Where you choose to live during retirement dictates exactly how long your savings will last, acting as a silent partner in your financial strategy. Relocating across state lines can immediately increase your net income by thousands of dollars a year without requiring you to change your investment approach. While states like Florida and Texas attract seniors with the promise of zero income tax, true retirement affordability involves your entire financial picture—including property taxes, sales tax rates, and the treatment of your Social Security and pension income. By understanding the complete tax footprint of your potential retirement destination, you can confidently protect your wealth and ensure your monthly income stretches as far as possible for the decades ahead.

Why State Taxes Matter More in Retirement

During your working years, managing state taxes usually meant simply accepting whatever your employer withheld from your paycheck. Retirement changes the rules entirely. You now control exactly where your income originates, how much you withdraw, and when you recognize those taxable events. Transitioning from a steady salary to a mix of Social Security, pensions, and portfolio withdrawals requires a completely different approach to tax management.

Different states treat these income streams in wildly divergent ways. Some states heavily tax wages but give retirees a free pass on investment distributions. Other states aggressively tax IRA withdrawals but completely ignore Social Security. If your financial plan relies heavily on distributions from a traditional 401(k), relocating to a state that aggressively taxes ordinary income could drain your portfolio years faster than you projected.

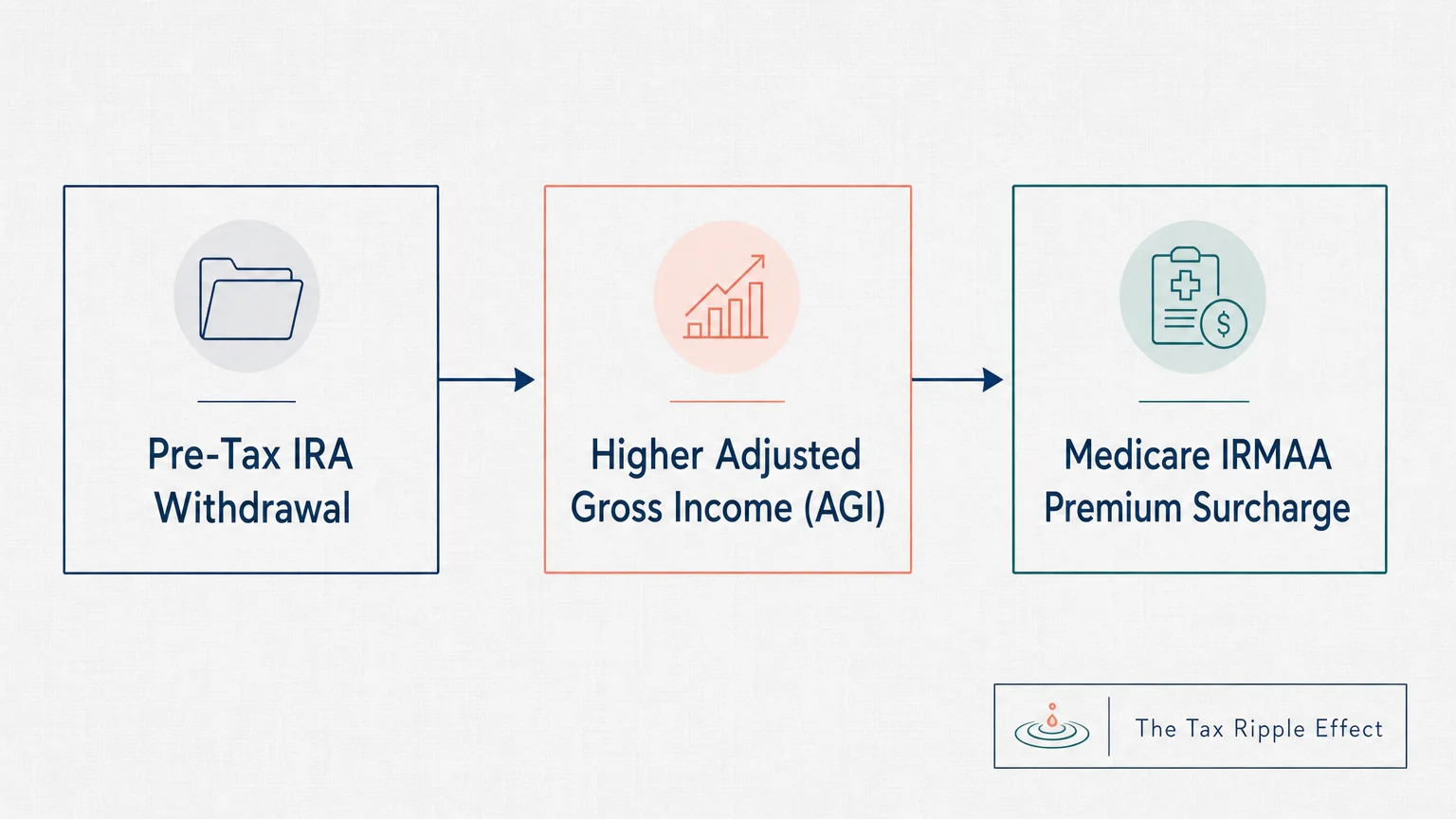

