Protecting your Social Security benefits requires knowing exactly how taxes, earnings, and Medicare premiums interact with your monthly checks. Every year, retirees unknowingly trigger rules that reduce their net payouts, leaving vital money behind. A poorly timed retirement withdrawal, a part-time job before full retirement age, or a sudden spike in taxable income can instantly shrink the amount deposited into your bank account. The system holds hidden traps, but you can sidestep them with strategic planning. By understanding current earnings limits, tax thresholds, and Medicare surcharges, you can keep more of your hard-earned benefits and secure your retirement income.

1. Working While Collecting Before Full Retirement Age

Many seniors assume they can claim Social Security early and continue working part-time without any consequences. However, the Social Security Administration (SSA) enforces strict earning limits for anyone who collects benefits before reaching their Full Retirement Age (FRA).

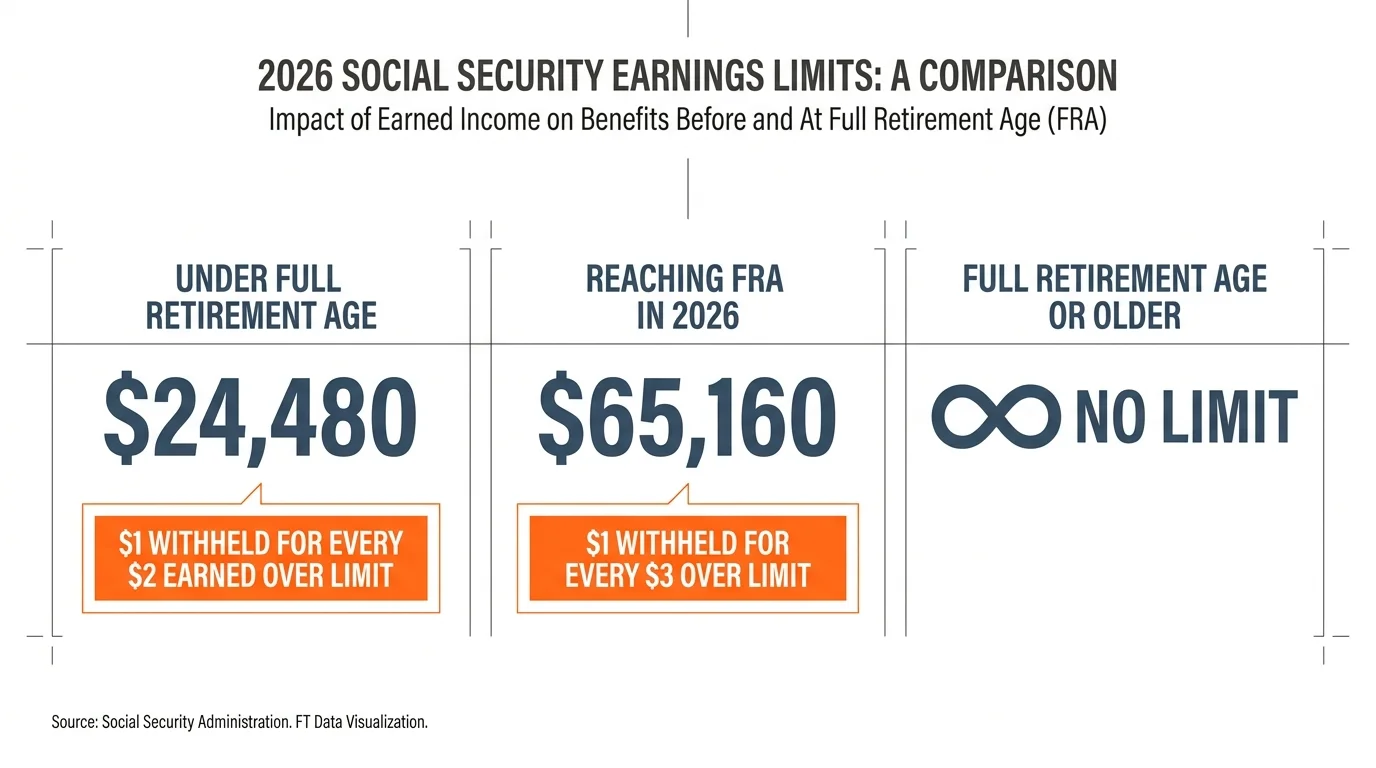

In 2026, if you are under your FRA for the entire year, the earnings limit is $24,480. For every $2 you earn above this threshold, the SSA withholds $1 from your benefit payments. If you reach your Full Retirement Age in 2026, the limit jumps to $65,160, and the SSA only withholds $1 for every $3 you earn over the limit—and they only count earnings from the months prior to your birthday. Once you hit your Full Retirement Age, the earning limits disappear entirely, allowing you to earn unlimited income without any penalty to your monthly check.

