Ignoring your financial checklist during retirement can quietly drain your hard-earned nest egg. Navigating the complex web of changing benefits, tax rules, and healthcare premiums requires proactive planning so you never leave money on the table. In 2026, shifting figures like the new 2.8% Social Security Cost-of-Living Adjustment (COLA) and a $202.90 standard Medicare Part B premium mean your previous financial strategy might already be outdated. By systematically reviewing your benefits, you can maximize government entitlements, leverage the latest senior tax deductions, and protect your savings from unexpected medical costs. This checklist breaks down exactly what you must review today to secure your income and enjoy a financially stress-free retirement.

Quick Summary

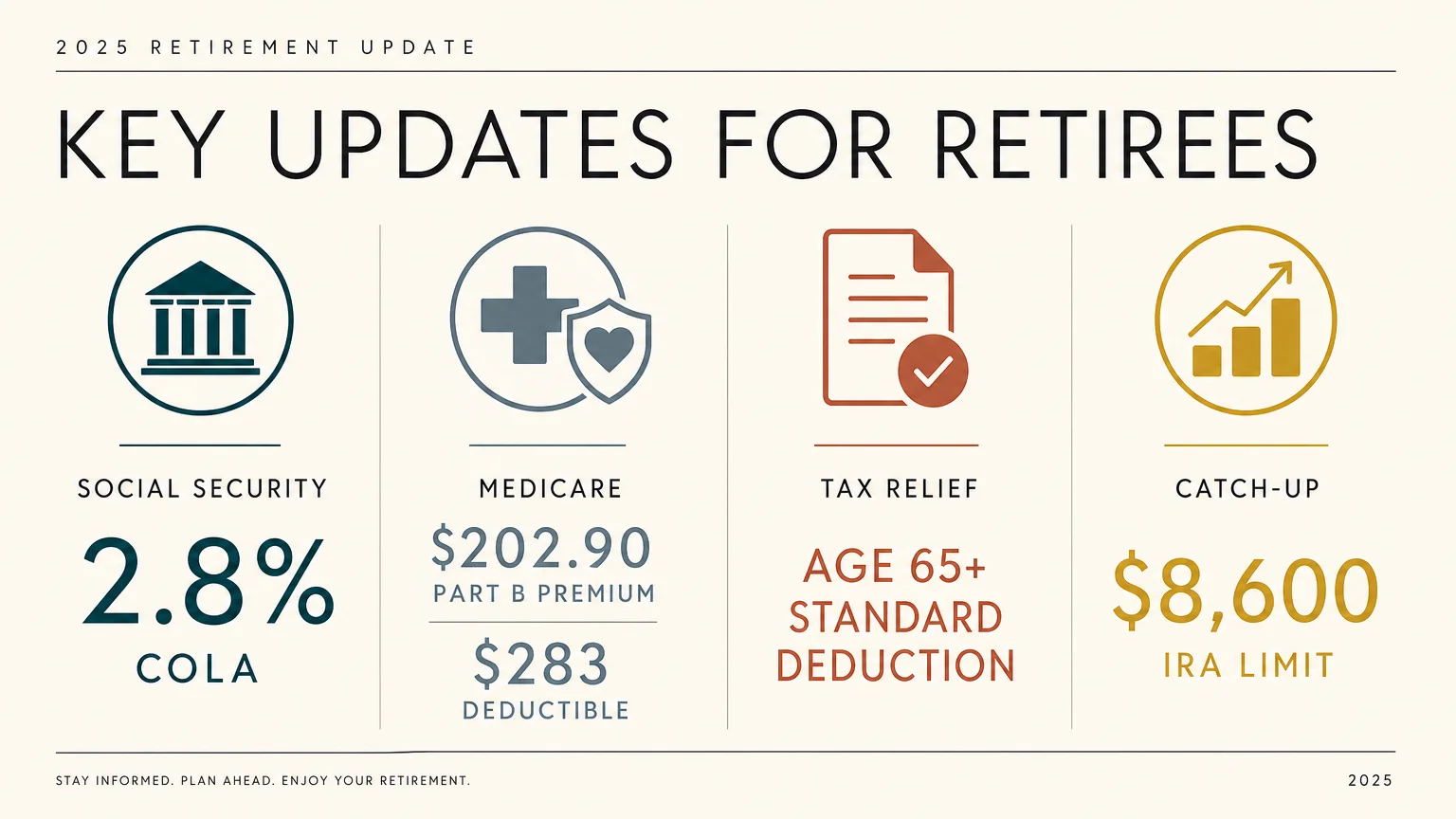

- Social Security Updates: Factor the 2026 2.8% COLA into your monthly budget to keep pace with inflation.

