Your pension and Social Security benefits could provide a steady stream of income for decades, but maximizing that money requires deliberate planning before you take your first withdrawal. Outliving your savings is a valid concern, especially since a 65-year-old today has a strong chance of living well into their late 80s or beyond. To keep your financial foundation rock-solid, you must understand how taxes, withdrawal rates, and inflation interact to stretch your fixed income. Navigating the current tax landscape—including updated standard deductions and required minimum distribution rules—can reveal surprising ways to keep more of your money. By strategically timing your benefits and minimizing hidden tax traps, you can ensure your retirement income comfortably outlasts your timeline.

The Essentials

- Your pension payout choice permanently dictates whether your spouse receives continued income after your death.

- Delaying your Social Security claim up to age 70 can dramatically increase your guaranteed monthly baseline income.

- New 2026 tax deductions for seniors offer unique opportunities to shield a significant portion of your retirement funds from federal taxes.

- Strategic IRA withdrawals can help you avoid massive Medicare surcharges and unexpected taxes on your Social Security.

The Mechanics of Modern Pension Payouts

Most retirees treat their pension like a set-it-and-forget-it income stream. You receive a monthly check, pay your bills, and go about your daily life. However, how long your pension actually provides financial security depends heavily on inflation and the exact payout structure you select at the point of retirement.

