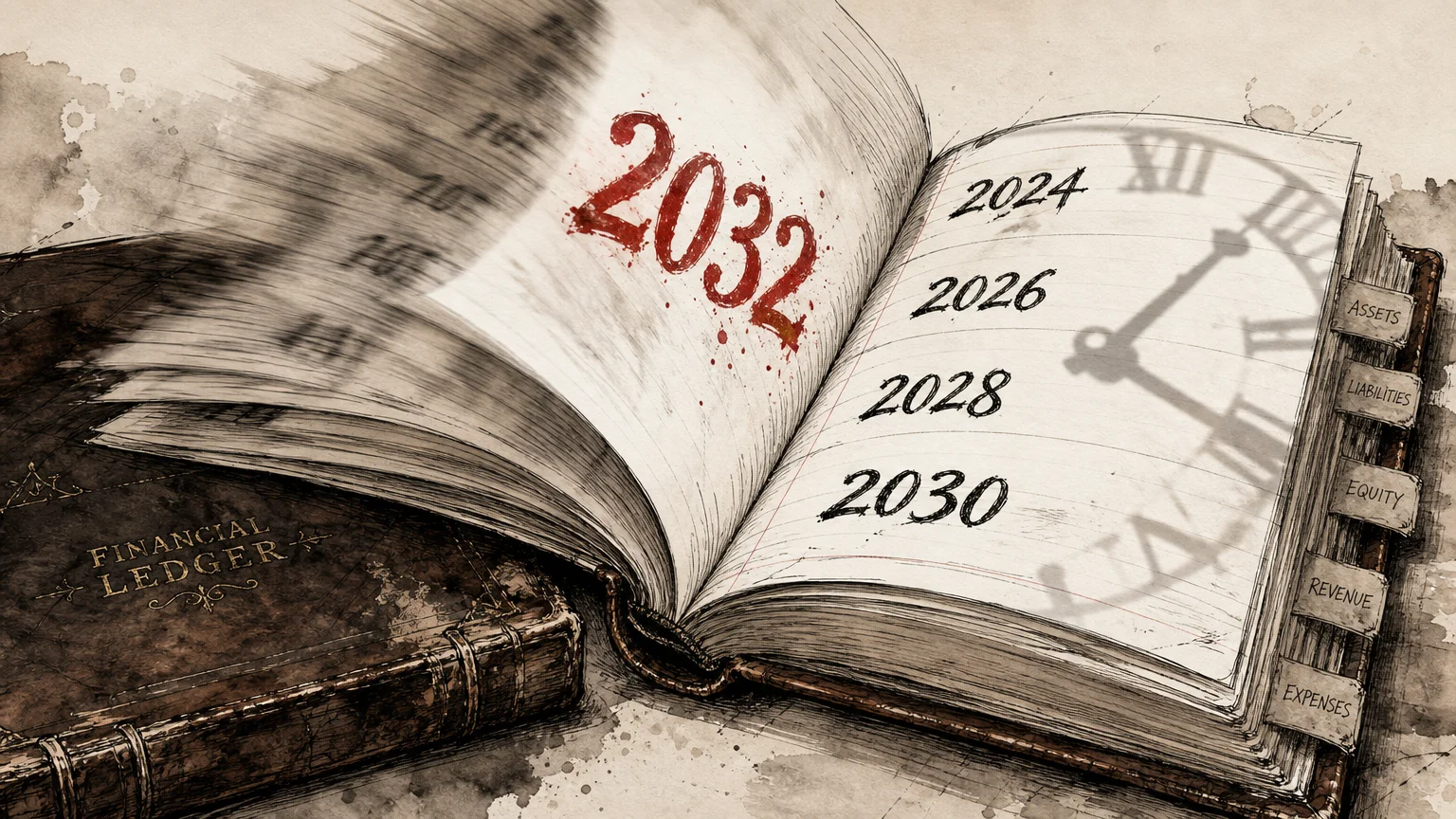

The June 2026 Trustees Report projects that the OASI Trust Fund will be depleted by the fourth quarter of 2032. This date is one year earlier than previously estimated, adding urgency to the conversation.

However, the word “depleted” is often misunderstood. It does not mean Social Security is going bankrupt or disappearing entirely. The program operates on a pay-as-you-go system funded by current payroll taxes. If Congress takes no action by 2032, the continuing tax revenue will still be sufficient to pay 78 percent of all scheduled benefits.

While a 22 percent reduction in monthly income would be devastating for millions of retirees, the system itself will endure. Furthermore, if the OASI fund were legally combined with the Disability Insurance (DI) Trust Fund, the combined reserves would last until 2034, at which point 83 percent of scheduled benefits could be paid. History shows that Congress typically waits until the eleventh hour to enact legislative fixes, such as they did with the major Social Security amendments of 1983.

