Millions of older Americans misunderstand how their hard-earned pension fits into a comprehensive retirement strategy. Failing to recognize the intricate rules governing defined benefit plans can lead to thousands of dollars left on the table or unexpected tax bills. Your pension does not operate in a vacuum; it directly interacts with your Social Security benefits, federal tax brackets, and legacy planning. Whether you are weighing a lump-sum buyout against a monthly annuity, navigating the complexities of the Windfall Elimination Provision, or calculating how the 2026 standard deduction offsets your taxable income, mastering these details is crucial. Securing your financial independence requires making proactive, informed decisions about the benefits you earned over a lifetime of work.

Quick Summary

- Federal Protection Has Limits: Private pensions are insured by the PBGC, but monthly payouts are strictly capped based on your age and annuity choice.

- Tax Codes Favor Seniors: New 2026 standard deductions and senior-specific tax breaks can shield a massive portion of your pension income from the IRS.

- Government Jobs Trigger Offsets: Earning a pension from a job that did not withhold Social Security taxes will likely reduce your Social Security benefits.

- Lump Sums Carry Market Risk: Cashing out your pension transfers the burden of investment performance and longevity risk from your former employer directly onto your shoulders.

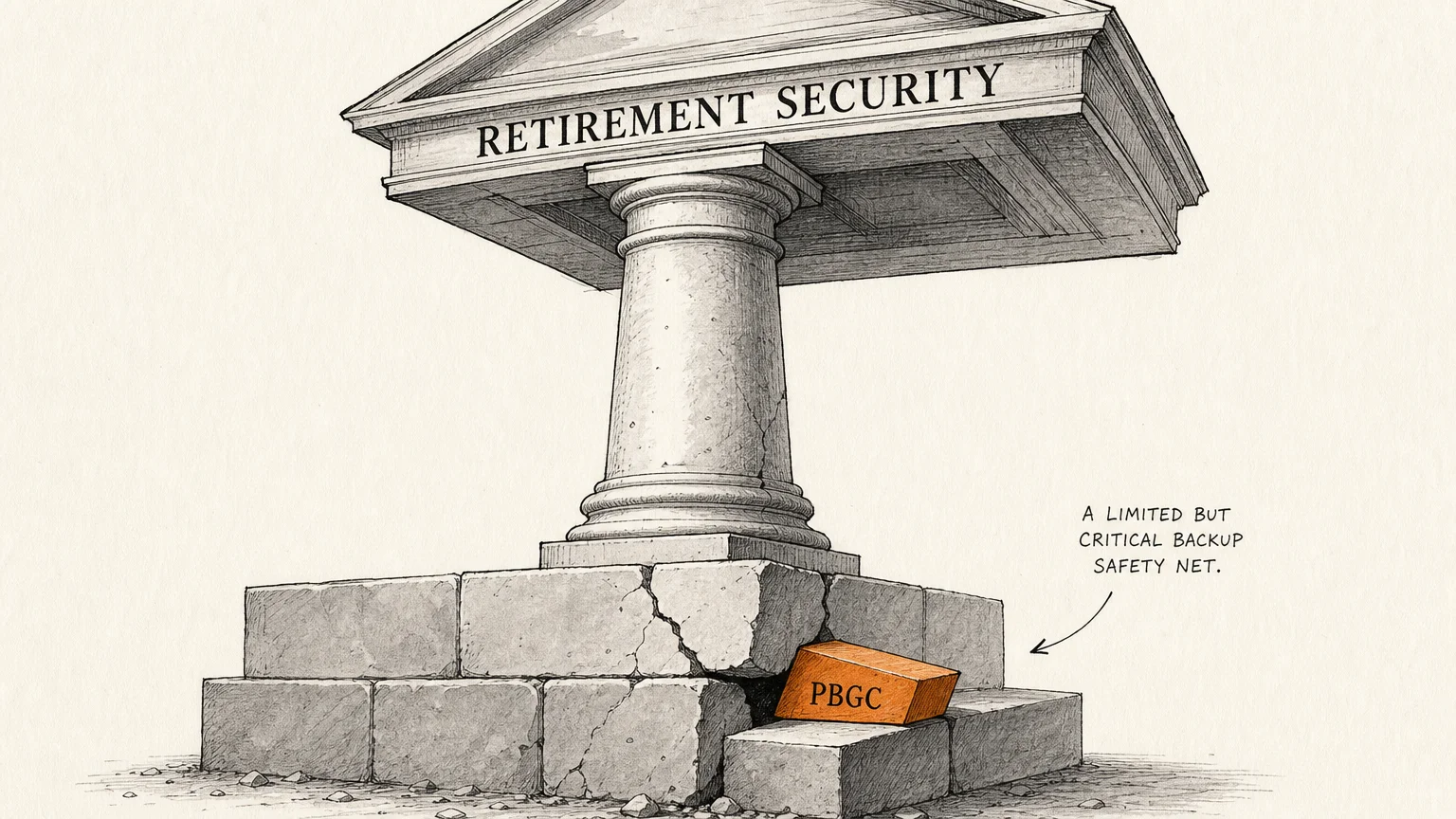

The Safety Net You Didn’t Know You Had: The PBGC

If you worked for a private corporation that sponsored a traditional defined benefit pension, you might assume your monthly payout is guaranteed no matter what happens to the company. While your pension is protected, that protection is not infinite. Private-sector pensions are insured by a federal agency called the Pension Benefit Guaranty Corporation (PBGC). If your former employer declares bankruptcy or cannot meet its pension obligations, the PBGC steps in to ensure you still receive a retirement check.

