Securing a dependable income stream in retirement is critical because living costs and healthcare expenses are rising faster than most portfolios can support. While traditional pensions are increasingly rare, replicating their guaranteed monthly payout is the safest way to ensure you never outlive your money. Reliable retirement income protects you against stock market volatility and unexpected inflation. With the 2026 Medicare Part B standard premium increasing to $202.90 and the latest Social Security cost-of-living adjustment at just 2.8%, covering baseline expenses requires more than a standard savings account. Understanding how to maximize guaranteed income sources like Social Security, annuities, and any remaining defined-benefit plans helps you build an unshakable financial safety net that lasts your entire life.

The Disappearing Traditional Pension

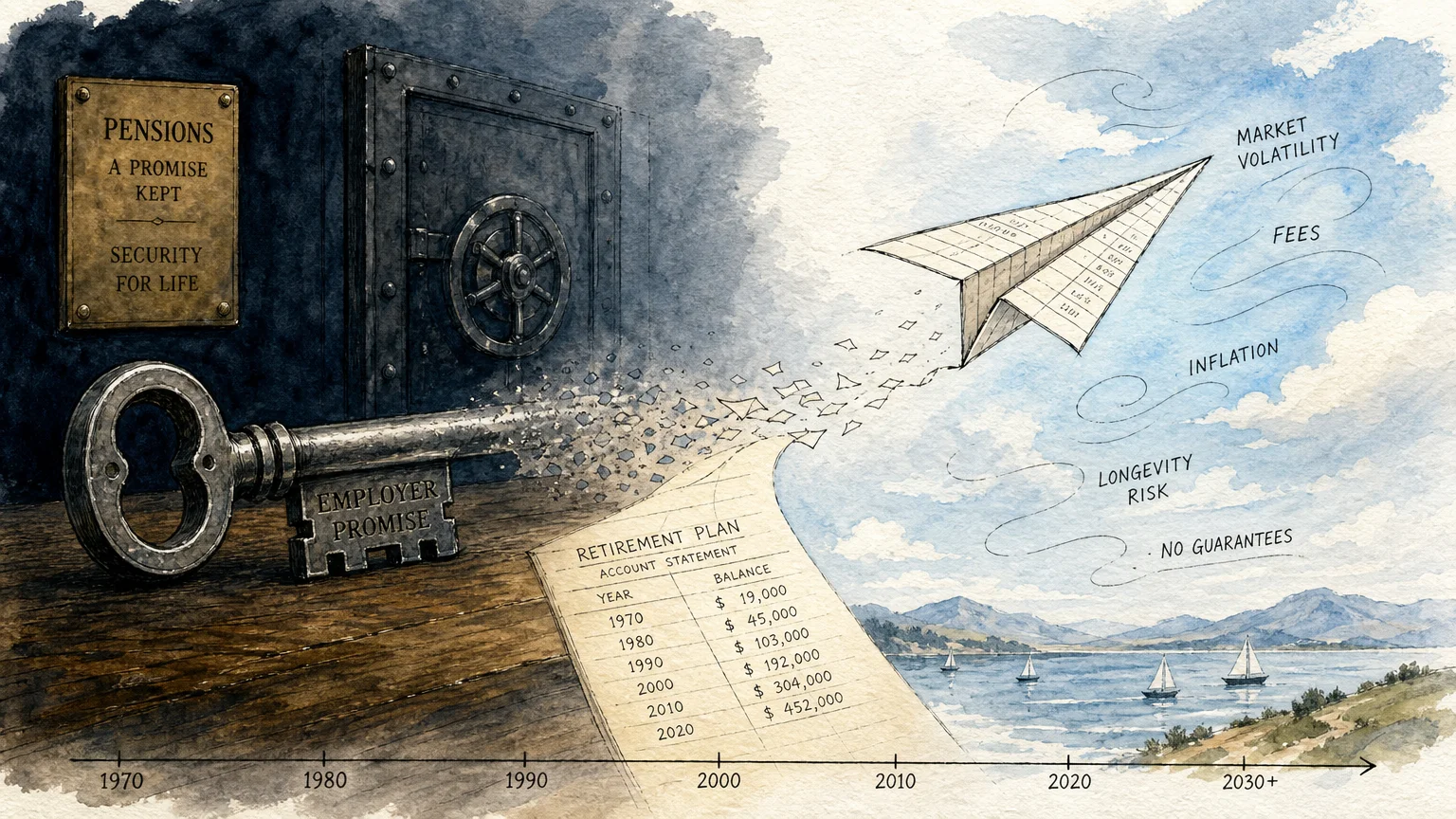

Decades ago, retiring comfortably almost always involved a gold watch and a reliable corporate pension. These defined-benefit plans promised a specific monthly payout for life, effectively shifting the risk of market crashes and longevity away from the worker and onto the employer. Today, the retirement landscape looks entirely different. Companies have largely replaced traditional pensions with defined-contribution plans, such as the 401(k), transferring the heavy burden of investment management and market risk directly onto your shoulders.