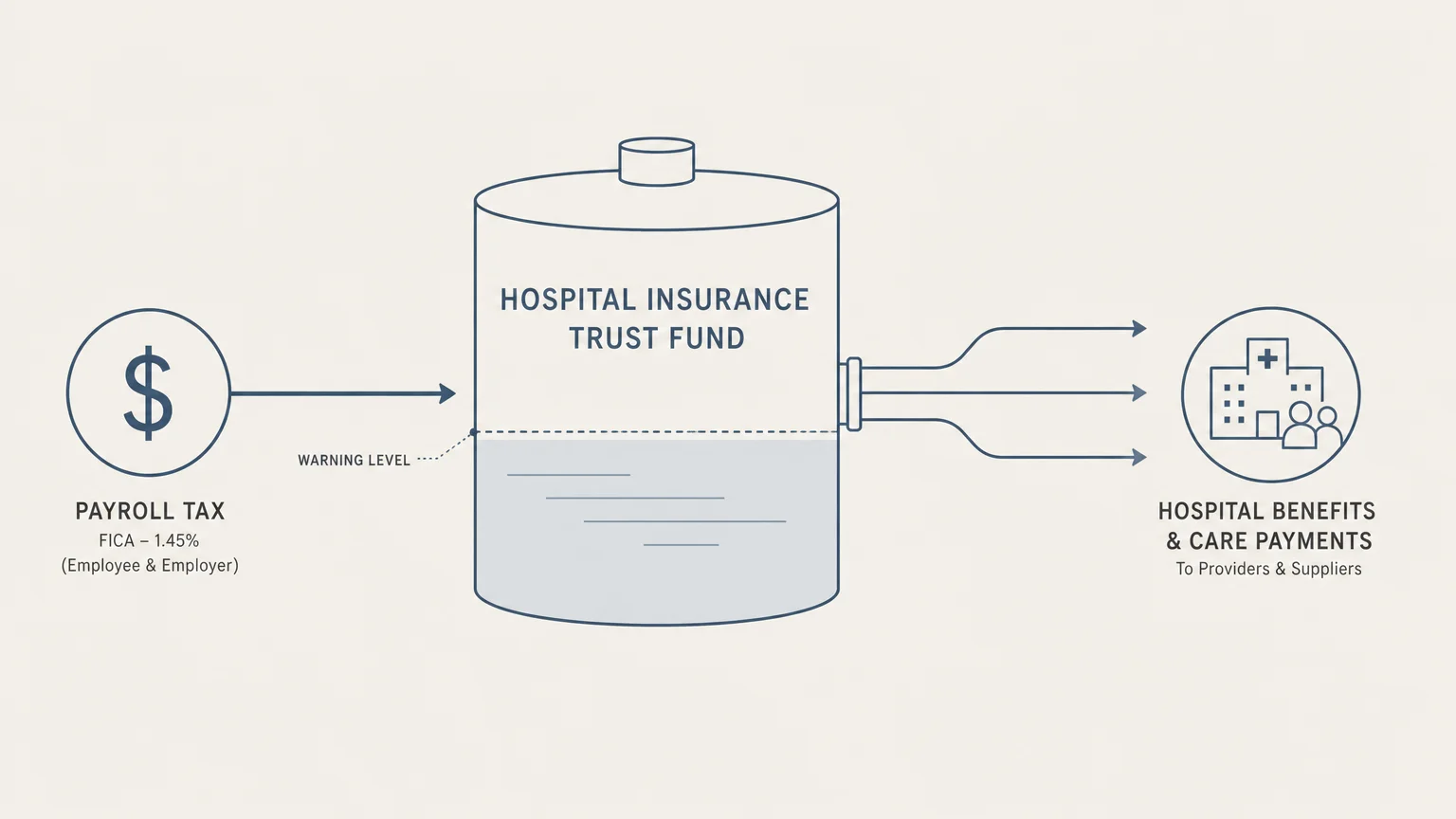

The Medicare Hospital Insurance Trust Fund

Social Security is not the only safety net facing a mathematical shortfall. The Medicare Hospital Insurance (HI) Trust Fund, which finances Medicare Part A (inpatient hospital care, skilled nursing facilities, and hospice), is on a similarly tight timeline.

The 2026 Trustees Report indicates that the Medicare Part A trust fund will be depleted by the second quarter of 2033. If no legislative reforms are passed, the ongoing tax revenue flowing into Medicare would cover roughly 89 percent of projected Part A benefit costs at that time.

This shortfall could force the government to reduce payments to hospitals and medical providers. While beneficiaries might not see an immediate direct benefit cut like they would with Social Security, reduced provider payments could lead to narrower networks, longer wait times, and hospitals opting out of Medicare altogether. The AARP and other advocacy groups continually press lawmakers to shore up this funding to prevent a crisis in healthcare access.

“Resilience is about planning for the things you can control, rather than panicking over the things you cannot.” — Jean Chatzky, Financial Editor and Author

What Can Go Wrong: 3 Mistakes Retirees Make Out of Fear

Anxiety about the future of government benefits frequently drives seniors to make emotional financial decisions. Operating out of fear rarely yields optimal results. Here are three common missteps to avoid:

- Claiming Social Security Early Out of Panic: Many pre-retirees choose to claim their benefits at age 62, rationalizing that they need to “get the money before it runs out.” Claiming at 62 permanently reduces your monthly check by up to 30 percent compared to waiting until your Full Retirement Age. If you live well into your 80s or 90s, this panicked decision permanently cripples your inflation-adjusted income.