Imagine you are 64 years old in 2026 and you take a consulting job that pays $34,480 for the year. Because your earnings exceed the $24,480 limit by $10,000, the SSA will withhold $5,000 from your benefits over the course of the year. This sudden reduction catches many working seniors completely off guard.

| Your Age Status in 2026 | 2026 Earnings Limit | Withholding Penalty |

|---|---|---|

| Under Full Retirement Age all year | $24,480 | $1 withheld for every $2 earned over limit |

| Reaching Full Retirement Age in 2026 | $65,160 | $1 withheld for every $3 earned over limit |

| Full Retirement Age or older | No Limit | No benefits withheld |

Actionable Insight: Withheld benefits do not vanish forever. The SSA recalculates your payout once you reach Full Retirement Age to give you credit for those withheld months. However, if you rely on that monthly cash flow now, carefully track your wages and communicate with the SSA to adjust your payments proactively. If you plan to continue working significantly, it often makes more financial sense to delay claiming your benefits until you stop working or reach FRA.

Wait, “lurks” is 1 word.

Let’s try:

“A tax torpedo covered in IRS forms lurks beneath a paper boat labeled Social Security.”

15 words

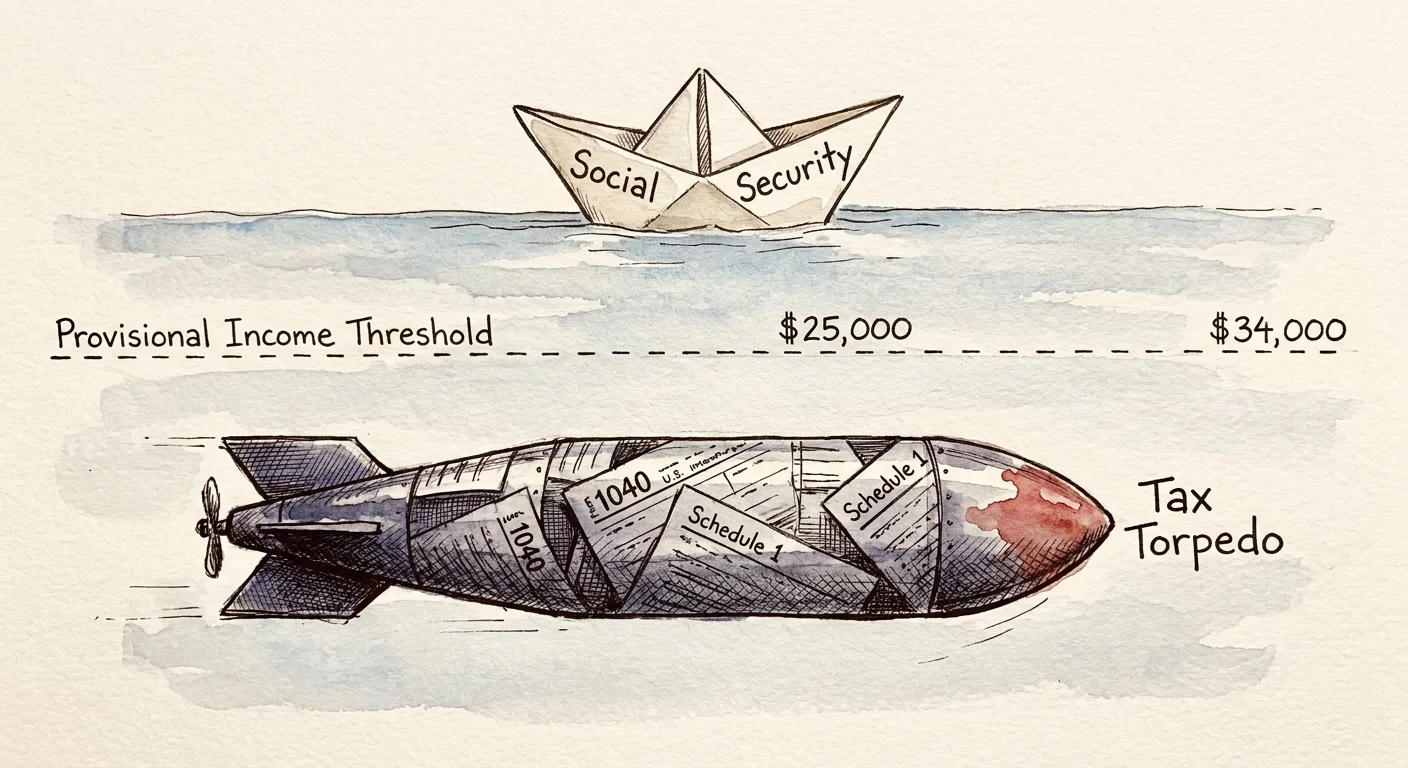

2. Triggering the “Tax Torpedo” with Retirement Withdrawals

A massive misconception among retirees is that Social Security income is entirely tax-free. In reality, up to 85% of your benefits become taxable if your income crosses specific thresholds set by the Internal Revenue Service (IRS).

The IRS uses a unique formula called “Provisional Income” to determine how much of your Social Security is subject to federal income tax. You calculate your Provisional Income by adding your Adjusted Gross Income (AGI), any nontaxable interest you earn, and exactly 50% of your annual Social Security benefits.

Because the IRS established these brackets in the 1980s and never indexed them for inflation, they trap more middle-class seniors every single year:

- Single Filers: A Provisional Income between $25,000 and $34,000 makes up to 50% of your benefits taxable. Above $34,000, up to 85% becomes taxable.

- Married Filing Jointly: A Provisional Income between $32,000 and $44,000 makes up to 50% of your benefits taxable. Above $44,000, up to 85% becomes taxable.

Seniors frequently trigger this “tax torpedo” by taking large, unplanned withdrawals from traditional 401(k)s or IRAs. Because traditional retirement withdrawals count toward your Adjusted Gross Income, a sudden $20,000 withdrawal to buy a new car can push your Provisional Income over the limit, suddenly subjecting your Social Security benefits to heavy taxation.

Actionable Insight: To protect your benefits from federal taxation, diversify your retirement income streams. Pulling from a Roth IRA or drawing down cash from a standard savings account does not increase your Adjusted Gross Income. By strategically balancing taxable and tax-free withdrawals, you can keep your Provisional Income below the IRS thresholds.

