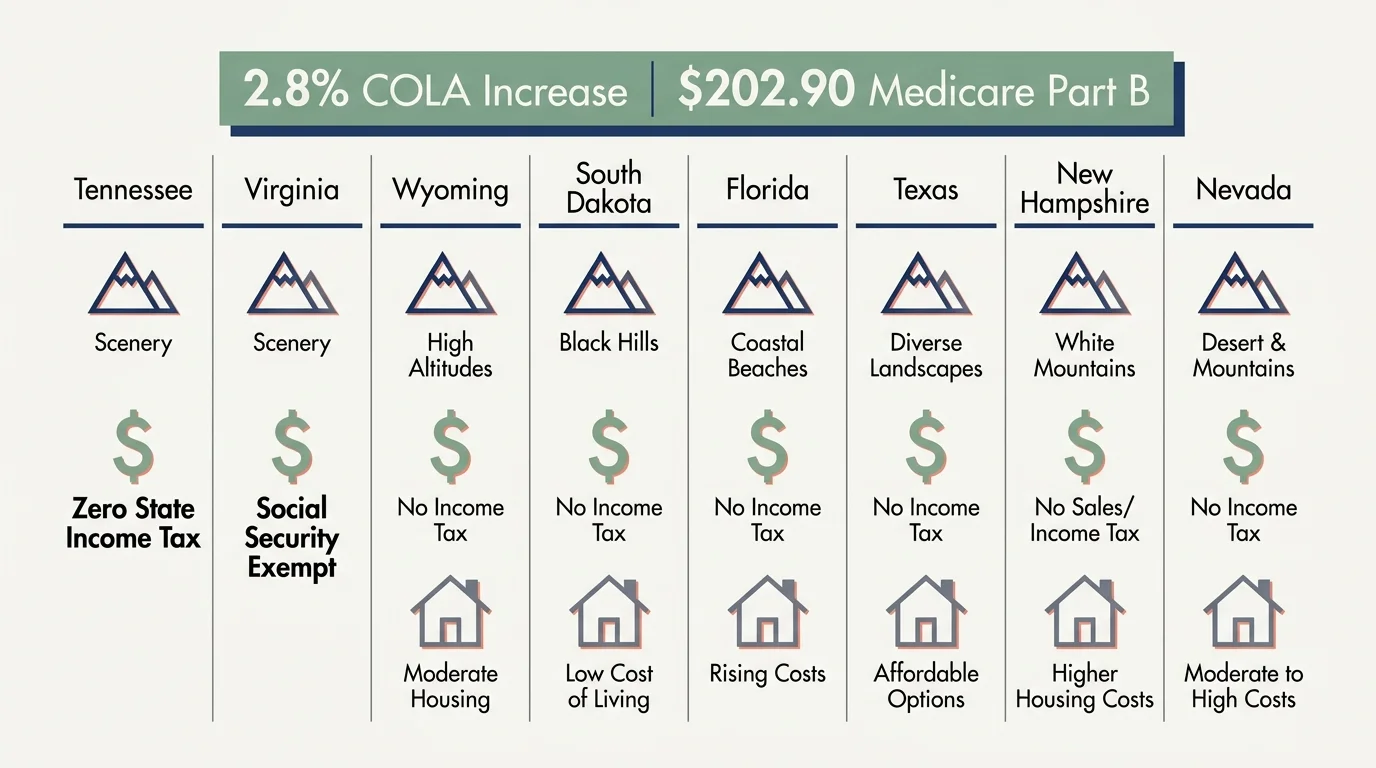

Trading your morning commute for coffee overlooking a sun-drenched mountain range is the ultimate retirement dream. Finding a scenic destination that won’t drain your savings requires more than just picking a spot on a map. With the 2026 Social Security cost-of-living adjustment adding a modest 2.8% to monthly checks and standard Medicare Part B premiums rising to $202.90, stretching your retirement dollar is critical. The good news is you don’t have to choose between breathtaking scenery and financial stability. By strategically relocating to states with favorable tax rules, affordable housing, and lower living costs, you can wake up to majestic peaks every single day without outliving your nest egg.