If you are among the fortunate few who still have a traditional pension, you hold an incredibly valuable asset. A guaranteed check arriving every month provides a psychological and financial anchor that a fluctuating stock portfolio simply cannot match. You do not have to worry about timing the market, adjusting your withdrawal rates during a recession, or calculating complex sequence-of-returns risks. The employer makes the promise, and the employer funds the payout.

Furthermore, even if a private company faces financial ruin, most traditional pensions have a powerful safety net. The Pension Benefit Guaranty Corporation (PBGC) is a federal agency that steps in to pay benefits if an employer’s plan fails. For plans terminating in 2026, the PBGC guarantees a maximum monthly benefit of $7,789.77 for a 65-year-old retiree electing a straight-life annuity. While highly compensated executives might see a reduction if their promised payout exceeded this cap, the vast majority of workers remain fully protected under federal law.

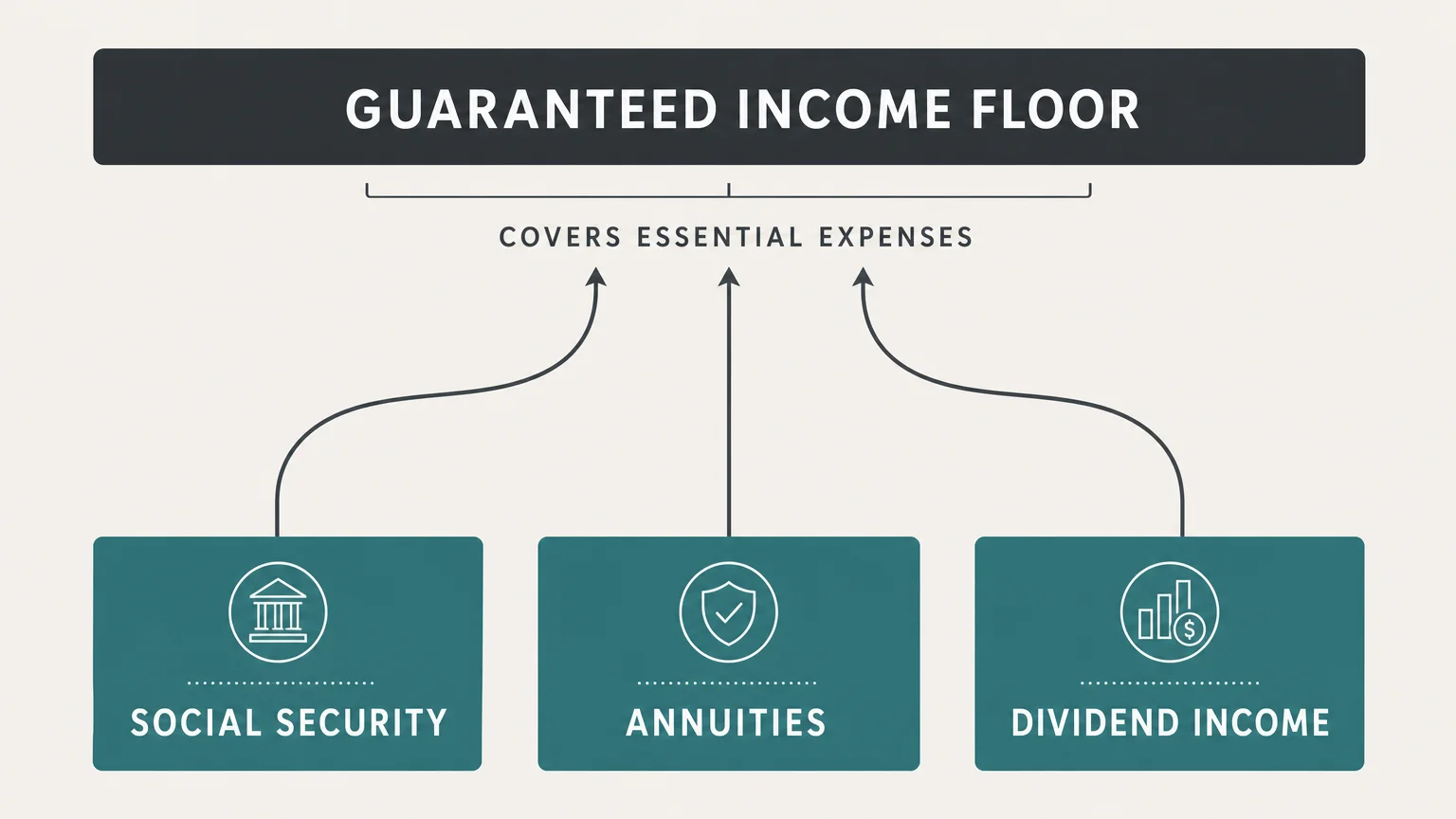

Why Guaranteed Income Provides True Peace of Mind

Building a successful retirement plan involves establishing an “income floor”—a reliable foundation of money that covers all your non-negotiable living expenses. When your housing, utilities, food, and healthcare costs are completely satisfied by guaranteed income sources like a pension and Social Security, your remaining investment portfolio is freed from the pressure of daily survival. You can allow your stocks and bonds to grow untouched during market downturns because your basic needs are already met.

Relying exclusively on investment withdrawals leaves you vulnerable to a phenomenon known as sequence of returns risk. If the stock market crashes during the first few years of your retirement, pulling money out of a shrinking portfolio permanently damages your account’s ability to recover. Pensions bypass this risk entirely. The fixed payout remains steady regardless of whether the stock market reaches a record high or suffers a severe correction.