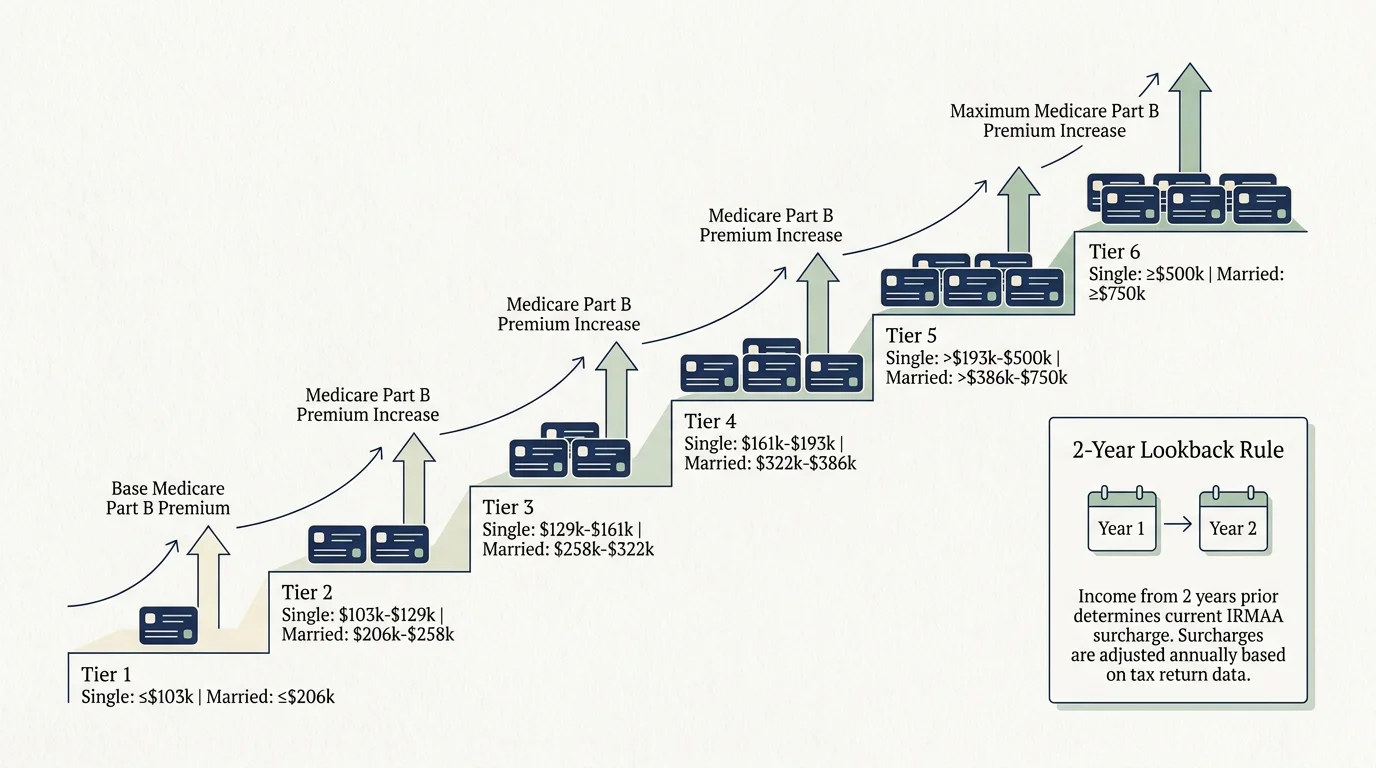

3. Getting Hit by Hidden Medicare Surcharges (IRMAA)

Your Social Security and Medicare benefits are permanently linked. For most seniors, Medicare Part B premiums are deducted directly from their Social Security checks before the money ever hits their bank account. When Medicare premiums rise, your net Social Security income shrinks.

In 2026, the standard Medicare Part B premium sits at $202.90 per month, alongside a $283 annual deductible. However, if you report a high income, Medicare slaps an extra surcharge onto your premium known as the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge stealthily erodes your Social Security payout.

IRMAA operates on a strict two-year lookback period. The official Medicare program determines your 2026 premiums based on the Modified Adjusted Gross Income (MAGI) you reported on your 2024 tax return. For 2026, IRMAA surcharges trigger if your MAGI exceeds $109,000 as a single filer or $218,000 as a married couple filing jointly.

If you sold a rental property, executed a massive Roth conversion, or cashed out a large stock position two years ago, you might suddenly see your Social Security check drop by hundreds of dollars a month as Medicare forces you to pay the elevated Part B premiums.

“Most people think their retirement planning is done once they stop working, but the tax planning has just begun. Pay taxes now at historically low rates so you can avoid paying more later.” — Ed Slott, CPA and Retirement Tax Expert

