You worked hard for decades, expecting your retirement years to bring financial freedom. Instead, an overwhelming number of seniors carry debt into retirement, drastically reducing the impact of their monthly benefits. With the average Social Security payment sitting around $2,025 in 2026, keeping up with credit card minimums, paying a mortgage, and covering medical expenses can quickly consume your fixed income. You need to know exactly where your money is going and how to restructure your obligations. By understanding the specific debts draining your benefits, you can implement strategic adjustments—like optimizing Medicare costs and leveraging new tax deductions—to protect your livelihood and reclaim your cash flow.

The Big Three: Where Senior Income Really Goes

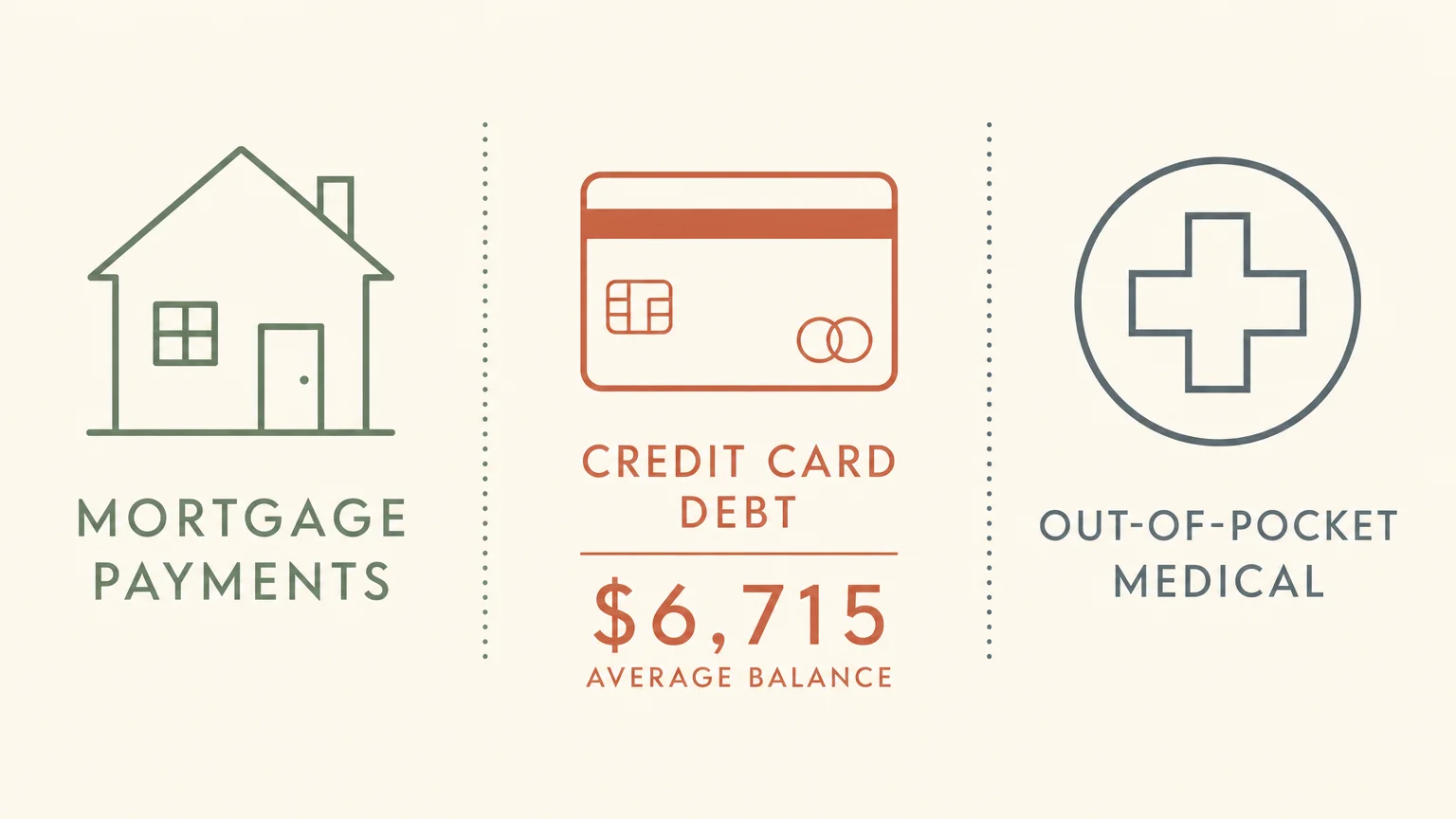

If you rely on a fixed income pool, every single dollar matters. While earlier generations often retired entirely debt-free, today’s seniors frequently enter their golden years juggling multiple financial liabilities. When you look closely at the math, you see three primary culprits actively eating away at Social Security checks.