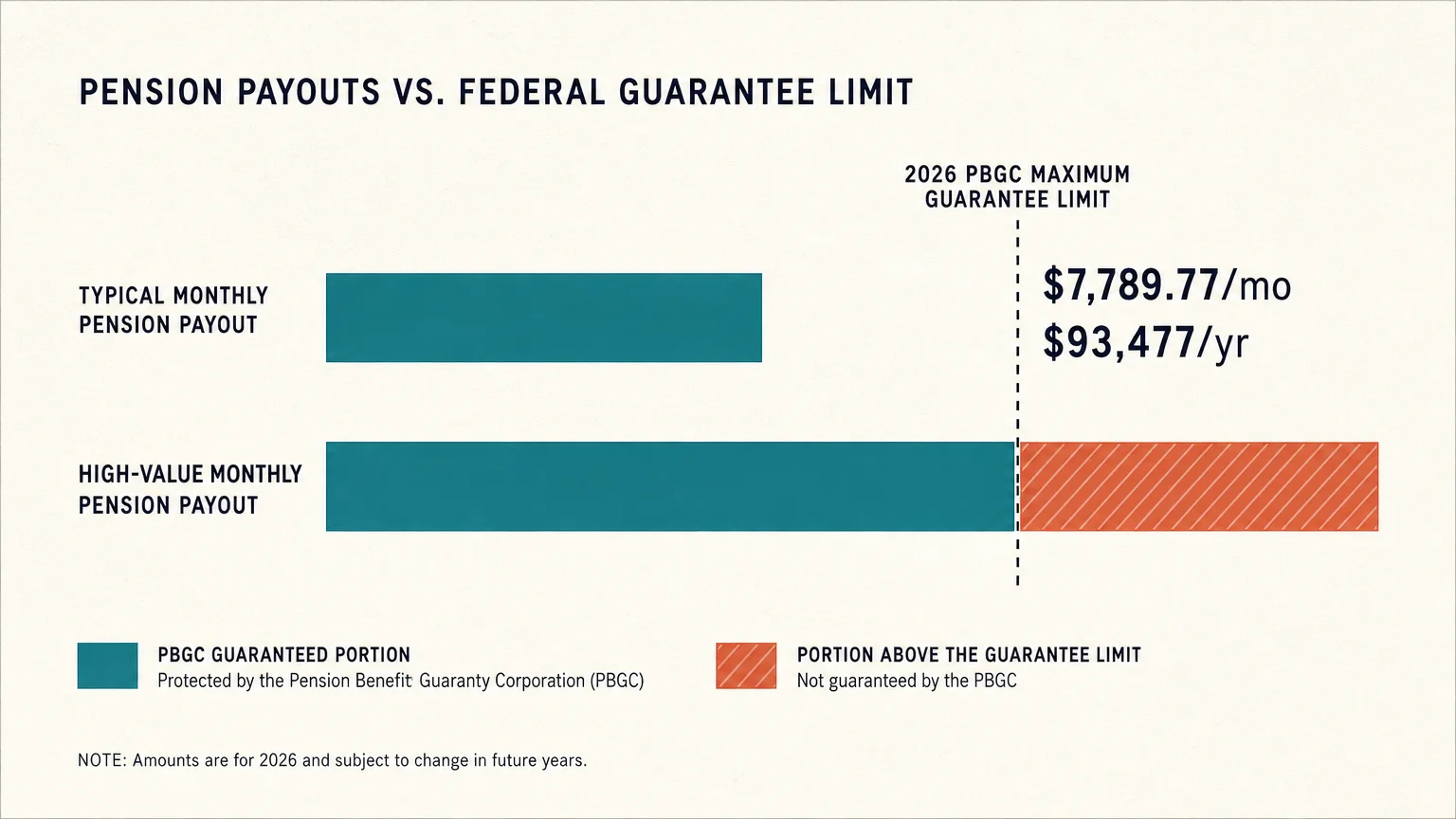

However, the PBGC strictly caps the amount they will pay. For a single-employer plan in 2026, the maximum guaranteed payout for a 65-year-old retiree electing a straight-life annuity is $7,789.77 per month, which translates to roughly $93,477 annually. While this covers the vast majority of middle-class workers, highly compensated employees anticipating six-figure annual pension payouts could see their benefits severely slashed if their employer folds.

Furthermore, this maximum limit fluctuates based on your age and the structure of your payout. If you retire early at age 55, the PBGC ceiling drops significantly because you will be collecting checks for a longer period. Similarly, if you choose a joint-and-survivor annuity to protect your spouse, the PBGC maximum limit is reduced to account for the extended timeline of two lifetimes.

Pension Income Versus Your Tax Return

Understanding how the IRS views your pension is critical to managing your cash flow. In almost all cases, pension distributions are taxed as ordinary income at the federal level. Unlike long-term capital gains, which enjoy preferential tax rates, your pension check is taxed at your highest marginal tax bracket.

“Taxes will be the single biggest expense in retirement. It’s not about what you make; it’s about what you keep.” — Ed Slott, CPA and Retirement Expert

