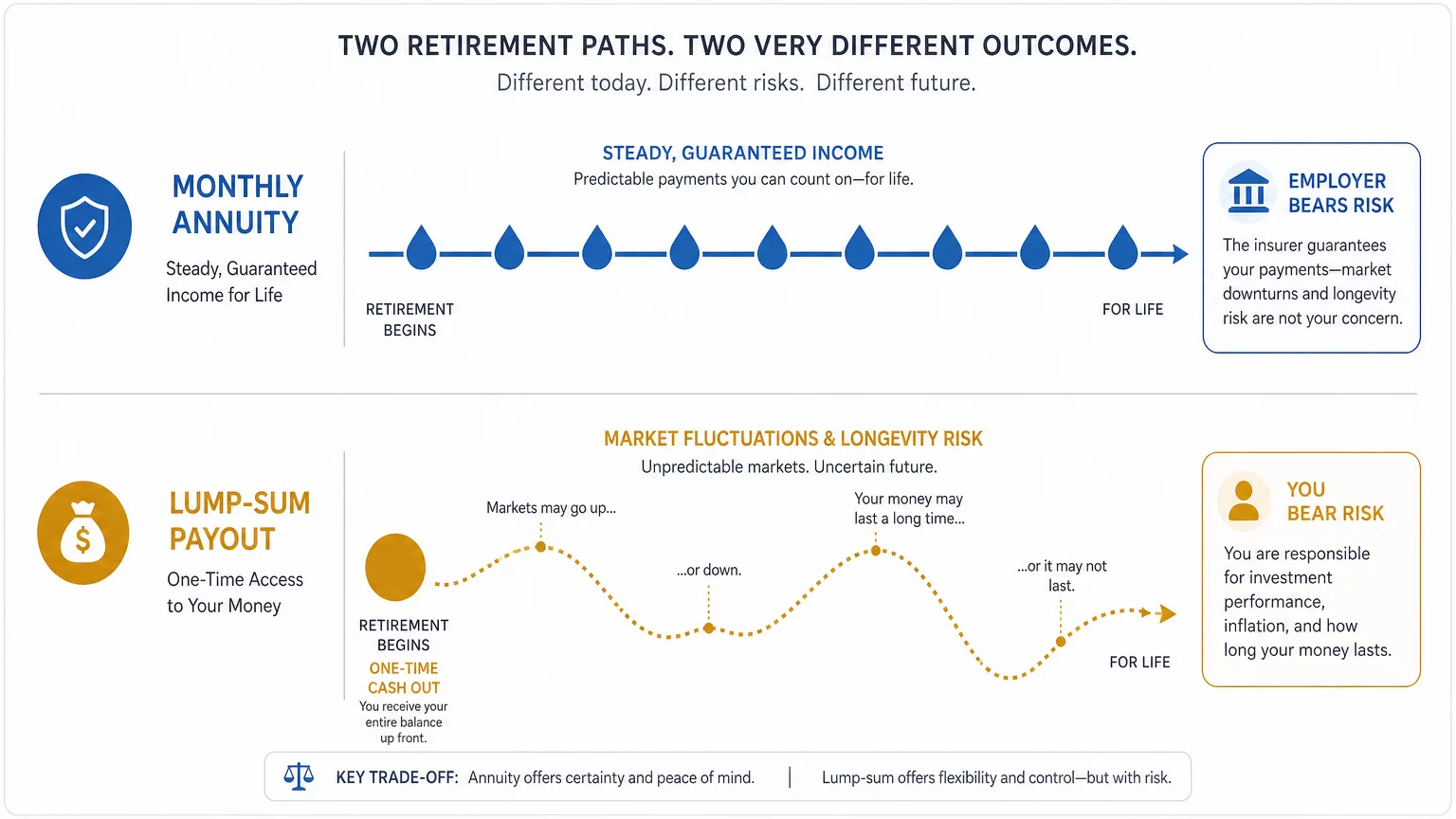

The Critical Decision: Monthly Annuity vs. Lump-Sum Payout

When you retire, many pension plans offer a one-time choice: take a guaranteed monthly payment for the rest of your life, or walk away with a massive lump-sum buyout. This is arguably the most consequential financial decision you will make in retirement.

Taking the monthly annuity provides peace of mind. The employer retains the longevity risk (the risk you live to be 105) and the market risk (the risk the stock market crashes). Conversely, a lump-sum buyout allows you to roll the total value of your pension into a Traditional IRA. This gives you complete control over the investments, offers the flexibility to withdraw large sums for emergencies, and ensures any remaining balance passes to your heirs when you die.

Here is a breakdown of how the two options compare:

| Feature | Monthly Annuity Pension | Lump-Sum Buyout (Rolled to IRA) |

|---|---|---|

| Income Guarantee | Lifelong payments guaranteed by employer/PBGC. | Market-dependent; you could run out of money. |

| Investment Control | None. The employer manages the pension fund. | Total control. You decide how funds are invested. |

| Legacy for Heirs | Limited. Stops when you (or your spouse) pass away. | Full legacy. Remaining balance goes to beneficiaries. |

| Inflation Protection | Typically fixed and loses purchasing power over time. | Potential to outpace inflation if invested aggressively. |

One Response

Good summary, most of which I knew prior but helpful refreshment. Biggest advantage is state (in this case IA) elimination of taxes on pension and related benefits.