“The goal in retirement is to have guaranteed income that covers your basic needs, so you never have to worry about outliving your money.” — Suze Orman, Personal Finance Expert

To understand exactly how a pension outshines other retirement assets, it helps to compare the foundational traits of different income sources. The table below illustrates why securing lifetime income is so advantageous.

| Income Source | Market Risk | Inflation Protection | Lifespan Guarantee |

|---|---|---|---|

| Traditional Pension | None | Varies (Depends on plan rules) | Yes (Pays for life) |

| Social Security | None | Yes (Annual COLA) | Yes (Pays for life) |

| Fixed Income Annuity | None | Optional (With rider) | Yes (Pays for life) |

| 401(k) / IRA Withdrawals | High (Subject to market drops) | Depends on investments | No (Can run out of money) |

The Impact of Rising Costs in 2026

Even with a solid nest egg, inflation acts as an invisible tax on your purchasing power. Managing modern retirement costs requires understanding exactly how much money is coming in versus how much is flying out the door. According to the Social Security Administration, the average monthly benefit for a retired worker in 2026 is approximately $2,081. While the 2026 Cost-of-Living Adjustment (COLA) of 2.8% provides a slight boost, it rarely feels like enough when weighed against skyrocketing senior living expenses.

Consider the math behind a typical retiree’s budget this year. A 2.8% COLA on a $2,081 benefit yields an extra $58 per month. However, healthcare costs aggressively consume that raise. The standard Medicare Part B premium increased from $185.00 in 2025 to $202.90 in 2026—an immediate $17.90 deduction from your check before you even see the money. When you add in the newly elevated 2026 Medicare Part B annual deductible of $283, your actual net increase is surprisingly small.

This stark reality highlights why a secondary source of guaranteed income is practically mandatory. Relying solely on Social Security guarantees a life spent strictly budgeting every dollar. A pension—or a strategically built substitute—bridges the dangerous gap between what the government provides and what a comfortable life actually costs.