1. Chattanooga, Tennessee: Appalachian Charm with Zero State Income Tax

Nestled in the foothills of the Appalachian Mountains and perched along the Tennessee River, Chattanooga provides a stunning natural backdrop without the resort-town price tag. The “Scenic City” surrounds you with lush ridges and offers miles of accessible walking trails right in the downtown corridor.

From a financial standpoint, Tennessee is incredibly friendly to retirees. The state levies zero income tax, meaning your Social Security, pension distributions, and 401(k) withdrawals stay entirely in your pocket. Furthermore, the local real estate market remains accessible. In early 2026, the median home sales price in Chattanooga sat around $330,000, making it feasible to secure a property with a view without carrying a heavy mortgage into retirement.

Chattanooga is also famous for its municipal broadband network, offering some of the fastest internet in the country. If you plan to consult, run a small business, or simply want reliable video calls with your grandchildren, the infrastructure here is unmatched.

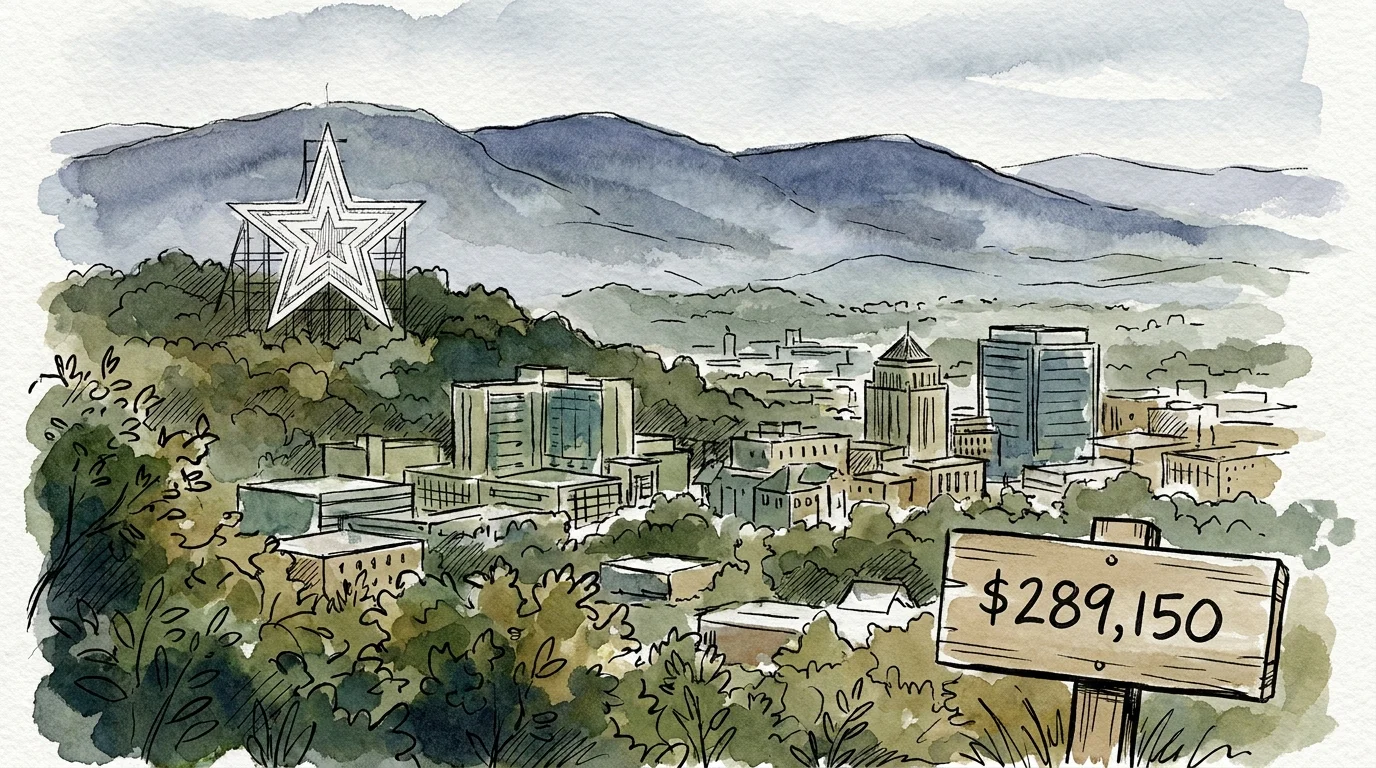

2. Roanoke, Virginia: Blue Ridge Beauty on a Budget

If you prefer the rolling, mist-covered peaks of the Blue Ridge Mountains, Roanoke offers a dense cultural scene wrapped in natural beauty. The iconic Roanoke Star overlooks a valley rich with museums, performing arts centers, and top-tier medical facilities like the Carilion Clinic.

Virginia treats retirees well by completely exempting Social Security benefits from state income taxation. While Virginia does tax other forms of retirement income, the cost of housing in Roanoke makes it a compelling financial choice. In early 2026, the median home sale price in Roanoke hovered around $289,150. Because housing costs are often the largest line item in a retirement budget, securing a home well below the national average frees up your cash flow for travel, hobbies, and healthcare.

3. Hendersonville, North Carolina: Mild Climates and Friendly Taxes

Just south of the busy tourist hub of Asheville, Hendersonville offers the same spectacular Appalachian views and temperate four-season climate with a more relaxed, community-focused pace. The downtown area features wide, walkable sidewalks lined with cafes and boutiques, perfect for a leisurely afternoon.

North Carolina recently transitioned to a flat income tax rate, simplifying the tax planning process. Even better, the state does not tax Social Security benefits. While you will pay state income tax on traditional IRA and 401(k) withdrawals, the overall property tax rates in Henderson County remain relatively low. This balance makes Hendersonville a practical choice for seniors who want the mountain lifestyle without the extreme winter weather found further north.

