Generating extra income during retirement allows you to counter inflation, preserve your primary savings, and enjoy a financial cushion without sacrificing your freedom. Retirees are stepping away from traditional full-time employment to embrace flexible income streams that leverage their decades of expertise, unused assets, and lifelong hobbies. From remote consulting and digital entrepreneurship to maximizing high-yield dividends, the current economy offers unprecedented opportunities to boost your monthly cash flow on your own terms. Balancing these revenue sources simply requires a clear understanding of the 2026 tax deductions and Social Security earnings thresholds. By carefully selecting the right supplementary income methods, you can build a highly resilient retirement strategy that fully supports your desired lifestyle.

At a Glance: The Essentials

If you are exploring ways to supplement your retirement earnings, the modern landscape provides numerous paths that do not require punching a traditional clock. Here is a brief overview of the income streams gaining the most traction among today’s retirees:

- Freelance Consulting: Monetizing decades of specialized career experience on a flexible schedule.

- Passive Investments: Optimizing portfolios for dividend yields and fixed-income returns.

- Asset Rentals: Generating cash flow from unused living spaces, storage areas, or vehicles.

- Digital Products: Selling crafts, guides, or online courses to a global audience.

- Online Tutoring: Mentoring students or teaching languages through virtual platforms.

- Virtual Assistance: Providing remote administrative support to small business owners.

- Local Part-Time Work: Finding community-based seasonal jobs that offer social engagement and employee discounts.

1. Freelance Consulting in Your Former Field

Walking away from a full-time career does not mean you have to leave your valuable skills behind. Many professionals choose to transition into consulting—offering their deep industry knowledge to smaller companies that cannot afford a full-time executive but desperately need expert guidance. Whether you spent thirty years in human resources, IT management, accounting, or corporate communications, your expertise remains highly marketable.

Freelance consulting allows you to control your workload; you choose the clients, set your hourly or project-based rates, and dictate your own schedule. Establishing yourself as an independent contractor is often as simple as updating your professional network, reaching out to former colleagues, or creating a profile on specialized freelance platforms. Because you are selling pure expertise rather than physical goods, your overhead costs are virtually zero. This makes consulting one of the most efficient ways to generate extra income while maintaining the freedom that retirement promises.

