Retail companies actively recruit older workers because they value your reliability, patience, and lifetime of problem-solving experience. Landing a retail job over 65 offers a practical way to stay socially active while generating extra income to offset inflation. Brands like CVS, The Home Depot, and Ace Hardware run specific hiring initiatives designed to attract retirees, offering flexible scheduling and seasonal transfer programs. Before accepting a part-time position, you must understand how new wages interact with your Social Security benefits and annual tax liability. This guide breaks down exactly which retailers want to hire you, what roles fit your lifestyle, and how to navigate 2026 earnings limits without sacrificing your hard-earned benefits.

Why Retailers Value Your Experience

The retail industry historically struggles with high turnover rates, unpredictable scheduling, and a lack of customer service expertise among entry-level hires. Older workers naturally solve these problems. When you bring decades of workplace discipline, emotional intelligence, and conflict resolution skills to the sales floor, managers notice immediately.

Major corporate chains understand that a multigenerational workforce directly improves their bottom line. Older adults are proven to be highly dependable—often showing up on time, handling high-stress customer interactions with grace, and requiring far less micromanagement than their younger counterparts. Through initiatives like the AARP Employer Pledge Program, over a thousand companies have publicly committed to creating age-inclusive workplaces that actively recruit, train, and retain workers over the age of 50.

Top Retail Companies That Specifically Recruit Seniors

While almost any local shop will appreciate a reliable senior applicant, several national brands have built formal programs tailored entirely around the needs of older adults.

- CVS Health: Known for its “Talent is Ageless” initiative, CVS actively seeks out older workers for both pharmacy support and front-end retail operations. One of their most popular offerings for retirees is the “Snowbird Program.” This unique benefit allows older workers to transfer their employment between northern and southern store locations based on the season, seamlessly accommodating a retirement lifestyle that shifts to warmer climates during the winter.

- The Home Depot: This home improvement giant has a long-standing reputation for hiring retired tradespeople, contractors, and DIY enthusiasts. They want employees who actually understand the tools and materials they are selling. If you spent your career in plumbing, carpentry, or electrical work—or if you simply know your way around a toolbox—your knowledge is highly valued on the sales floor.

- Ace Hardware: As an AARP Employer Pledge signer, Ace Hardware focuses on a community-first approach. Because their stores maintain a smaller footprint compared to massive warehouse retailers, working at Ace generally requires less grueling physical exertion and walking. They prioritize friendly, localized customer service, making it an excellent fit for highly social retirees.

- Walgreens: Similar to CVS, Walgreens offers flexible scheduling for front-end cashiers, merchandisers, and pharmacy technicians. They often provide solid benefits, including employee discounts, which can be incredibly helpful for managing daily household expenses.

- TJX Companies (TJ Maxx, Marshalls, HomeGoods): For those looking for a lower-stress environment focused on apparel and home decor, TJX brands offer excellent part-time merchandising and customer service roles. Their flexible shift options make it easy to work 15 to 20 hours a week without overwhelming your schedule.

