Deciding how to take your pension is one of the most critical financial choices you face, and understanding your benefit’s true value in 2026 is the first step. With recent shifts in IRS segment rates and new tax brackets taking effect, the math behind your pension has changed. If your employer offers a choice between a lifetime monthly annuity and a single lump sum, you need to know exactly how much that income stream is worth in today’s dollars. A miscalculation could leave you facing an unexpected tax bill or falling short of your retirement goals. By learning how to calculate your pension’s present value, you can confidently secure the reliable income you earned and protect your financial future.

Why Your Pension’s Present Value Matters in 2026

Understanding the present value of your pension gives you a clear baseline for your retirement planning. Present value is a mathematical calculation that determines what a future stream of payments is worth today. If your company owes you $1,500 a month for the rest of your life, that future income has a specific, calculable dollar value right now. Employers use complex actuarial formulas, mortality tables, and prevailing interest rates to translate decades of monthly checks into a single lump-sum figure.

Knowing this number empowers you to make an apples-to-apples comparison between your pension and other retirement assets like your 401(k) or traditional IRA. It also helps you assess whether taking a corporate buyout offer makes mathematical sense. If your employer offers you a $250,000 lump sum, you must determine whether you could invest that money yourself and safely generate more than your guaranteed monthly payout over a twenty- or thirty-year retirement.