First, mortgage debt remains a heavy burden for the modern retiree. Many seniors refinanced their homes during periods of historically low interest rates, extending their loan terms well into their seventies or eighties. While the interest rates on these loans might be favorable, the required monthly payment still demands a large slice of your available cash flow. Maintaining a home also means paying property taxes, insurance, and maintenance costs—all of which rise continually due to inflation.

Second, credit card balances have become a silent trap. The average American carries roughly $6,715 in credit card debt. When you live on a fixed income, paying double-digit interest rates destroys your purchasing power. Many retirees rely on plastic to cover unexpected home repairs, rising utility costs, or basic groceries, only to find themselves trapped making minimum payments that barely touch the principal balance.

Third, medical debt consistently catches seniors completely off guard. Even with comprehensive government healthcare, out-of-pocket medical expenses accumulate rapidly. Copayments, specialty prescription drugs, and uncovered services like extensive dental work and vision care force many retirees to dip into their savings. The National Council on Aging (NCOA) frequently notes that healthcare expenses remain one of the most significant stressors for older adults managing a strict budget.

How Inflation and COLAs Impact Your Debt Repayment

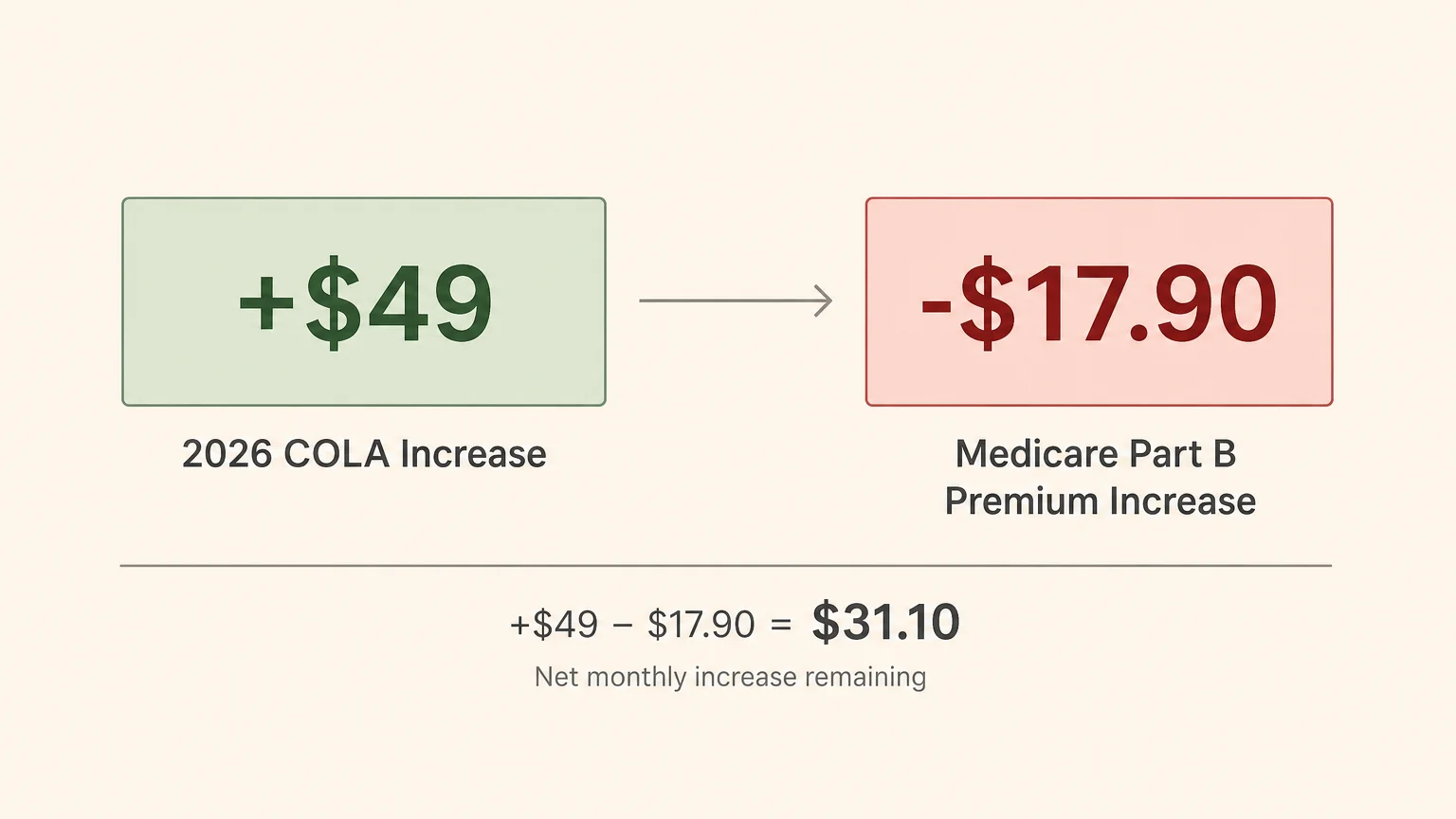

Social Security benefits adjust for inflation, but those adjustments rarely feel large enough to cover the actual rising costs of senior living. In 2026, the 2.5 percent Cost-of-Living Adjustment (COLA) added roughly $49 to the average monthly Social Security check. On paper, a raise sounds excellent for paying down your debt.

However, you must look at your net increase. While you gained $49 from the COLA, the standard Medicare Part B premium increased by $17.90 per month in 2026. Instantly, more than a third of your raise vanished before it ever reached your bank account. Because essential expenses—like groceries, insurance, and utilities—also rise with inflation, the mathematical reality is that you often have less disposable income left over to aggressively tackle your debt.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Investor

Buffett’s advice rings incredibly true for retirees. If you wait to see what is left at the end of the month to pay down your credit cards, you will likely pay nothing. You must treat your debt repayment as a non-negotiable fixed expense in your monthly budget.

The Hidden Weight of Healthcare and Medicare Costs

You might assume that turning 65 means your healthcare costs are largely covered by the federal government. The reality is quite different; failing to budget for Medicare premiums and deductibles often leads retirees directly into high-interest debt.

Your Medicare Part B premium is automatically deducted from your Social Security check. For 2026, the standard Part B premium is $202.90 per month. If your Social Security benefit is average—roughly $2,025 a month—that single health premium consumes exactly 10 percent of your income before you even pay a utility bill or buy groceries.