Actionable Insight: If your income spiked two years ago due to an isolated event—like selling a home or receiving severance pay—but your income has since dropped, you do not simply have to accept the penalty. You can file Form SSA-44 to request an IRMAA reduction due to a “Life-Changing Event,” such as retirement, divorce, or the death of a spouse. Successfully appealing this surcharge will immediately increase your net Social Security check.

4. Misjudging the Impact of Required Minimum Distributions (RMDs)

The government eventually forces you to take money out of your tax-deferred retirement accounts. These mandatory withdrawals are called Required Minimum Distributions (RMDs). Depending on your birth year, you must begin taking RMDs at age 73 (if born between 1951 and 1959) or age 75 (if born in 1960 or later).

When RMDs kick in, they create a brutal domino effect on your finances. You are forced to withdraw taxable income, which instantly drives up your Adjusted Gross Income. This higher AGI simultaneously triggers the Social Security Tax Torpedo and pushes you into higher Medicare IRMAA brackets. Suddenly, a mandatory $40,000 IRA withdrawal results in thousands of dollars in lost Social Security income through increased taxes and Medicare deductions.

Many retirees spend their 60s avoiding traditional IRA withdrawals to keep their taxes low, only to face massive RMDs in their 70s because their account balances grew so large.

Actionable Insight: Start managing your tax-deferred balances early. Consider executing systematic Roth conversions during your late 50s and 60s when you fall into lower tax brackets. Alternatively, if you are charitably inclined, utilize Qualified Charitable Distributions (QCDs) once you turn 70 and a half. A QCD allows you to transfer funds directly from your IRA to an eligible charity, satisfying your RMD requirement without adding a single dollar to your Adjusted Gross Income.

