With the 2026 Social Security cost-of-living adjustment sitting at 2.8% and standard Medicare Part B premiums rising to $202.90, making your retirement income stretch further is more critical than ever. If you are looking to lower your cost of living without sacrificing quality of life or healthcare access, the Midwest holds incredible opportunities. Beyond the bustling metropolitan areas, several smaller, affordable towns offer a blend of rich culture, top-tier medical facilities, and surprisingly friendly tax codes. Whether you want zero state income tax or charming lakeside living, discovering these understated retirement destinations can help you keep more of your hard-earned money while enjoying a fulfilling, comfortable next chapter.

At a Glance: The Essentials of Midwest Relocation

- Aggressive tax reforms: States like Iowa and Michigan recently overhauled their tax codes to heavily favor retirees, exempting most or all retirement income from state taxes.

- Drastic housing discounts: While the national average home price hovers above $400,000, several hidden gem towns in the Midwest offer comfortable homes for under $250,000.

- World-class healthcare: You do not need to live in a crowded metropolis to receive excellent medical care. Regional Midwest hubs boast highly rated hospital systems.

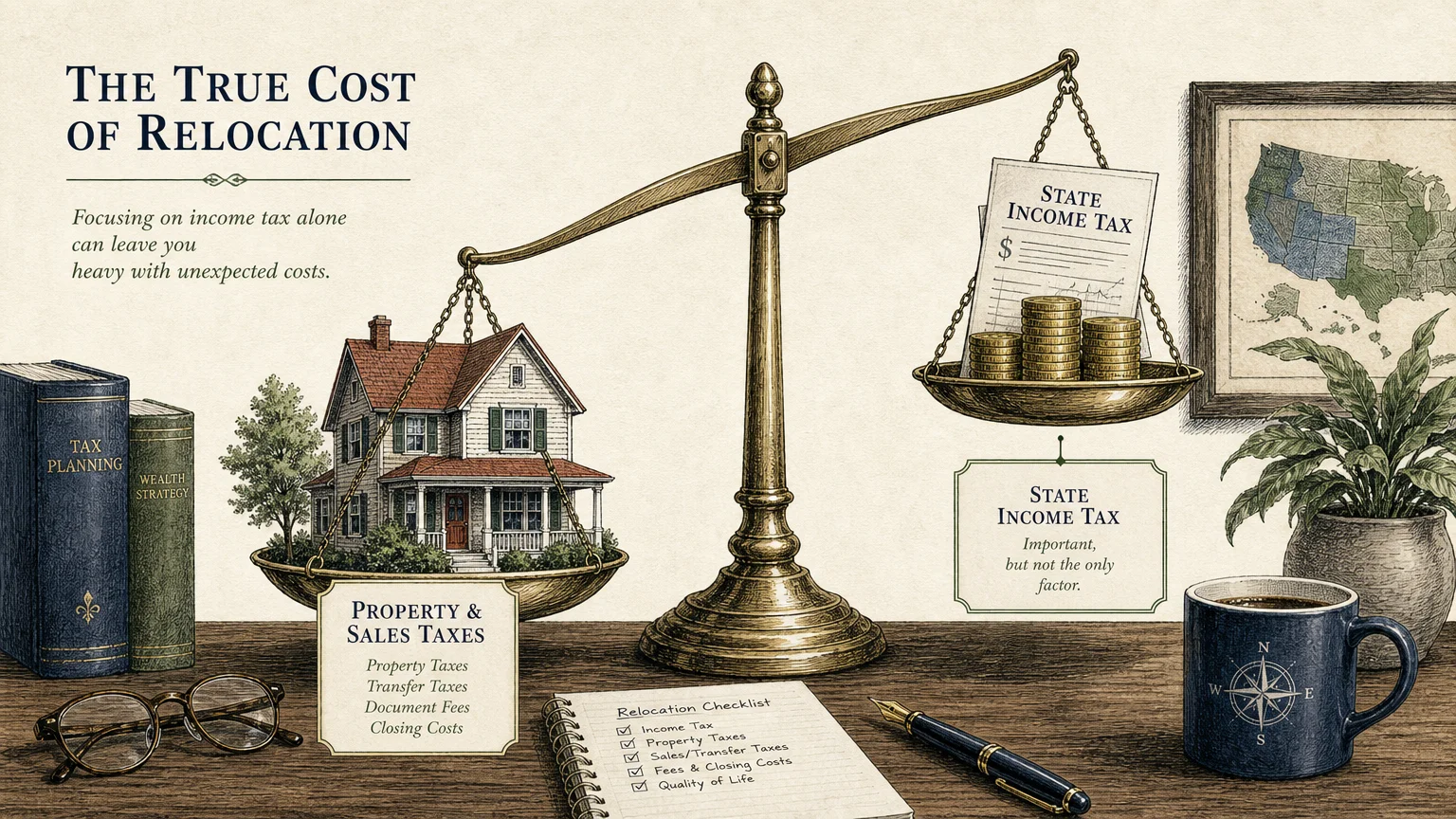

- Total tax evaluation: A successful relocation requires measuring your complete tax footprint—balancing income taxes against property and sales taxes.