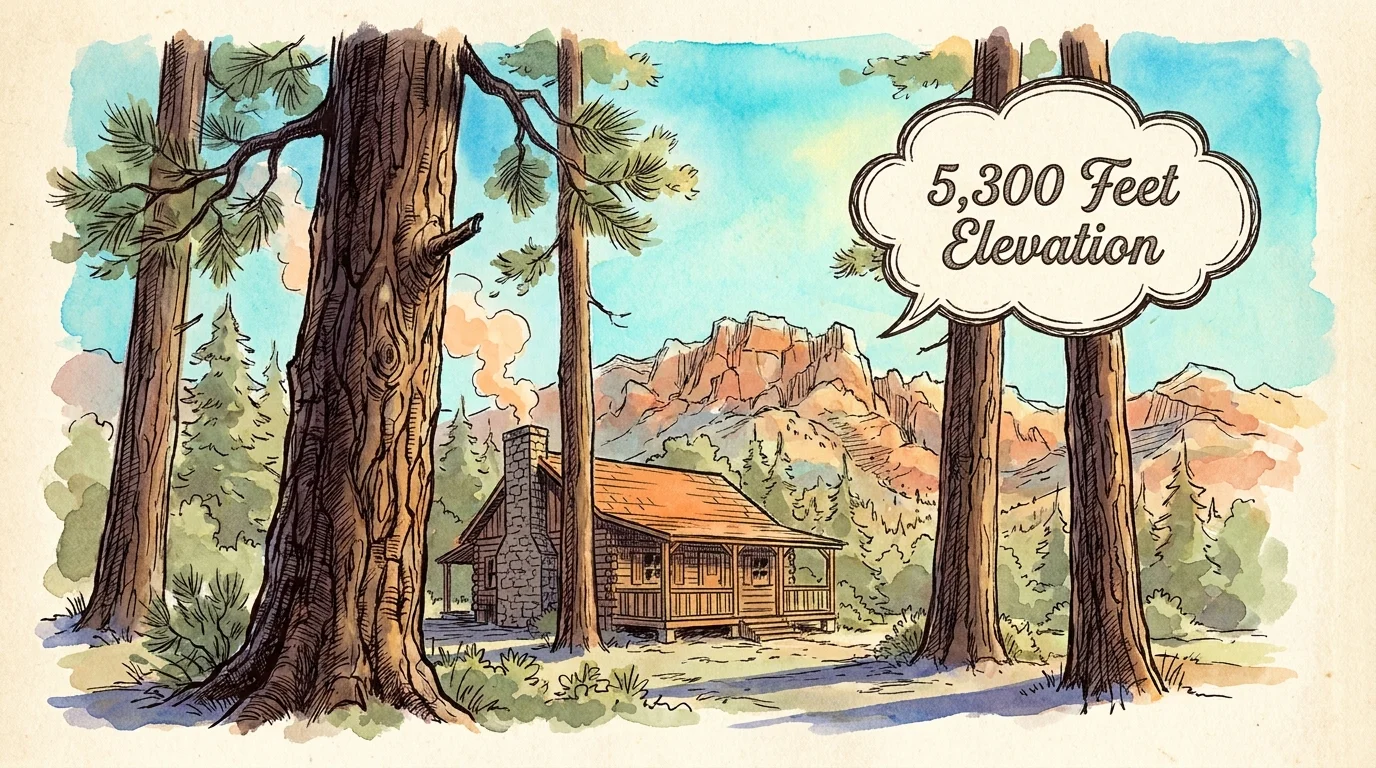

4. Prescott, Arizona: Mile-High Living Without the Social Security Tax

When you hear Arizona, you might picture scorching deserts. Prescott, however, sits at an elevation of 5,300 feet in the Bradshaw Mountains, offering four distinct but mild seasons. You get the crisp mountain air and pine forests without the relentless, heavy snowfall common in the Rockies.

Arizona is a haven for retirees looking to protect their fixed income. The state does not tax Social Security benefits and applies a very low flat income tax rate of 2.5% to other forms of income. Additionally, property taxes in Arizona are generally lower than the national average. While home prices in Prescott have risen as the town’s popularity has grown, the long-term tax savings on your retirement income can help offset a slightly higher initial housing cost.

5. Taos, New Mexico: High Desert Peaks and Retiree Tax Exemptions

Surrounded by the awe-inspiring Sangre de Cristo Mountains, Taos provides a unique blend of high-desert scenery, rich Native American history, and a vibrant arts community. It is a town that feels entirely different from a typical retirement community, appealing to those who want an eclectic and culturally immersive environment.

New Mexico has worked hard to attract seniors by restructuring its tax laws. For 2026, the state fully exempts Social Security income for single taxpayers with an adjusted gross income under $100,000, and for married couples filing jointly with an income under $150,000. If your income falls below these thresholds, your Social Security checks remain entirely yours. Property taxes across New Mexico are also notably low, ensuring your ongoing housing costs stay manageable.