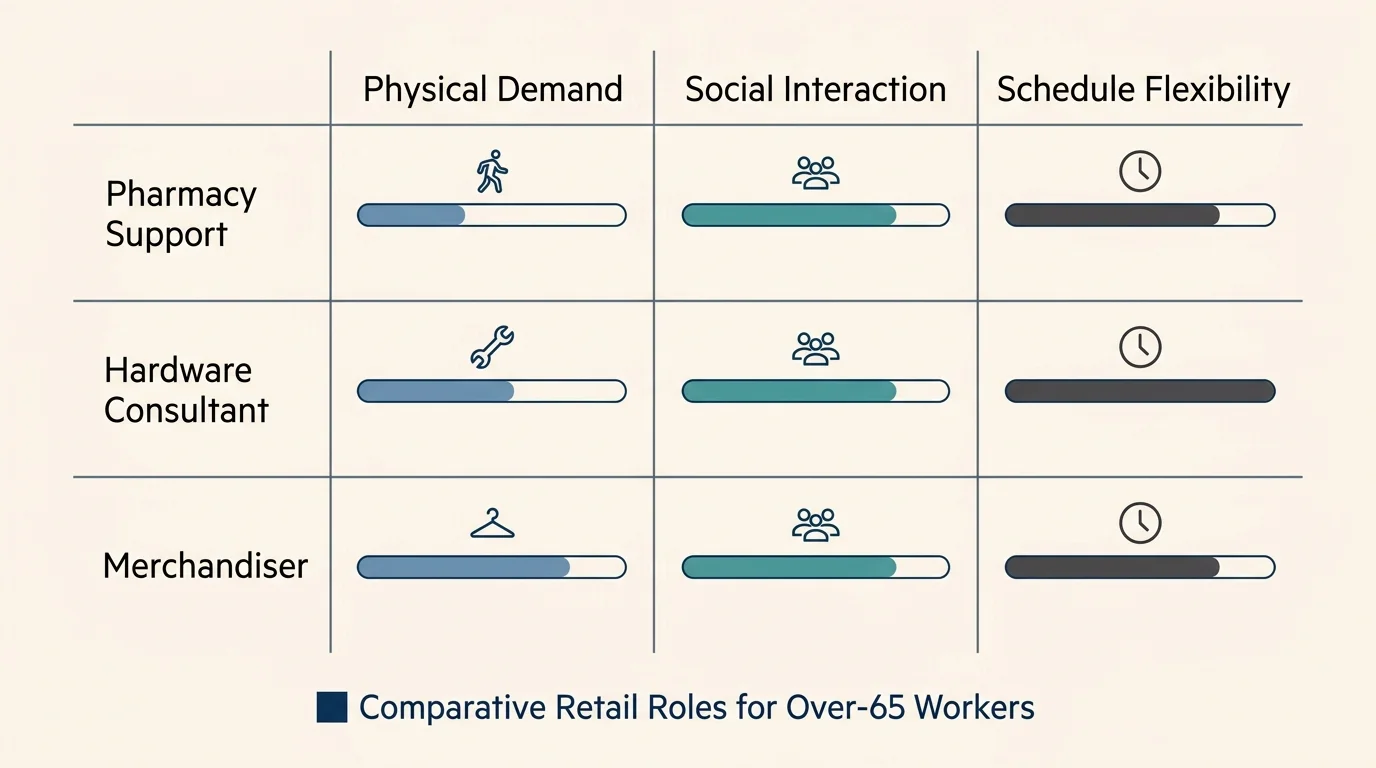

Comparing Popular Retail Roles for Retirees

Not all retail jobs demand the same level of physical exertion. When applying, it helps to match the specific duties of a role to your personal comfort level, stamina, and physical mobility.

| Retail Role | Physical Demand | Customer Interaction | Best Fit For… |

|---|---|---|---|

| Store Greeter | Low to Medium (Requires standing, but little lifting) | Very High | Social butterflies who enjoy welcoming people and answering basic directional questions. |

| Cashier | Medium (Standing in one place, repetitive motion) | High | Detail-oriented individuals comfortable handling transactions and operating basic software. |

| Merchandiser / Stocker | High (Lifting, bending, walking long distances) | Low | Active seniors looking to get paid while getting a workout, who prefer working independently. |

| Specialty Consultant (e.g., Hardware, Beauty) | Medium (Walking the floor, demonstrating products) | High | Former professionals or hobbyists who want to share their specific lifetime expertise. |

| Pharmacy Clerk | Medium (Standing, organizing small items) | Medium | Organized individuals who respect patient privacy and can handle detail-oriented administrative tasks. |