Why the Midwest is Making Financial Sense in 2026

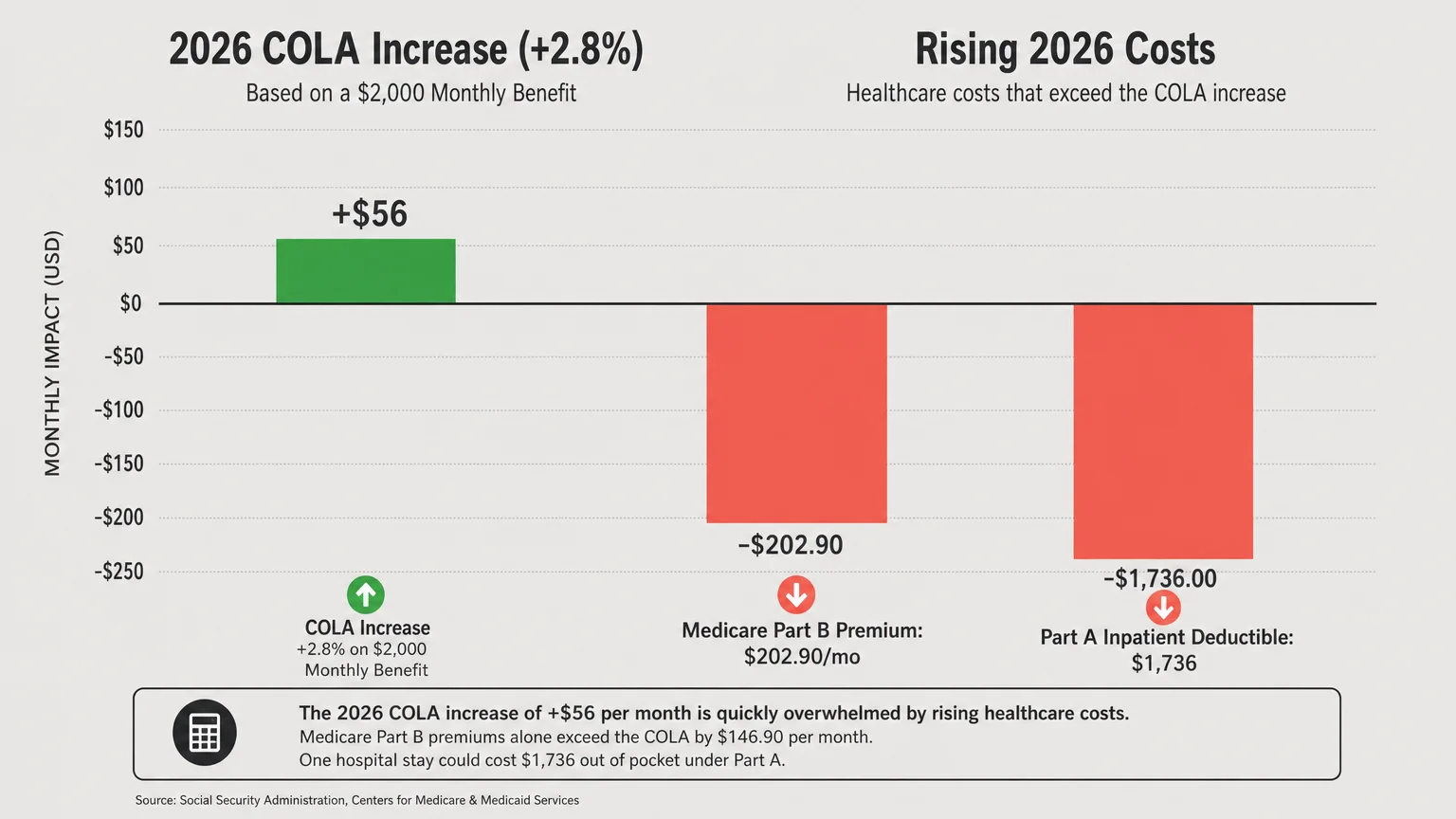

Retirees are facing a distinct financial squeeze. According to the Social Security Administration, the 2026 cost-of-living adjustment (COLA) is 2.8%. For a retiree receiving a $2,000 monthly benefit, that translates to a modest $56 increase. However, the standard Medicare Part B premium has risen to $202.90 per month in 2026, and the Part A inpatient hospital deductible now sits at $1,736. These rising healthcare costs quickly consume your COLA boost.

To protect your purchasing power, relocating to a low-cost, tax-friendly region is a highly effective strategy. The Midwest has quietly transformed into a haven for budget-conscious seniors. Several state legislatures have recognized the economic value of attracting retirees and have slashed taxes on pensions, 401(k) distributions, and Social Security benefits.

“Price is what you pay. Value is what you get.” — Warren Buffett, Investor

By moving to a carefully chosen Midwestern town, you can drastically reduce the price you pay for housing and taxes while maximizing the value of your retirement savings. Below is a quick comparison of the state tax policies for our top four hidden gem destinations.

| State | State Income Tax on Social Security? | State Tax on Pensions and 401(k)s | State Estate or Inheritance Tax? |

|---|---|---|---|

| Iowa | No | Exempt for residents age 55 and older | No (Repealed) |

| Illinois | No | Most retirement income is exempt | Yes (Estate tax applies to large estates) |

| South Dakota | No | No state income tax | No |

| Michigan | No | 100% deduction available in 2026 (up to limits) | No |

1. Decorah, Iowa: The Small-Town Tax Haven

Iowa has recently executed some of the most retiree-friendly tax reforms in the nation, making it a premier destination for your golden years. Starting in 2023, the state completely stopped taxing retirement income for anyone 55 and older. This sweeping exemption applies to pensions, 401(k)s, and IRAs. Furthermore, Iowa transitioned to a flat individual income tax rate, which sits at an affordable 3.8% for the 2025 and 2026 tax years.

Nestled in the rolling bluffs of northeastern Iowa, Decorah is a small town that punches far above its weight in culture and livability. Known for its rich Norwegian heritage, the town features the famous Vesterheim museum, vibrant community festivals, and miles of accessible walking trails.

