Pension Income Versus Your Tax Return

Understanding how the IRS views your pension is critical to managing your cash flow. In almost all cases, pension distributions are taxed as ordinary income at the federal level. Unlike long-term capital gains, which enjoy preferential tax rates, your pension check is taxed at your highest marginal tax bracket.

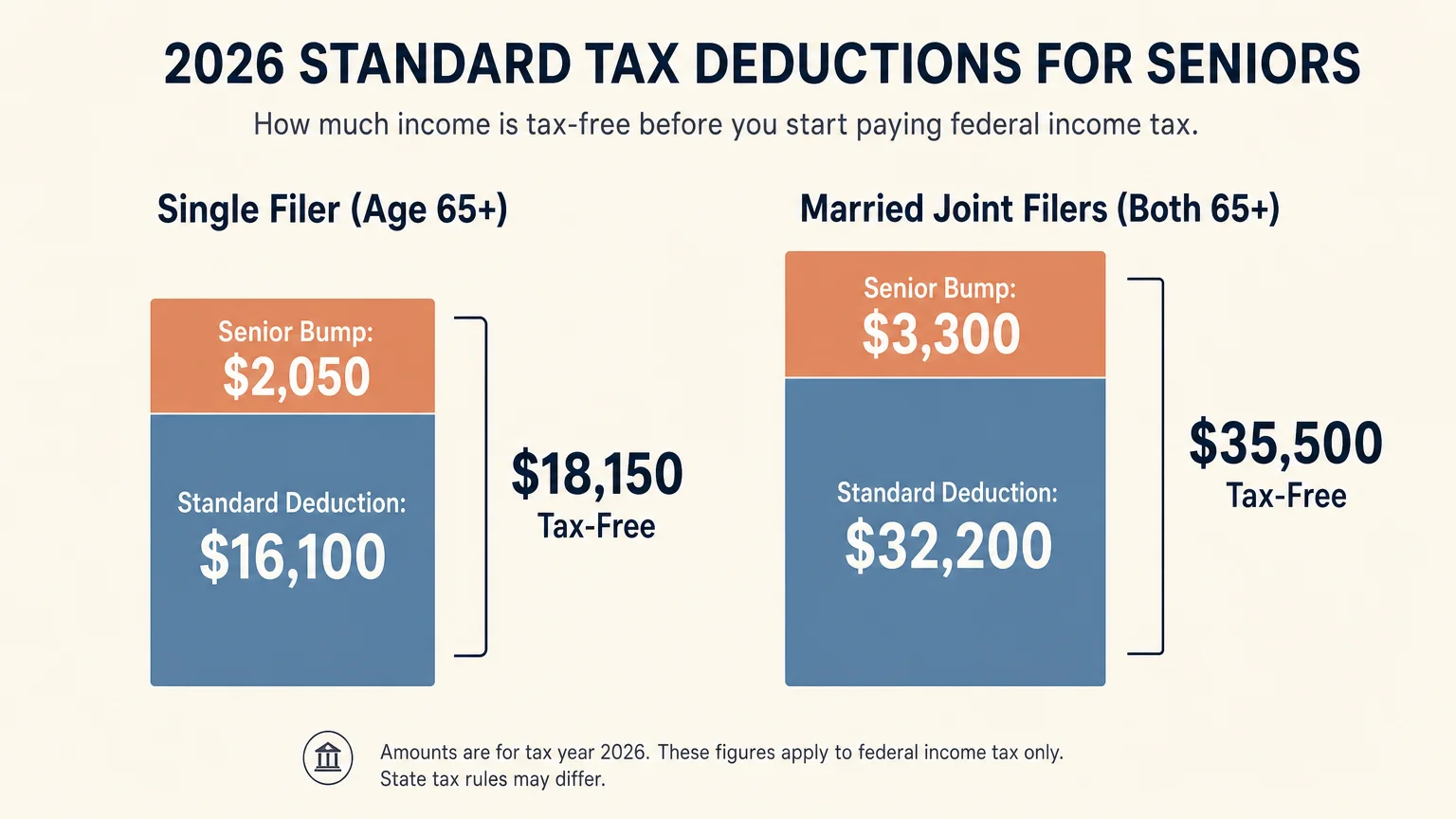

Fortunately, the tax code provides significant buffers for seniors. In 2026, the baseline standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. On top of this, the IRS offers an additional standard deduction for taxpayers aged 65 and older: $2,050 for single filers and $1,650 per qualifying spouse for joint returns.

Recent legislation introduced an even larger shield. Through 2028, taxpayers 65 and older can claim an additional senior deduction of $6,000 per person, provided their adjusted gross income stays below $75,000 for singles or $150,000 for joint returns.

Consider a married couple, both 66 years old, who qualify for these deductions. They could combine the $32,200 base deduction, $3,300 in standard senior add-ons, and $12,000 in the new temporary senior deductions. This effectively shields $47,500 of their income from federal income tax before they pay a single dime to the Internal Revenue Service (IRS).

State taxes, however, are a different story. While states like Florida and Texas have no state income tax, and others fully exempt pension income, several states tax your pension precisely the same way the federal government does. Always verify your state’s specific revenue guidelines.

One Response

Good summary, most of which I knew prior but helpful refreshment. Biggest advantage is state (in this case IA) elimination of taxes on pension and related benefits.