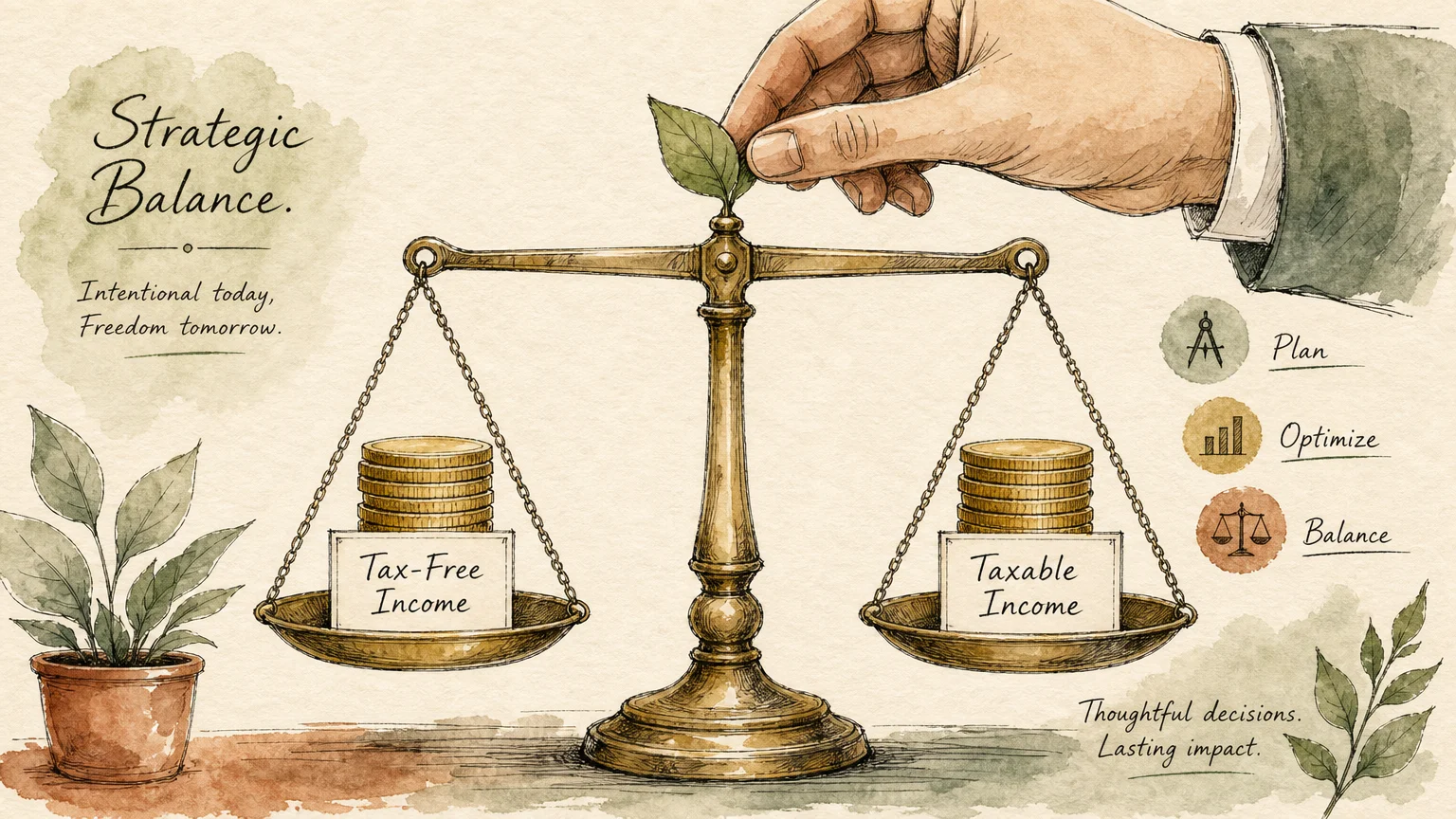

Navigating Your Tax Strategy

Receiving guaranteed monthly income is wonderful, but keeping it out of the hands of the Internal Revenue Service requires deliberate planning. Most traditional pension payouts are taxed as ordinary income at the federal level because the contributions were made with pre-tax dollars. Depending on where you live, you may also owe state income taxes on your monthly check, though many states offer generous exemptions for retirees.

The 2026 tax landscape introduces important figures that every senior should memorize. The standard deduction has increased to $16,100 for single filers and $32,200 for married couples filing jointly. Furthermore, the IRS continues to offer an additional standard deduction for taxpayers age 65 and older—$2,050 for singles and $1,650 per qualifying spouse for married couples filing jointly. Taking advantage of these higher thresholds helps shelter a significant portion of your pension and Social Security income from federal taxation.

Additionally, retirees in 2026 benefit from the recently enacted senior tax provisions—often referred to as the “No Tax on Social Security” framework. This provision allows qualifying taxpayers age 65 and older to claim a new $6,000 federal deduction, which phases out for high earners making over $75,000 as a single filer or $150,000 jointly. Maximizing these specific tax breaks ensures that your hard-earned pension money stays in your bank account where it belongs.