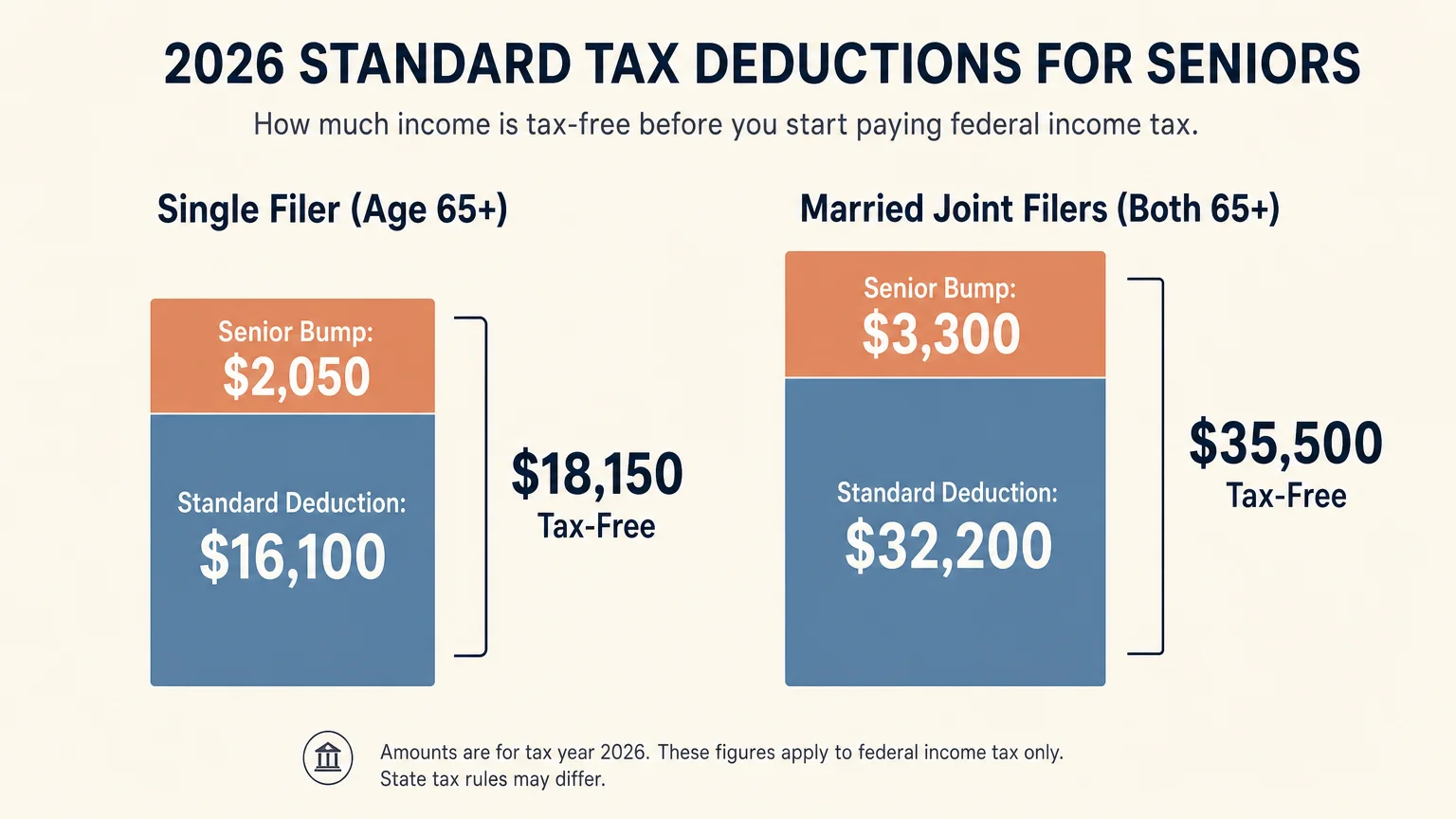

Fortunately, the tax code provides significant buffers for seniors. In 2026, the baseline standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. On top of this, the IRS offers an additional standard deduction for taxpayers aged 65 and older: $2,050 for single filers and $1,650 per qualifying spouse for joint returns.

Recent legislation introduced an even larger shield. Through 2028, taxpayers 65 and older can claim an additional senior deduction of $6,000 per person, provided their adjusted gross income stays below $75,000 for singles or $150,000 for joint returns.

Consider a married couple, both 66 years old, who qualify for these deductions. They could combine the $32,200 base deduction, $3,300 in standard senior add-ons, and $12,000 in the new temporary senior deductions. This effectively shields $47,500 of their income from federal income tax before they pay a single dime to the Internal Revenue Service (IRS). State taxes, however, are a different story. While states like Florida and Texas have no state income tax, and others fully exempt pension income, several states tax your pension precisely the same way the federal government does. Always verify your state’s specific revenue guidelines.

