Rethinking retirement means looking beyond traditional sunbelt communities to the vibrant, intellectually stimulating environments of college towns. Retiring near a university gives you immediate access to top-tier healthcare, reliable public transportation, free continuing education, and a dynamic cultural scene that keeps your mind sharp. These communities perfectly blend big-city amenities with the charm and affordability of a smaller town. From tax-friendly states with renowned medical facilities to walkable downtowns featuring diverse culinary options, the right academic hub can stretch your retirement savings while dramatically improving your daily lifestyle. If you want an active, engaged, and financially sustainable next chapter, exploring the nation’s best college towns is your smartest first step.

Why College Towns Are Becoming Premier Retirement Destinations

Modern retirees want more than a golf cart and a quiet street. You want purpose, community, and the ability to maintain an active lifestyle. College towns naturally foster these elements because they are built to support diverse populations, promote walkability, and provide constant intellectual stimulation.

“I think what we’re realizing in a number of ways is that life is just really long, much longer than it was when retirement was originally defined.” — Jean Chatzky, Financial Expert

When you evaluate a retirement destination, a university town often checks the most important boxes for long-term aging in place. Consider the built-in advantages these communities offer:

- World-Class Healthcare: Universities with medical schools typically operate advanced teaching hospitals. This gives you local access to cutting-edge treatments, specialized geriatrics departments, and top-tier specialists without needing to travel to a major metropolitan area.

- Lifelong Learning Opportunities: Many universities host Osher Lifelong Learning Institutes (OLLI) or allow senior citizens to audit undergraduate classes for free or at a steep discount. Keeping your brain engaged is one of the most effective ways to maintain cognitive health.

- Robust Public Transit: College towns feature extensive, accessible, and often free bus networks designed to move thousands of students. For seniors who eventually prefer to drive less, this infrastructure ensures you maintain your independence.

- Cultural Amenities on a Budget: You gain access to theater productions, guest lectures, art museums, and NCAA sporting events, often at a fraction of the cost you would pay in a major city like New York or Chicago.

4 Top College Towns for an Active, Tax-Friendly Retirement

Finding the right community requires balancing lifestyle amenities with tax efficiency. State taxes on pensions, Social Security, and 401(k) withdrawals will dramatically affect your monthly cash flow. Here are four standout college towns that combine exceptional amenities with favorable financial landscapes.

Athens, Georgia (University of Georgia)

