If you want to stretch your retirement income in 2027, picking the right state is the most profitable decision you can make. The landscape of senior benefits is shifting rapidly, with states quietly passing sweeping tax cuts on pensions and eliminating taxes on Social Security. Meanwhile, a rising wave of political power has pushed 14 states to adopt formal Master Plans for Aging, ensuring local governments actively support your healthcare and housing needs. You no longer have to settle for sunshine alone. By understanding which locations offer zero income tax, robust senior infrastructure, and true political leverage, you can protect your assets and build a significantly more secure retirement.

The Federal Financial Landscape Driving State Relocation

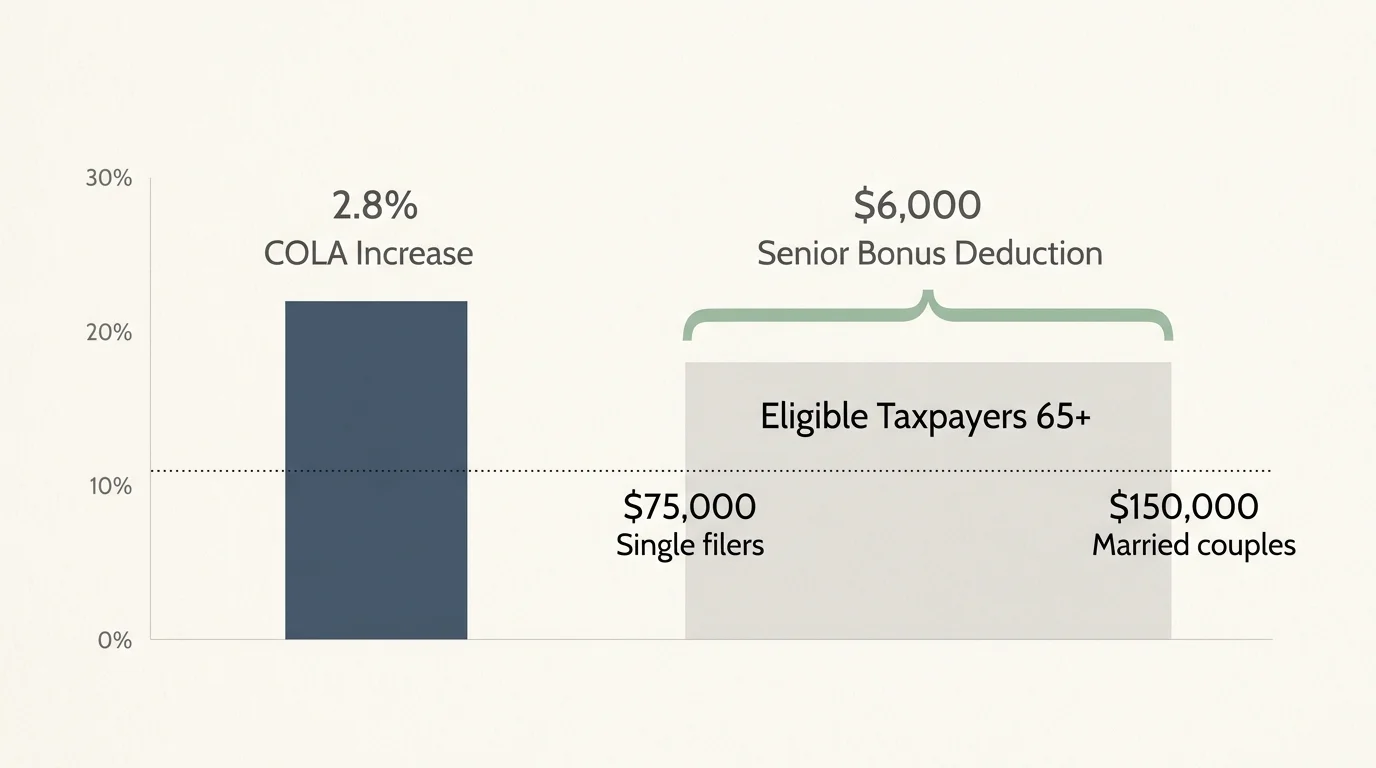

Recent federal changes have made state tax policy more critical than ever. Every dollar of income matters when you rely on a fixed budget. In 2026, the Social Security Administration implemented a 2.8% cost-of-living adjustment (COLA). While this increase helps preserve your buying power against inflation, it also pushes many seniors closer to federal and state income tax thresholds. If your state taxes this additional income, your real-world gain shrinks considerably.