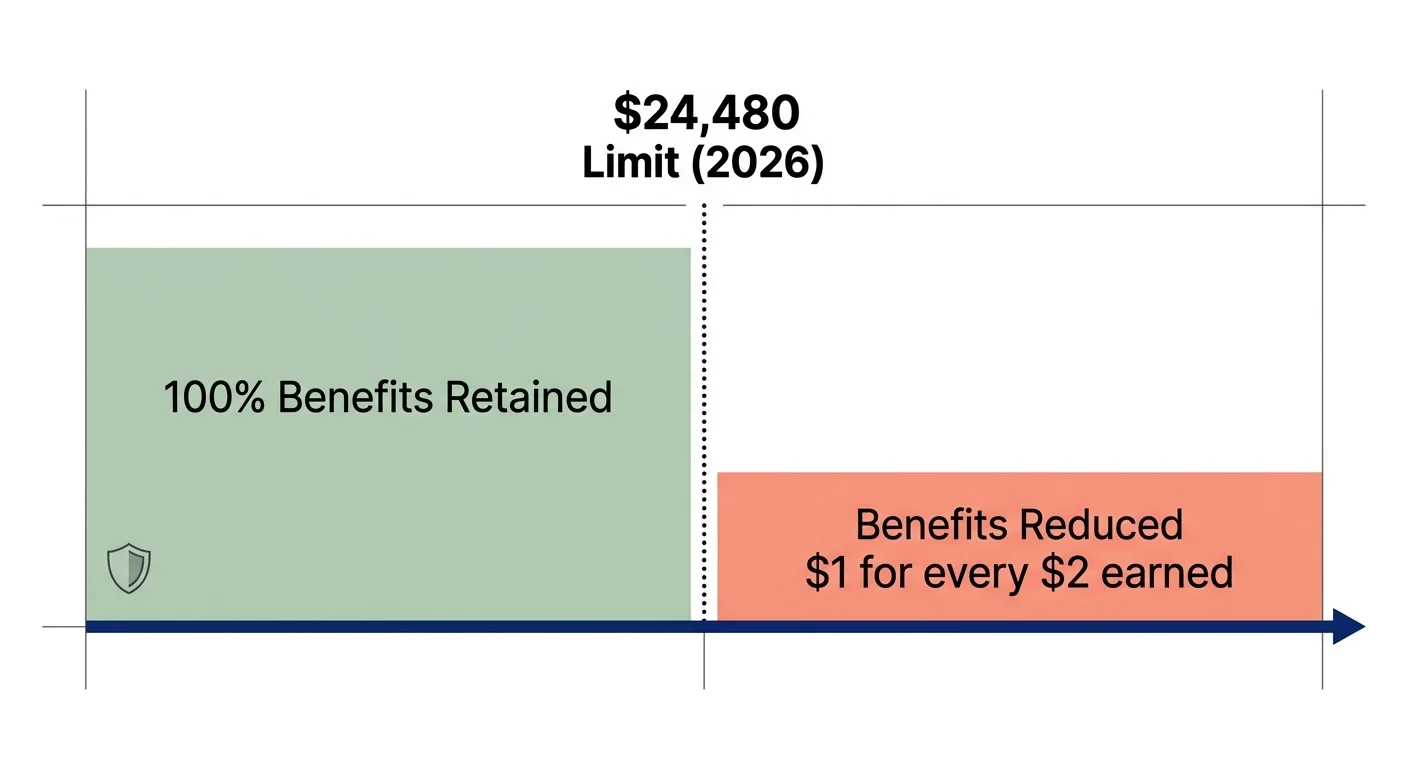

How Your Retail Wages Affect Social Security in 2026

The most common anxiety older adults face when returning to work is the fear of losing their Social Security benefits. If you claim Social Security before reaching your Full Retirement Age (FRA), the Social Security Administration (SSA) applies an earnings limit. Fortunately, these limits are adjusted annually for inflation.

According to the SSA (2026), here is exactly how the earnings limit impacts your take-home pay based on your age:

- Under Full Retirement Age for the Entire Year: The 2026 earnings limit is $24,480. If you earn more than this amount from your retail job, the SSA will withhold $1 in benefits for every $2 you earn above the limit.

- The Year You Reach Full Retirement Age: The rules loosen significantly in the calendar year you hit your FRA. The limit jumps to $65,160 for 2026. Furthermore, this limit only applies to the months prior to your birthday. If you exceed this generous cap, the SSA withholds $1 for every $3 earned above the limit.

- After Full Retirement Age: Once you reach your exact birth month for your FRA, the earnings limit disappears entirely. You can earn $10,000 or $100,000 at your job, and your Social Security checks will not be reduced by a single penny.

It is critical to understand that withheld benefits are not permanently lost. If the SSA reduces your checks because you earned too much at your part-time job, they will recalculate your monthly benefit amount once you reach Full Retirement Age, gradually paying you back those withheld funds over your remaining lifetime.