How IRS Segment Rates Impact Your Lump-Sum Offer

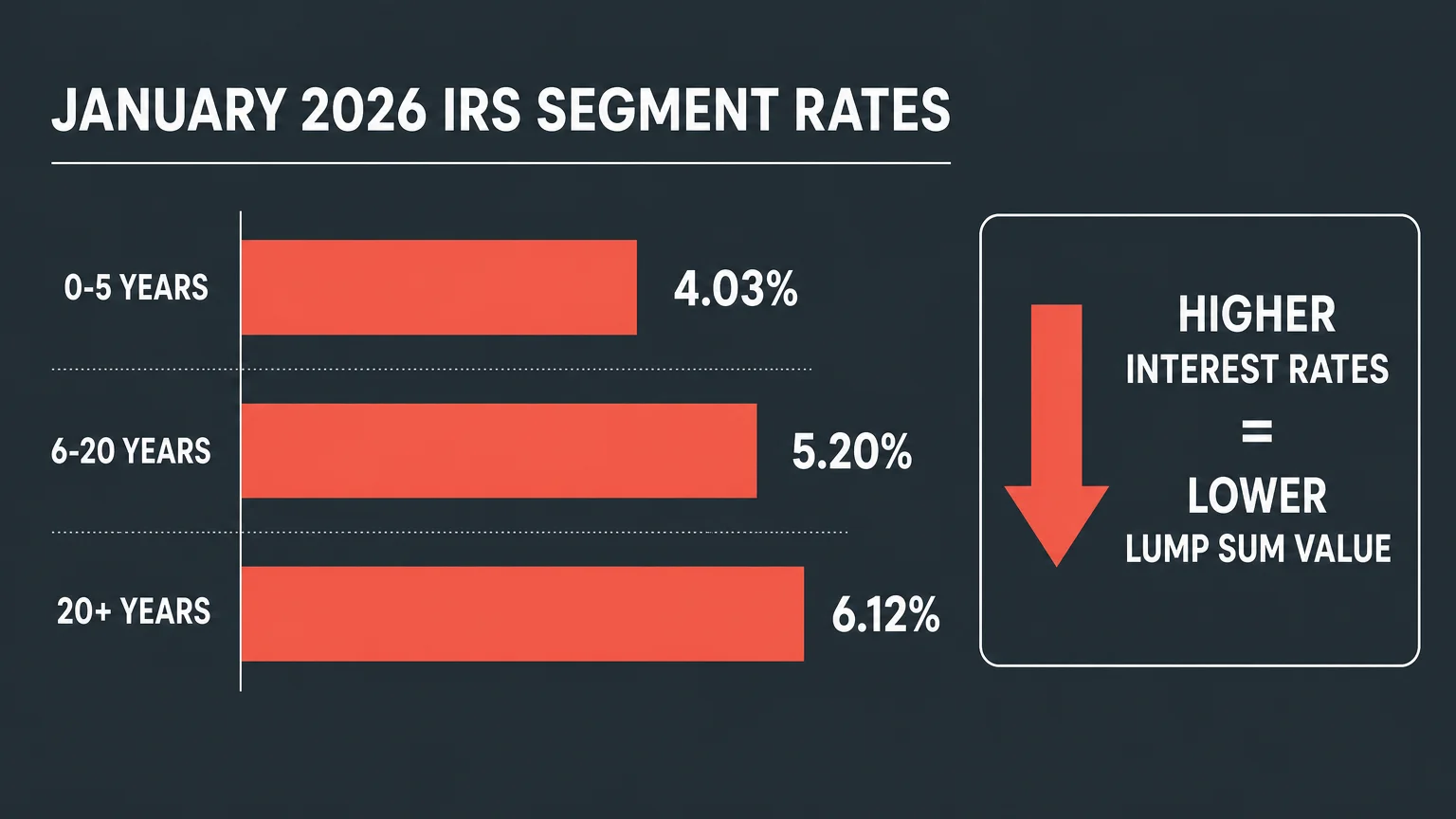

When an employer calculates the lump-sum value of your pension, they do not simply guess how much money you need. They are legally required to use specific interest rates published by the Internal Revenue Service, known as IRS segment rates. These rates are based on corporate bond yields and are divided into three time horizons: the first segment covers the initial five years of retirement, the second covers years six through twenty, and the third covers years beyond twenty.

The most critical concept to understand here is the inverse relationship between interest rates and your lump-sum value. When interest rates rise, the present value of your pension decreases. When rates fall, your lump-sum value increases.

For January 2026, the IRS set the spot segment rates at 4.03% for the first segment, 5.20% for the second segment, and 6.12% for the third segment. Because these rates are substantially higher than the rock-bottom rates seen a few years ago, lump-sum offers today are generally lower than they were in the early 2020s. A shift of just one percent in these segment rates can change your lump-sum payout by tens of thousands of dollars. Always check the specific month your plan uses to calculate your benefit, as the timing of your retirement date can dramatically impact the final number deposited into your account.