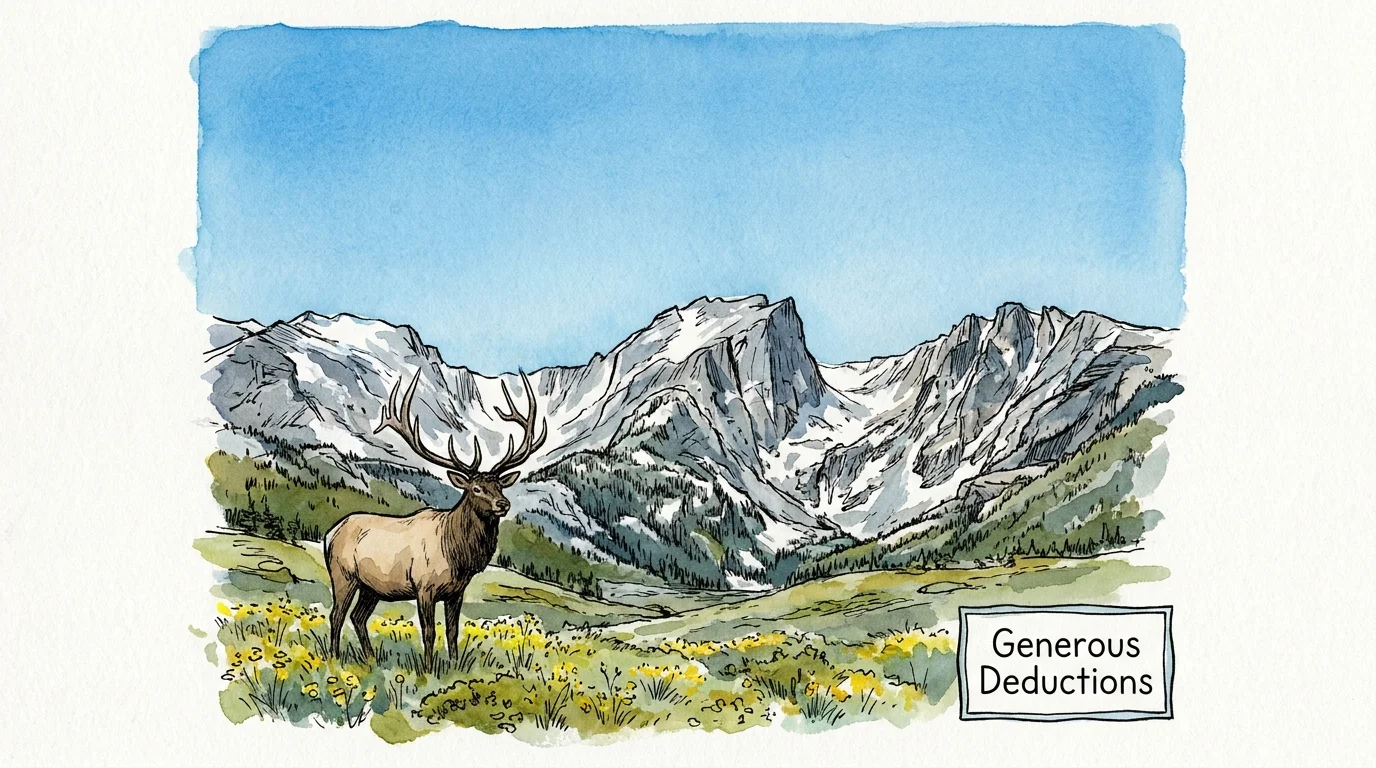

6. Estes Park, Colorado: Rocky Mountain Majesty with Generous Deductions

Serving as the basecamp for Rocky Mountain National Park, Estes Park delivers the dramatic, snow-capped peaks that adorn postcards. Elk freely wander through town, and the outdoor recreation opportunities are practically endless.

Because it is a highly desirable resort destination, home prices here are elevated. However, Colorado offsets some of this expense through highly favorable retiree tax policies. The state levies a flat income tax rate of 4.4%. More importantly, Colorado allows residents aged 65 and older to deduct up to $24,000 of qualifying retirement income per year—including Social Security, pensions, and IRA distributions. If you and your spouse are both over 65, you can shelter up to $48,000 of your combined retirement income from state taxes, providing significant annual relief.

7. Coeur d’Alene, Idaho: Lakeside Peaks in a Tax-Friendly Haven

Coeur d’Alene pairs the rugged beauty of the Bitterroot Mountains with the stunning expanse of Lake Coeur d’Alene. It is an outdoor lover’s paradise, offering world-class golfing, boating, and hiking right in your backyard.

