Eliminating state income taxes from your budget immediately frees up cash to stretch your fixed income further. With the average Social Security check for retired workers sitting near $2,071 per month in 2026, protecting every dollar of your benefits is critical. Nine states currently charge zero income tax, but finding a place that pairs this advantage with affordable housing requires research. Sky-high property taxes and soaring home prices routinely offset tax savings in popular coastal destinations. Fortunately, several mid-sized cities and charming towns offer median home prices drastically below the national average. From the warm climate of Florida to the scenic mountains of Wyoming, here are fifteen tax-friendly destinations where your retirement savings go much further.

Why State Taxes Matter for Social Security Retirees

When you rely on a fixed income, predictability is your greatest asset. While the federal government taxes up to 85 percent of your Social Security benefits depending on your combined income, your state sets its own rules. Living in a state that taxes your wages, retirement distributions, and Social Security benefits can easily drain thousands of dollars from your budget every single year.

Currently, nine states impose zero broad-based state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Relocating to one of these states means you keep more of your pension, 401(k) withdrawals, and Social Security checks.

“Taxes will be the single biggest expense in retirement. It’s not about what you make; it’s about what you keep.” — Ed Slott, CPA and Retirement Expert

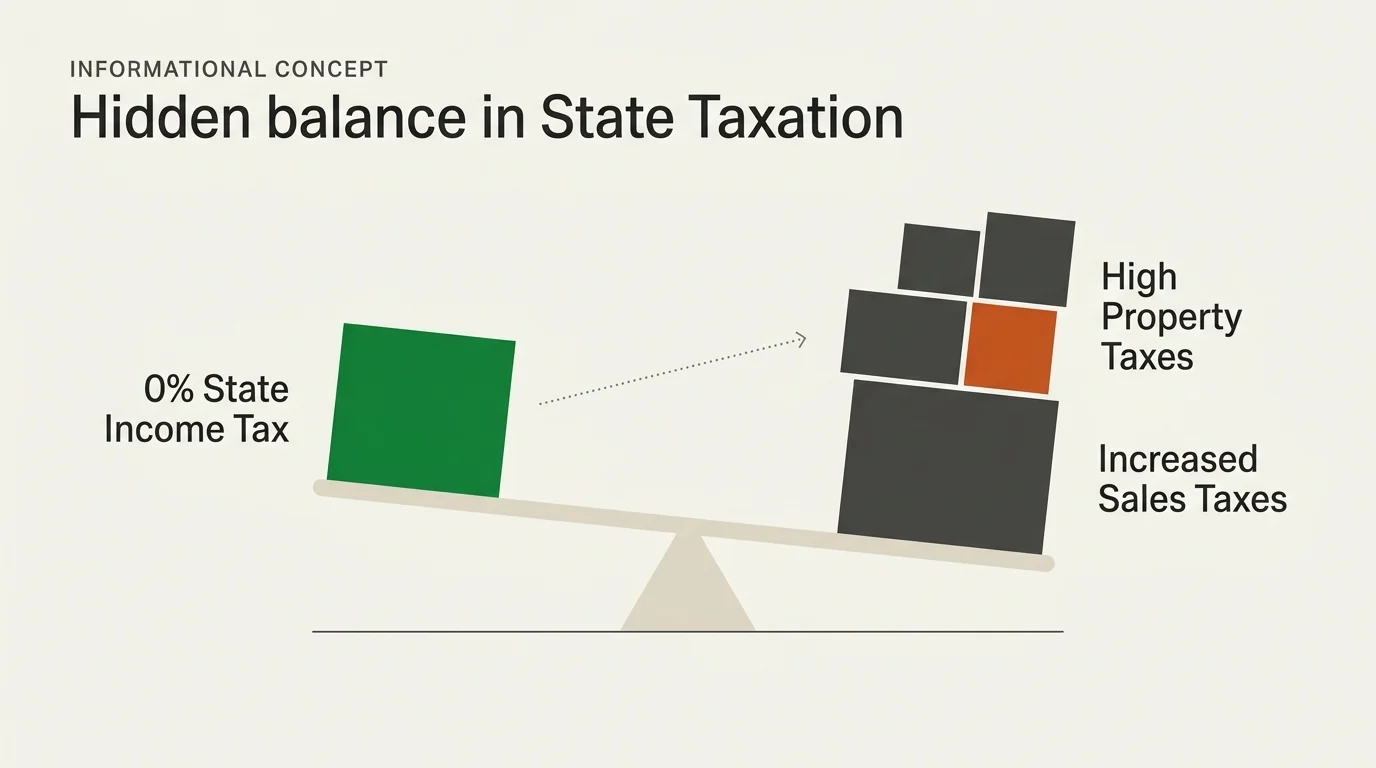

Keep in mind that “tax-free” only refers to income taxes. States must fund their roads, schools, and emergency services somehow, which usually means leaning heavier on sales taxes or property taxes. For instance, New Hampshire fully eliminated its interest and dividends tax in 2025, but its property taxes remain among the highest in the country. That is why finding an affordable housing market within a tax-free state is the ultimate strategy for budget-conscious retirees.