- Skipping Necessary Healthcare: Rising Medicare premiums and deductibles cause some seniors to skip annual screenings, delay necessary surgeries, or ration their prescription medications. Ignoring preventive care inevitably leads to catastrophic health events that cost exponentially more—both physically and financially—down the road.

- Hoarding Cash Due to Policy Fears: Hearing that trust funds will run dry by 2032 prompts some retirees to pull their investments out of the market and stockpile cash. While a healthy emergency fund is critical, leaving your entire life savings in a checking account exposes you to inflation risk. Your purchasing power will erode long before any potential Social Security cuts take place.

Actionable Steps to Protect Your Retirement Income

You cannot control congressional gridlock, demographic trends, or federal inflation metrics. You can, however, control how you structure your personal balance sheet. Implementing protective strategies now will insulate your lifestyle from future benefit uncertainty.

- Optimize Your Tax Strategy: Social Security benefits become taxable once your combined income (adjusted gross income + nontaxable interest + half of your Social Security benefit) surpasses $25,000 for an individual or $32,000 for a married couple filing jointly. By utilizing Roth IRAs or implementing strategic Roth conversions before Required Minimum Distributions (RMDs) begin, you can lower your future taxable income and keep more of your benefits.

- Shop Your Medicare Coverage Annually: Never let your Medicare Advantage or Part D prescription drug plan auto-renew without reviewing it. Insurance carriers frequently change their formularies (the list of covered drugs), copays, and provider networks. Use the Open Enrollment Period (October 15 to December 7) to compare plans. Choosing a plan tailored to your specific medications can save you thousands of dollars annually.

- Build a “Bridge” Fund: If you are worried about the 2032 depletion date, create a dedicated cash buffer outside of your traditional retirement accounts. Having two to three years of living expenses securely held in high-yield savings accounts or short-term Certificates of Deposit (CDs) gives you a reliable income source if market volatility coincides with legislative adjustments to your benefits.

- Understand the Hold Harmless Provision: A federal law known as the “hold harmless” provision prevents your net Social Security check from decreasing due to standard Medicare Part B premium hikes. If the dollar amount of your Part B increase is larger than your COLA, your Part B premium is capped to ensure your Social Security check does not drop. Knowing this rule exists can provide immediate peace of mind during years with low COLA increases.

When to Consult a Professional

Navigating the intersection of taxes, Medicare, and Social Security is complex. There are specific milestones where the cost of a mistake heavily outweighs the cost of professional advice. You should strongly consider consulting a fiduciary financial planner or a certified tax professional in the following scenarios:

- You are approaching age 63: Medicare IRMAA calculations look at your tax returns from two years prior. The income you generate at age 63 determines the Medicare premiums you will pay at age 65. A professional can help you avoid accidental income spikes.

- You are coordinating spousal benefits: If you and your spouse have vastly different earnings histories, optimizing when each of you claims Social Security can add tens of thousands of dollars to your lifetime payout.

- You are considering large retirement withdrawals: Paying off a mortgage, buying an RV, or paying for a grandchild’s college out of a traditional IRA can trigger massive tax bills, force up your Medicare premiums, and increase the taxation on your Social Security benefits all at once.

Frequently Asked Questions

Will Social Security stop paying benefits completely in 2032?

No. If the Old-Age and Survivors Insurance Trust Fund is depleted in 2032, ongoing payroll tax revenues would still cover 78 percent of scheduled benefits. Social Security is continuously funded by current workers, meaning the program will always have revenue coming in.

How do rising Medicare premiums affect my COLA?

Because standard Medicare Part B premiums are deducted directly from your Social Security payments, premium hikes reduce your net benefit. For example, in 2026, the Part B premium jumped by $17.90 per month to $202.90. This amount is subtracted directly from your gross 2.8 percent COLA raise before the money reaches your bank account.

Should I claim Social Security early because of the trust fund deadline?

Claiming early permanently locks in a lower monthly benefit for the rest of your life. Financial experts generally advise against claiming early purely out of fear. Even if legislative changes occur to fix the shortfall, historical precedent shows that Congress typically grandfathers in or protects benefits for those who are already in or near retirement.

What is IRMAA and how does it affect my benefits?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is a surcharge added to your Medicare Part B and Part D premiums if your modified adjusted gross income exceeds specific thresholds set by the Internal Revenue Service. Managing your taxable income is critical to avoiding these surcharges.

Taking Charge of Your Future

While the headlines regarding trust fund depletion dates and rising healthcare premiums are undoubtedly stressful, they do not dictate your financial destiny. Knowledge is your most powerful asset. By staying informed about the actual numbers—like the 2026 COLA of 2.8 percent and the $202.90 standard Part B premium—you can build realistic budgets that outlast legislative uncertainties.

Focus your energy on the elements of your retirement that you can actively manage: tax efficiency, healthcare plan optimization, and strategic withdrawal sequencing. You have successfully navigated decades of economic changes to reach retirement; with careful planning, you can navigate these benefit adjustments as well.

Disclaimer: This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.