Idaho stands out as a fiscally conservative state that treats its senior population favorably. The state does not tax Social Security benefits, preserving a significant portion of your baseline retirement income. While Idaho does tax other forms of retirement income, it offers a grocery tax credit to help offset the sales tax applied to food, helping you manage day-to-day living expenses more effectively.

8. Whitefish, Montana: Glacier Gateway with No Sales Tax

Located near Glacier National Park, Whitefish is a premier mountain town offering pristine lakes, dense forests, and towering peaks. It provides a robust, active lifestyle for retirees who want to spend their golden years skiing, fishing, and exploring.

Montana’s tax structure requires careful planning, but it offers a massive benefit: zero state sales tax. Every purchase you make—from a new vehicle to daily groceries—costs exactly what is on the price tag. Montana does partially tax Social Security benefits following federal inclusion rules, and its top state income tax rate sits at 5.9%. However, the absence of a sales tax can result in thousands of dollars of savings annually, particularly in years when you make large purchases like appliances or a retirement vehicle.

At a Glance: State Tax Rules for Our Mountain Towns

When comparing these locations, use this table to quickly assess how state laws will impact your fixed income. Always verify your specific tax situation with the Internal Revenue Service (IRS) and a local tax professional.

| Town & State | State Taxes Social Security? | Key Tax Benefit for Seniors |

|---|---|---|

| Chattanooga, TN | No | Zero state income tax overall. |

| Roanoke, VA | No | No tax on Social Security. |

| Hendersonville, NC | No | Flat income tax rate dropping annually. |

| Prescott, AZ | No | Low 2.5% flat state income tax. |

| Taos, NM | No (Income limits apply) | SS exempt for couples earning under $150k. |

| Estes Park, CO | Yes (Partially) | $24,000 retirement income deduction for ages 65+. |

| Coeur d’Alene, ID | No | No tax on Social Security; grocery tax credits available. |

| Whitefish, MT | Yes (Partially) | Zero state sales tax. |

“Taxes will be the single biggest factor that separates people from their retirement dreams.” — Ed Slott, CPA and Retirement Expert