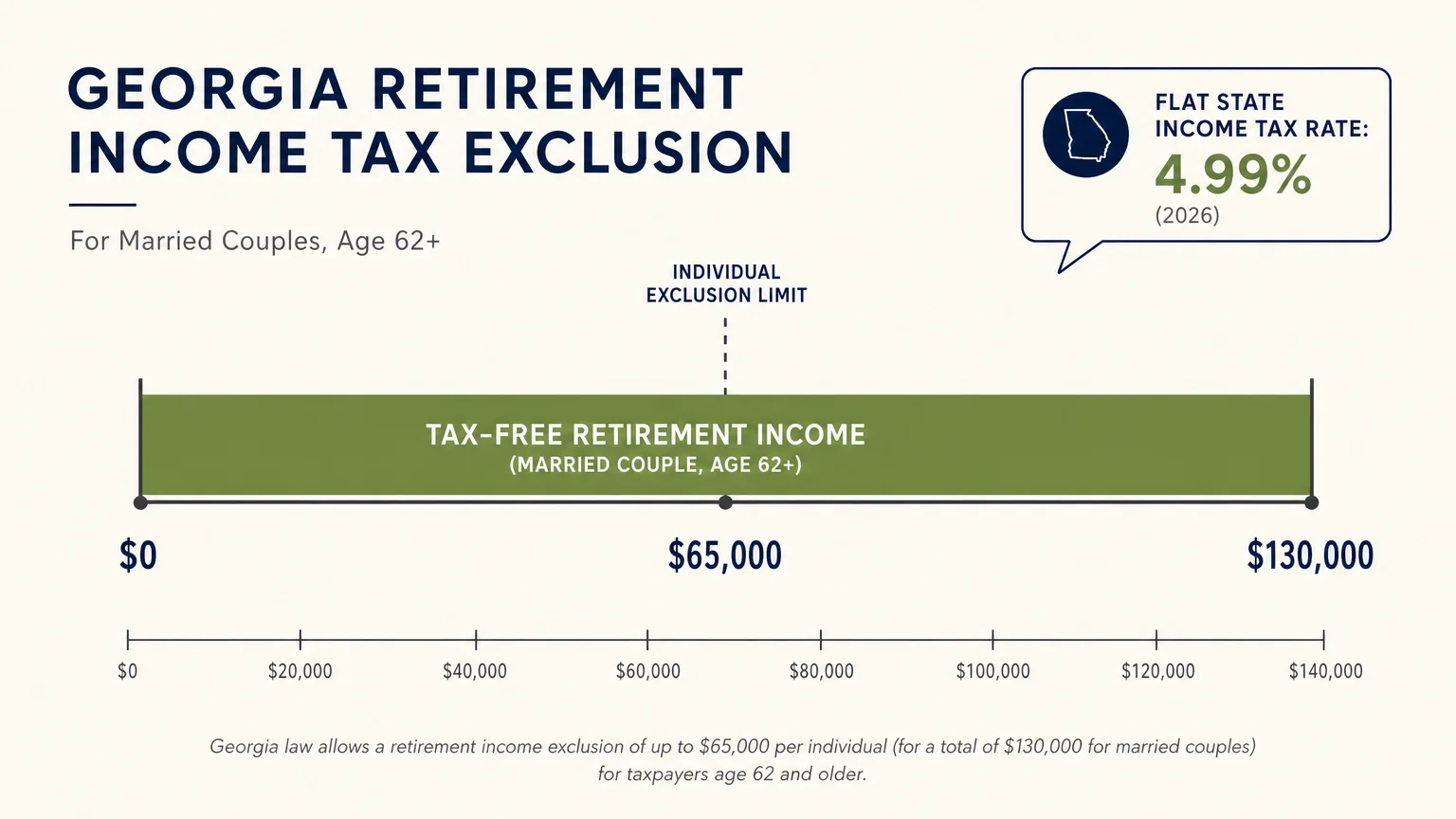

Athens perfectly blends Southern charm with a vibrant music and arts scene. From a financial perspective, Georgia is highly accommodating to retirees. The state does not tax your Social Security Administration benefits. More importantly, starting at age 62, Georgia allows you to exclude up to $65,000 of retirement income per person—meaning a married couple can shield up to $130,000 of pension, IRA, and investment income from state taxes. With a flat state income tax rate of 4.99% in 2026, Athens lets you keep more of your hard-earned money.

Ann Arbor, Michigan (University of Michigan)

Consistently ranked as one of the best places to live in the U.S., Ann Arbor boasts the renowned Michigan Medicine health system. Michigan has aggressively improved its tax landscape for seniors through the Lowering MI Costs Plan. For tax year 2026, eligible retirees can deduct up to $64,040 (single) or $128,080 (joint) of qualifying retirement income from state taxes. This phased-in repeal of the state’s prior “pension tax” makes Ann Arbor a highly lucrative option for midwestern retirees.

State College, Pennsylvania (Penn State)

Nicknamed “Happy Valley,” State College offers a tight-knit community deeply connected to Penn State University. Pennsylvania stands out as one of the most tax-friendly states for retirees. The state completely exempts Social Security benefits, eligible pension income, and distributions from 401(k)s and IRAs from state income tax. This total exemption on retirement account withdrawals makes it incredibly easy to project your net income.

Gainesville, Florida (University of Florida)

If you want warm weather and exceptional healthcare, Gainesville is home to the UF Health Shands Hospital. Florida levies no state income tax, meaning your Social Security, pensions, and retirement account distributions remain untouched by the state. While property insurance costs in Florida require careful budgeting, Gainesville’s inland location protects it from the worst coastal weather events, often resulting in more manageable insurance premiums than coastal cities.

| College Town | University | Healthcare Hub | Retirement Tax Benefit |

|---|---|---|---|

| Athens, GA | University of Georgia | Piedmont Athens Regional | $65,000 exclusion per person (62+); No Social Security tax |

| Ann Arbor, MI | University of Michigan | Michigan Medicine | Up to $128,080 joint retirement income deduction (2026) |

| State College, PA | Penn State | Mount Nittany Medical | No state tax on Social Security, pensions, or IRAs |

| Gainesville, FL | University of Florida | UF Health Shands | No state income tax |

The Financial Impact: Stretching Your Retirement Budget

When analyzing the financial feasibility of a college town, you must account for current federal tax benefits designed to lower your taxable income. For tax years 2025 through 2028, the recently enacted tax legislation provides a significant Senior Bonus Deduction. If you are 65 or older, you can claim an additional $6,000 deduction per person—or $12,000 for married couples filing jointly where both spouses qualify. This below-the-line deduction applies whether you take the standard deduction or choose to itemize.