How to Build Your Own Pension

If you spent your career in the private sector and never had access to a defined-benefit plan, you are responsible for manufacturing your own pension. Creating a reliable, lifetime income stream requires converting a portion of your accumulated savings into guaranteed paychecks. Here are the most effective strategies to build your personal pension floor.

- Delay Social Security for Maximum Payouts: The easiest way to increase your guaranteed lifetime income is to wait before claiming Social Security. While you can claim at age 62, your monthly check is permanently reduced. Waiting until your full retirement age guarantees 100% of your earned benefit. Delaying until age 70 adds an 8% guaranteed return for every year you wait past your full retirement age. In 2026, the absolute maximum Social Security benefit for someone retiring at age 70 is an impressive $5,181 per month.

- Purchase a Single Premium Immediate Annuity (SPIA): An immediate annuity functions exactly like a traditional pension. You hand over a lump sum to a highly rated insurance company, and in return, they contractually guarantee to pay you a fixed monthly amount for the rest of your life. This eliminates market risk entirely and provides a precise figure you can use to pay your baseline bills.

- Construct a Bond and CD Ladder: For those who prefer to keep control of their principal, building a ladder of Certificates of Deposit (CDs) and highly rated government bonds provides predictable cash flow. By purchasing investments that mature at regular intervals—every six months or every year—you create a steady stream of accessible cash that mimics a pension without tying your money up in an insurance contract.

- Utilize Guaranteed Minimum Income Riders: If you hold funds in a variable or fixed-indexed annuity, you can often add an income rider. This allows your underlying investments to grow with the market while still providing a contractual guarantee that your income withdrawals will never drop below a specified threshold, even if the market crashes.

Costly Errors to Sidestep

Managing guaranteed income requires navigating several irreversible decisions. Making a mistake at the starting line of retirement can permanently damage your financial security over a thirty-year timeframe.

- Taking the Lump Sum Without Doing the Math: Many companies offer retiring employees a choice between a lifetime monthly pension check and a massive, one-time lump-sum buyout. While receiving a check for hundreds of thousands of dollars is tempting, managing that money to replicate the pension’s lifetime payout is incredibly difficult. Unless you have a pristine health history indicating a short lifespan, or you are an exceptionally skilled investor, the monthly annuity is often the mathematically superior choice.

- Ignoring the Surviving Spouse: When selecting your pension payout option, you must decide what happens to the money when you pass away. Choosing the “Single-Life” payout generates the highest monthly check, but the payments cease the moment you die, potentially leaving your spouse destitute. Selecting a 50% or 100% “Joint-and-Survivor” option reduces your initial monthly payout, but guarantees your surviving spouse continues receiving checks for the rest of their life.

- Forgetting About Inflation: A flat $2,000 monthly pension check feels comfortable on the day you retire, but inflation silently erodes its buying power. If your pension does not include an automatic Cost-of-Living Adjustment, you must build inflation protection into your other investments. Assuming a fixed check will cover your expenses twenty years from now is a recipe for financial disaster.

When DIY Isn’t Enough

While basic budgeting and saving can be handled independently, coordinating massive tax moves and intricate income strategies often requires professional intervention. Attempting to navigate the complexities of federal benefit laws alone can trigger massive penalties.

Consider hiring a fiduciary financial planner if you are facing a corporate buyout offer. Evaluating a lump-sum vs. annuity decision requires running complex actuarial software that factors in your specific mortality tables, expected market returns, and current interest rates. A professional can objectively analyze the math to ensure you are not leaving money on the table.

You should also seek professional guidance when your guaranteed income pushes you into higher tax brackets. High required minimum distributions (RMDs) combined with a robust pension and Social Security can trigger Medicare IRMAA (Income-Related Monthly Adjustment Amount) surcharges. These hidden taxes can silently double your Medicare Part B and Part D premiums. A qualified CPA or Certified Financial Planner can help you strategize Roth conversions and charitable giving to keep your taxable income safely below these expensive thresholds.

As you map out your financial future, remember that securing a guaranteed income stream is the ultimate defense against an unpredictable world. Whether you are relying on a hard-earned corporate pension, maximizing your Social Security benefits, or purchasing an annuity to build an income floor, protecting your monthly cash flow ensures you remain in complete control of your retirement.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.