- Medicare Adjustments: Review your health coverage alongside the new $202.90 standard Part B premium and the $283 annual deductible.

- Tax Relief: Claim the expanded 2026 standard deduction, which provides thousands of dollars in extra tax relief if you are over age 65.

- Catch-Up Contributions: Maximize your retirement accounts with increased 2026 limits, including an $8,600 total allowance for IRAs if you are 50 or older.

Step 1: Maximize Your Social Security and Calculate the COLA

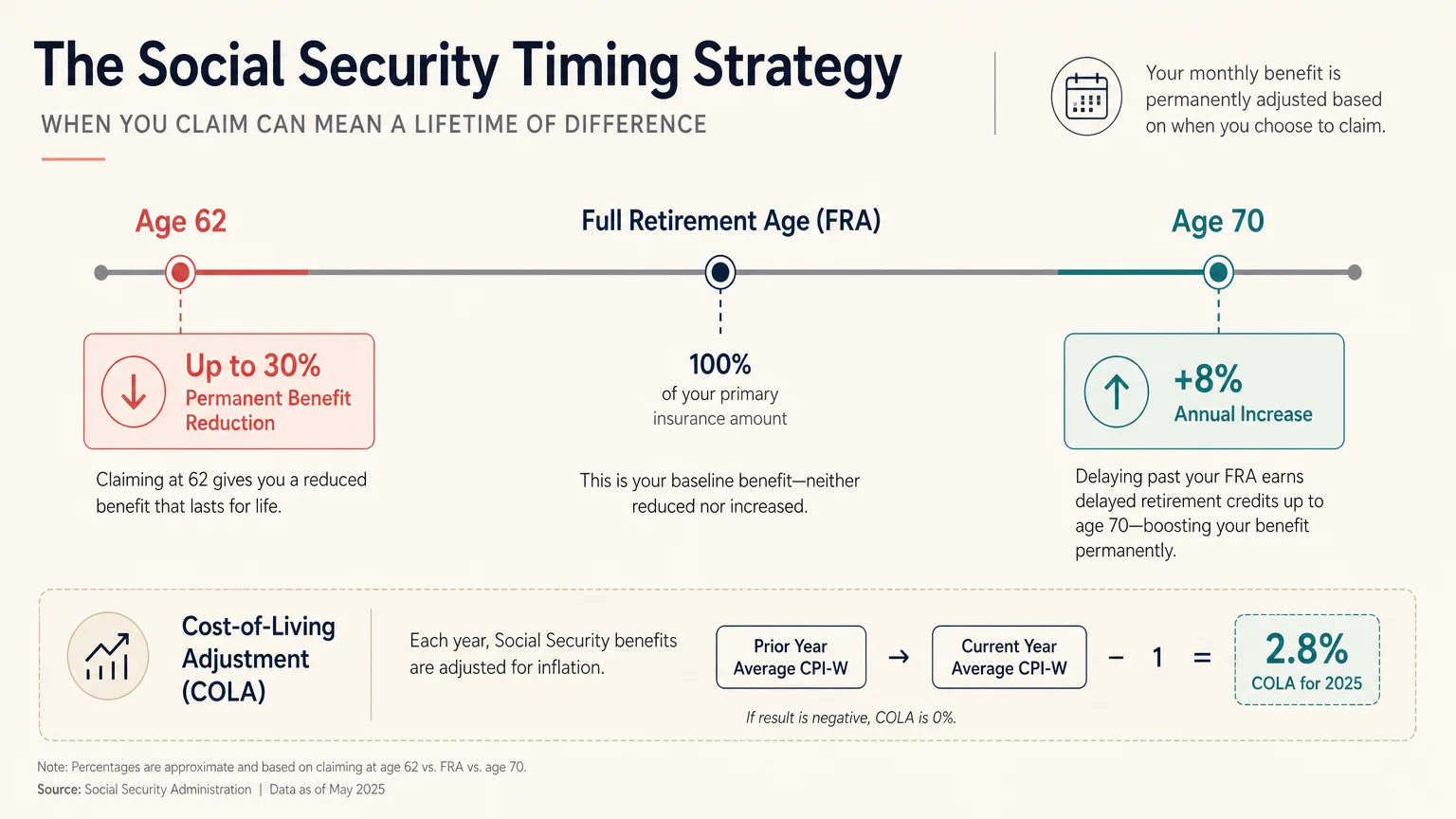

Social Security remains the bedrock of retirement income for most Americans. However, treating your benefits as a static number is a mistake. The Social Security Administration evaluates inflation annually and adjusts payments to help retirees maintain their purchasing power.

According to the Social Security Administration (2026), the Cost-of-Living Adjustment (COLA) is 2.8%. If your monthly benefit currently sits at $1,800, a 2.8% COLA adds roughly $50 per month—putting an extra $600 in your pocket annually. You must actively review your annual benefit statement to understand how this increase affects your broader tax picture. To verify your exact benefit amount, log into your secure account at SSA.gov.

Beyond the annual COLA, you should routinely audit your claiming strategy:

- Verify Your Earnings Record: Mistakes happen. Check your earnings record on the SSA website to ensure every year of your working life is accurately reported. Your benefit is calculated based on your highest 35 years of indexed earnings; a single missing year will drag down your monthly check.

- Assess Spousal Benefits: If you are married, divorced, or widowed, you might be eligible for benefits based on your spouse’s earnings. A lower-earning spouse can claim up to 50% of the higher earner’s primary insurance amount, which often yields a higher payout than claiming on their own record.

- Strategize Your Claiming Age: While you can claim benefits as early as age 62, doing so permanently reduces your monthly payout by up to 30%. Conversely, delaying past your Full Retirement Age (FRA) earns you delayed retirement credits, boosting your benefit by 8% per year until age 70. Evaluate your health, longevity, and immediate cash needs before locking in a claiming age.

Step 2: Audit Your Medicare Coverage and Navigate Part B Costs

Healthcare costs consistently rank as the top financial concern for retirees. Medicare coverage is not free, and the premiums fluctuate every year based on national healthcare expenditures and your personal income.

