Your transition into retirement requires an entirely new set of financial and personal tools, replacing the saving habits you spent decades perfecting. You must now learn how to safely spend your nest egg, navigate complex government benefits, and protect your identity in an increasingly digital world. Many retirees mistakenly believe that stopping work means an end to learning, but personal growth becomes even more critical when managing fixed incomes and evolving healthcare costs. Mastering these abilities ensures your money lasts and your lifestyle remains fulfilling. By updating your approach to taxes, budgeting, and retirement hobbies, you can build a resilient strategy that turns your golden years into a period of confidence rather than financial anxiety.

1. Mastering the Shift from Saving to Spending

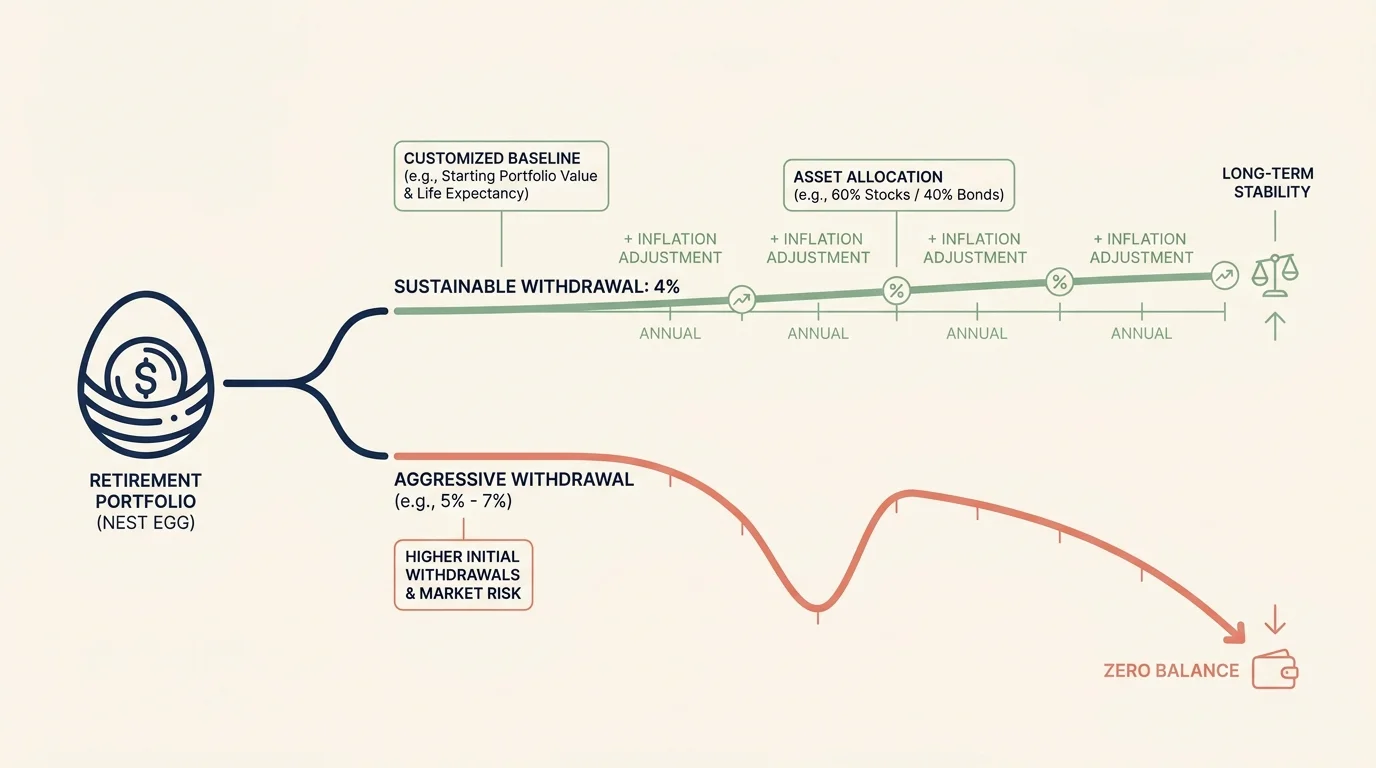

For decades, you focused on accumulating wealth by saving a portion of every paycheck, maximizing matching contributions, and watching your balances grow over time. Transitioning into the decumulation phase requires a complete psychological reversal. You must learn how to confidently withdraw from your nest egg without depleting it too early.