Understanding Your 2026 Tax Deductions

Taking on a retail job means generating taxable earned income. Fortunately, the tax code provides significant buffers for older adults, allowing you to earn a healthy part-time wage before owing federal income tax.

For the 2026 tax year, the Internal Revenue Service (IRS) increased the standard deduction to $16,100 for single filers and $32,200 for married couples filing jointly. However, seniors receive a built-in advantage.

If you are 65 or older, you qualify for an additional standard deduction. In 2026, this extra amount is $2,050 for single filers and heads of household. For married couples filing jointly, it is $1,650 per qualifying spouse. This means a single 65-year-old taking the standard deduction can shield $18,150 of income from federal taxes right out of the gate.

Additionally, qualifying older adults may benefit from the temporary $6,000 senior bonus deduction active through 2028, which further drastically reduces your taxable burden. Between these deductions, a part-time retail wage of $15 to $20 an hour for 20 hours a week often results in very little to zero federal income tax liability.

“The biggest risk to your retirement isn’t the stock market—it’s taxes. When you take on part-time work, you must map out how those wages impact your broader financial picture.” — Ed Slott, CPA and Retirement Expert

Pitfalls to Watch For

Even with great corporate programs and favorable tax deductions, working a retail job in your late 60s or 70s requires careful navigation. Avoid these common missteps:

- Ignoring the Physical Toll: Concrete store floors are notoriously unforgiving on aging joints. Never assume you can stand for four hours straight without pain just because you stay active at home. Negotiate for roles that allow intermittent sitting, request an anti-fatigue mat for your workstation, and invest heavily in high-quality, supportive footwear.

- Failing to Report Income Estimates to the SSA: If you are under your Full Retirement Age and expect to exceed the $24,480 earnings limit in 2026, you must proactively inform the SSA. If you wait until tax season for them to discover your extra wages, they will demand a lump-sum repayment of the benefits they overpaid you, which can severely disrupt your cash flow.

- Overlooking Hidden Costs of Employment: Some grocery chains and large retailers require employees to join a union, which means union dues will be automatically deducted from your paycheck. Factor in the cost of commuting, uniform requirements, and specialized shoes when calculating whether a $15-an-hour job is actually worth your time.

- Triggering Higher Medicare Premiums: If your combined income (including half of your Social Security, your retail wages, and retirement account withdrawals) pushes you over specific IRS thresholds, you could trigger the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge increases your Medicare Part B and Part D premiums. Keep a close eye on your total modified adjusted gross income.

Getting Expert Help

While picking up a part-time shift might seem straightforward, the ripple effects on your financial ecosystem can be complex. You should seriously consider speaking with a fiduciary financial advisor or a licensed CPA if:

- You are attempting to balance a new part-time retail salary with mandatory Required Minimum Distributions (RMDs) from your traditional IRA or 401(k).

- You are receiving spousal or survivor Social Security benefits, as the earnings limit rules can affect these distributions differently than benefits drawn on your own work record.

- You rely on Medicaid, housing assistance, or ACA health insurance subsidies, as even a small bump in earned income could push you over strict eligibility cliffs for these vital programs.

Frequently Asked Questions

Will a part-time retail job provide health insurance?

While a few select retailers (such as Costco and Starbucks) offer health benefits to part-time workers, the vast majority do not. Most workers over 65 rely on Medicare for their primary health coverage. If you are not yet 65, you will need to rely on the ACA marketplace, COBRA, or a spouse’s plan.

Can I lose my pension if I start working in retail?

Generally, no. Your pension from a previous career (such as teaching, manufacturing, or corporate management) is entirely disconnected from a new retail job. The only time a pension is typically jeopardized is if you return to work for the exact same employer or union system that pays your pension.

How many hours per week is considered part-time?

In the retail sector, part-time work usually ranges between 15 and 28 hours per week. During the interview process, be explicitly clear about your maximum availability. Retail managers value predictability, so telling them upfront that you will only work Tuesdays, Thursdays, and Saturday mornings is better than accepting a fluid schedule that leaves you exhausted.

Entering the retail workforce as an older adult is an excellent way to maintain a sharp mind, engage with your community, and pad your savings account. By choosing the right employer and understanding the 2026 tax and benefit rules, you can transform a simple part-time job into a highly rewarding phase of your retirement. The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.