Every dollar you hand over to the state department of revenue is a dollar you cannot spend on travel, healthcare, or family. Worse, withdrawing extra funds from your pre-tax accounts just to cover a high state tax bill increases your overall adjusted gross income. This ripple effect can push you into a higher federal tax bracket or trigger higher Medicare premiums through the Income-Related Monthly Adjustment Amount (IRMAA). Controlling your state tax burden allows you to keep your federal adjusted gross income lower, protecting your wealth on multiple fronts.

“Taxes will be the single biggest expense in retirement. The lower your taxes, the longer your money will last.” — Ed Slott, CPA and Retirement Tax Expert

The True Cost of No-Income-Tax States

The concept of keeping 100 percent of your retirement distributions holds obvious appeal. In 2026, nine states boast no broad-based personal income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

Moving to one of these states feels like an automatic pay raise. If you withdraw $80,000 annually from a traditional IRA, skipping a 5 percent state income tax keeps $4,000 in your pocket every single year. Over a twenty-year retirement, that represents $80,000 in pure tax savings, assuming your withdrawals remain static.

However, states must generate revenue to pave highways, fund local schools, and maintain emergency services. When a state gives up the income tax, it inevitably leans heavily on property taxes, sales taxes, and vehicle registration fees. Evaluating affordability requires you to look beyond the income tax zero and assess the total cost of living.

Texas and Florida serve as prime examples of this trade-off. Texas charges zero income tax but enforces some of the steepest property taxes in the nation, routinely exceeding 2 percent of a home’s assessed value in major metropolitan areas. A $400,000 home in Texas could easily generate an $8,000 annual property tax bill. Florida balances its lack of income tax with higher insurance premiums and above-average sales taxes in many counties. New Hampshire does not tax earned income but maintains incredibly high local property taxes to fund its municipalities.

| State | Individual Income Tax | Typical Sales Tax Impact | Property Tax Burden |