Creating a sustainable withdrawal strategy often starts with evaluating your asset allocation. If you withdraw too conservatively, you might artificially restrict your lifestyle; if you withdraw too aggressively, you risk outliving your resources. A common starting point is the 4 percent rule, which suggests withdrawing 4 percent of your portfolio in your first year of retirement and adjusting for inflation annually. However, you should customize this baseline to fit your specific health needs, longevity expectations, and market conditions.

To safely manage this shift, track your essential expenses against your guaranteed income sources. If your Social Security and pension cover your baseline living costs, your investment withdrawals can fund discretionary spending. Utilizing free tools from Investor.gov can help you calculate sustainable withdrawal rates over a long-term time horizon.

2. Budgeting for Your New Healthcare Reality

Healthcare costs typically represent one of the largest expenses for retirees, and navigating Medicare requires active management. Unlike employer-sponsored health insurance, Medicare features fluctuating premiums, out-of-pocket limits, and annual plan changes that demand your attention every fall.

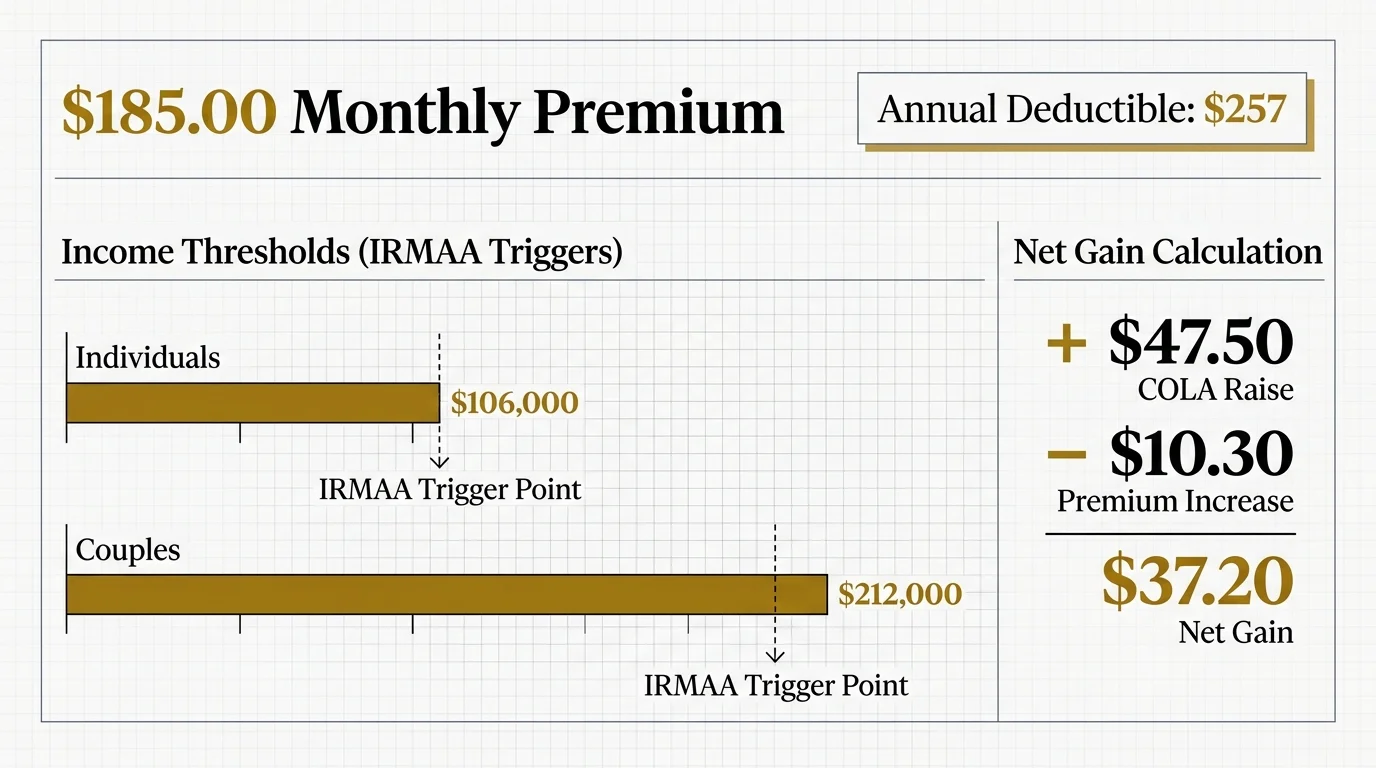

You must factor these evolving costs into your monthly budget. According to the Centers for Medicare and Medicaid Services, the standard Medicare Part B premium in 2025 is $185.00 per month, accompanied by an annual deductible of $257. If your modified adjusted gross income from two years prior exceeded $106,000 as an individual or $212,000 as a married couple filing jointly, you will also face an Income-Related Monthly Adjustment Amount (IRMAA), which significantly increases your monthly premium.

Social Security cost-of-living adjustments (COLAs) help offset some of these increases, but the math requires close monitoring. For example, if your monthly benefit is $1,900, the 2.5 percent COLA applied in 2025 adds $47.50 to your check. However, the $10.30 increase in the standard Part B premium absorbs a portion of that raise before the money ever reaches your bank account. You can verify your specific benefit amounts and Medicare deductions by logging into your official account at SSA.gov.

To help you understand your coverage options, compare the two main paths for Medicare enrollment:

| Feature | Original Medicare (Parts A & B) + Medigap | Medicare Advantage (Part C) |

|---|---|---|

| Provider Network | See any doctor or hospital in the U.S. that accepts Medicare. | Restricted to an HMO or PPO network. |

| Out-of-Pocket Limits | No limit unless paired with a Medigap policy. | Includes a built-in annual out-of-pocket maximum. |

| Prescription Drugs | Requires a standalone Part D plan. | Usually included in the plan. |

| Premium Costs | Higher monthly premiums for comprehensive Medigap coverage. | Often features lower or zero-dollar premiums, but higher copays. |