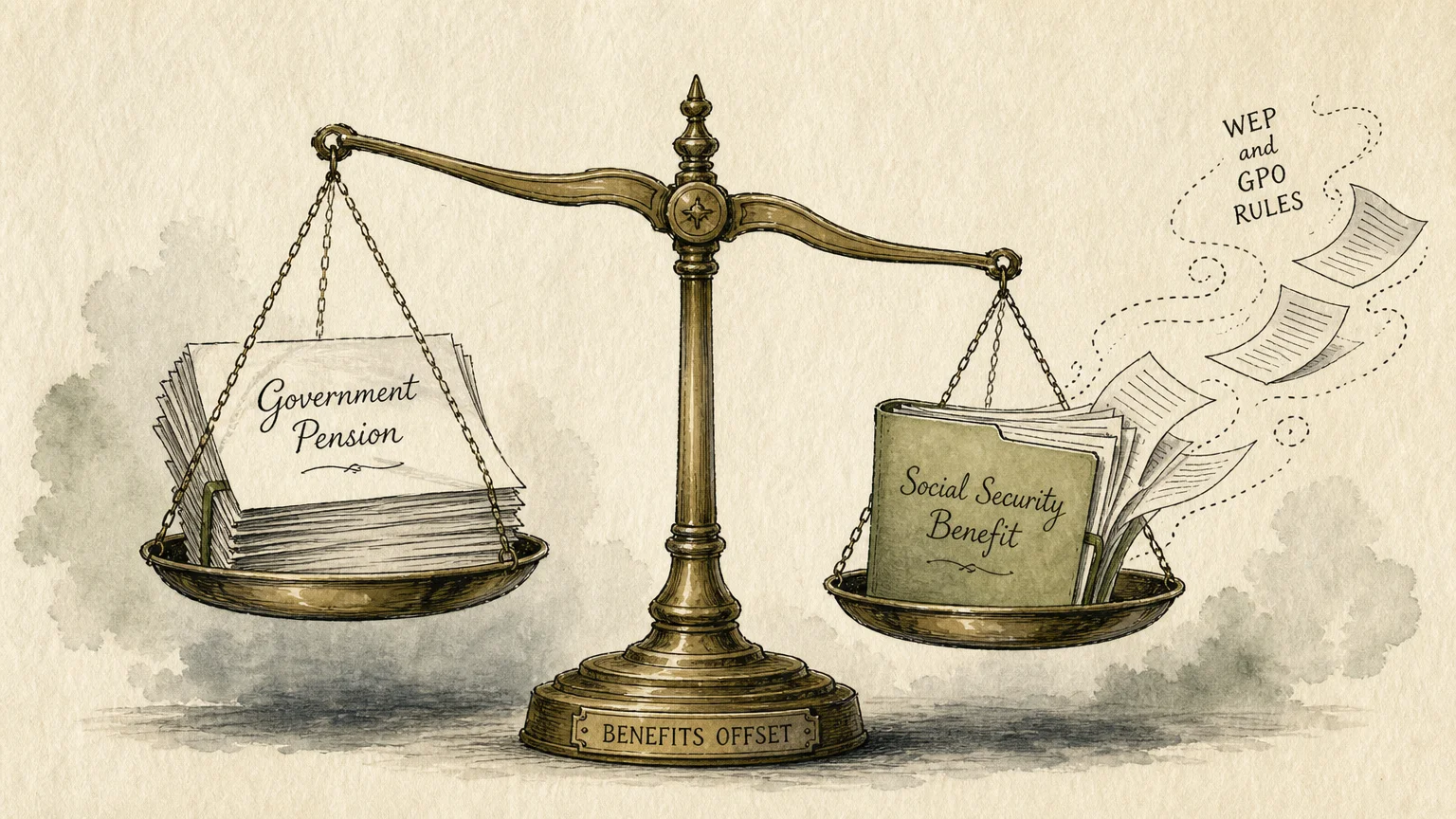

Social Security Offsets: The WEP and GPO Explained

Many seniors mistakenly believe their pension and Social Security operate independently. If you earned your pension in the private sector where you paid FICA payroll taxes, your Social Security benefits will not be reduced. In fact, the 2026 Social Security cost-of-living adjustment (COLA) increased benefits by 2.8%, pushing the average retired worker’s monthly check to roughly $2,026 and the maximum benefit at full retirement age to $4,152.

However, if you worked as a teacher, police officer, or municipal employee in a state that did not withhold Social Security taxes, you are dealing with “non-covered” employment. This triggers two specific provisions that can drastically reduce your Social Security Administration (SSA) benefits:

- Windfall Elimination Provision (WEP): If you earned a pension from non-covered work but also worked enough years in the private sector to qualify for Social Security, the WEP reduces your primary Social Security benefit. The formula lowers the multiplier used to calculate your benefit, which can result in hundreds of dollars lost each month.

- Government Pension Offset (GPO): The GPO affects spousal and survivor benefits. If you receive a government pension from a job where you did not pay Social Security taxes, the SSA reduces your spousal or survivor benefit by two-thirds of the amount of your government pension. For example, if your municipal pension is $1,500 a month, two-thirds of that is $1,000. If your expected spousal Social Security benefit was $1,200, the GPO reduces it by $1,000, leaving you with just $200 a month from Social Security.

