Taking a seasonal job provides an immediate way to boost your retirement income without surrendering your hard-earned freedom. You can generate thousands of dollars during a brief two-month sprint, giving you the cash to fund a major vacation or manage rising household expenses. Temporary work bridges the gap between total retirement and a demanding career. Whether you prefer leading summer tours in a national park, preparing tax returns in the spring, or helping with holiday retail in December, the right seasonal role offers a valuable financial safety net and a reliable social outlet. You step in during peak demand, earn a competitive hourly wage, and gracefully step away when the season concludes.

Why Seasonal Jobs Provide the Perfect Balance

Stepping away from a full-time career leaves many seniors feeling a sudden void. Beyond the obvious loss of a regular paycheck, retirement often eliminates daily social interactions and a structured routine. A temporary position solves these problems simultaneously. You dictate when and how much you work, choosing to engage only during the times of year that suit your personal schedule.

Employers actively seek older workers for these short-term roles because seniors bring decades of reliability, strong communication skills, and unmatched problem-solving abilities. Retail managers, tax preparation firms, and park directors know that mature workers require less micromanagement and handle customer interactions with remarkable grace. By leveraging your lifelong experience, you can negotiate better shifts, command higher starting wages, and enjoy the mental stimulation of learning new skills without making a permanent commitment.

“Working in retirement is no longer an oxymoron; it is a financial strategy and a life strategy that keeps you engaged, relevant, and secure.” — Jean Chatzky, Financial Editor

The Top Seasonal Employment Opportunities for Older Adults

Finding the right role depends entirely on your interests, physical mobility, and income goals. The best opportunities generally cluster around major retail holidays, tax season, and summer tourism. According to the Bureau of Labor Statistics, these industries experience massive hiring spikes, meaning you have the leverage to find a position that fits your exact needs.

Winter and Holiday Retail Support

The final three months of the year offer the highest concentration of temporary work. Retailers desperately need reliable staff to handle the influx of holiday shoppers. If you enjoy a fast-paced environment and interacting with the public, this season provides endless opportunities.

- Customer Service Representatives: Many companies hire remote, work-from-home customer service agents to handle holiday order inquiries. You can earn between $17 and $20 per hour without ever leaving your living room; a perfect option if you have mobility concerns or prefer to avoid winter weather.

- Retail Sales Associates: Local boutiques and major department stores ramp up hiring in October. These roles keep you physically active and often come with a valuable perk—steep employee discounts on your own holiday shopping.

- Logistics and Packaging: Delivery companies and warehouses need extra hands to sort packages and coordinate shipping. These roles sometimes pay upward of $21 per hour, though they typically require standing for extended periods and lifting moderately heavy items.

Tax Season Preparation

If you possess a strong attention to detail and enjoy working with numbers, the spring tax season offers incredibly lucrative seasonal work. Financial firms begin hiring in December for positions that run through mid-April.

- Tax Preparers: National chains offer paid training programs to teach you the fundamentals of tax software. Once certified, you guide clients through their annual filings. Experienced preparers easily earn over $24 per hour.

- Administrative Office Support: Accounting firms require organized individuals to manage client appointments, handle phone calls, and organize financial documents. These low-stress roles allow you to enjoy a professional office environment without the pressure of calculating tax liabilities.

National Parks and Summer Hospitality

Seniors who spend their winters in warm climates and their summers traveling often flock to the outdoor hospitality industry. State and national parks rely heavily on retirees to keep their campgrounds running smoothly.

- Campground Hosts: In exchange for a few hours of work each day—greeting visitors, answering questions, and doing light site maintenance—many parks provide a free RV hookup along with a modest hourly wage or stipend.

- Tour Guides and Museum Docents: If you love history or local ecology, leading guided tours provides a highly engaging way to spend the summer. These roles pay around $18 per hour and keep you physically active while sharing your knowledge with appreciative vacationers.