|---|---|---|---|

| Alaska | 0% | Low (No state tax; local varies) | Average |

| Florida | 0% | Average | Average to High |

| Nevada | 0% | High | Low |

| New Hampshire | 0% | None | Very High |

| South Dakota | 0% | Average | Average |

| Tennessee | 0% | High | Low |

| Texas | 0% | Average to High | Very High |

| Washington | 0% | High | Average |

| Wyoming | 0% | Low | Low |

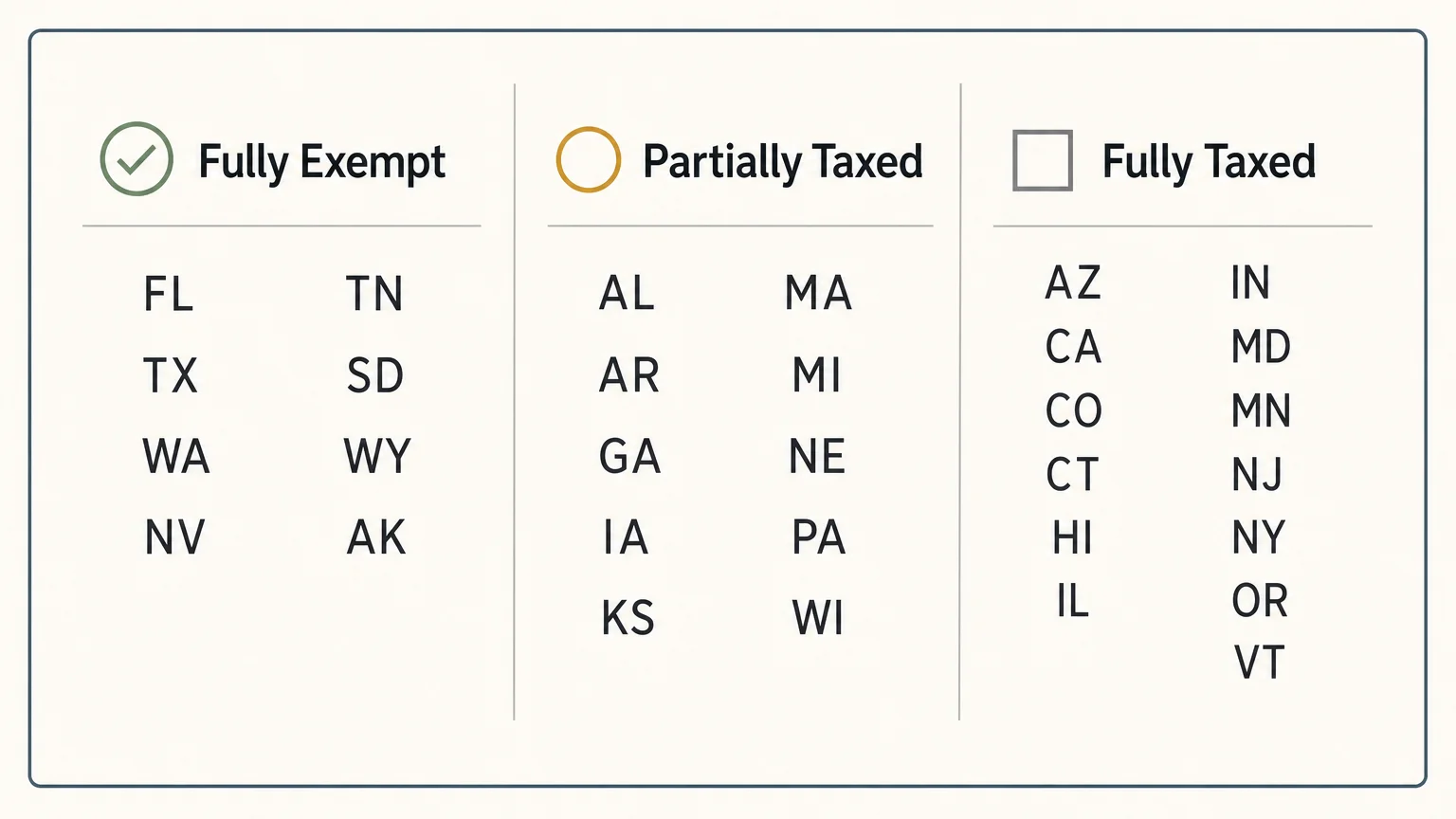

States That Will Not Tax Your Social Security

For most Americans, Social Security represents the absolute foundation of their retirement income plan. Protecting this guaranteed income stream from state taxation provides immediate financial relief and helps your benefits keep pace with the annual Cost of Living Adjustment (COLA).

According to current tax codes, 41 states completely exempt Social Security benefits from state taxation in 2026. If you live in one of these states, you will never owe a dime of state tax on your monthly benefits, regardless of how much you earn from other sources.

Unfortunately, nine states still tax Social Security benefits to some degree: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, Vermont, and West Virginia.

Even within these nine states, nuance matters. Many offer income thresholds that protect middle-class retirees from the tax. For instance, New Mexico exempts Social Security for single filers earning under $100,000 and joint filers earning under $150,000. Connecticut and Vermont also phase out the exemption based on your adjusted gross income. However, if you possess a high net worth and generate substantial income from investments or part-time consulting, living in these states guarantees the local government will take a slice of your Social Security.

Remember that state taxation operates completely separately from federal taxation. The Internal Revenue Service (IRS) may tax up to 85 percent of your Social Security benefits if your combined income exceeds federal thresholds. Relocating to a state that does not tax Social Security only solves the state-level problem; it does not eliminate your federal tax obligations.

States That Completely Exempt Pension and IRA Income

While the nine no-income-tax states steal the headlines, several states with standard income taxes offer massive carve-outs specifically for retirees. These locations actively encourage seniors to relocate by sheltering their retirement savings from state taxation entirely.

Illinois, Pennsylvania, Mississippi, and Iowa stand out as uniquely beneficial destinations for retirees who rely heavily on fully taxable retirement accounts.

Illinois levies a flat state income tax on wage earners, but it completely exempts distributions from 401(k) plans, traditional IRAs, and public or private pensions. If your entire income derives from retirement accounts and Social Security, your Illinois state income tax bill drops to zero. Pennsylvania offers a similar deal, completely exempting pension and IRA income for residents who have reached age 59½. Mississippi excludes all qualified retirement income from state taxes, pairing this aggressive tax break with an exceptionally low overall cost of living.

Iowa recently joined this elite tier. As of 2023, Iowa completely eliminated state income taxes on retirement income for residents aged 55 and older. This sweeping change transformed Iowa into one of the most tax-friendly states in the Midwest for older adults.

If you plan to execute large Roth conversions during your early retirement years, living in one of these exempt states saves you thousands of dollars. A $100,000 Roth conversion normally triggers a massive state tax bill. Executing that same conversion in Pennsylvania or Illinois costs you nothing at the state level, allowing you to maximize the power of tax-free growth moving forward.