To combat inflation and rising tax burdens, the federal government recently implemented the “One Big Beautiful Bill,” which introduced a temporary $6,000 Senior Bonus Deduction for eligible taxpayers aged 65 and older. This deduction, available through tax year 2028, provides significant federal tax relief. It phases out for single filers earning over $75,000 and married couples earning over $150,000. You can combine this bonus with the standard deduction for seniors to aggressively lower your federal taxable income.

However, federal relief is only half the battle. Your state government has the power to either multiply these federal savings or drain them away through high income brackets, property taxes, and sales taxes. Living in a state that aligns with your financial strategy is the single most effective way to keep your wealth intact.

States Eliminating Taxes on Social Security and Pensions

For decades, retirees simply fled to states with no broad income tax, such as Florida, Texas, and Nevada. But as we approach 2027, you have far more nuanced options. State legislatures are actively competing for older residents by dramatically lowering or eliminating taxes specifically on retirement income.

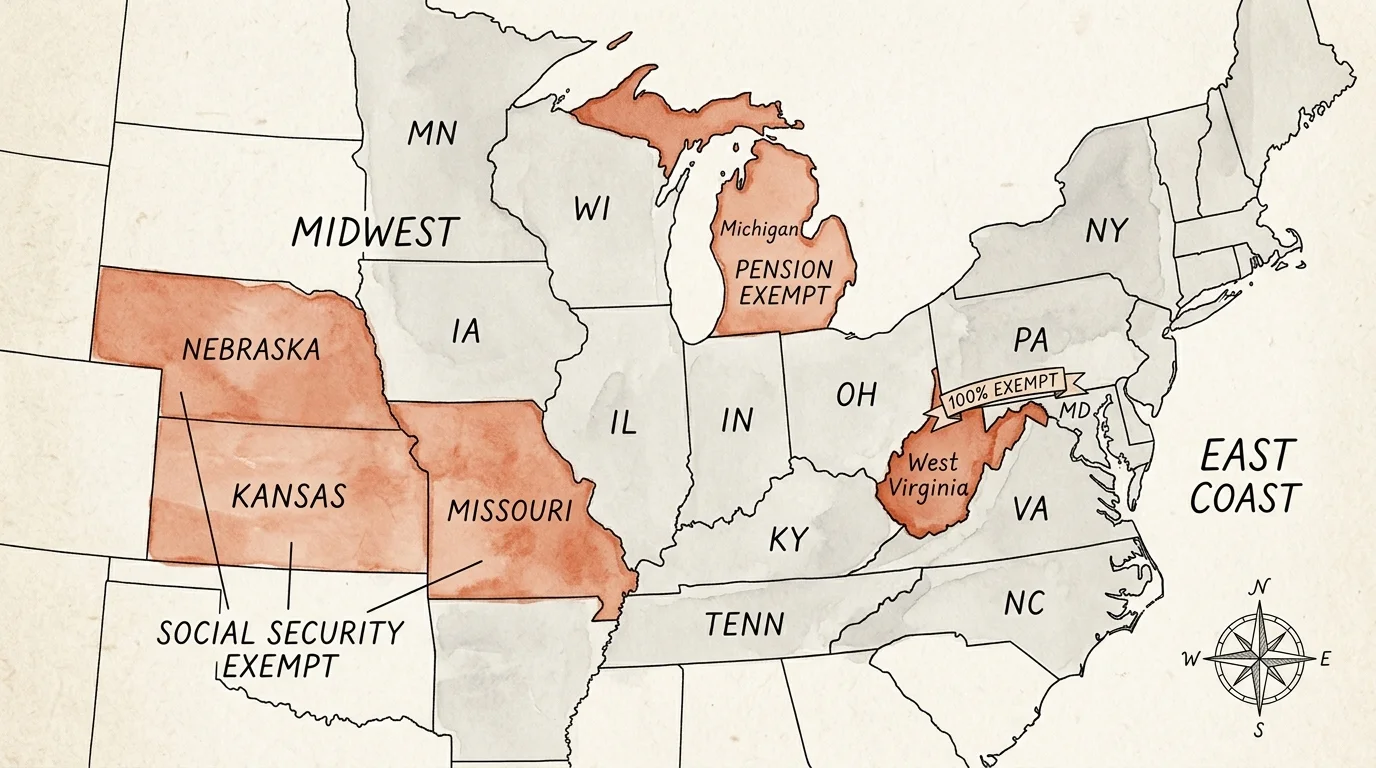

As of 2026, 42 states refuse to tax your Social Security benefits. Recent legislative victories have made the national map much friendlier for retirees:

- West Virginia: Fully phased out its state tax on Social Security benefits in 2026, making these payments 100% exempt for retirees.