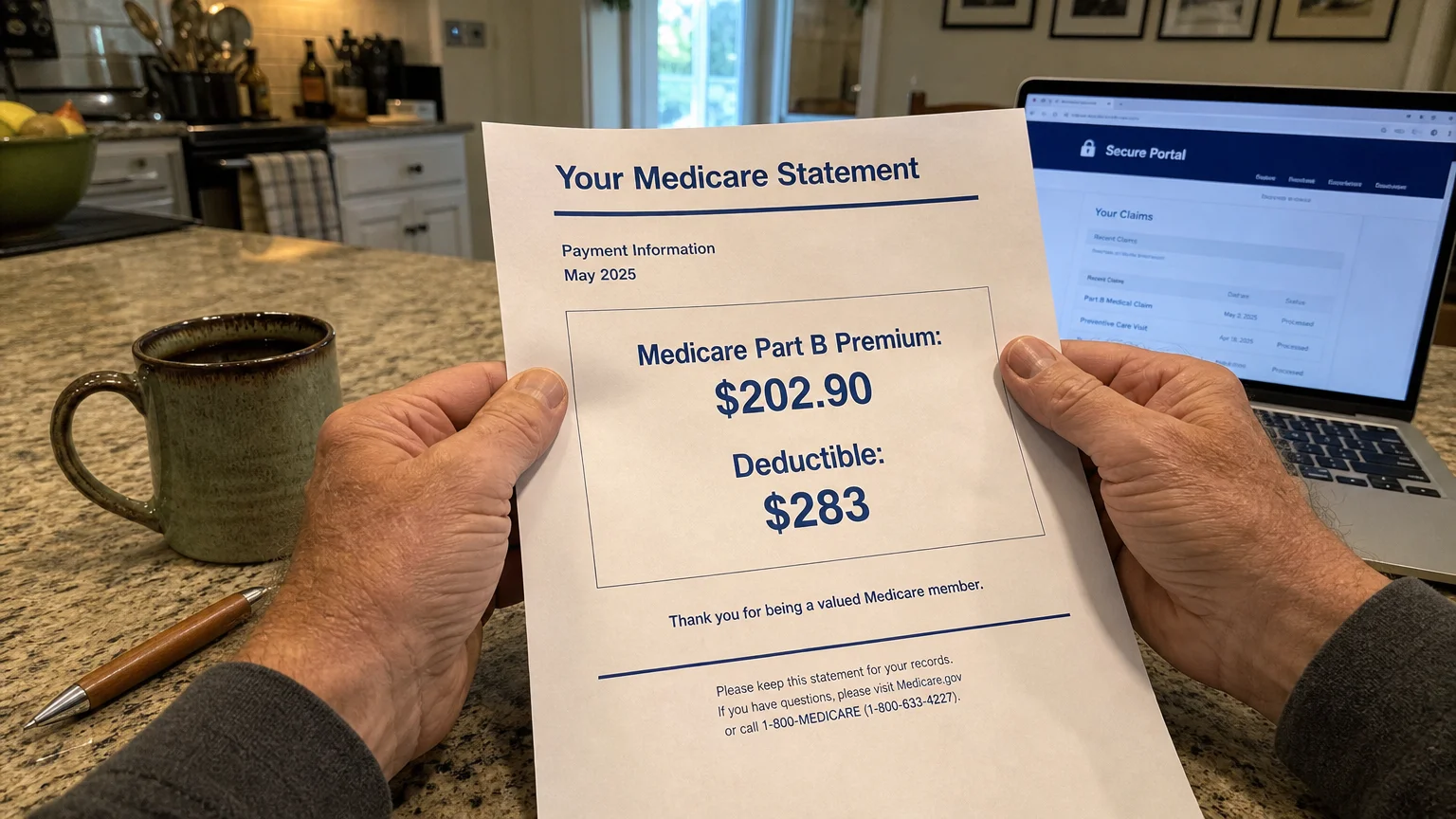

For 2026, the standard Medicare Part B premium sits at $202.90 per month, alongside an annual deductible of $283, according to the Centers for Medicare & Medicaid Services (CMS). However, Medicare does not apply a flat rate to everyone. If you had a high income two years ago, you will face an Income-Related Monthly Adjustment Amount (IRMAA).

IRMAA functions as a hidden tax on successful retirees. The Social Security Administration determines your 2026 premium based on your 2024 tax return. If your Modified Adjusted Gross Income (MAGI) exceeded $109,000 as a single filer or $218,000 as a married couple filing jointly, your Part B and Part D premiums will jump significantly above the base rate. You must factor these higher out-of-pocket costs into your monthly budget.

To protect your wallet, schedule an annual Medicare audit:

- Review Part D Formularies: Prescription drug plans change their covered medications (formularies) every year. A medication that cost you $10 a month last year might suddenly cost $50 a month this year. Use the plan finder tool on Medicare.gov during the Annual Enrollment Period (October 15 to December 7) to compare plans.

- File an IRMAA Appeal if Applicable: If your income dropped due to a life-changing event—such as retiring, getting divorced, or losing a spouse—you do not have to pay the higher IRMAA surcharge based on old income. You can file Form SSA-44 to request a premium reduction based on your current, lower retirement income.

- Compare Advantage vs. Supplemental Plans: Determine whether Original Medicare paired with a Medigap policy serves you better than a Medicare Advantage (Part C) plan. Medigap provides predictable out-of-pocket costs, while Advantage plans often limit you to specific provider networks.