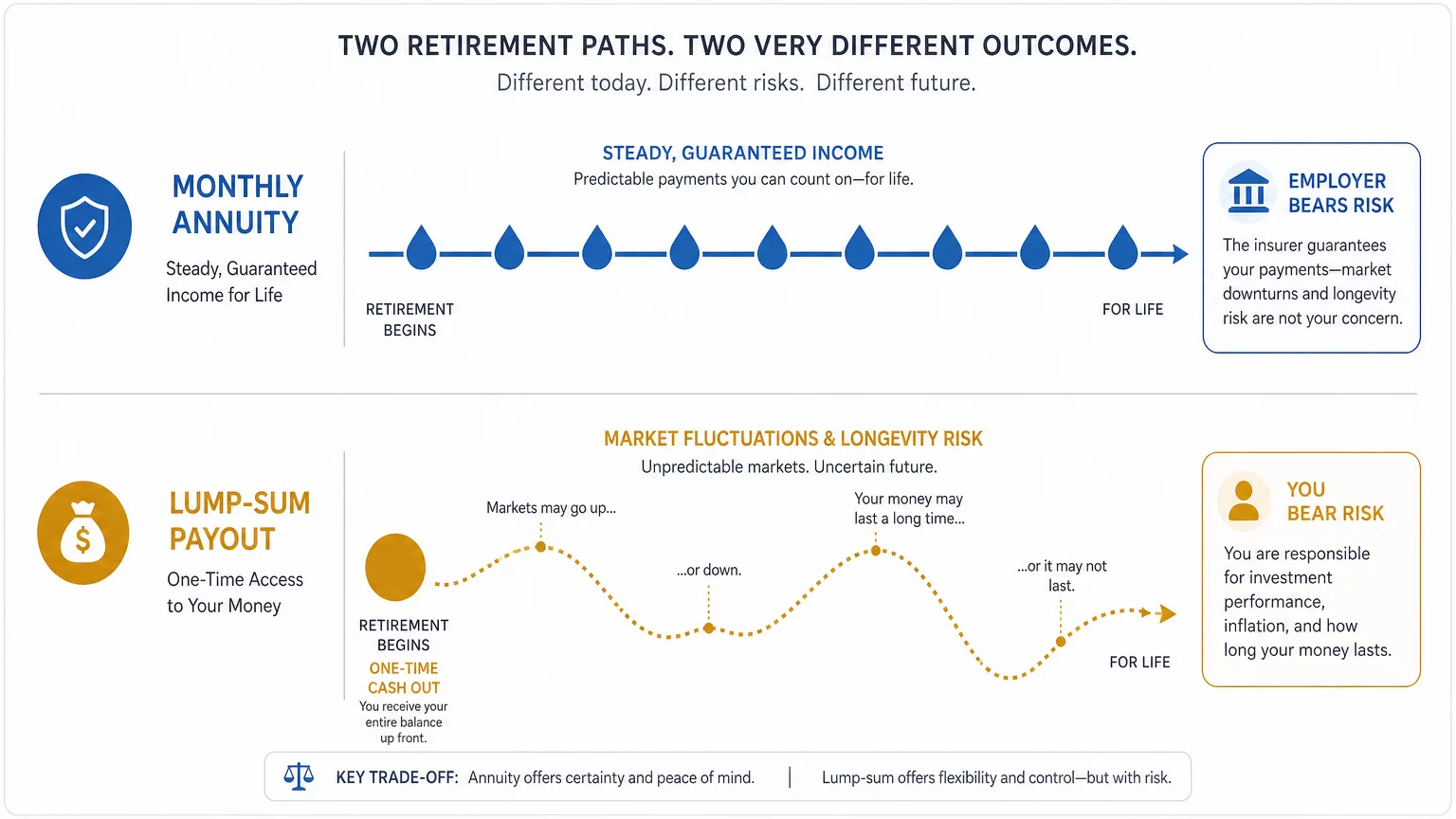

The Critical Decision: Monthly Annuity vs. Lump-Sum Payout

When you retire, many pension plans offer a one-time choice: take a guaranteed monthly payment for the rest of your life, or walk away with a massive lump-sum buyout. This is arguably the most consequential financial decision you will make in retirement.

“If you are lucky enough to have a defined benefit pension, cherish it. Guaranteed lifetime income is the ultimate financial security blanket.” — Suze Orman, Personal Finance Expert

Taking the monthly annuity provides peace of mind. The employer retains the longevity risk (the risk you live to be 105) and the market risk (the risk the stock market crashes). Conversely, a lump-sum buyout allows you to roll the total value of your pension into a Traditional IRA. This gives you complete control over the investments, offers the flexibility to withdraw large sums for emergencies, and ensures any remaining balance passes to your heirs when you die.