- Michigan: Joined the tax-friendly list for pensions starting in the 2026 tax year, offering massive relief to former private-sector and union workers who rely on defined-benefit plans.

- The Midwest Shift: Missouri, Kansas, and Nebraska all completely eliminated their state taxes on Social Security benefits leading up to this year.

Only eight states still tax Social Security in some capacity: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont. Even within these states, immense political pressure from older voting blocs is forcing legislative compromises. For example, Colorado now allows residents aged 65 and older to fully deduct their Social Security benefits from their state taxable income. If your primary income source is Social Security or a traditional pension, moving just one state over could save you thousands of dollars annually.

Property Taxes and Senior Exemptions: The Hidden Financial Lever

You cannot evaluate a state’s financial viability purely on income tax. Property taxes act as a hidden financial lever that can crush a poorly planned retirement. States with zero income tax often offset their budgets by aggressively taxing real estate. If you buy a home in a high-property-tax state without understanding the local exemption laws, your fixed income will suffer.

The most financially advantageous states for retirees offer robust property tax relief specifically designed for seniors. These programs typically fall into three categories:

- Age-Based Homestead Exemptions: States like Florida and Georgia offer additional homestead exemptions for residents over age 65, directly lowering the assessed taxable value of their primary residence.

- Property Tax Freezes: Texas provides an over-65 school tax ceiling. Once you turn 65 and apply for the exemption, the amount you pay in school district property taxes cannot increase, regardless of how much your home appreciates in value.

- Circuit Breaker Programs: High-tax states like New York and New Jersey offer circuit breaker rebates, which refund a portion of your property taxes if they exceed a certain percentage of your income.

Before buying a retirement home, always check with the local county assessor to verify exactly which senior property tax exemptions you qualify for and how long you must be a resident to claim them.

The Political Shift: Master Plans for Aging

Financial gains mean very little if a state lacks the infrastructure to support your physical and social well-being. This is where political leverage comes into play. Currently, 14 states have adopted Multisector Plans for Aging (MPAs)—comprehensive, 10-year blueprints designed to restructure policies across health, housing, transportation, and community engagement. These states recognize that by 2030, older adults will outnumber children, and they are allocating budgets to prepare.

Living in a state with an MPA means your local government is legally and politically committed to funding senior initiatives. Notable examples include:

- California: The state’s progressive Master Plan for Aging tracks real-time data on affordable housing, caregiving resources, and age-friendly public transportation across all counties.

- Florida: The recently implemented 2026-2029 State Plan on Aging focuses heavily on combating ageism, supporting family caregivers, and expanding long-term care advocacy.

- Maryland: The state’s ambitious 10-year plan aims to build a “longevity ecosystem” that optimizes healthcare affordability and economic opportunity for its aging residents.

When selecting a retirement destination, confirming the existence of a Master Plan for Aging is just as important as reviewing state tax brackets. It guarantees that political momentum is working in your favor to improve local Administration for Community Living resources, home-care funding, and age-friendly urban design.

Balancing Relocation with Medicare and Healthcare Costs

While Medicare is a federal program, your out-of-pocket healthcare costs are heavily influenced by your zip code. The availability, pricing, and network quality of Medicare Advantage (Part C) plans and Medigap (Medicare Supplement) policies vary drastically from state to state.

For 2026, the Centers for Medicare & Medicaid Services set the standard Medicare Part B premium at $202.90 per month, with an annual deductible of $283. However, your relocation strategy can inadvertently trigger higher premiums. If you sell a highly appreciated home to fund your move, or if you execute a massive Roth IRA conversion before establishing residency in a tax-free state, your modified adjusted gross income (MAGI) will spike.