Housing in Decorah remains highly accessible. Median home values hover around $230,000, allowing you to downsize comfortably without draining your nest egg. If you prefer independent living communities, the local options are moderately priced and offer a close-knit, welcoming atmosphere. For seniors who want a quiet, picturesque retirement supported by an incredibly generous state tax code, Decorah is a true hidden gem.

2. Peoria, Illinois: The Surprising Healthcare and Affordability Hub

Illinois often gets a bad reputation for its overall tax burden, but the state treats retirees remarkably well. Illinois completely exempts Social Security, public pensions, and qualified retirement plan distributions (like your 401(k) and IRA) from state income tax. If the bulk of your income comes from these sources, your state income tax bill could be practically zero.

Peoria frequently ranks at the top of national lists for Midwest retirement, and for good reason. The affordability is staggering. Average home values in Peoria sit around $131,000—a fraction of the national average. This deep discount on housing allows you to buy a beautiful home outright and keep your remaining capital invested.

Beyond cheap housing, Peoria shines in healthcare. It is home to the massive OSF Saint Francis Medical Center, providing you with access to top-tier specialists, advanced cardiac care, and comprehensive senior health services right in your backyard. You get the medical infrastructure of a major city at the price point of a rural town.

3. Rapid City, South Dakota: The Zero-Income-Tax Frontier

If your primary goal is to shield your income from the government, look no further than South Dakota. The Mount Rushmore State is one of the few states in the country that levies exactly 0% in state income tax. Your Social Security benefits, pension payouts, and IRA withdrawals belong entirely to you.

Rapid City acts as the gateway to the Black Hills, offering an extraordinary quality of life for active retirees. The town is surrounded by national parks, scenic drives, and abundant wildlife. It features a lively downtown area with art galleries, restaurants, and historical sites.