Step 3: Capitalize on Senior-Specific Tax Deductions

Failing to optimize your taxes in retirement effectively throws money away. The IRS provides specific, generous tax breaks for seniors, starting with an expanded standard deduction. You must actively claim these benefits when filing your return.

According to the Internal Revenue Service (2026), the base standard deduction has increased to combat inflation. More importantly, taxpayers age 65 and older receive an additional standard deduction on top of the base amount. For single filers or heads of household, the extra deduction is $2,050. For married couples filing jointly, the extra deduction is $1,650 per qualifying spouse.

| Filing Status | 2026 Base Standard Deduction | Additional Deduction (Age 65+) | Total 2026 Deduction for Seniors |

|---|---|---|---|

| Single | $16,100 | $2,050 | $18,150 |

| Married Filing Jointly (Both 65+) | $32,200 | $3,300 ($1,650 per spouse) | $35,500 |

Because the total standard deduction for a senior married couple now reaches $35,500, very few retirees actually need to itemize their deductions. However, you should still track your medical expenses. If you do itemize, the IRS allows you to deduct unreimbursed medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI). This includes Medicare premiums, long-term care costs, and out-of-pocket medical bills.

“Taxes will be the single biggest expense in retirement. The goal is to move your money from accounts that are forever taxed to accounts that are never taxed.” — Ed Slott, CPA and Retirement Expert

Additionally, if you are 70½ or older, you can utilize Qualified Charitable Distributions (QCDs). A QCD allows you to transfer funds directly from your traditional IRA to an eligible charity. This transfer satisfies your Required Minimum Distribution (RMD) without adding a single dollar to your taxable income. For seniors hovering near an IRMAA threshold, a QCD is a brilliant strategy to lower AGI while supporting a good cause.

Step 4: Turbocharge Your Retirement Savings Before and During Retirement

Just because you are approaching retirement—or are already retired—does not mean you have to stop saving. If you still have earned income from consulting, a part-time job, or a spouse’s employment, you should continue funding your retirement accounts to take advantage of tax-deferred or tax-free growth.