This income spike can trigger an Income-Related Monthly Adjustment Amount (IRMAA) surcharge. IRMAA is a progressive surcharge that forces high-income beneficiaries to pay a larger share of Medicare’s costs. Depending on your tax bracket, an IRMAA surcharge can easily double or triple your Part B and Part D premiums for the year. Relocating requires precise tax planning to ensure your move does not inadvertently penalize your healthcare budget.

“Taxes will be the single biggest factor that separates people from their retirement dreams.” — Ed Slott, CPA and Retirement Expert

Comparing Top States Making Moves for Seniors

To help you evaluate your relocation options, here is a quick comparison of how several prominent retirement destinations stack up regarding taxes and political support in 2027.

| State | State Income Tax Structure | Social Security Tax | Master Plan for Aging (MPA) Active |

|---|---|---|---|

| Florida | None | Exempt | Yes (2026-2029 Plan) |

| Michigan | 4.25% Flat Rate | Exempt | No |

| Colorado | 4.40% Flat Rate | Deductible at Age 65+ | Yes |

| West Virginia | Graduated Brackets | Exempt (as of 2026) | No |

| Nevada | None | Exempt | No |

Pitfalls to Watch For

Relocating for retirement can be highly lucrative, but it is easy to make permanent, costly mistakes. Watch out for these four common pitfalls when choosing your destination:

- Fixating on Income Tax While Ignoring Sales and Property Taxes: A state might boast zero income tax, but they must generate revenue elsewhere. Texas and Florida rely heavily on property taxes and sales taxes. If you buy an expensive home and spend heavily on taxable goods, you might pay more to the state than you did under an income tax regime.

- Failing to Establish Legal Domicile: If you move to a tax-free state like Nevada but spend six months of the year in your old home in California, your former state will likely demand income taxes. You must formally break ties by changing your driver’s license, voter registration, vehicle titles, and primary medical providers to prove your new residency.

- Misunderstanding Pension Taxation Rules: Not all retirement income is treated equally under state law. Some states exempt military, federal, and local government pensions entirely, but fully tax distributions from private 401(k)s and traditional IRAs. Always verify how the state classifies your specific income streams.

- Overlooking Rural Healthcare Access: Moving to an isolated, inexpensive rural town might seem idyllic for your budget. However, if the nearest top-tier hospital or specialized cardiologist is a three-hour drive away, it could severely compromise your health and force a costly secondary move later in life.

Getting Expert Help

State laws, tax codes, and federal health programs change annually. Because your financial baseline is entirely unique, you should strongly consider consulting a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) if you find yourself in any of the following scenarios:

- You are selling a highly appreciated asset: A professional can help you time the sale of your primary home or business to minimize capital gains exposure and legally avoid Medicare IRMAA surcharges.

- Your income originates from multiple states: If you spent your career in New York but are retiring in Florida, a CPA can help you navigate complex non-resident tax returns and ensure your former state does not overstep its bounds.

- You need long-term care and estate planning: Medicaid look-back periods and asset protection laws vary drastically by state. An elder law attorney can help you shield your estate from exorbitant nursing home costs while complying with local regulations.

Frequently Asked Questions

Do I have to pay taxes to my old state if my pension is from a company located there?

No. Federal law prohibits states from taxing the retirement income of non-residents. If you firmly establish your legal domicile in a new state, your former state cannot tax your pension, 401(k), or IRA distributions, regardless of where the company is headquartered.

Will my Medicare Supplement (Medigap) plan travel with me if I move out of state?

Yes, standard Medigap plans are federally standardized and valid with any doctor or facility in the United States that accepts Original Medicare. However, if you are enrolled in a Medicare Advantage (Part C) plan, you will almost certainly need to enroll in a new plan specific to your new county, as Advantage networks are highly localized.

What exactly is a Master Plan for Aging?

A Master Plan for Aging (MPA) is a formal, cross-sector blueprint created by state governments to prepare for incoming demographic shifts. It directs public funding, state departments, and policy toward critical issues affecting older adults, such as building affordable senior housing, expanding home-based healthcare access, and improving public transit infrastructure.

By staying thoroughly informed about shifting tax laws, checking official Internal Revenue Service brackets, and evaluating state-level political support, you can strategically position yourself for a more prosperous lifestyle. Take the time to evaluate your specific income sources, healthcare needs, and lifestyle goals against the laws of your target state. A well-planned move does more than save money; it buys peace of mind.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.