3. Optimizing Taxes on a Fixed Income

Many seniors mistakenly assume their tax obligations disappear once they stop working. In reality, retirement introduces a complex web of taxable and non-taxable income streams. Relearning how to manage your tax brackets can save you thousands of dollars annually.

First, understand how the IRS treats your benefits. Depending on your combined income, which includes half of your Social Security benefits plus your other taxable income, up to 85 percent of your Social Security payments may be subject to federal income tax. Furthermore, withdrawals from traditional IRAs and 401(k)s are taxed as ordinary income, while withdrawals from Roth accounts remain completely tax-free.

You should also take advantage of tax provisions designed specifically for retirees. For the 2025 tax year, the IRS provides an additional standard deduction for taxpayers age 65 and older. For single filers in 2025, the base standard deduction of $15,750 is boosted by an additional $2,000, bringing the total standard deduction to $17,750. Married couples filing jointly receive an extra $1,600 per qualifying spouse. Because these figures adjust periodically, check IRS.gov for the most current brackets before you file.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

4. Protecting Assets with Digital Fluency

Managing finances in the modern era requires comfort with online portals, mobile banking, and digital security. While you may have relied on paper statements during your working years, mastering digital tools provides real-time oversight of your accounts and helps prevent fraud.

Scammers aggressively target retirees, making cybersecurity a mandatory skill. You must learn to spot phishing emails, secure your devices with two-factor authentication, and monitor your credit reports for suspicious activity. Setting up your official online accounts for Social Security and Medicare before a fraudster attempts to claim them in your name serves as a critical defensive strategy.

5. Transforming Retirement Hobbies into Purpose

Leaving the workforce can sometimes create a void in your daily routine. Many seniors are relearning how to structure their time by transforming retirement hobbies into structured, meaningful pursuits. This focus on personal growth prevents boredom and can even provide supplemental income to stretch your savings further.

Whether you enjoy woodworking, gardening, consulting, or writing, the modern economy offers accessible ways to monetize your passions. Selling crafts online, tutoring local students, or turning a lifelong skill into a part-time consulting role provides financial breathing room while keeping your mind sharp. If you prefer to volunteer without financial compensation, programs organized by the Administration for Community Living (ACL) connect older adults with community service opportunities that foster deep social connections.