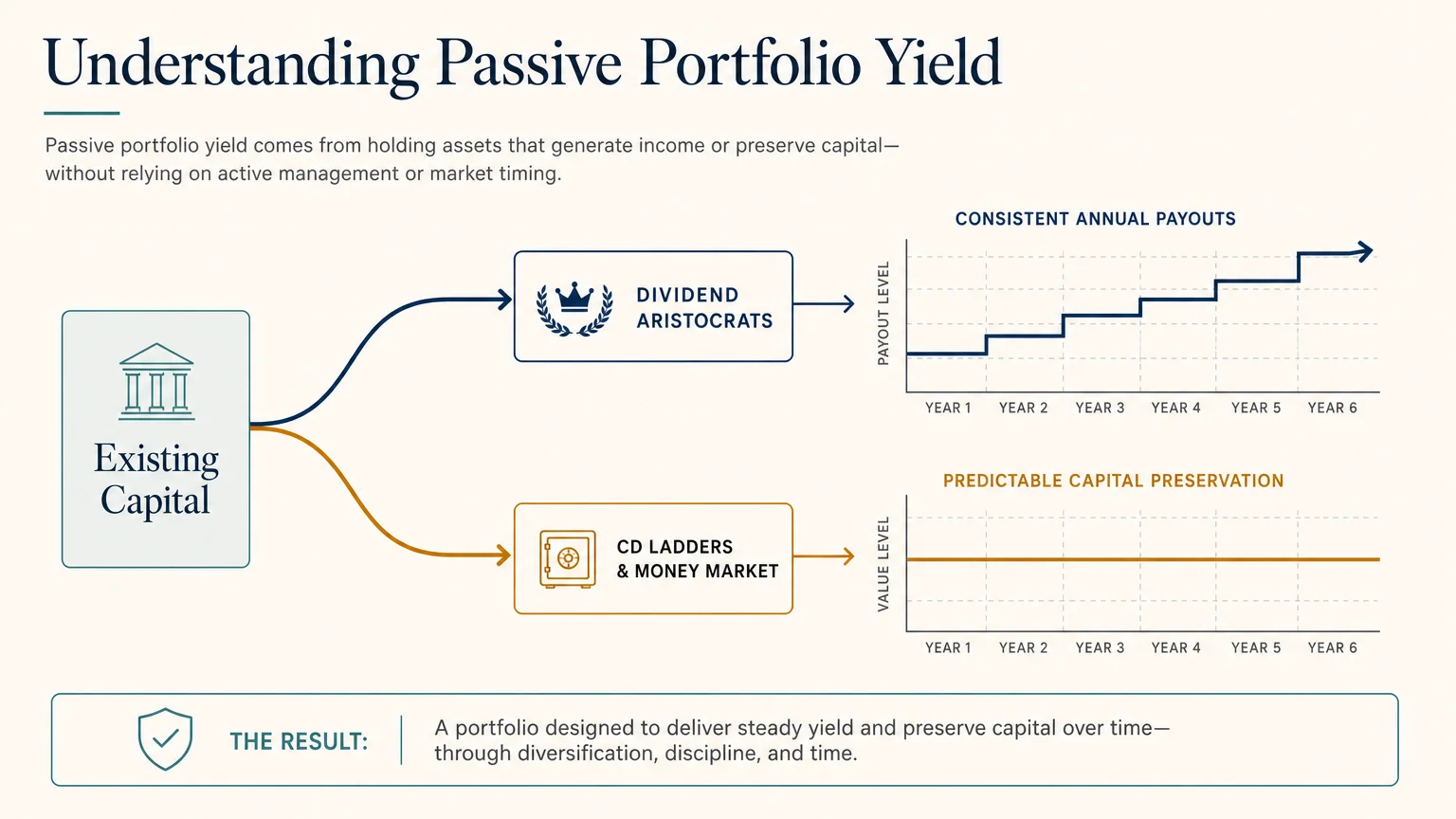

2. Maximizing Yields from Passive Investments

Not all income requires active labor. In fact, optimizing your existing capital to generate reliable cash flow is a cornerstone of robust retiree finances. By shifting a portion of your portfolio toward income-generating assets, you can create a revenue stream that requires minimal day-to-day management.

“If you don’t find a way to make money while you sleep, you will work until you die.” — Warren Buffett, Investor

Many retirees are capitalizing on dividend-paying stocks, specifically focusing on “Dividend Aristocrats”—companies with a long, proven history of consistently increasing their payouts year after year. Additionally, high-yield savings accounts, money market funds, and certificate of deposit (CD) ladders offer secure, predictable returns that outpace traditional banking products. To explore secure investment strategies and verify historical performance data, the SEC’s Investor.gov portal provides excellent, unbiased educational resources. Establishing a passive income strategy ensures that your money continues working hard, even when you decide to take a month off.

3. Turning Unused Assets into Rental Income

If you have downsized your lifestyle but not your living space, you likely possess valuable assets that are sitting idle. The sharing economy has made it incredibly simple to monetize what you already own. Retirees with a spare bedroom, a finished basement, or a detached garage are converting these spaces into consistent monthly cash flow through short-term or long-term rental platforms.

Renting extends far beyond real estate. If you own a secondary vehicle or an RV that spends most of the year parked in the driveway, specialized peer-to-peer rental networks allow you to lease these vehicles to pre-screened, fully insured drivers. Even empty storage space—like an unused attic or shed—can be rented out to neighbors looking for local, affordable places to keep their seasonal belongings. Before listing any property or vehicle, always consult your homeowner’s or auto insurance provider to ensure you have adequate liability coverage for commercial use.