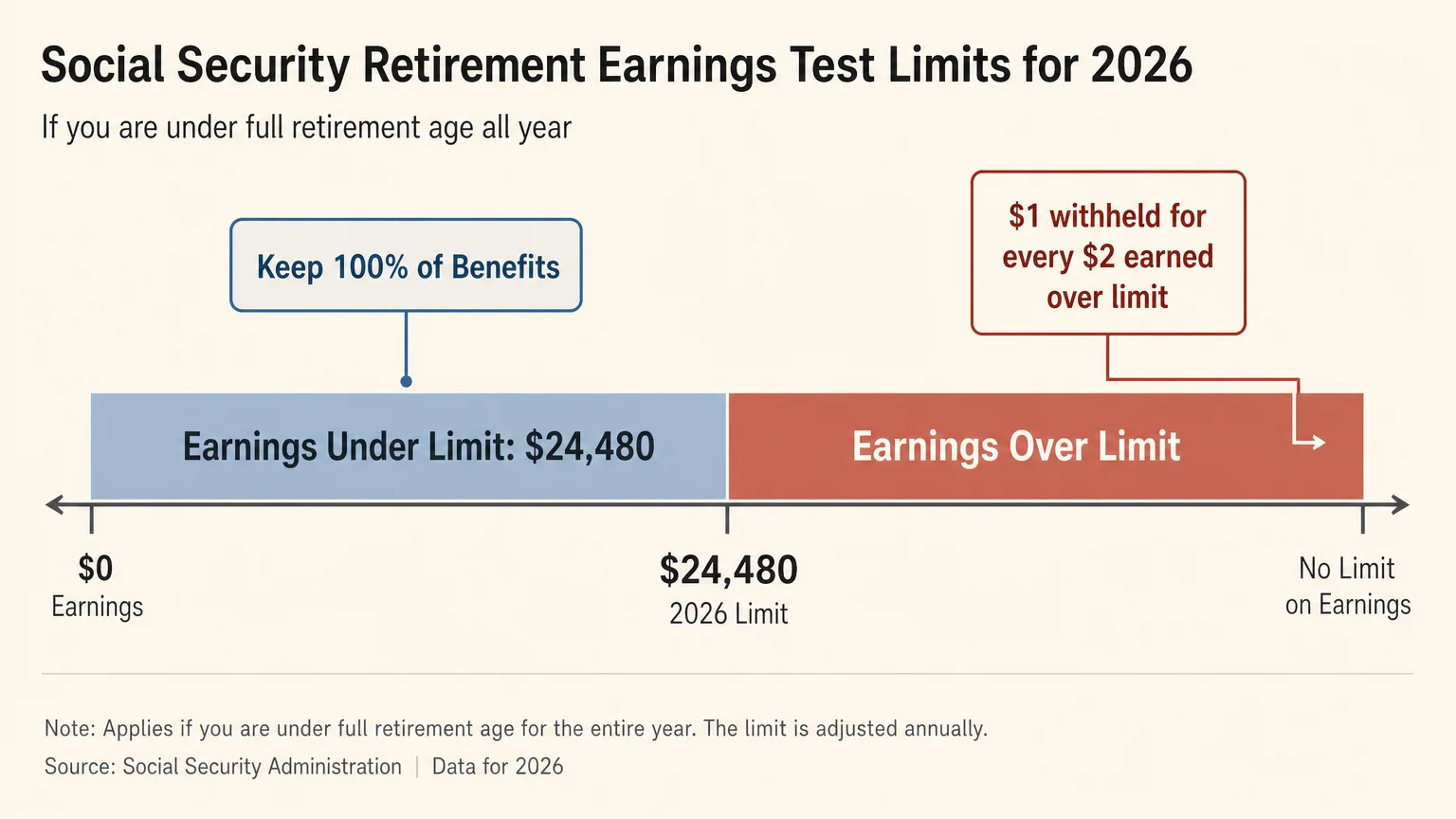

How Seasonal Income Affects Your 2026 Social Security Benefits

Before accepting a seasonal job, you must understand how your wages interact with the Social Security Administration (SSA) earnings limit. A common misconception prevents many seniors from working; they mistakenly believe that any extra income permanently destroys their retirement benefits. In reality, the rules are highly structured and easy to navigate once you know your Full Retirement Age (FRA).

If you claim Social Security before your FRA, the government limits how much you can earn from an employer before they begin temporarily withholding a portion of your monthly check. For the 2026 tax year, the SSA enforces two distinct earnings thresholds depending on your birth year.

| Age Status in 2026 | 2026 Annual Earnings Limit | Benefit Withholding Formula |

|---|---|---|

| Under Full Retirement Age for the entire year | $24,480 | The SSA withholds $1 for every $2 earned above the limit. |

| Reaching Full Retirement Age this year | $65,160 | The SSA withholds $1 for every $3 earned above the limit (applies only to months prior to your birth month). |

| At or above Full Retirement Age | No Limit | You keep 100% of your benefits, regardless of how much you earn. |

Consider a realistic numeric example: Let us say your Full Retirement Age is 67, but you are currently 64. Your monthly Social Security benefit is $1,800. You decide to take a high-paying seasonal job consulting for your former industry and earn $30,480 during the year. Because you exceeded the $24,480 limit by $6,000, the SSA must withhold $1 for every $2 you earned over the cap. This results in a $3,000 withholding penalty.

The SSA does not deduct this gradually. Instead, they withhold your entire $1,800 check for January, and $1,200 from your February check to satisfy the $3,000 penalty. You receive the remaining $600 in February, and your full $1,800 checks resume in March.

Most importantly, the withheld money is not permanently forfeited. Once you finally reach your Full Retirement Age, the SSA recalculates your lifetime payout. They increase your future monthly checks to slowly return the money they withheld during your seasonal working years.