Combine this with the current standard deduction amounts, and the savings compound rapidly. A single filer age 65 or older receives a standard deduction of $17,750 (the $15,750 base plus a $2,000 age-based addition). Add the $6,000 bonus deduction, and your total federal deductions reach $23,750 before paying federal income tax. Married couples (both 65+) taking the $34,700 age-adjusted standard deduction plus the $12,000 bonus deduction can shelter up to $46,700 of income. Keep in mind that the $6,000 bonus deduction begins to phase out if your Modified Adjusted Gross Income (MAGI) exceeds $75,000 for singles or $150,000 for joint filers. Always verify the most current limits and brackets on IRS.gov.

When you pair these massive federal tax shields with a state that exempts retirement income—like Pennsylvania or Georgia—your gross distributions from your 401(k) translate to much higher net cash in your pocket. This allows you to afford the slightly higher real estate prices typically found in desirable college towns.

Common Mistakes to Avoid When Retiring in a College Town

While the benefits are plentiful, moving to a university city requires strategic planning. Avoid these frequent missteps to ensure a peaceful transition.

- Buying Too Close to Campus: The immediate blocks surrounding a university are generally dominated by student rentals. This means late-night noise, transient neighbors, and limited street parking. Look for neighborhoods positioned two to five miles away from the main campus—you will retain easy access to amenities without living in the middle of a fraternity party.

- Ignoring Local Property Taxes: States with zero income tax (like Florida or Texas) often compensate by levying higher local property taxes. College towns specifically may have higher school district taxes to support local infrastructure. Always run the math on the total tax burden, not just the income tax rate.

- Forgetting About Medicare Advantage Networks: If you use a Medicare Advantage (Part C) plan rather than Original Medicare, your coverage is restricted to a specific network of doctors and hospitals. Before moving across state lines to a college town, use Medicare.gov to verify that the local university hospital system accepts your specific plan. Otherwise, you may be forced to switch plans or pay steep out-of-network costs.

Finding the Right Advisor

Moving your life and your assets to a new state introduces complex tax planning variables. Partnering with a fiduciary financial advisor ensures you optimize your relocation. Consider seeking professional guidance if you encounter these scenarios:

- You plan to establish a new state residency: An advisor can help you execute the legal and financial steps required to sever ties with your former high-tax state to avoid a residency audit.

- You need to optimize Medicare plan selection: A local Medicare broker or financial planner can evaluate whether Original Medicare with a Medigap policy serves you better in your new college town than a localized Medicare Advantage plan.

- You are managing Roth conversions: If you plan to move to a state that does not tax IRA distributions, an advisor can help you time your Roth conversions to capitalize on both the new state tax rules and the federal Senior Bonus Deduction phase-out limits.

Frequently Asked Questions

Do I have to be an alumni to retire in a specific college town?

Not at all. While universities heavily market their affiliated retirement communities (often called University-Based Retirement Communities or UBRCs) to their alumni, the vast majority of residents in the surrounding town have no prior affiliation with the school. You can enjoy the community amenities regardless of where you earned your degree.

Are college towns affordable for retirees living on a fixed income?

It depends entirely on the town. Elite coastal college towns can be prohibitively expensive. However, large state universities in the Midwest, South, and Rust Belt often boast a cost of living below the national average. By leveraging senior tax deductions and choosing states with favorable retirement tax laws, you can easily make a college town fit a fixed-income budget.

Can I really take college classes for free?

In many states, yes. Over 30 states have legislation requiring state-supported universities to offer free or heavily discounted tuition to senior citizens (typically age 60 or 65+). These programs usually allow you to audit classes on a space-available basis, meaning you get the intellectual stimulation of the lectures without the stress of homework or exams.

How do I handle the influx of students in the fall?

Long-term residents of college towns learn the natural rhythms of the academic calendar. You will quickly learn to run your errands outside of class transition times, avoid certain downtown restaurants on game days, and enjoy the blissful quiet of the town during summer and winter breaks.

Retiring in a college town offers a unique blend of intellectual vitality, outstanding healthcare, and vibrant community life. By carefully analyzing your state tax liabilities, maximizing your federal deductions, and choosing a neighborhood that aligns with your desired noise level, you can build a deeply fulfilling next chapter. Take the time to visit your top choices during both the busy fall semester and the quiet summer months to ensure the rhythm of the town matches the pace you want for your retirement.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.