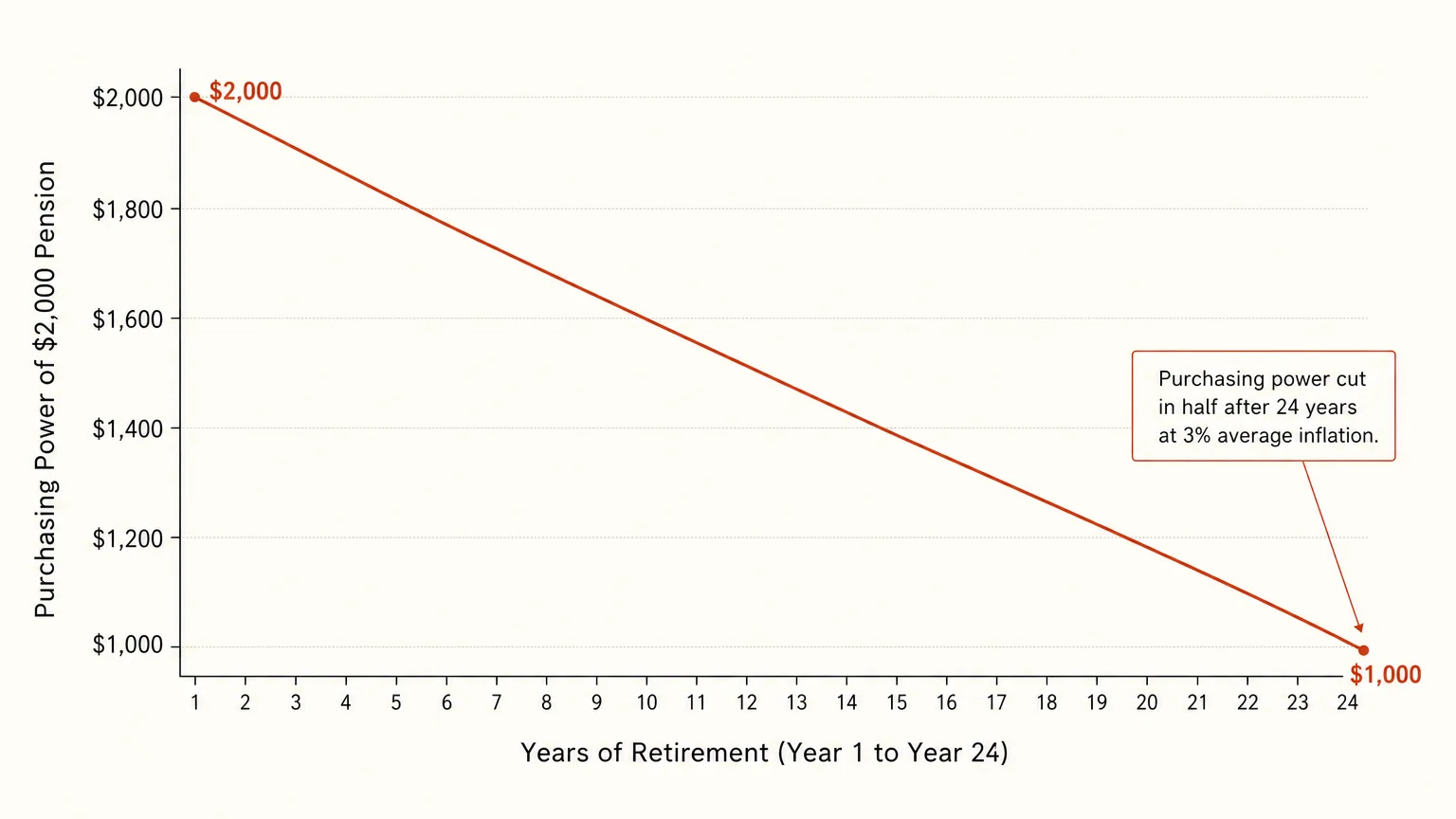

A defined benefit pension guarantees you a specific monthly amount for the rest of your life. Unless your pension plan includes a Cost-of-Living Adjustment (COLA), the real value of that monthly check will erode over time. If inflation averages just 3% per year, the true purchasing power of a fixed $2,000 monthly pension is essentially cut in half over a 24-year retirement. You will still receive the same amount, but it will cover far fewer of your essential expenses.