Factoring in Medicare and Healthcare Costs

Evaluating a state solely on its tax code ignores the largest variable expense of your later years: healthcare. Medical costs vary dramatically by geographic region, heavily influencing how far your retirement income actually stretches.

Base Medicare costs remain identical nationwide. For 2026, the standard Medicare Part B premium costs $202.90 per month, and the Medicare Part A inpatient hospital deductible sits at $1,736 per benefit period. Everyone pays these baseline amounts, regardless of whether they live in a high-tax coastal city or a rural midwestern town.

The localized costs emerge when you purchase supplemental coverage. Medicare Supplement (Medigap) premiums fluctuate significantly based on your zip code. Insurance carriers base their pricing on local healthcare utilization rates, the cost of medical care in the area, and state-specific insurance regulations. A Plan G policy that costs $130 a month in a low-cost state might easily cost $250 a month in a different region.

Medicare Advantage (Part C) plans also operate on a localized basis. Moving to a rural area with low property taxes might leave you with exactly one Medicare Advantage plan to choose from, severely limiting your access to specialists. Conversely, highly populated areas often boast fiercely competitive Medicare Advantage markets, resulting in plans with zero-dollar premiums and robust extra benefits like dental and vision coverage. Before finalizing a move, verify your anticipated healthcare costs at Medicare.gov to ensure your preferred doctors participate in the local networks.

Pitfalls to Watch For

Relocating purely for financial reasons requires meticulous execution. Avoid these common missteps when chasing a lower cost of living:

- Moving Without Renting First: Buying a home in a new state without testing the community often leads to expensive reversals. Rent for at least six months to verify the climate, healthcare access, and social environment fit your expectations before committing your equity.

- Ignoring Property Tax Reassessments: Many states strictly limit how much property taxes can increase for existing homeowners. However, when a home sells, the county immediately reassesses the property at its current market value. The tax bill you see on a real estate listing rarely matches the bill you will receive after closing.

- Overlooking Inheritance and Estate Taxes: Some states give you a pass on income tax but aggressively target your wealth when you pass away. States like Pennsylvania and New Jersey levy inheritance taxes that apply even to modest estates, significantly reducing the legacy you leave to your children.

- Underestimating Travel Expenses: Moving halfway across the country to save $3,000 in state income taxes makes little sense if you end up spending $5,000 a year on flights and hotels to visit your grandchildren. Always factor geographic distance into your annual budget.

Getting Expert Help

Uprooting your life and finances across state lines introduces significant complexity to your tax planning. Consider consulting a qualified financial planner or tax professional in these scenarios:

- Managing Complex Pension Payouts: If you earned a pension in a high-tax state but plan to retire in a no-tax state, federal law generally protects your payouts from your former state. However, properly navigating the withholding rules requires professional oversight.

- Selling a Highly Appreciated Primary Residence: Liquidating a home in a high-cost area can trigger massive capital gains if your profit exceeds the standard IRS exclusions ($250,000 for singles; $500,000 for couples). A tax professional can help you structure the sale to minimize your federal and state tax liabilities.

- Executing Roth Conversions: Timing your Roth conversions around a geographic move requires precision. An advisor can help you execute these conversions exactly when your state tax liability bottoms out, shielding your assets from unnecessary taxation.

- Establishing New Domicile: High-tax states aggressively audit former residents who claim to have moved. A professional will guide you through the legal steps required to sever ties with your old state, such as updating your driver’s license, voter registration, and estate documents.

Frequently Asked Questions

Do I pay taxes to the state where I earned my pension, or where I live now?

Under federal law, specifically the State Taxation of Pension Income Act, your former state cannot tax your retirement income once you establish domicile in a new state. You only owe state income taxes on your pension to your current state of residence.

Will my Medicare costs change if I move to another state?

Your foundational Medicare Part A and Part B costs remain the same nationwide. However, premiums for Medicare Advantage (Part C), standalone Prescription Drug Plans (Part D), and Medicare Supplement (Medigap) plans vary significantly by zip code and state regulations.

Do states tax Social Security survivor benefits differently than standard benefits?

No. If a state exempts standard Social Security retirement benefits, it also exempts Social Security spousal and survivor benefits. You can verify your specific state regulations and benefit amounts through the Social Security Administration (SSA).

Relocating in retirement offers a powerful lever to increase your standard of living and make your savings last longer. Take the time to run the numbers on property taxes, healthcare premiums, and state income taxes before packing your boxes. With careful planning, you can find a destination that honors your hard work and protects your financial future.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.