Annuity vs. Lump Sum: Weighing Your 2026 Options

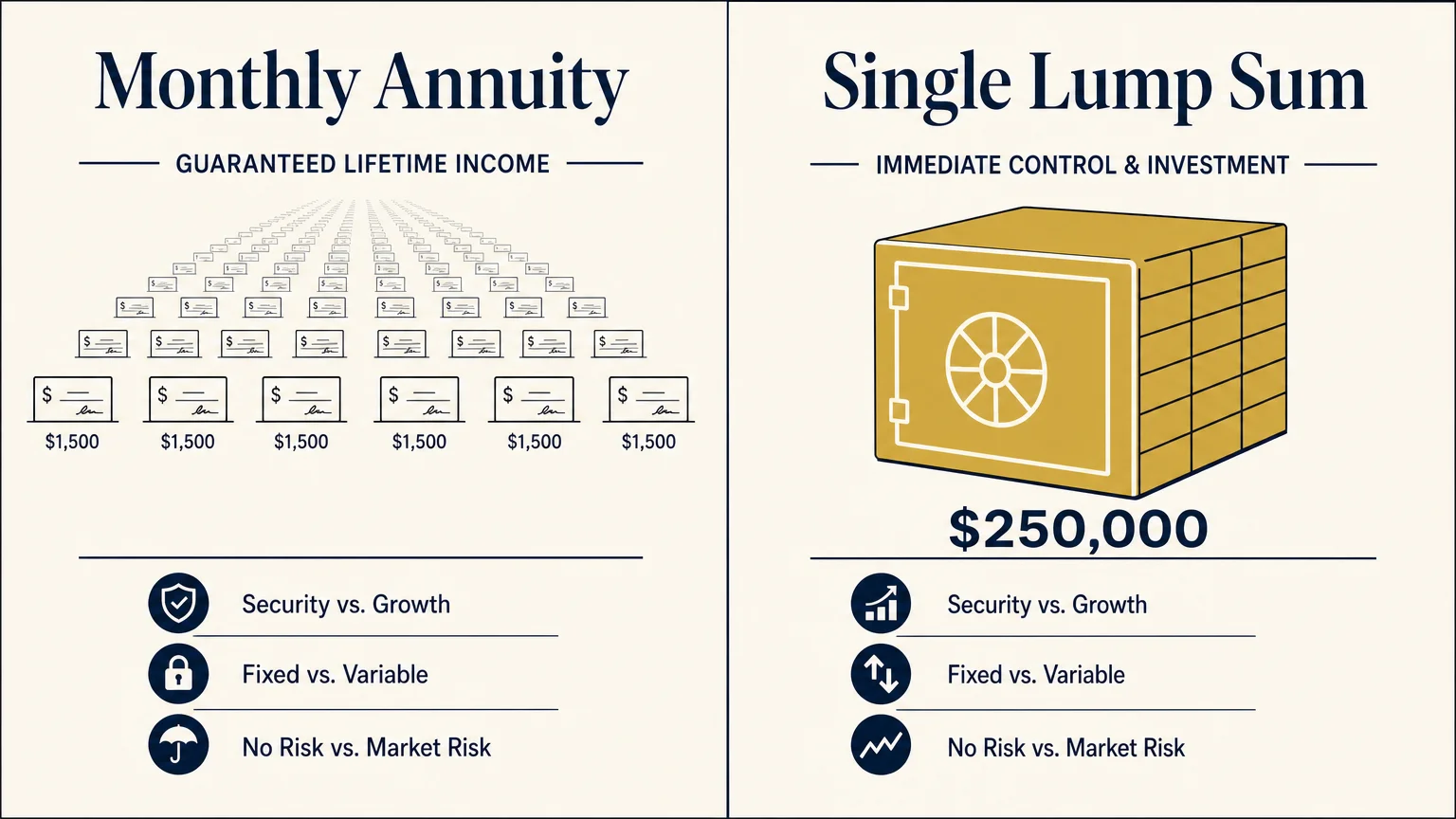

You essentially have two paths when claiming your pension: accepting a lifetime monthly payment or walking away with a single pile of cash. Each choice carries unique benefits and risks.

| Feature | Monthly Annuity | Single Lump Sum |

|---|---|---|

| Income Security | Guaranteed payments for life, regardless of market conditions. | Income depends entirely on your investment performance and withdrawal strategy. |

| Inflation Protection | Typically fixed; loses purchasing power over time without a COLA. | Offers the potential to grow and outpace inflation if invested prudently. |

| Legacy and Heirs | Payments usually stop when you (or your designated spouse) pass away. | The remaining balance can be passed down to your children or beneficiaries. |

A monthly annuity provides deep peace of mind. You receive a fixed check every month, regardless of stock market crashes or economic downturns. However, most private corporate pensions do not offer a cost-of-living adjustment. For context, the Social Security Administration announced a 2.8% cost-of-living adjustment for 2026. If your pension is a flat $1,800 a month, inflation will quietly erode your purchasing power over time, meaning that $1,800 will buy significantly less at age 85 than it did at age 65.

A lump sum gives you total control. You can roll the funds into an IRA, manage your own investments, and potentially grow your balance to outpace inflation. You can also leave whatever remains to your heirs. The trade-off is carrying the full weight of investment risk. If your portfolio underperforms, you bear the sole responsibility of stretching those dollars across your lifespan.

PBGC Protections and Your Pension Safety Net

Many seniors worry about their former employer going bankrupt and taking their pension down with it. The Pension Benefit Guaranty Corporation (PBGC) serves as a vital federal safety net for defined benefit plans. If your employer fails and the pension plan cannot meet its obligations, the PBGC steps in to pay your benefits up to certain legal limits.