Additionally, you must account for significant out-of-pocket deductibles. The 2026 Medicare Part B annual deductible is $283, while the Part A inpatient hospital deductible is a staggering $1,736 per benefit period. If you experience a sudden illness and require hospitalization, that $1,736 must be paid out of your own pocket unless you carry a robust supplemental policy (Medigap) or a Medicare Advantage plan that covers it. These sudden financial shocks are precisely why so many seniors find themselves swiping a credit card at the hospital billing office.

You can learn more about managing these premiums and comparing supplemental plans directly at Medicare.gov.

Tackling High-Interest Credit Card Debt on a Fixed Income

Credit card debt is toxic to your retirement plan. If you carry a balance month-to-month, the interest charges actively work against your long-term financial stability. To break the cycle, you need a proactive, mathematical strategy.

Start by auditing your current billing statements. Identify which cards carry the highest interest rates and prioritize paying those down first—a method known as the debt avalanche approach. If your credit score remains strong, you might qualify for a 0 percent introductory APR balance transfer card. Shifting your high-interest debt to a card with no interest for 12 to 18 months allows your payments to directly reduce the principal balance, rather than simply treading water against interest fees.

Another excellent option is to consolidate your debt through a lower-interest personal loan. By converting multiple revolving credit card balances into a single fixed-rate loan, you gain a predictable monthly payment and a clear payoff date. This predictability is vital when managing a strict retirement budget.

“You cannot borrow your way out of debt, and you cannot fund your retirement with credit cards. You must face your numbers head-on.” — Suze Orman, Personal Finance Expert

Should You Pay Off Your Mortgage Before Claiming Benefits?

Deciding whether to aggressively pay off your mortgage before relying entirely on Social Security is a remarkably common dilemma. The right choice depends on your current interest rate, your available cash liquidity, and your emotional tolerance for carrying debt.

Consider the trade-offs carefully. If your mortgage rate is extremely low—say, 3 percent or less—your money might work harder for you if left in a balanced retirement account earning a higher average market return. However, eliminating your monthly housing payment dramatically lowers your baseline living expenses, allowing your fixed Social Security check to cover your remaining lifestyle needs with ease.

| Strategy | Pros | Cons |

|---|---|---|

| Keep the Mortgage | Preserves your cash liquidity; keeps your funds invested in potential growth assets. | Requires a higher monthly income; increases financial risk if your investments underperform the market. |

| Pay It Off | Dramatically reduces your monthly living expenses; provides incredible psychological peace of mind. | Ties up your cash in an illiquid asset; may trigger massive income tax bills if you pull funds from a traditional IRA. |

Before making a massive lump-sum payment to your lender, evaluate how it will affect your emergency savings and your tax bracket. If pulling cash from a traditional IRA pushes you into a significantly higher marginal tax bracket, the tax cost of paying off the mortgage might completely outweigh the benefits of living mortgage-free.

