The Safety Net You Didn’t Know You Had: The PBGC

If you worked for a private corporation that sponsored a traditional defined benefit pension, you might assume your monthly payout is guaranteed no matter what happens to the company. While your pension is protected, that protection is not infinite. Private-sector pensions are insured by a federal agency called the Pension Benefit Guaranty Corporation (PBGC). If your former employer declares bankruptcy or cannot meet its pension obligations, the PBGC steps in to ensure you still receive a retirement check.

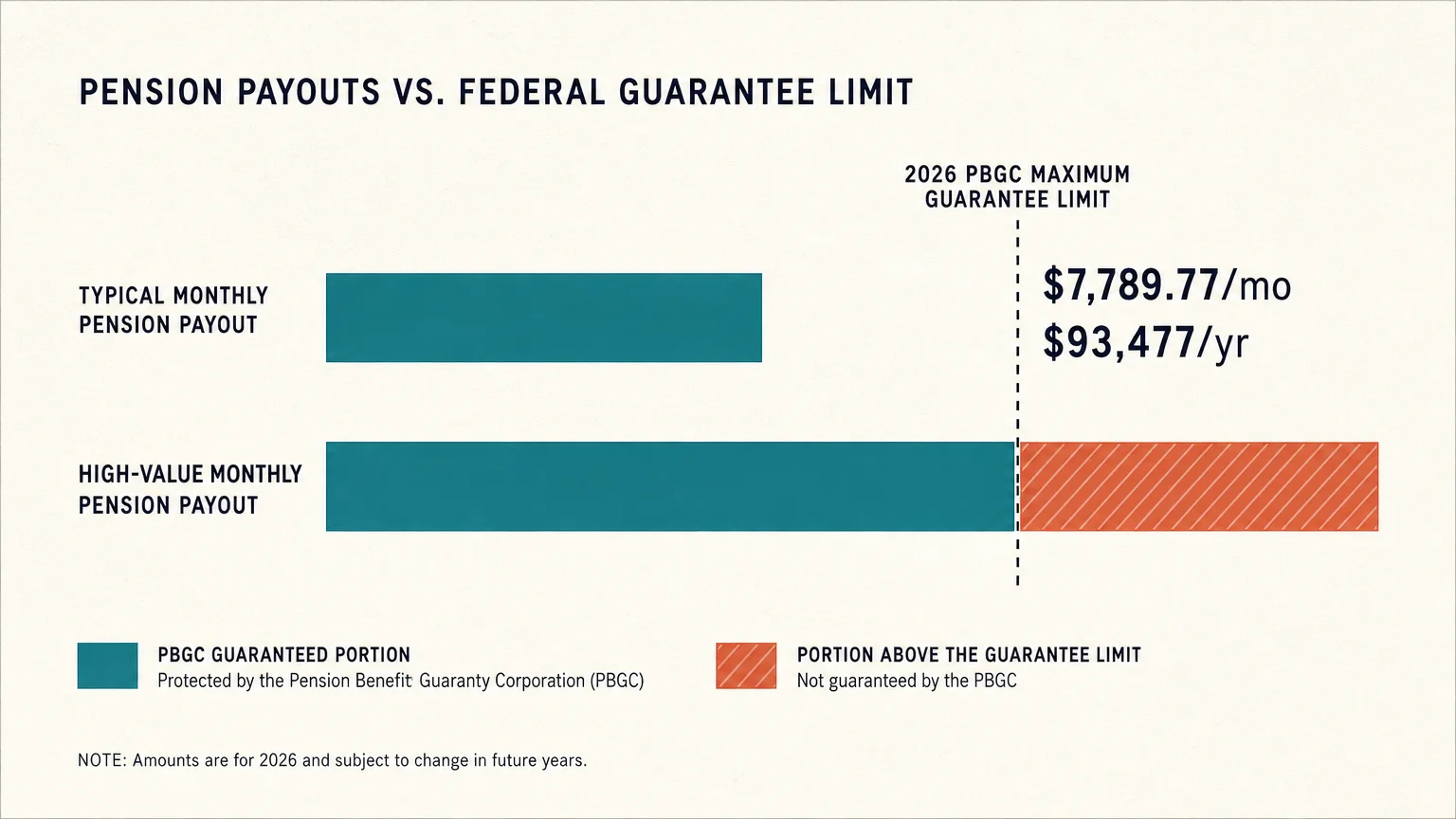

However, the PBGC strictly caps the amount they will pay. For a single-employer plan in 2026, the maximum guaranteed payout for a 65-year-old retiree electing a straight-life annuity is $7,789.77 per month, which translates to roughly $93,477 annually. While this covers the vast majority of middle-class workers, highly compensated employees anticipating six-figure annual pension payouts could see their benefits severely slashed if their employer folds.

Furthermore, this maximum limit fluctuates based on your age and the structure of your payout. If you retire early at age 55, the PBGC ceiling drops significantly because you will be collecting checks for a longer period. Similarly, if you choose a joint-and-survivor annuity to protect your spouse, the PBGC maximum limit is reduced to account for the extended timeline of two lifetimes.

One Response

Good summary, most of which I knew prior but helpful refreshment. Biggest advantage is state (in this case IA) elimination of taxes on pension and related benefits.