Here is a breakdown of how the two options compare:

| Feature | Monthly Annuity Pension | Lump-Sum Buyout (Rolled to IRA) |

|---|---|---|

| Income Guarantee | Lifelong payments guaranteed by employer/PBGC. | Market-dependent; you could run out of money. |

| Investment Control | None. The employer manages the pension fund. | Total control. You decide how funds are invested. |

| Legacy for Heirs | Limited. Stops when you (or your spouse) pass away. | Full legacy. Remaining balance goes to beneficiaries. |

| Inflation Protection | Typically fixed and loses purchasing power over time. | Potential to outpace inflation if invested aggressively. |

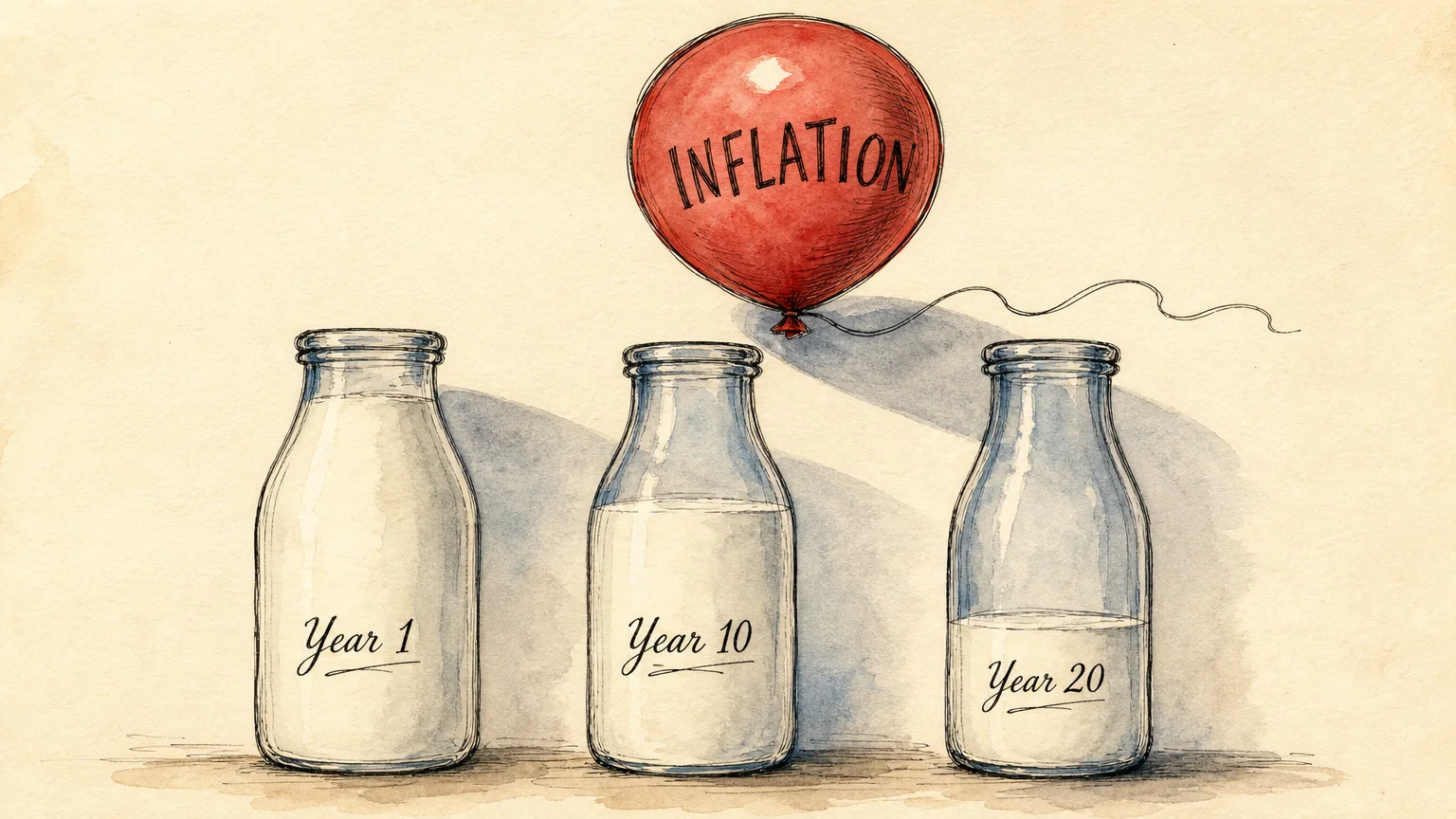

Inflation Risk: Does Your Pension Have a COLA?