While property taxes exist, the state’s average combined state and local sales tax rate is a reasonable 6.11%, and the gas tax is only 30 cents per gallon. South Dakota also has no estate tax and no inheritance tax, making it incredibly easy to pass your wealth to the next generation. If you love the outdoors and hate filing state tax returns, Rapid City is an unbeatable choice.

4. Traverse City, Michigan: The Scenic Winner of New Tax Laws

Michigan recently overhauled its tax treatment of retirees, restoring the state to a highly competitive position. Under the Lowering MI Costs Plan (Public Act 4 of 2023), the state initiated a four-year phase-in to eliminate the so-called “pension tax.” By the 2026 tax year, eligible retirees can deduct 100% of their qualifying retirement and pension income up to generous inflation-adjusted limits (which sit at $64,040 for single filers and $128,080 for joint filers in 2026).

With these favorable tax rules in place, Traverse City emerges as a premium retirement destination. Situated on the stunning shores of Lake Michigan, this town offers a lifestyle that feels like a year-round vacation. Known for its cherry orchards, wineries, and vibrant arts scene, Traverse City keeps you active and engaged.

While housing in Traverse City is slightly more expensive than in Peoria or Decorah, it is still remarkably affordable compared to coastal retirement towns in Florida or California. You gain the aesthetic beauty of coastal living paired with the fresh water and distinct seasons of the upper Midwest.

Costly Errors to Sidestep When Relocating

Relocating for retirement is a massive financial pivot. Make sure you do not step into these common traps:

- Overlooking the Full Tax Footprint: A state that exempts retirement income might compensate by heavily taxing your property. For instance, while Illinois does not tax your 401(k) withdrawals, its property tax rates are among the highest in the country. Always measure the total combination of income, property, and sales taxes before buying a home.

- Fumbling the Medicare Transition: If you use Original Medicare (Parts A and B), your coverage travels with you anywhere in the United States. However, Medicare Advantage (Part C) and Part D prescription drug plans are tied to your specific geographic county. Moving out of your service area triggers a Special Enrollment Period. If you fail to update your coverage at Medicare.gov, you risk severe coverage gaps and permanent late-enrollment penalties.

- Underestimating the Climate Shift: The Midwest experiences true four-season weather. If you have lived your whole life in the Sunbelt, the transition to snowy winters requires adjustment. Renting a home for a full year before committing to a purchase is a smart way to ensure the lifestyle truly fits your expectations.

When DIY Isn’t Enough

While packing boxes and changing your mailing address is straightforward, the financial logistics of moving across state lines can get incredibly complicated. Consider hiring a professional in these scenarios:

- Establishing Legal Domicile: If you plan to split your time—spending summers in Michigan and winters in a southern state—you must legally prove your primary residency to secure the best tax rates. A CPA can help you track your days and file the correct documentation to prevent two different states from claiming you owe them income tax.

- Navigating Interstate Estate Planning: Laws dictating trusts, probate, and medical directives vary wildly by state. Moving requires updating your will and estate plan with an attorney licensed in your new jurisdiction to ensure your assets are protected.

- Managing Required Minimum Distributions (RMDs): Withdrawing funds under a new state’s tax regime requires setting up proper withholding amounts. A financial advisor can calculate these distributions correctly based on current IRS and state guidelines, ensuring you do not underpay your estimated taxes.

Frequently Asked Questions

Do all Midwest states exempt Social Security from taxes?

No, but a large majority of them do. States like Illinois, Iowa, Michigan, and South Dakota fully exempt Social Security benefits from state income taxes. A few states still tax Social Security under specific income thresholds, so always verify the current rules with your new state’s department of revenue.

Does moving to a new state affect my Social Security benefit amount?

Your federal Social Security benefit amount does not change simply because you move to a new state. The check sent by the Social Security Administration remains the same. However, the net amount you keep in your bank account may increase if your new home state does not tax those benefits.

How do I find out what specific state benefits I qualify for after moving?

Once you establish residency in your new town, you can use USA.gov Benefits or contact the local Area Agency on Aging. They can connect you with state-specific property tax freezes, utility assistance programs, and senior transit discounts.

Relocating to the Midwest offers a practical, highly effective way to stretch your retirement budget. By leveraging friendly tax codes, affordable housing, and excellent local amenities, you can secure a financially stable and deeply rewarding retirement. Take the time to visit these hidden gems, run the numbers on your personal tax situation, and map out your next great adventure.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.