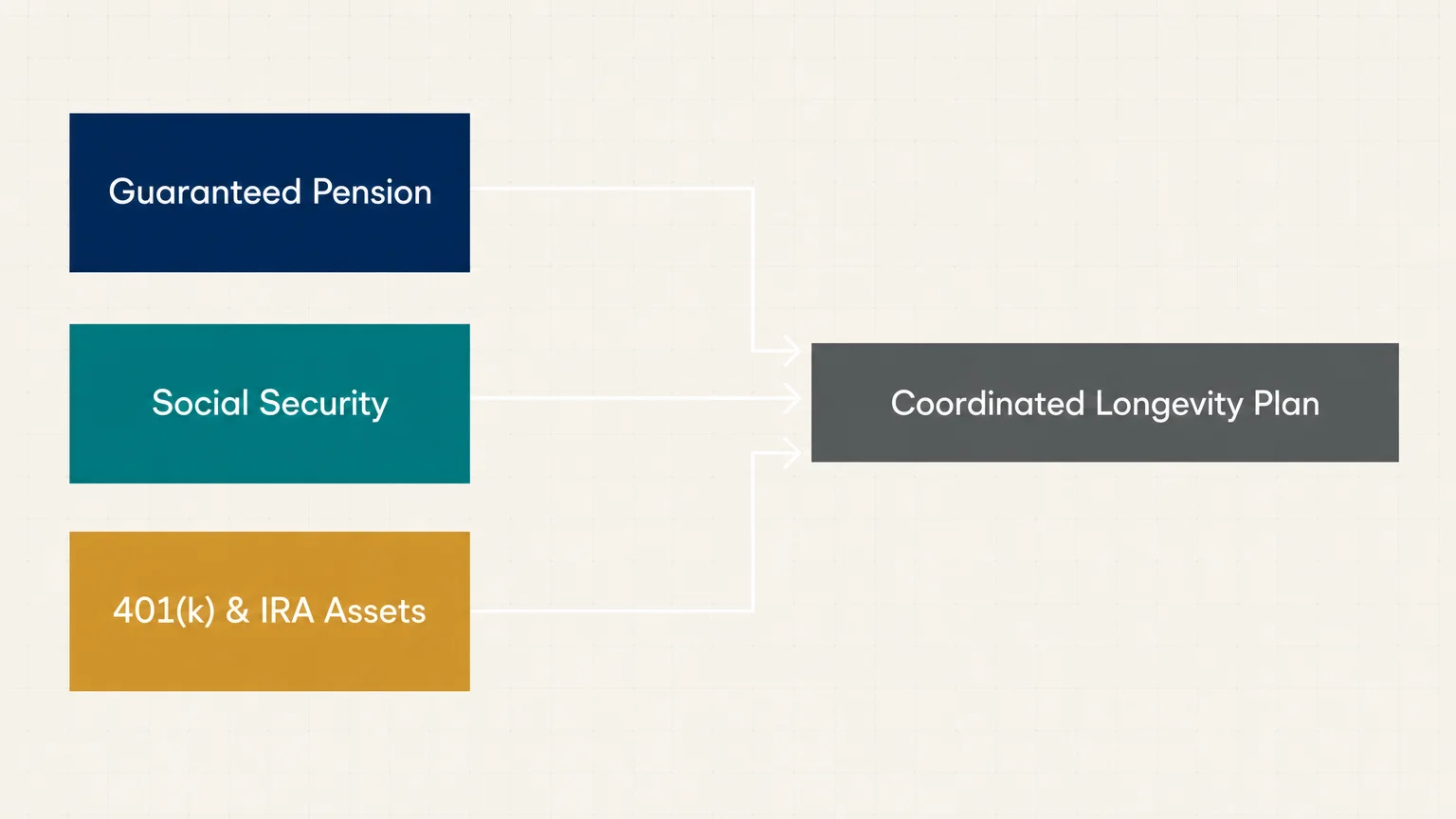

To combat this silent financial drain, you must coordinate your guaranteed pension income with your other assets; your 401(k), IRAs, and Social Security all play a critical role in your longevity plan.

“We’ve spent so much time thinking about accumulation that we haven’t thought about a plan to take what we have accumulated and stretch it over however long we live.” — Jean Chatzky, Financial Expert