5. Claiming Early Without Maximizing Survivor Benefits

Choosing when to claim Social Security represents one of the most consequential financial decisions you will ever make. You can claim as early as age 62, but doing so permanently reduces your monthly check by up to 30% compared to waiting for your Full Retirement Age. Delaying past FRA earns you delayed retirement credits, increasing your benefit by 8% per year up to age 70.

While taking a smaller check early might make sense for a single individual with health issues, it often wreaks havoc on married couples. When one spouse passes away, the surviving spouse inherits the larger of the two Social Security checks, and the smaller check disappears entirely.

If the higher-earning spouse claims their benefit at age 62, they permanently lock in a dramatically lower payout. When they pass away, they leave their surviving widow or widower with a permanently shrunken survivor benefit, often struggling to cover rising household costs with only one reduced income stream.

Actionable Insight: Coordinate claiming strategies with your spouse. The highest earner should try to delay claiming their benefit until age 70 whenever possible. This strategy guarantees the maximum possible monthly payout for the household while both are alive, and it locks in the absolute highest survivor benefit for the remaining spouse later in life.

Common Mistakes to Avoid

Even the most careful planners can stumble when navigating the complex web of federal retirement programs. The National Council on Aging (NCOA) and financial experts routinely highlight the following errors seniors make that unintentionally reduce their net income:

- Ignoring State Taxes: While we focus heavily on federal rules, a handful of states still levy state income taxes on Social Security benefits. Depending on your state of residence, your check might face additional reductions. Always verify current tax regulations with your state department of revenue.

- Forgetting that Medicare Outpaces COLA: The SSA adjusts benefits annually using a Cost-of-Living Adjustment (COLA). For example, the 2026 COLA projection sits around 2.8%. However, Medicare Part B premiums routinely rise at a much faster rate—jumping nearly 10% to $202.90 in 2026. This dynamic means your actual net raise is often much smaller than the headline COLA percentage suggests.

- Setting and Forgetting Withholdings: If you elect to have federal taxes voluntarily withheld from your Social Security checks, you must revisit this percentage annually. Major life changes, paying off a mortgage, or turning 73 and starting RMDs dramatically change your tax picture. Keeping an outdated withholding rate means you might be sending the IRS too much of your monthly income unnecessarily.

Finding the Right Advisor

Managing the intersection of Social Security, Medicare, and taxation requires precision. You do not have to tackle this complex puzzle alone. Consider consulting a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) if you fall into any of these specific scenarios:

- You are planning Roth conversions: An advisor can project your future tax brackets and calculate exactly how much you can convert today without inadvertently triggering an IRMAA surcharge or maxing out the Social Security tax torpedo.

- You recently retired and received an IRMAA letter: A professional can help you navigate the SSA-44 appeals process, ensuring you properly document your life-changing event to eliminate the heavy Medicare penalty.

- You have a significant age or income gap with your spouse: Dual-income couples with varying ages need advanced break-even analysis to determine the absolute best months for each spouse to file for benefits, maximizing both spousal and survivor payouts.

Frequently Asked Questions

Are my Social Security benefits permanently lost if I earn over the limit?

No. If the SSA withholds money because you exceeded the earnings limit before your Full Retirement Age, those funds are not gone forever. Once you reach FRA, the SSA will recalculate your monthly benefit amount to account for the months they withheld payments, resulting in a higher monthly check for the rest of your life.

How can I stop my Social Security from being taxed?

You minimize federal taxation by keeping your Provisional Income low. You achieve this by funding living expenses from tax-free sources like a Roth IRA or standard savings accounts, rather than pulling entirely from traditional, tax-deferred accounts like a 401(k). Proper asset location allows you to manage your Adjusted Gross Income efficiently.

Does a spouse’s income affect my Medicare premium?

Yes. If you are married and file your taxes jointly, Medicare looks at your combined Modified Adjusted Gross Income to determine your IRMAA tier. Even if one spouse has zero income, a large IRA withdrawal or capital gain generated by the other spouse will raise the Medicare Part B premiums for both individuals, directly shrinking both Social Security checks.

Implementing a defensive strategy around your retirement income ensures that you actually get to spend the money you spent decades earning. By actively managing your taxable withdrawals, monitoring your part-time wages before Full Retirement Age, and carefully navigating Medicare thresholds, you take firm control over your financial future. Sit down with your tax documents, map out your upcoming withdrawals, and build a plan that prioritizes keeping your money in your own pocket.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.

Leave a Reply