4. Developing Digital Products and E-Commerce Ventures

The barrier to entry for starting a small business has never been lower. Retirees with a creative streak are turning their lifelong hobbies into lucrative e-commerce ventures. If you enjoy woodworking, knitting, or jewelry making, online marketplaces connect you directly with global buyers who value handmade craftsmanship over mass-produced goods.

Furthermore, digital products offer a phenomenal return on investment because you create the item once and sell it an infinite number of times. This might include writing and self-publishing an eBook on Amazon KDP, designing downloadable gardening planners, or creating financial spreadsheets based on your past career experience. Because digital goods require no inventory management or shipping logistics, they represent a highly scalable form of retirement side income that runs automatically in the background of your daily life.

5. Online Tutoring and Educational Mentorship

Patience, life experience, and a strong command of the English language are highly sought-after commodities in the global education market. Online tutoring has exploded in popularity, offering retirees an incredibly fulfilling way to earn extra money from the comfort of their home offices.

You do not necessarily need a formal teaching degree to get started. Many international language platforms simply require a stable internet connection and a conversational fluency in English to help overseas students practice their pronunciation and vocabulary. If you do have a background in mathematics, science, or music, domestic tutoring platforms allow you to connect with high school and college students seeking specialized help. This income stream provides not only a flexible paycheck but also a meaningful intergenerational connection that many seniors miss after leaving the traditional workforce.

6. The Flexibility of the Virtual Assistant Gig Economy

Small business owners and busy entrepreneurs are increasingly relying on virtual assistants (VAs) to handle their daily administrative burdens. This role is perfectly suited for organized, detail-oriented retirees who want to work from home without the stress of managing their own physical business.

As a virtual assistant, your tasks might include managing email inboxes, scheduling appointments, performing basic bookkeeping, or coordinating travel arrangements. The work is inherently flexible; you can take on a single client for five hours a week or build a full roster of clients for a more robust income. Because the work is entirely remote, you can continue earning whether you are sitting in your living room or visiting family across the country.

7. Seasonal and Local Part-Time Work

While digital income streams offer ultimate flexibility, many retirees genuinely miss the social interaction and structured routine of a physical workplace. Local part-time work bridges this gap beautifully. Community-based roles—such as working at a local garden center during the spring, assisting at a golf course in the summer, or providing tax preparation services during the spring filing season—offer a low-stress way to stay active.

Beyond the hourly wage, these roles often come with significant secondary benefits. Working at a specialized retail store or a hobby shop usually provides generous employee discounts on items you already purchase. Moreover, local jobs root you firmly in your community, fostering new friendships and a strong sense of purpose that combats the isolation some feel during early retirement.