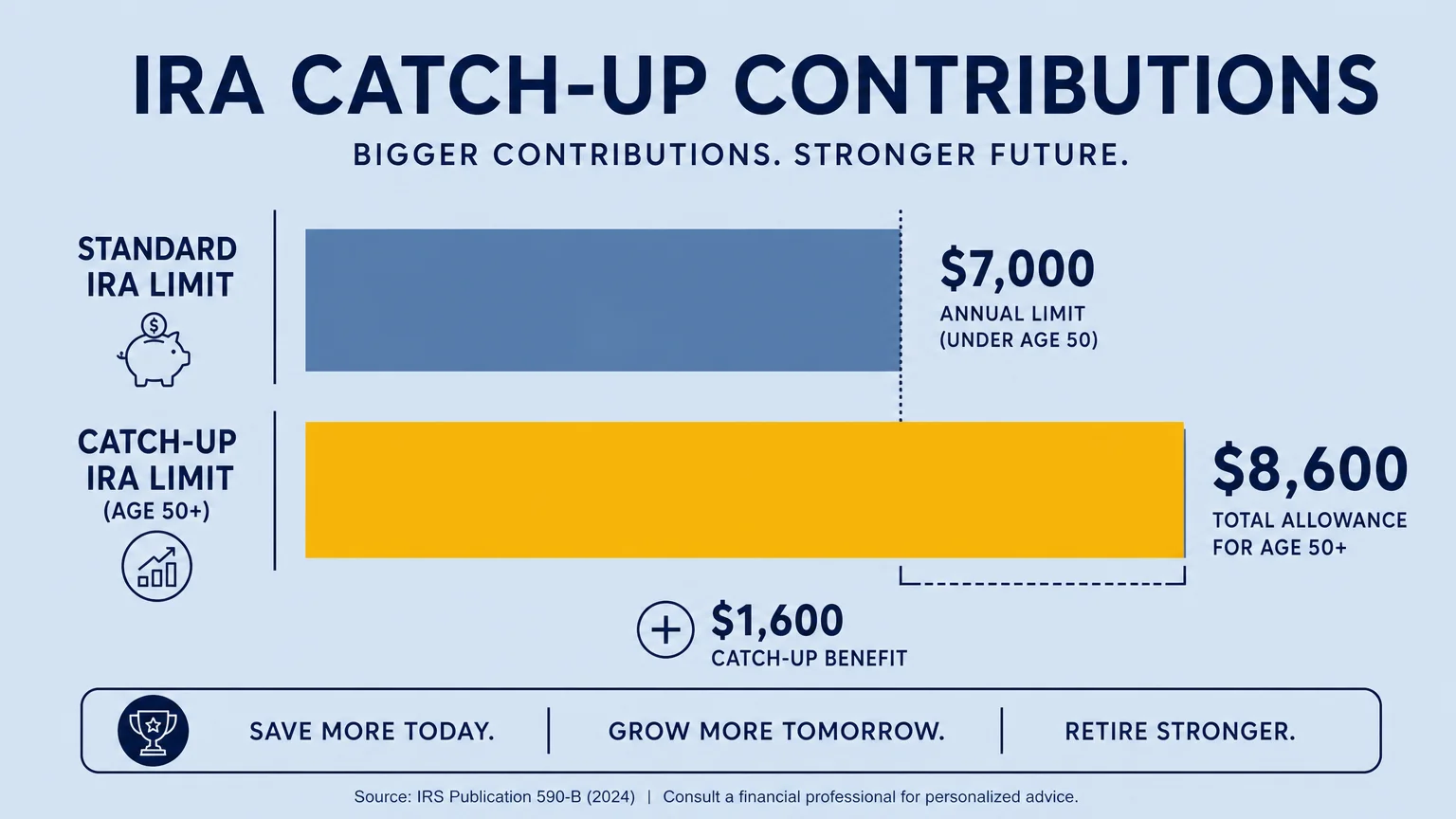

The IRS consistently raises contribution limits, and the rules heavily favor older workers. For 2026, the base contribution limit for Individual Retirement Accounts (IRAs) is $7,500. However, if you are age 50 or older, you qualify for an additional $1,100 catch-up contribution, bringing your total allowable IRA contribution to $8,600 for the year.

Workplace plans offer even higher thresholds. The 2026 contribution limit for 401(k), 403(b), and most 457 plans stands at $24,500, with substantial catch-up provisions for employees over age 50. Keep in mind that recent legislative changes mean high earners may be required to make their workplace catch-up contributions into a Roth account rather than a traditional pre-tax account.

If you have a High Deductible Health Plan (HDHP), do not overlook the Health Savings Account (HSA). The IRS (2026) raised HSA contribution limits to $4,400 for individuals and $8,750 for families. If you are 55 or older, you can contribute an extra $1,000 catch-up amount. HSAs offer an unparalleled triple-tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are entirely tax-free. You can learn more about managing these accounts at IRS.gov.

Step 5: Check Eligibility for Extra Assistance Programs

Many seniors mistakenly assume they earn too much to qualify for financial assistance. In reality, state and federal programs frequently adjust their income thresholds, and millions of older Americans miss out on benefits simply because they never applied.

You should routinely check your eligibility for programs that lower daily living expenses:

- BenefitsCheckUp: Operated by the National Council on Aging (NCOA), this free, confidential tool scans thousands of public and private programs to see if you qualify for help paying for food, medicine, or utilities.

- Medicare Savings Programs (MSPs): If your income is limited, your state may help pay your Medicare Part B premiums, deductibles, and coinsurance.

- Property Tax Relief: Almost every state offers some form of property tax reduction, freeze, or deferral for senior citizens. Check with your local county tax assessor’s office to see if you meet the age and income requirements to lower your annual property tax bill.

- SNAP (Supplemental Nutrition Assistance Program): Medical deductions can lower your net income calculation, making it easier for seniors to qualify for monthly food assistance.

What Can Go Wrong

Even with a checklist in hand, simple oversights can trigger severe financial penalties. Protect your retirement by avoiding these common pitfalls.