Comparing the Zero-Tax States

Before packing your boxes, review how these states balance their tax codes. The table below outlines the nine income-tax-free states and their typical property and sales tax burdens to help you gauge overall affordability.

| State | Income Tax | Average Sales Tax Base | Typical Property Tax Burden |

|---|---|---|---|

| Alaska | 0% | 0% (Local taxes vary) | Medium to High |

| Florida | 0% | 6.00% | Medium |

| Nevada | 0% | 6.85% | Low |

| New Hampshire | 0% | 0% | Very High |

| South Dakota | 0% | 4.50% | Medium |

| Tennessee | 0% | 7.00% | Low |

| Texas | 0% | 6.25% | High |

| Washington | 0% (Excludes high capital gains) | 6.50% | Medium |

| Wyoming | 0% | 4.00% | Low |

Affordable Florida Destinations

Florida remains the quintessential retirement haven. The state boasts favorable weather, robust Medicare networks, and a complete lack of state income, estate, or inheritance taxes. However, coastal hotspots like Miami, Naples, and West Palm Beach command massive real estate premiums. By looking inland or slightly north, you can find the Florida lifestyle at a fraction of the cost.

- Ocala: Known globally as the “Horse Capital of the World,” Ocala offers wide-open green spaces and a remarkably low cost of living. In 2026, median home prices hover between $275,000 and $303,000. You gain easy access to natural springs and the Ocala National Forest, along with top-tier medical facilities in nearby Gainesville.

- Sebring: Situated in central Florida’s Highlands County, Sebring is surrounded by freshwater lakes perfect for boating and fishing. The median home price here is an incredibly affordable $236,000 to $262,000. The slower, small-town pace appeals to retirees looking to escape the traffic of Orlando and Tampa.

- Homosassa Springs: If you want to live near the Gulf Coast without paying premium beachfront prices, Homosassa Springs delivers. With a median home price of $279,000, you get access to a gorgeous wildlife state park and a laid-back fishing village atmosphere. Its slightly inland location also offers better protection from direct coastal weather events.

- Lake City: Located in north central Florida, Lake City is an emerging hub for budget-conscious retirees. Homes routinely list for around $254,000. The city offers quiet suburban living, proximity to freshwater springs, and excellent interstate access for road-tripping to larger cities.

Budget-Friendly Texas Cities

Texas does not tax your income, but it does levy significant property taxes to fund local municipalities. To make Texas work on a Social Security budget, you must target cities with very low baseline housing costs so that your property tax bill remains manageable. Fortunately, the Lone Star State is massive, offering plenty of affordable regional hubs.

- McAllen: Located in the deep south of Texas near the border, McAllen boasts one of the lowest costs of living in the United States. With median home prices hovering around $210,000, your Social Security checks will go incredibly far. The area is a famous haven for “Winter Texans” seeking warm weather from December through March.

- El Paso: Nestled in the high desert of West Texas, El Paso offers stunning mountain views, a dry climate, and consistent sunshine. It frequently ranks as one of the safest large cities in the country. With median home prices ranging from $230,000 to $250,000, you get big-city amenities on a small-town budget.

- San Antonio: While larger than the other cities on this list, San Antonio remains highly affordable compared to Austin or Dallas. The median home price sits between $290,000 and $334,000. The city offers an incredible cultural scene, the famous River Walk, and massive military and medical infrastructure, including the South Texas Medical Center.

- Corpus Christi: If you dream of retiring near the ocean but cannot stomach Florida or California prices, Corpus Christi is the answer. Located right on the Gulf of Mexico, the city offers a balanced real estate market with median home prices around $330,000. You gain immediate access to Padre Island and exceptional saltwater fishing.

Scenic and Affordable Tennessee

Tennessee fully phased out its “Hall Tax” on interest and dividends a few years ago, cementing its status as a true zero-income-tax destination. The state pairs this tax advantage with some of the lowest property taxes in the nation. For retirees who prefer four distinct seasons and rolling mountains over endless flat beaches, Tennessee is a premier choice.