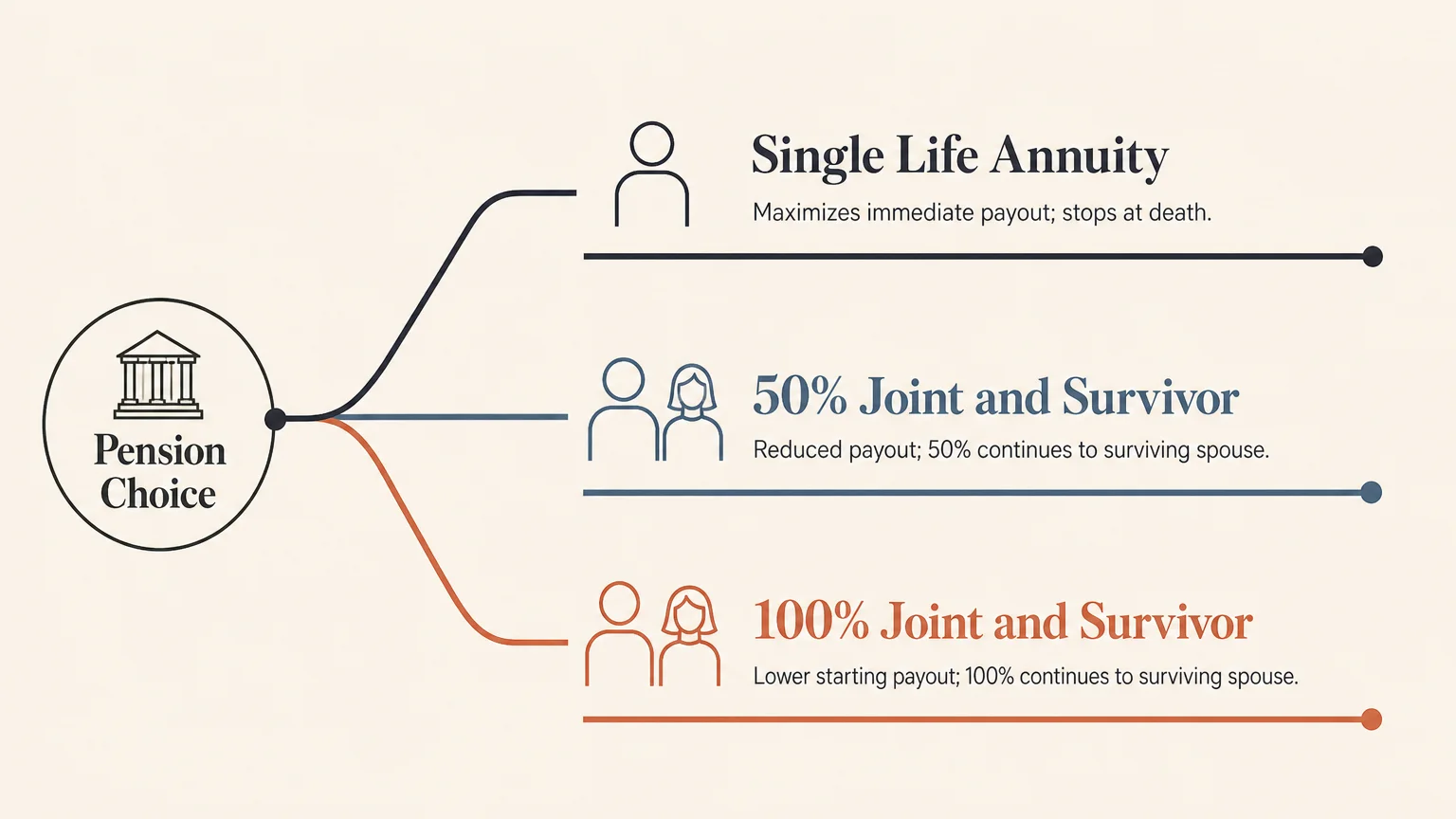

Single Life vs. Joint and Survivor: Weighing Your Options

When you sit down to finalize your pension paperwork, your employer will present you with several payout options. This choice is almost always irrevocable. Once you lock in a structure, you cannot change your mind a few years later. The path you select dictates whether your pension income survives you or disappears the moment you pass away.

Here is how the most common pension payout structures compare:

| Payout Option | How It Works | The Advantage | The Drawback |

|---|---|---|---|

| Single Life Annuity | Pays a set monthly amount for your lifetime only. | Maximizes your immediate monthly cash flow. | Payments stop entirely when you pass away; your surviving spouse receives absolutely nothing. |

| 50% Joint and Survivor | Pays a slightly reduced monthly amount during your lifetime. | When you pass away, your surviving spouse continues to receive 50% of your monthly benefit for the rest of their life. | Your starting monthly benefit is lower than the Single Life option. |

| 100% Joint and Survivor | Pays a significantly reduced monthly amount while you are alive. | Your surviving spouse continues to receive the exact same monthly payment after your death without interruption. | You take the largest upfront reduction in your current monthly income. |

| Period Certain Annuity | Guarantees payments for your life, but also guarantees payments for a set timeline (e.g., 10 or 20 years). | If you die within the designated period, your beneficiary receives the remaining payments for that term. | Does not guarantee lifetime income for a surviving spouse if you happen to outlive the set term. |

Choosing a Single Life Annuity might seem tempting because the initial monthly payout is the highest. But if you are married and your spouse relies on that income to pay the mortgage or buy groceries, opting for the highest payout today could severely compromise their financial security tomorrow.

Coordinating Your Pension with Social Security

Your pension is only one pillar of your retirement income. Social Security forms the other guaranteed pillar. Because pensions provide a reliable base of income, they grant you incredible flexibility when deciding the optimal time to claim your government benefits.

As of 2026, the average Social Security monthly check for retired workers is approximately $2,081. While that helps cover foundational living expenses, it might not be enough on its own to fund a comfortable lifestyle. This is why the timing of your claim is paramount. You can claim Social Security as early as age 62, but doing so permanently reduces your monthly benefit. If you wait until your Full Retirement Age (FRA)—which is 67 for anyone born in 1960 or later—you receive 100% of your earned benefit.

Delaying past your FRA is where the strategy yields massive dividends. For every single year you delay claiming Social Security between your FRA and age 70, your benefit increases by a guaranteed 8% per year. The maximum Social Security retirement benefit at age 70 in 2026 reaches an impressive $5,181 per month.