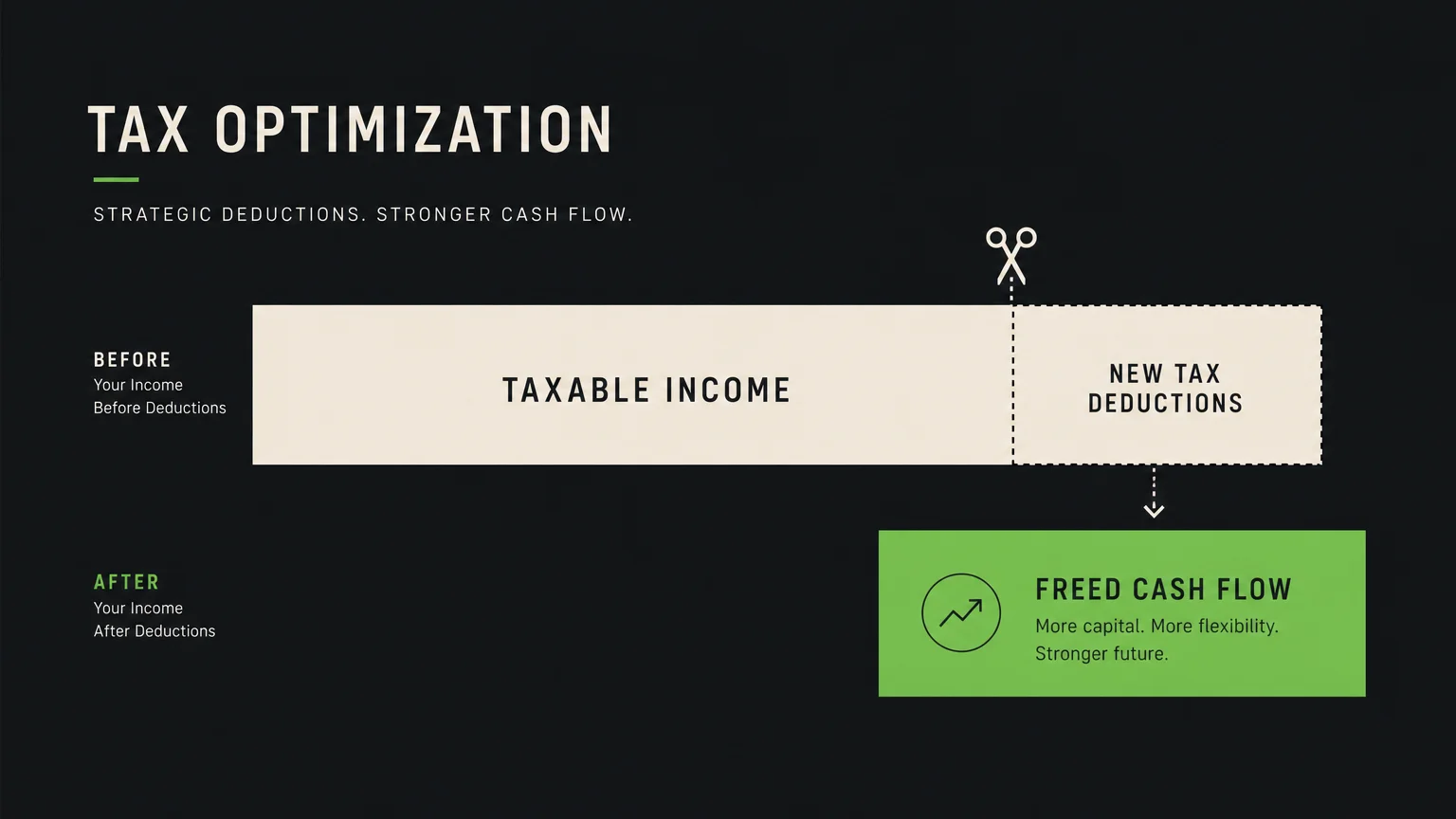

Leveraging New Tax Rules to Free Up Cash

One of the most effective ways to combat retiree debt is to relentlessly minimize your tax liability, leaving you with more cash to pay down your balances. Fortunately, recent legislative changes offer massive financial relief for seniors.