- Johnson City: Tucked into the Appalachian Mountains in the northeast corner of the state, Johnson City anchors the “Tri-Cities” region. The median home price ranges from $250,000 to $300,000. It is a haven for outdoor enthusiasts, offering easy access to hiking, lakes, and a relaxed, small-town pace.

- Knoxville: Situated along the Tennessee River, Knoxville provides a vibrant college-town atmosphere courtesy of the University of Tennessee. The median home price of $314,000 to $327,000 buys you access to excellent healthcare networks, cultural events, and close proximity to the Great Smoky Mountains National Park.

- Chattanooga: Known as the “Scenic City,” Chattanooga has revitalized its downtown and riverfront over the past decade. It also boasts some of the fastest municipal internet in the country. With a median home price between $325,000 and $340,000, it remains highly accessible for retirees who want an active, modern community nestled in a valley.

Western Tax-Free Havens

If you prefer sweeping desert landscapes, rugged mountains, or evergreen forests, the western half of the United States offers several compelling tax-free retirement destinations. These locations provide distinct lifestyle choices while protecting your Social Security income.

- Pahrump, Nevada: Located just an hour west of Las Vegas, Pahrump offers a quiet, rural desert lifestyle with incredible affordability. The median home price sits around $340,000 to $375,000, and lots are typically an acre or more. You enjoy wide-open spaces while remaining close enough to Las Vegas for major medical care, dining, and entertainment.

- Sioux Falls, South Dakota: South Dakota boasts zero state income tax and incredibly low business taxes, creating a booming local economy. Sioux Falls offers top-tier healthcare systems—including Sanford and Avera—and a growing downtown. The median home price is very reasonable at $310,000 to $327,000. If you do not mind cold winters, it is a fantastic financial sanctuary.

- Casper, Wyoming: Wyoming is an outdoor lover’s paradise with the lowest population density in the lower 48 states. Casper sits along the North Platte River and offers median home prices between $290,000 and $320,000. Retirees here enjoy world-class fly fishing, zero income tax, and a rugged, independent lifestyle.

- Spokane, Washington: Washington state does not tax standard retirement income or Social Security. While Seattle is notoriously expensive, Eastern Washington tells a different story. Spokane offers four distinct seasons, beautiful parks, and a median home price of $395,000 to $410,000—roughly half the cost of coastal Washington markets.

Pitfalls to Watch For

Relocating to a zero-income-tax state is a powerful financial move, but tunnel vision can lead to expensive mistakes. As you evaluate these fifteen cities, keep a close eye on the total cost of living. Watch out for these three common retirement relocation traps:

- Ignoring Property Taxes: A state that does not collect income tax must generate revenue elsewhere. Texas and New Hampshire rely heavily on property taxes. Before buying a home in San Antonio or El Paso, verify the exact property tax rate for your target neighborhood, and ask the county assessor about homestead exemptions for residents over age 65.

- Underestimating Homeowners Insurance: Real estate prices in Florida might look appealing, but the state is currently facing a massive insurance crisis. Premiums for homeowners and flood insurance have skyrocketed. Always get an insurance quote for a property before making an offer; a cheap house is not a bargain if the insurance costs $6,000 a year.

- Overlooking Healthcare Networks: If you use a Medicare Advantage plan, your coverage is highly regional. Moving across state lines means you will almost certainly need to enroll in a new plan, and your preferred doctors may not be in-network at your new location. Always check the availability of top-rated hospitals and specialists before committing to a rural area like Pahrump or Casper.

“When you are on a fixed income, predictability is your best friend. Choosing a location with lower fixed costs—like housing and taxes—gives you the breathing room to actually enjoy your retirement.” — Jean Chatzky, Personal Finance Expert

Getting Expert Help

Uprooting your life to move across the country is a massive logistical and financial undertaking. To ensure your tax strategy holds water, consult with professionals who understand both your current and future home states.

Consider hiring a Certified Public Accountant (CPA) to help you properly establish legal domicile in your new state. Simply buying a house in Florida does not mean your former high-tax state will stop trying to tax you—you must change your driver’s license, voter registration, and banking details to prove your move is permanent.

Additionally, work with an independent, licensed Medicare broker. Because you are moving out of your current plan’s service area, you will trigger a Special Enrollment Period. A broker can help you seamlessly transition your health coverage so you do not experience a gap in care.

By pairing zero state income taxes with an affordable median home price, you set yourself up for a financially secure retirement. Whether you choose the warm shores of the Gulf Coast, the quiet lakes of Tennessee, or the wide-open spaces of the West, keeping more of your own money gives you the freedom to retire on your own terms.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA. Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources like SSA.gov and Medicare.gov.