Missing the Medicare Initial Enrollment Period (IEP)

Your Medicare IEP is a strict seven-month window that begins three months before your 65th birthday month and ends three months after it. If you fail to enroll in Part B during this time—and you do not have creditable health coverage from an active employer—you will face a permanent late enrollment penalty. Your Part B premium will permanently increase by 10% for every full 12-month period you delayed enrollment.

Failing to Take Required Minimum Distributions (RMDs)

The IRS does not let you defer taxes on your traditional retirement accounts forever. Once you reach age 73 (or age 75, depending on your birth year), you must withdraw a minimum amount from your traditional IRAs and 401(k)s every year. If you forget to take your RMD, or calculate the amount incorrectly, you will face a steep penalty of up to 25% on the amount you failed to withdraw. You can reduce this penalty to 10% if you correct the mistake quickly, but it is much easier to automate your distributions.

Triggering the “Tax Torpedo” on Social Security

Social Security benefits are not automatically tax-free. If your “provisional income”—which includes half of your Social Security benefit plus all other taxable income and municipal bond interest—exceeds $25,000 for a single filer or $32,000 for a joint filer, up to 50% of your benefits become taxable. If your provisional income exceeds $34,000 (single) or $44,000 (joint), up to 85% of your benefits are taxed. Taking massive withdrawals from a traditional IRA can inadvertently push your Social Security income into a higher taxable bracket.

Carrying Too Much Risk in Your Portfolio

When you transition from saving to spending, your investment strategy must shift. Relying on the same aggressive portfolio you had in your 40s exposes you to “sequence of returns risk.” If the stock market crashes right as you begin withdrawing funds, your portfolio will deplete rapidly, making it nearly impossible to recover. Diversify your assets into safer buckets to cover immediate living expenses while leaving long-term funds invested for growth.

“Retirement is not just about what you’ve saved, it’s about what you keep.” — Jean Chatzky, Financial Expert

When to Consult a Professional

While you can handle many aspects of this checklist independently, certain milestones warrant expert guidance. Consider hiring a fee-only fiduciary financial planner or a certified public accountant (CPA) in the following scenarios:

- Navigating Complex IRMAA Appeals: If you recently retired and need to file Form SSA-44 to eliminate a Medicare surcharge, a professional ensures you provide the correct documentation to prove your life-changing event.

- Optimizing Your Withdrawal Sequence: Deciding which accounts to tap first—taxable brokerage, traditional IRA, or Roth IRA—requires precise tax planning. A professional will calculate the most tax-efficient withdrawal strategy to extend the life of your portfolio.

- Coordinating Spousal Claiming Strategies: If you and your spouse have vastly different earnings histories and life expectancies, a financial planner can run software simulations to determine the exact age each of you should claim Social Security to maximize lifetime benefits.

Frequently Asked Questions

What is the Social Security COLA for 2026?

The Social Security Administration announced a 2.8% Cost-of-Living Adjustment for 2026. This increase helps your monthly benefits keep pace with inflation and applies to your payments starting in January 2026.

Can I still contribute to an IRA if I am already retired?

Yes, but you must have “earned income.” If you or your spouse still earn money from wages, salaries, or self-employment, you can contribute to an IRA up to the amount of your earned income or the annual limit ($8,600 for those 50 and older in 2026), whichever is less. Pension, Social Security, and investment income do not count as earned income.

How do I appeal a Medicare IRMAA surcharge?

If your income has decreased due to a qualifying life-changing event like retirement, marriage, or divorce, you can file Form SSA-44 with the Social Security Administration. This form requests that they calculate your Part B and Part D premiums using your current estimated income rather than the standard two-year lookback.

At what age do Social Security benefits become tax-free?

Social Security benefits never become automatically tax-free based on your age. Whether you pay federal income taxes on your benefits depends entirely on your provisional income level for that specific tax year.

Next Steps for Your Retirement Plan

Going through this benefits checklist annually is the most effective way to protect your financial independence. Start by reviewing your Social Security statement and Medicare plan this week. Small adjustments—like appealing an IRMAA surcharge, tweaking your tax withholdings, or opening an HSA—compound significantly over the course of a two- or three-decade retirement. By staying informed and proactive, you empower yourself to make confident decisions that secure your future.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.