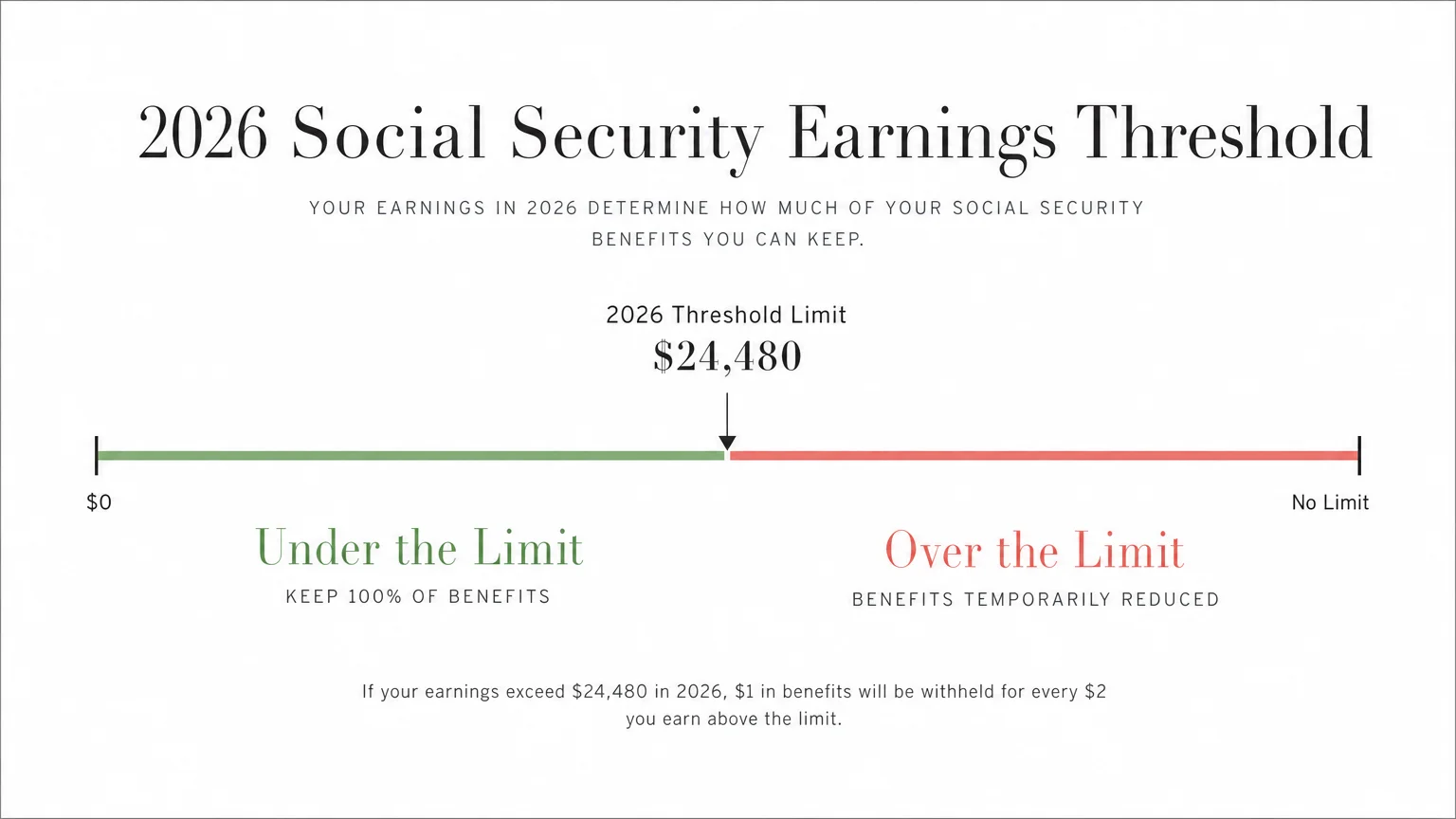

Navigating the 2026 Social Security Earnings Limits

One of the most critical factors to consider before launching a side hustle is how your new income will interact with your existing benefits. If you claim Social Security before reaching your Full Retirement Age (FRA) and continue to work, the Social Security Administration (SSA) enforces specific earnings limits. Earning above these thresholds will result in a temporary reduction of your monthly benefit payments.

For the 2026 calendar year, the SSA has updated these crucial thresholds to account for inflation. It is vital to understand that the SSA only counts wages from an employer or net earnings from self-employment; they do not count passive income like investments, pensions, or annuities.

| Your Age in 2026 | 2026 Annual Earnings Limit | SSA Withholding Rule |

|---|---|---|

| Under Full Retirement Age (for the entire year) | $24,480 | $1 withheld for every $2 earned above the limit |

| Reaching Full Retirement Age in 2026 | $65,160 (Applies only to months prior to your birthday) | $1 withheld for every $3 earned above the limit |

| Full Retirement Age or Older | No Limit | No benefit reduction regardless of earnings |

It is important to remember that benefits withheld due to the earnings limit are not lost forever. Once you reach your Full Retirement Age, the SSA automatically recalculates your benefit amount to give you credit for the months they withheld payments, ultimately resulting in a higher monthly check for the rest of your life.