This insurance program is funded by premiums paid by plan sponsors. For 2026, the PBGC flat-rate premium for single-employer plans increased to $111 per participant. While this safety net provides significant reassurance, it has a strict cap. The PBGC sets a maximum monthly guarantee based on your age when you begin taking benefits.

If you earned a massive executive pension over a long career, the PBGC maximum might not cover your entire promised benefit. Those with exceptionally large pensions sometimes opt for a lump-sum payout specifically to eliminate the risk of their employer defaulting and their benefit being cut down to the PBGC maximum limit. You should always verify current guarantee levels for your specific age and plan type directly through official PBGC resources.

Tax Implications of Your Pension Payout

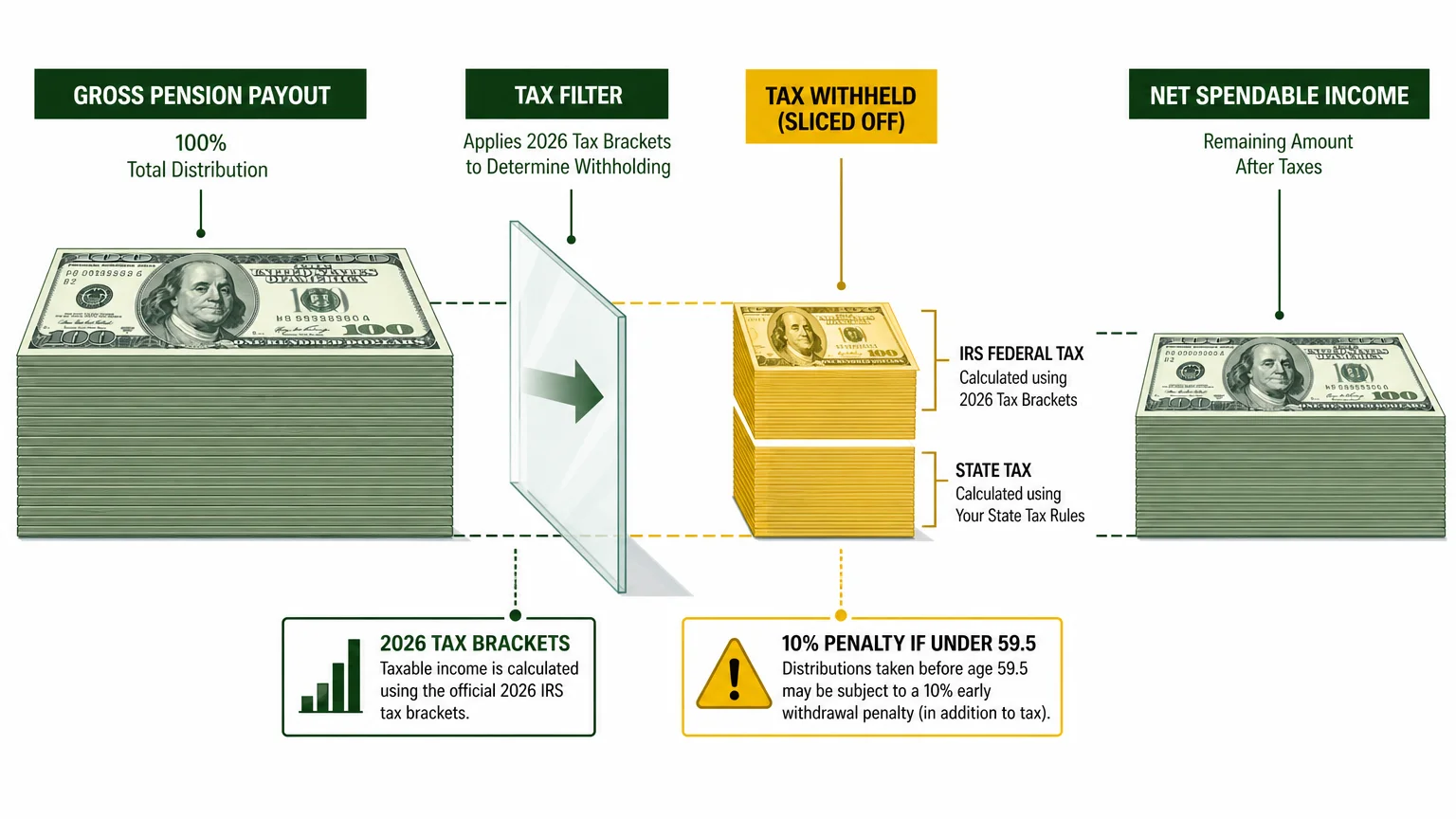

Your pension is likely funded with pre-tax dollars, meaning the IRS is waiting for its share. How you choose to receive your pension dictates exactly when and how much you will pay in taxes.

“As much as 70 percent of your hard-earned retirement funds can be eaten up by income, estate and state taxes.” — Ed Slott, CPA and IRA Expert

If you take a monthly annuity, those payments are treated as ordinary income. You simply pay taxes on the money as you receive it each year, smoothing out your tax liability over decades. However, if you choose a lump sum, the tax traps become significantly more dangerous.

If you request a lump-sum check payable directly to you, your employer is required by law to withhold 20% for federal taxes. Furthermore, the entire distribution amount becomes fully taxable in that single year. For perspective, the standard deduction for married couples filing jointly in 2026 is $32,200. Dropping a $400,000 lump sum on top of your other income will likely push you into the highest federal tax brackets—which peak at 37% for 2026.

To avoid this massive tax penalty, you must execute a “direct rollover.” By having your employer transfer the funds directly into a traditional IRA, you maintain the tax-deferred status of your money and bypass the mandatory 20% withholding entirely. You will only pay taxes when you eventually withdraw the money from your IRA during retirement.

Pitfalls to Watch For

Pension decisions are generally irreversible. Avoiding common missteps can save you from decades of financial regret. Keep a close eye on these frequent pitfalls:

- Misunderstanding Survivor Benefits: Taking a single-life annuity gives you the highest monthly payout, but the payments stop completely when you die. This leaves your surviving spouse with zero pension income. Always review joint-and-survivor options before signing your final paperwork to ensure your partner is protected.

- Underestimating Healthcare Costs: A lump sum might look like an endless fortune, but a single medical emergency or the need for long-term care can deplete an investment portfolio rapidly. Guaranteed monthly income can help stabilize your cash flow during an unpredictable health crisis.

- Ignoring the Timing of Your Retirement Date: Because pension plans update their IRS segment rates at different times of the year, retiring in December versus January could result in a drastically different lump-sum calculation. Ask your plan administrator exactly when they update their rates and run estimates for both sides of that date to maximize your payout.

Getting Expert Help

Navigating the complexities of actuarial math, tax brackets, and investment risk is challenging. It is highly recommended to seek professional guidance from a fee-only fiduciary financial advisor or a CPA in the following scenarios:

- You are offered a limited-time buyout window: Employers often pressure employees to take a lump sum during corporate restructuring. A fiduciary advisor can evaluate whether the offer is mathematically fair or if you are better off keeping the guaranteed annuity.

- You need to coordinate with Social Security: Maximizing your household income requires aligning your pension start date with your optimal Social Security claiming strategy. An expert can run the software necessary to find your break-even point.

- You are unsure about your investment ability: If managing a large lump sum feels overwhelming, an expert can build a diversified income portfolio that aligns with FINRA investor guidelines and your personal risk tolerance.

Next Steps for Your Pension Strategy

Review your latest pension statement and request both the lump-sum and annuity projections from your plan administrator. Use these figures to build a comprehensive retirement income plan that factors in your monthly living expenses, current tax bracket, and long-term goals. Taking control of your pension strategy today ensures your hard work translates into the comfortable, secure future you deserve.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.