If your pension provides enough income to cover your basic living expenses throughout your early 60s, you hold a tremendous advantage. You can afford to delay your Social Security claim. By living off your pension and intentionally drawing down some tax-deferred IRA funds early in your retirement, you let your Social Security benefits grow by that guaranteed 8% annually. Because Social Security includes an annual inflation adjustment, delaying your claim gives you a much larger financial base upon which all future cost-of-living increases are calculated.

The Hidden Impact of Inflation on Fixed Income

While a pension offers a stable foundation, you must respect how inflation operates as a relentless, silent tax on your retirement lifestyle. Healthcare expenses—including Medicare premiums, supplemental insurance, and out-of-pocket costs—routinely outpace general inflation metrics.

Consider a fixed pension of $3,000 per month. Without a cost-of-living adjustment, a modest 3% inflation rate over ten years reduces the real-world purchasing power of that $3,000 to approximately $2,230. Give it twenty years, and it plummets to roughly $1,660. You will physically receive a check for $3,000, but it will buy drastically less at the grocery store, pharmacy, and gas pump.

To offset this erosion, retirees must utilize their investment portfolios to generate reliable, inflation-beating growth. Because your pension acts similarly to a massive bond—delivering predictable, steady income regardless of market conditions—you likely have the psychological fortitude to keep a larger portion of your 401(k) or IRA invested in equities. Equities historically outpace inflation over long timelines, providing the aggressive growth engine necessary to supplement your fixed pension when you reach your 80s and 90s.

Tax Strategies to Stretch Your Retirement Dollars

Retirement success is not just about what you make; it is primarily about what you keep. Taxes will likely be the single largest expense you face in your golden years. If you blindly pull money from your retirement accounts while simultaneously collecting a pension and Social Security, you could inadvertently trigger a massive tax bill.

“Advisors do pretty well helping people build money, but they have to play the full game, and that includes the distribution phase, too. As an advisor, if you can help people keep more of the money they’ve made and make it last through retirement, that’s where the value is.” — Ed Slott, CPA and Retirement Expert

A proactive strategy requires a solid understanding of current IRS regulations. The 2026 tax landscape presents incredible opportunities for seniors to shield their income. The baseline standard deduction for married couples filing jointly is $32,200, while single filers receive a $16,100 deduction. Furthermore, if you are age 65 or older, the IRS offers an additional standard deduction of $1,650 per qualifying spouse for joint filers, and $2,050 for single filers.

Even better, taxpayers aged 65 and older in 2026 who claim the standard deduction may also qualify for a newly implemented $6,000 deduction per eligible person (phasing out at higher income levels). When you stack these deductions, the math becomes incredibly favorable. A married couple over 65 could potentially shield up to $47,500 of their income from federal taxes before paying a single dollar to the IRS. For a single filer over 65, that tax-free threshold reaches $24,150.

By carefully managing how much taxable income you generate from IRA distributions on top of your pension, you can comfortably stay within the lowest possible tax brackets. You must also prepare for the mandatory distributions the government forces you to take. Under the SECURE 2.0 Act, the age at which you must begin taking Required Minimum Distributions (RMDs) from traditional IRAs and 401(k)s is 73 for individuals born between 1951 and 1959. Failing to take this distribution on time results in a steep penalty of up to 25% of the amount you were supposed to withdraw.

Because your pension utilizes your lowest tax brackets, your RMDs sit directly on top of that income, often catapulting you into a higher marginal tax bracket. To circumvent this issue, consider executing Roth IRA conversions during your early retirement years—specifically in the window between the day you retire and the year you turn 73. Moving funds from a tax-deferred traditional IRA to a tax-free Roth IRA requires paying taxes upfront, but it permanently shelters that money and its future growth from both taxes and lifetime RMD requirements.

Costly Errors to Sidestep

Navigating the transition from earning a paycheck to generating retirement income involves a minefield of potential missteps. Avoid these specific mistakes to ensure your money lasts as long as you do.

- Triggering the Social Security “Tax Torpedo”: Many retirees are stunned to learn that up to 85% of their Social Security benefits can be taxed. The IRS determines this using a formula called “Combined Income,” which calculates your Adjusted Gross Income, plus your nontaxable interest, plus half of your Social Security benefits. Because your pension directly increases your Adjusted Gross Income, it can easily push your Combined Income over the threshold, causing a large portion of your Social Security to instantly become taxable.