6. Embracing Continuous Senior Learning

Intellectual stagnation is one of the hidden risks of retirement. To maintain cognitive health and adapt to a changing world, successful retirees embrace continuous senior learning as a core lifestyle habit rather than a chore.

You do not need to enroll in a formal degree program to benefit from continuing education. Many state universities and community colleges offer free or heavily discounted auditing programs for residents over age 60. Taking courses in history, foreign languages, or technology keeps your brain engaged and introduces you to new social circles. Expanding your knowledge base ensures you remain adaptable, interesting, and mentally resilient throughout your later years.

7. Adapting Your Lifestyle for Long-Term Fulfillment

Your housing and daily routines must evolve alongside your physical and financial needs. Reevaluating your lifestyle allows you to cut unnecessary expenses and redirect funds toward activities that bring genuine joy.

For many retirees, adapting means downsizing to a more manageable property or modifying an existing home to support aging in place safely. Lowering your utility bills, reducing property taxes, and eliminating the physical burden of extensive home maintenance frees up both time and money. Focus on building a lifestyle that prioritizes health, mobility, and proximity to supportive community resources over the accumulation of material possessions.

Pitfalls to Watch For

Even the most careful planners can stumble when adapting to retirement. Avoid these common missteps as you relearn how to manage your finances and time:

- Ignoring Required Minimum Distributions (RMDs): Once you reach the IRS-mandated age, you must withdraw a minimum amount from your tax-deferred retirement accounts each year. Failing to take these distributions results in steep penalty taxes on the amount not withdrawn.

- Overlooking State-Specific Tax Rules: While federal tax rules apply universally, state taxation of pensions, Social Security, and property varies wildly. Do not assume your current state remains the most tax-friendly option for your fixed income.

- Delaying Medicare Enrollment: If you do not sign up for Medicare Part B when you first become eligible, and you do not have qualifying employer coverage, you will face a permanent late enrollment penalty that increases your monthly premium for the rest of your life.

- Falling Victim to the Early Spending Surge: Many seniors overspend during the first few years of retirement on travel and large purchases. Pace yourself to ensure your portfolio can survive the later, potentially more expensive years when health needs typically rise.

Getting Expert Help

Managing the complexities of retirement often requires a team approach. Consider seeking professional guidance in the following scenarios:

- Navigating Social Security Timing: A fee-only financial planner can analyze your life expectancy, marital status, and portfolio to determine the exact age you should claim benefits to maximize your lifetime payout.

- Evaluating Medicare Plans: The State Health Insurance Assistance Program (SHIP) offers free, unbiased counseling to help you navigate Medicare choices and find a plan that covers your specific prescription drugs and preferred doctors.

- Managing Complex Tax Liabilities: If you are planning large Roth conversions or selling a significant asset, a Certified Public Accountant (CPA) can help you sequence these events to avoid triggering IRMAA surcharges or pushing yourself into higher tax brackets.

Frequently Asked Questions

Do I have to pay taxes on my Social Security benefits?

It depends on your combined income. If your combined income, which is your adjusted gross income plus nontaxable interest plus half of your Social Security benefits, exceeds $25,000 for an individual or $32,000 for a married couple filing jointly, a portion of your benefits will be subject to federal income tax.

What is the standard deduction for someone over 65?

For the 2025 tax year, the IRS provides an additional standard deduction of $2,000 for single filers age 65 and older, bringing the total standard deduction to $17,750. Married couples filing jointly receive an extra $1,600 per qualifying spouse. These numbers adjust annually to account for inflation.

How can I protect my retirement savings from inflation?

Maintaining a diversified portfolio that includes a mix of equities and inflation-protected assets provides long-term growth potential. Additionally, relying on inflation-adjusted income sources like Social Security helps preserve your purchasing power as living costs rise over time.

Learning these new skills takes time, but every small adjustment builds a more secure foundation for your future. Stay engaged, keep your mind open to new financial strategies, and do not hesitate to lean on community resources when you need support. Relearning how to live fully on a fixed income empowers you to stop worrying about money and start enjoying the lifestyle you worked so hard to achieve. The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: May 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.