If you decide to take the monthly annuity, you must account for inflation. Unlike Social Security, which saw a 2.8% automatic COLA increase for 2026, the vast majority of private-sector pensions offer a fixed, flat payout. A $2,500 monthly pension feels substantial on the day you retire at age 65. However, if inflation averages 3% per year, the purchasing power of that $2,500 will be nearly cut in half by the time you reach age 85. When building your retirement budget, you must rely on other assets—like 401(k) withdrawals, IRAs, or part-time work—to bridge the gap as your fixed pension loses its true value over time.

What Can Go Wrong

Managing a pension seems straightforward, but administrative oversights and poor tax planning can easily derail your retirement. Avoid these common mistakes:

- Choosing a Single-Life Annuity Without Spousal Consent: A single-life annuity offers the highest monthly payout because payments permanently stop the moment you die. If you are married and choose this option without realizing the consequences, you could leave your surviving spouse destitute. By law, married participants usually must obtain a signed, notarized waiver from their spouse to choose a single-life option over a joint-and-survivor annuity.

- Taking a Lump Sum in Cash: If you accept a lump-sum buyout and the company writes a check directly to you, the IRS requires the plan administrator to withhold 20% for federal taxes. If you are under age 59½, you may also face a 10% early withdrawal penalty. To avoid this entirely, you must execute a “direct trustee-to-trustee rollover” straight into your Traditional IRA.

- Forgetting About Medicare IRMAA: Heavy pension income increases your Modified Adjusted Gross Income (MAGI). If your MAGI crosses certain thresholds, the government slaps you with an Income-Related Monthly Adjustment Amount (IRMAA), forcing you to pay significantly higher premiums for Medicare Part B and Part D. You can find current IRMAA brackets at Medicare.gov.

- Losing Track of Old Pensions: If you worked for a company 30 years ago and they were acquired, merged, or went bankrupt, your pension still belongs to you. Countless seniors miss out on free money simply because they forgot to claim a pension from a job they held in their twenties.

When to Consult a Professional

Because pension decisions are permanent, consulting a fiduciary financial advisor or a Certified Public Accountant (CPA) is highly recommended in specific situations. You should seek professional guidance if:

- You are offered a limited-time buyout window. Companies often offer a 60-day window to accept a lump sum. An advisor can run the mathematical “present value” calculation to tell you if the buyout is a fair deal or if you are better off keeping the monthly check.

- You are subject to the WEP or GPO. Calculating exact Social Security offsets is notoriously complex. A professional can help you time your Social Security filing to minimize the damage of these provisions.

- You are worried about estate taxes and legacy planning. If passing wealth to your children is your primary goal, a tax professional can help you structure your pension buyout and IRA rollovers to ensure your heirs do not inherit a massive tax burden.

Frequently Asked Questions

Are pensions taxed by the state?

State tax rules vary widely. While some states have no income tax and others fully exempt pension income, certain states tax your pension just like regular income. Always check your specific state’s revenue department guidelines to determine your liability.

Can I roll my pension into an IRA?

Yes, if your defined benefit plan offers a lump-sum payout option, you can typically execute a direct rollover into a Traditional IRA. This defers federal income taxes until you take withdrawals in retirement and gives you control over the investments.

Do private pensions adjust for inflation?

Generally, no. Most private-sector pensions do not include an annual cost-of-living adjustment (COLA) and pay a fixed dollar amount for life. In contrast, federal, state, and military pensions frequently offer automatic inflation adjustments.

What happens to my pension if I die?

It depends entirely on the payout option you chose at retirement. If you selected a single-life annuity, payments cease immediately upon your death. If you selected a 50% or 100% joint-and-survivor annuity, your designated spouse will continue receiving a portion or all of your monthly benefit for the remainder of their life.

Taking control of your retirement requires understanding exactly how your pension assets fit into your broader financial picture. Review your plan documents, update your beneficiaries, and project your future tax liabilities today. This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.