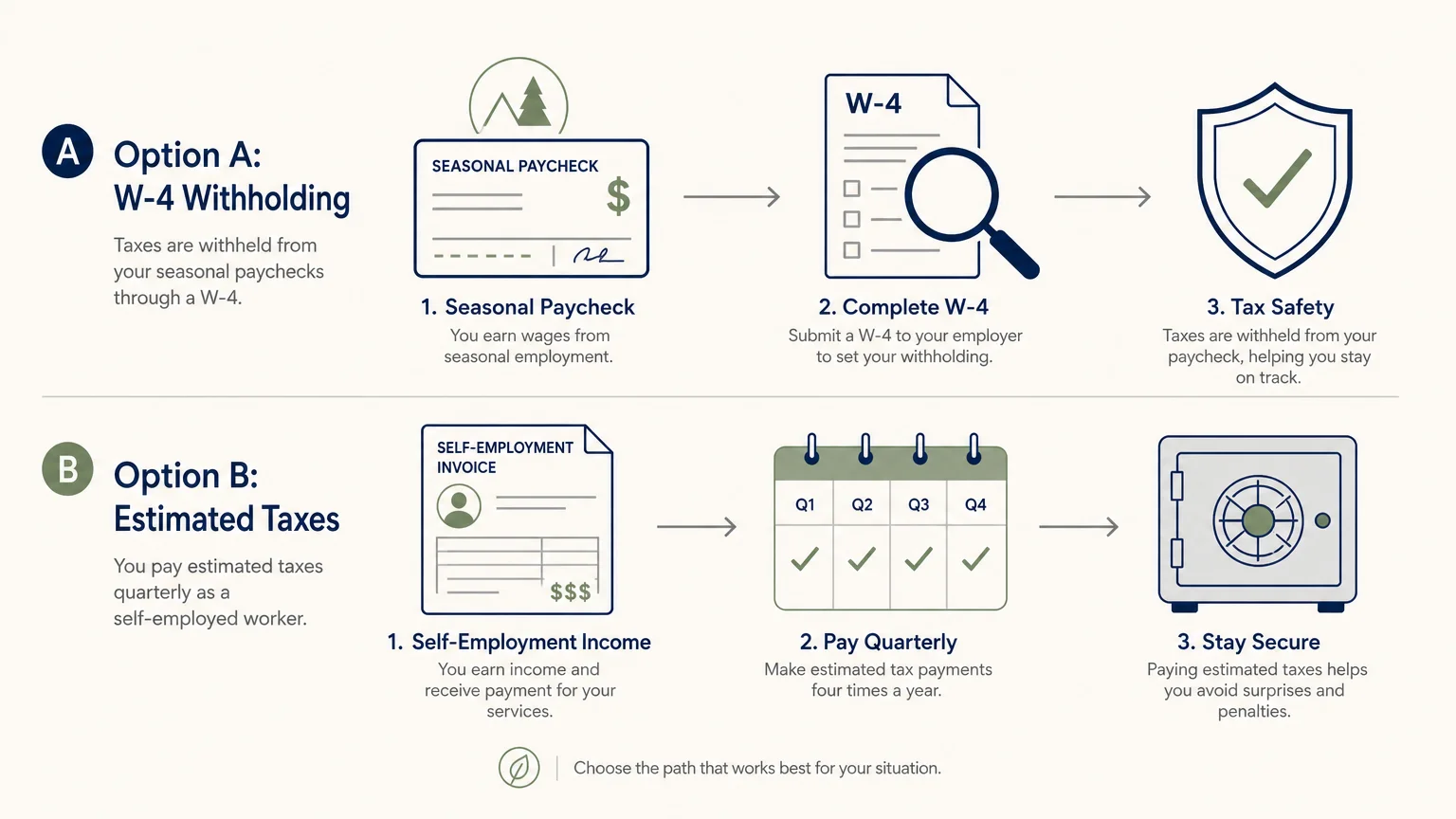

Tax Strategies for Your Seasonal Wages

Working a temporary job changes your tax profile, but the federal tax code offers robust protections for older adults. Knowing how these deductions operate ensures you do not hand your hard-earned seasonal wages right back to the Internal Revenue Service (IRS).

Every dollar you earn from a seasonal employer is subject to standard payroll taxes—commonly known as FICA. Your employer automatically deducts 7.65% of your gross pay to fund Medicare and Social Security. You must pay this tax even if you currently receive Medicare and Social Security benefits; there is no age exemption for payroll taxes.

However, your liability for federal income tax tells a much brighter story. The IRS provides highly generous standard deductions that shield a massive portion of your income. For the 2026 tax year, the baseline standard deduction sits at $16,100 for single filers and $32,200 for married couples filing jointly.