- Ignoring Medicare IRMAA Surcharges: Medicare Part B and Part D premiums are inextricably tied to your income level from two years prior. If your pension, combined with IRA withdrawals or real estate capital gains, pushes your Modified Adjusted Gross Income (MAGI) above specific IRS thresholds, you will face the Income-Related Monthly Adjustment Amount (IRMAA). This hidden surcharge can double or even triple your monthly Medicare premiums.

- Misunderstanding the Widow’s Penalty: When one spouse passes away, the surviving spouse’s tax filing status changes from “Married Filing Jointly” to “Single.” Even though total household income generally drops due to the loss of one Social Security check and a potentially reduced pension, the surviving spouse is thrust into the much narrower single tax brackets. This often results in the surviving spouse paying significantly higher taxes on less overall income.

- Accepting a Pension Buyout Without Scrutiny: Employers sometimes offer a massive lump-sum buyout check instead of a lifetime monthly pension. While receiving a six-figure check sounds incredibly appealing, taking it means you are transferring all the longevity risk and investment risk directly onto your own shoulders. If the stock market crashes the year after you invest your lump sum, your lifetime income is severely jeopardized. Always evaluate the lump sum against the monthly annuity using life expectancy projections and realistic investment returns.

When DIY Isn’t Enough

Managing a straightforward pension and a few savings accounts might seem entirely manageable on your own. However, certain financial intersections require highly specialized professional intervention. Do not attempt to navigate these complex scenarios without expert help:

- Evaluating a Pension Lump-Sum Offer: If your employer offers you $400,000 today instead of $2,500 a month for the rest of your life, the math behind the scenes is incredibly complex. A fiduciary financial advisor or an actuary can run a discount rate analysis to determine if the lump sum is genuinely a fair financial deal compared to the lifetime annuity payout.

- Executing Large Roth Conversions: Moving hundreds of thousands of dollars from a traditional IRA to a Roth IRA requires meticulous multi-year tax planning. A professional will calculate exactly how much to convert each year to maximize the current favorable tax brackets without inadvertently triggering Medicare IRMAA surcharges or bumping you into a severely punitive tax rate.

- Inheriting a Retirement Account: The rules surrounding inherited IRAs drastically changed under recent legislation. Most non-spouse beneficiaries must now completely empty an inherited IRA within a strict 10-year window. Liquidating this money strategically requires an expert to prevent massive, unnecessary tax spikes during your peak earning years.

Frequently Asked Questions

Can my pension plan ever run out of money?

If you have a traditional defined benefit pension backed by a private employer, your benefits are generally protected up to certain limits by the Pension Benefit Guaranty Corporation (PBGC), a federal agency. Even if your former employer declares bankruptcy, the PBGC steps in to pay your pension up to a legally mandated maximum. State and local government pensions are not covered by the PBGC but are typically backed by the taxing authority of the state itself.

What is the RMD age for 2026?

Under the SECURE 2.0 Act, the Required Minimum Distribution (RMD) age for individuals in 2026 is 73, provided you were born between 1951 and 1959. If you were born in 1960 or later, your required beginning age will eventually increase to 75.

Does my pension count as earned income for IRA contributions?

No. Pension income, Social Security benefits, and annuity payouts are considered passive or retirement income. To contribute funds to a traditional IRA or Roth IRA, the IRS explicitly requires you to have taxable compensation (earned income), such as wages, salaries, or self-employment income.

Will receiving a pension reduce my Social Security benefits?

If you paid Social Security taxes while working at the specific job that provided your pension, your pension will not reduce your Social Security benefits. However, if your pension stems from a government job where you did not pay Social Security taxes—such as certain federal, state, or local government roles—your Social Security benefits may be significantly reduced by the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO).

Securing your retirement is about much more than just collecting a monthly check and hoping for the best. By carefully coordinating your pension, Social Security, and investment withdrawals, you can actively safeguard your purchasing power against inflation and insidious tax traps. Take the time today to review your payout options, map out a cohesive withdrawal strategy, and lock in the financial peace of mind you deserve. This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.