Starting in the 2025/2026 tax years, the “One Big Beautiful Bill Act” introduced a powerful new $6,000 Senior Bonus Deduction for eligible taxpayers aged 65 and older. For married couples filing jointly where both spouses are 65 or older, this deduction doubles to a massive $12,000. Best of all, this is completely separate from your standard deduction; it stacks on top of it.

When you combine the baseline standard deduction—$15,750 for singles and $31,500 for married couples in 2025—with the over-65 additional standard deduction ($2,000 for singles, $3,200 for couples), and the new Senior Bonus Deduction, your taxable income shrinks significantly. A single senior 65 or older taking the standard deduction can shield up to $23,750 of income, while a married couple (both 65+) can shield up to $46,700.

However, you must watch your income thresholds carefully. This new $6,000 deduction begins to phase out if your modified adjusted gross income exceeds $75,000 as a single filer or $150,000 for married couples filing jointly. By utilizing these deductions to lower your tax bill, you can direct the saved cash straight toward your outstanding debt. For complete tax filing guidelines, always verify the latest rules and forms at IRS.gov.

Common Mistakes to Avoid

When you are trying to eliminate debt on a fixed income, financial desperation can easily lead to costly errors. Avoid these incredibly common missteps to protect your wealth:

- Draining Retirement Accounts for Consumer Debt: Pulling large, sudden sums from a traditional 401(k) or IRA to pay off credit cards triggers immediate federal and state income tax liabilities. Furthermore, artificially inflating your income for the year can increase your Medicare Part B premiums two years down the line through the Income-Related Monthly Adjustment Amount (IRMAA).

- Ignoring Available Relief Programs: Many seniors struggle unnecessarily because they simply do not realize they qualify for government assistance. Programs like the Medicare Savings Programs (MSP) can help cover your Part B premiums, deductibles, and copayments if your income falls below a certain threshold. Check Benefits.gov to see what specific aid you qualify for.

- Co-Signing Loans for Family Members: It is entirely natural to want to help your children or grandchildren, but co-signing a student loan or auto loan makes you 100 percent legally responsible for the debt. If they miss a payment or default, your credit score plummets, and aggressive creditors can come after your retirement assets.

- Delaying Medical Care to Save Money: Skipping prescriptions or avoiding the doctor to save on copays often leads to severe health crises later. These crises inevitably result in expensive hospitalizations and massive bills that far exceed the cost of preventative care.

Finding the Right Advisor

Navigating the complex intersection of consumer debt, tax optimization, and Social Security is incredibly difficult. You do not have to figure it all out alone. Consider working with a Certified Financial Planner (CFP) or a fee-only fiduciary if you face any of the following scenarios:

- You are deciding exactly which retirement accounts to withdraw from to pay off a mortgage without triggering a massive, unexpected tax bill.

- You need to aggressively restructure high-interest credit card debt but want to protect your long-term investment portfolio from liquidation.

- You are trying to optimize your Social Security claiming strategy while simultaneously managing severe monthly cash flow deficits.

A professional planner can run detailed, long-term projections to show you exactly how various debt repayment strategies will impact your portfolio over the next twenty years.

Frequently Asked Questions

Can debt collectors garnish my Social Security benefits?

Under federal law, standard debt collectors cannot garnish your Social Security retirement or disability benefits for consumer debts like credit cards, medical bills, or personal loans. If a debt collector threatens your Social Security, they are violating the law. However, the federal government can legally garnish your benefits for unpaid federal taxes, federal student loans, or court-ordered child support and alimony. Learn your exact rights by visiting the Consumer Financial Protection Bureau (CFPB).

Will Medicare pay for my past medical debt?

No. Medicare coverage applies exclusively to current and future eligible medical expenses. It does not retroactively pay off medical debt you accrued before your coverage officially began, nor does it pay off balances owed to providers for services that Medicare simply did not fully cover.

Should I delay claiming Social Security to pay off my debt?

Delaying Social Security increases your permanent monthly benefit amount by 8 percent for every year you wait past your full retirement age, up until age 70. If you are currently working and using your salary to aggressively pay down high-interest debt, delaying benefits is often a mathematically sound move. However, if you are racking up new credit card debt just to delay claiming your benefits, the math works entirely against you. The 20 percent interest compounding on a credit card will always outpace the 8 percent delayed retirement credit you earn from the Social Security Administration.

Taking complete control of your retirement debt requires honesty, discipline, and a willingness to explore every available resource. Start by assessing your complete financial picture without judgment. List your debts, understand your upcoming Medicare obligations, and apply for any tax deductions or government benefit programs you qualify for. It is never too late to restructure your finances, eliminate the burden of high-interest liabilities, and build the genuine peace of mind you deserve.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.