Furthermore, the IRS grants an additional standard deduction specifically for taxpayers age 65 and older. In 2026, single seniors receive an extra $2,050 deduction. Married couples receive an extra $1,650 per spouse, meaning a married couple where both partners are over 65 can claim an additional $3,300. Combined with recent legislative enhancements that provide further deductions for senior tax filers, you can earn a substantial seasonal wage without owing a single cent in federal income taxes. Always verify these precise limits with a tax professional, as your pension or traditional IRA distributions will combine with your seasonal wages to determine your final tax bracket.

Common Mistakes to Avoid When Taking a Seasonal Job

Re-entering the workforce, even for a brief period, requires careful planning. Seniors who rush into a temporary gig often make predictable errors that cost them money and cause unnecessary physical strain. Protect your health and your wallet by avoiding these frequent pitfalls.

- Ignoring the physical demands of the role: A job description might sound delightful until you spend eight hours standing on a concrete floor. Retail and warehouse positions take a heavy toll on your knees and lower back. Always ask the hiring manager if the role allows for seated breaks or requires lifting objects over twenty pounds.

- Falling for work-from-home scams: The seasonal job market unfortunately attracts cybercriminals looking to exploit eager retirees. Legitimate employers never ask you to pay upfront for background checks, training materials, or software. If a remote job offer promises unusually high pay for basic data entry—and requires you to buy your own equipment using a provided “company check”—it is absolutely a scam.

- Forgetting to track business expenses: If you accept a seasonal job as an independent contractor (such as driving for a delivery app or doing freelance photography), your taxes operate differently. You must track your mileage, phone usage, and supply costs. Failing to deduct these expenses leaves you paying significantly higher self-employment taxes at the end of the year.

- Mismanaging Medicare premiums: If your seasonal gig is incredibly lucrative, the extra income could trigger the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge dramatically increases your Medicare Part B and Part D premiums. Keep a close eye on your total Modified Adjusted Gross Income to ensure your brief stint in the workforce does not inflate your healthcare costs.

Finding the Right Advisor for Your Retirement Income Strategy

Integrating seasonal wages into a fixed-income lifestyle occasionally requires professional calibration. A certified financial planner or specialized tax advisor provides clarity when federal regulations overlap. Consider seeking expert guidance if you relate to any of the following scenarios:

- You face a complex tax situation: If you manage Required Minimum Distributions (RMDs) from retirement accounts alongside pension income and seasonal wages, a professional calculates exactly how much you can earn before bumping into a higher tax bracket.

- You plan to work extensively before your Full Retirement Age: An advisor models exactly how the Social Security earnings limit will impact your cash flow month by month, helping you decide if the temporary job is truly worth the withheld benefits.

- You want to reinvest your seasonal earnings: If you took a holiday job specifically to pad your savings, a fiduciary helps you allocate those funds into tax-advantaged accounts or high-yield vehicles that protect your purchasing power against inflation.

You can find vetted, fee-only fiduciaries through reputable organizations like AARP or the National Association of Personal Financial Advisors. Always ensure the professional you choose acts as a fiduciary, legally bound to prioritize your financial well-being over their own commissions.

Frequently Asked Questions About Seasonal Retirement Jobs

Can I work a seasonal job while collecting Social Security?

Yes. You are fully permitted to work while collecting benefits. However, if you have not yet reached your Full Retirement Age, your monthly benefits face temporary reductions if your job pays more than the 2026 earnings limit of $24,480.

Do I have to pay taxes on seasonal job income if I am already retired?

Yes. All earned wages face standard FICA payroll taxes, which fund Medicare and Social Security. Whether you owe federal income tax depends entirely on your total combined income and the standard deductions you claim. Many seniors earn seasonal wages that fall entirely beneath the IRS deduction limits.

What happens to the Social Security benefits withheld due to the earnings limit?

The government does not permanently confiscate your money. Once you hit your Full Retirement Age, the Social Security Administration recalculates your benefit amount upward. You gradually recover the withheld funds through larger monthly checks for the remainder of your life.

Will a temporary job affect my Medicare coverage?

A seasonal job will not cause you to lose your Medicare coverage. However, if your seasonal income is exceptionally high, it could trigger an IRMAA surcharge, which raises the monthly premiums you pay for Medicare Part B and Part D. This typically only affects seniors generating substantial supplementary income.

Where is the safest place to find legitimate remote seasonal jobs?

Focus your search on verified corporate career pages, government portals like USA.gov, and specialized senior employment boards. Avoid responding to unsolicited text messages or vague social media advertisements promising easy remote work.

A seasonal job serves as an outstanding tool for maintaining your financial independence and mental sharpness. You retain the freedom to travel, relax, and enjoy your golden years, but you also hold the power to generate reliable income exactly when you need it most. Review the current earnings limits, calculate your standard deductions, and step back into the workforce with absolute confidence.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.