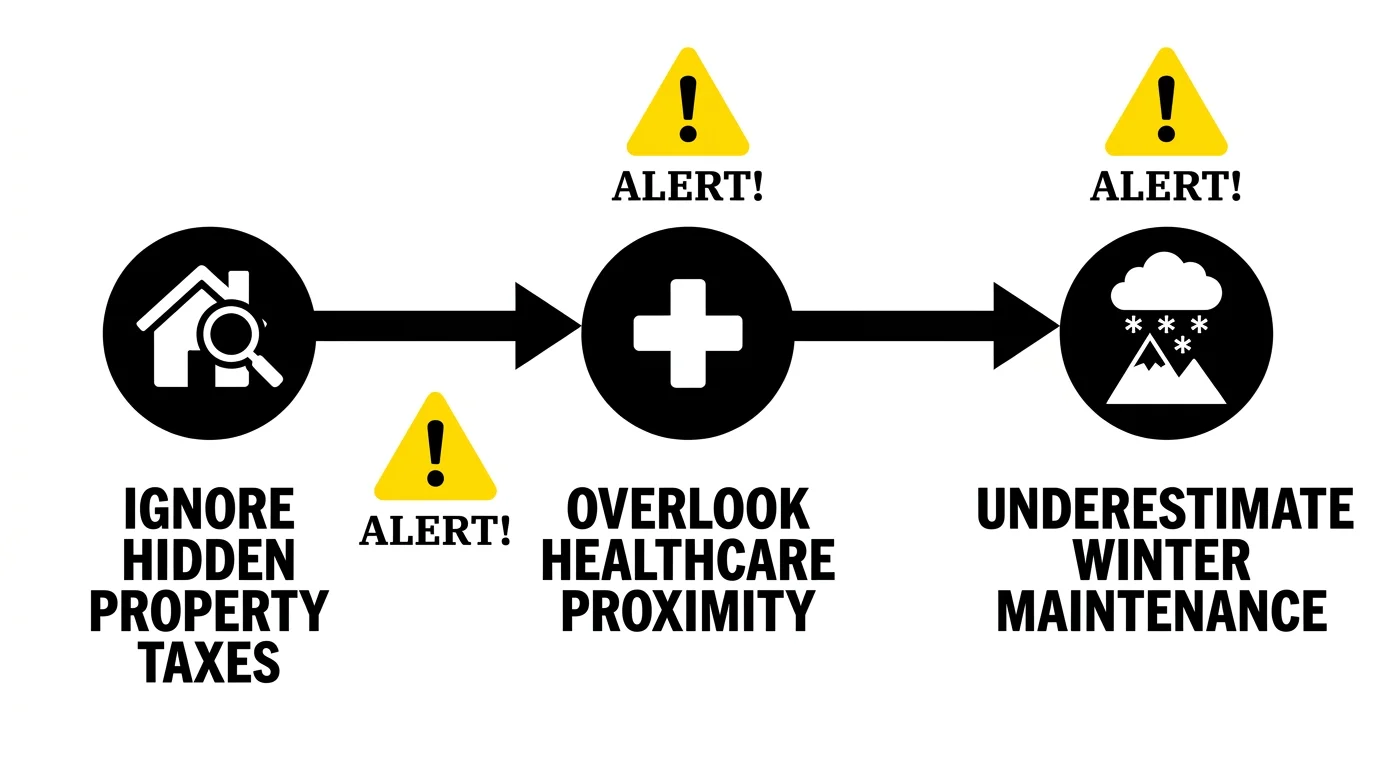

Costly Errors to Sidestep When Relocating

Moving across state lines in retirement introduces a host of financial variables. Avoid these common traps to ensure your mountain view doesn’t come with hidden financial stress.

- Forgetting Medicare Network Restrictions: If you use a Medicare Advantage plan (Part C), your coverage is strictly regional. Moving to a new county or state means you must enroll in a new plan, or switch back to Original Medicare. Check the Medicare.gov plan finder tool before moving to ensure your new town has robust healthcare options in your network.

- Focusing Only on Income Tax: States have to generate revenue somehow. A state with zero income tax might have high property taxes or sales taxes. Always calculate your “total tax burden” rather than just looking at the income tax rate.

- Underestimating Mountain Living Costs: Living at a higher elevation involves expenses you might not face in the suburbs. Factor in the costs of heavier winter clothing, snow tires, potential four-wheel-drive vehicles, snow removal services, and higher home heating bills.

- Ignoring Healthcare Proximity: A remote cabin on a ridgeline sounds idyllic, but a 45-minute drive to the nearest hospital is a serious risk as you age. Prioritize towns like Roanoke or Chattanooga that integrate natural beauty with immediate access to top-tier medical facilities. You can use the Eldercare Locator to research supportive services in your prospective new community.

Frequently Asked Questions

Do I have to notify Social Security if I move to a new state?

Yes. You must update your address with the Social Security Administration (SSA) to ensure your tax forms (like the SSA-1099) arrive safely and your Medicare records remain accurate. You can easily update this through your personal “my Social Security” account online.

Will moving to a new state change my federal Social Security tax?

No. The IRS applies federal taxes to your Social Security benefits based on your “combined income,” regardless of where you live in the United States. State taxes vary, but your federal obligation remains consistent nationwide.

How do I handle my 2026 Medicare Part B premiums when relocating?

Your standard Medicare Part B premium—set at $202.90 for 2026—is a federal baseline and does not change based on your ZIP code. However, if you are moving and enrolling in a new Medicare Advantage or Part D prescription drug plan, those specific supplemental plan premiums will vary based on your new location.

Relocating in retirement is one of the most exciting chapters of your life. By running the numbers on state taxes, housing costs, and healthcare access, you ensure your new mountain home serves as a source of peace, not financial anxiety. Take the time to visit these towns during their off-seasons, talk to local retirees, and consult a tax professional to see how your specific financial picture aligns with the local economy.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.