Taxes on Extra Income: What Changes in 2026?

Before you commit to a new money-making endeavor, you must understand the tax implications. The Internal Revenue Service (IRS) treats freelance income, consulting fees, and digital product sales as taxable income. If you operate as an independent contractor, you are also responsible for self-employment taxes, which cover both the employer and employee portions of Medicare and Social Security contributions.

“Taxes will be the single biggest factor that separates people from their retirement money.” — Ed Slott, CPA and Retirement Tax Expert

Fortunately, the 2026 tax year introduces significant relief for older Americans. To verify the most current tax brackets and deduction rules, always refer directly to the Internal Revenue Service (IRS). For 2026, the standard deduction has increased to $16,100 for single filers and $32,200 for married couples filing jointly. Furthermore, taxpayers age 65 or older are entitled to an additional standard deduction of $2,050 for singles, or $1,650 per qualifying spouse for joint filers.

Most notably, under the recent legislative updates for 2026, eligible seniors age 65 and older can claim a new, separate senior deduction of $6,000 per person (up to $12,000 for married couples filing jointly). This massive enhancement to the standard deduction means that retirees can generate a substantial amount of extra income before facing severe federal income tax liabilities.

What Can Go Wrong: Common Income-Generating Mistakes

While earning extra money is generally a positive step, navigating the financial logistics requires careful attention. Many retirees stumble into completely avoidable traps during their first year of gig work or consulting.

- Ignoring Estimated Quarterly Taxes: When you work as a traditional employee, taxes are withheld automatically from every paycheck. As a freelancer or small business owner, you are responsible for paying estimated taxes four times a year. Failing to do so can result in hefty IRS penalties and a massive, unexpected tax bill in April.

- Triggering Higher Medicare Premiums: A sudden, massive spike in your adjusted gross income does not just affect your income taxes; it can also trigger Income-Related Monthly Adjustment Amounts (IRMAA). This means you could end up paying significantly more for your Medicare Part B and Part D premiums two years down the line. You can review current IRMAA brackets at Medicare.gov.

- Falling for “Pay-to-Play” Scams: Legitimate side hustles require your time and effort—not your credit card. If an online platform demands a large upfront investment for “training materials” or a “starter kit” to begin working from home, it is highly likely a scam or pyramid scheme. Always research opportunities through trusted consumer watchdogs like the Consumer Financial Protection Bureau (CFPB).

- Burning Out: The primary goal of retirement is to enjoy your time. If a side hustle begins to feel exactly like the stressful, 50-hour-a-week career you just left, it is time to scale back. Protect your physical and mental energy fiercely.

When to Consult a Professional

While straightforward jobs like tutoring or seasonal retail work require minimal financial planning, certain income streams add profound complexity to your financial life. You should strongly consider hiring a professional if your situation involves any of the following scenarios:

If your consulting business or e-commerce store begins generating substantial revenue, a Certified Public Accountant (CPA) can help you decide if it makes financial sense to formally incorporate as an LLC or an S-Corporation to optimize your tax liabilities. Additionally, if you are approaching your Full Retirement Age and your side income fluctuates wildly, a Certified Financial Planner (CFP) can help you perfectly time your Social Security claiming strategy to minimize the earnings test penalties. Finally, if you generate a sudden windfall—such as a massive return on an investment or a highly lucrative contract—a professional can help you shield those assets from unnecessary taxation while ensuring your Medicare premiums remain as low as possible.

Generating extra income in retirement is a powerful way to stay engaged, counter the rising cost of living, and add a comfortable buffer to your budget. Whether you decide to consult, rent out property, or turn a lifelong hobby into a digital storefront, the key is finding an endeavor that brings you joy rather than stress. Take your time, weigh the tax implications, and choose an opportunity that aligns perfectly with the lifestyle you have worked so hard to achieve.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.