Millions of older Americans misunderstand how their hard-earned pension fits into a comprehensive retirement strategy. Failing to recognize the intricate rules governing defined benefit plans can lead to thousands of dollars left on the table or unexpected tax bills. Your pension does not operate in a vacuum; it directly interacts with your Social Security benefits, federal tax brackets, and legacy planning.

Whether you are weighing a lump-sum buyout against a monthly annuity, navigating the complexities of the Windfall Elimination Provision, or calculating how the 2026 standard deduction offsets your taxable income, mastering these details is crucial. Securing your financial independence requires making proactive, informed decisions about the benefits you earned over a lifetime of work.

Quick Summary

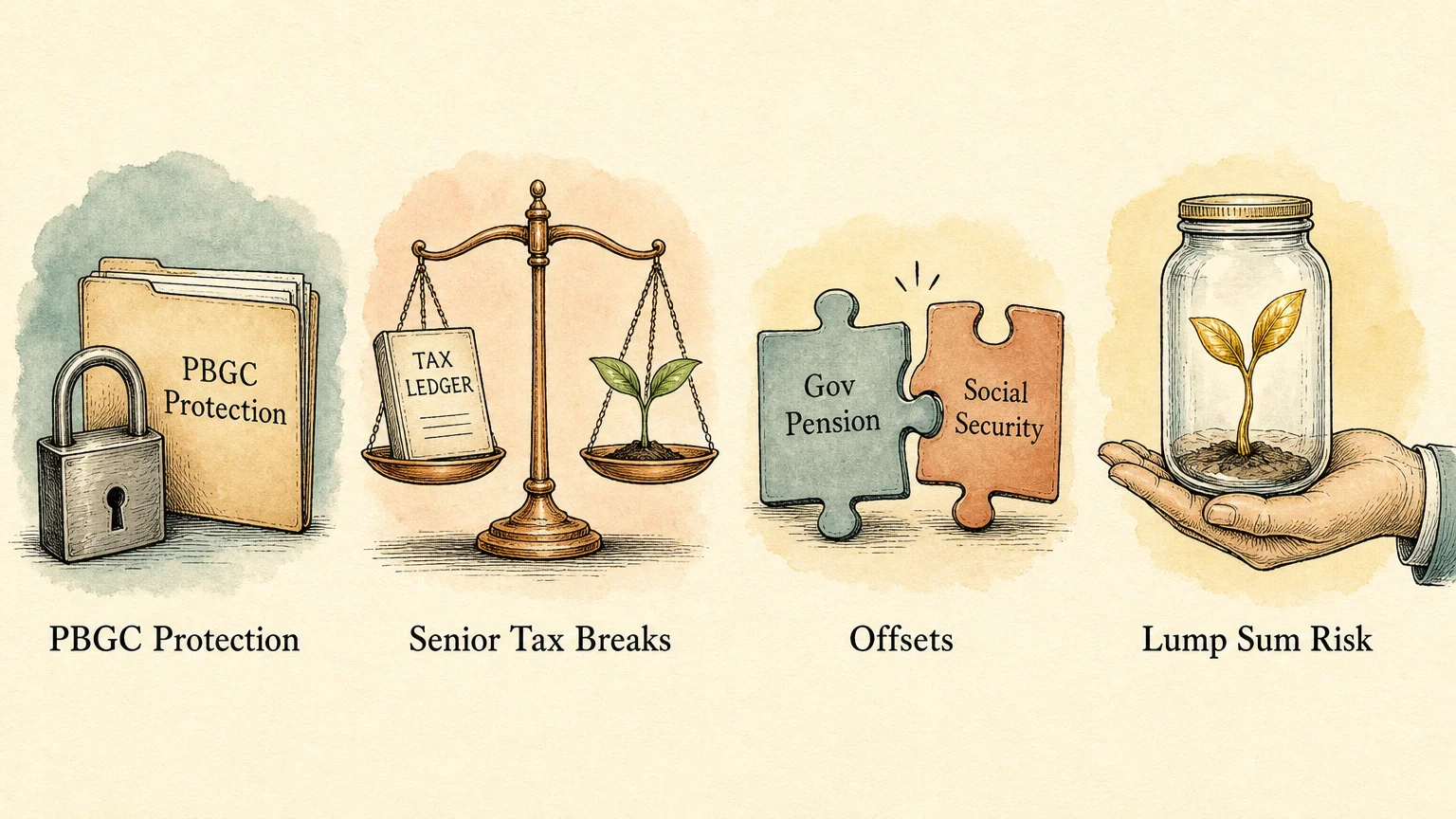

- Federal Protection Has Limits: Private pensions are insured by the PBGC, but monthly payouts are strictly capped based on your age and annuity choice.

- Tax Codes Favor Seniors: New 2026 standard deductions and senior-specific tax breaks can shield a massive portion of your pension income from the IRS.

- Government Jobs Trigger Offsets: Earning a pension from a job that did not withhold Social Security taxes will likely reduce your Social Security benefits.

- Lump Sums Carry Market Risk: Cashing out your pension transfers the burden of investment performance and longevity risk from your former employer directly onto your shoulders.

One Response

Good summary, most of which I knew prior but helpful refreshment. Biggest advantage is state (in this case IA) elimination of taxes on pension and related benefits.