Retiring before age 65 offers incredible freedom, but it comes with a massive financial hurdle: bridging the health insurance gap before Medicare kicks in. Without employer-sponsored coverage or Medicare eligibility, early retirees often face staggering medical costs. Navigating the open market can feel overwhelming, especially with fluctuating premiums and changing tax subsidy rules. You need a clear, actionable plan to protect both your health and your hard-earned life savings. Whether you are weighing Affordable Care Act options, evaluating short-term COBRA plans, or strategizing with a Health Savings Account, finding the best coverage requires looking closely at your monthly budget. Here is exactly what you need to know to secure affordable, comprehensive health insurance for your early retirement years.

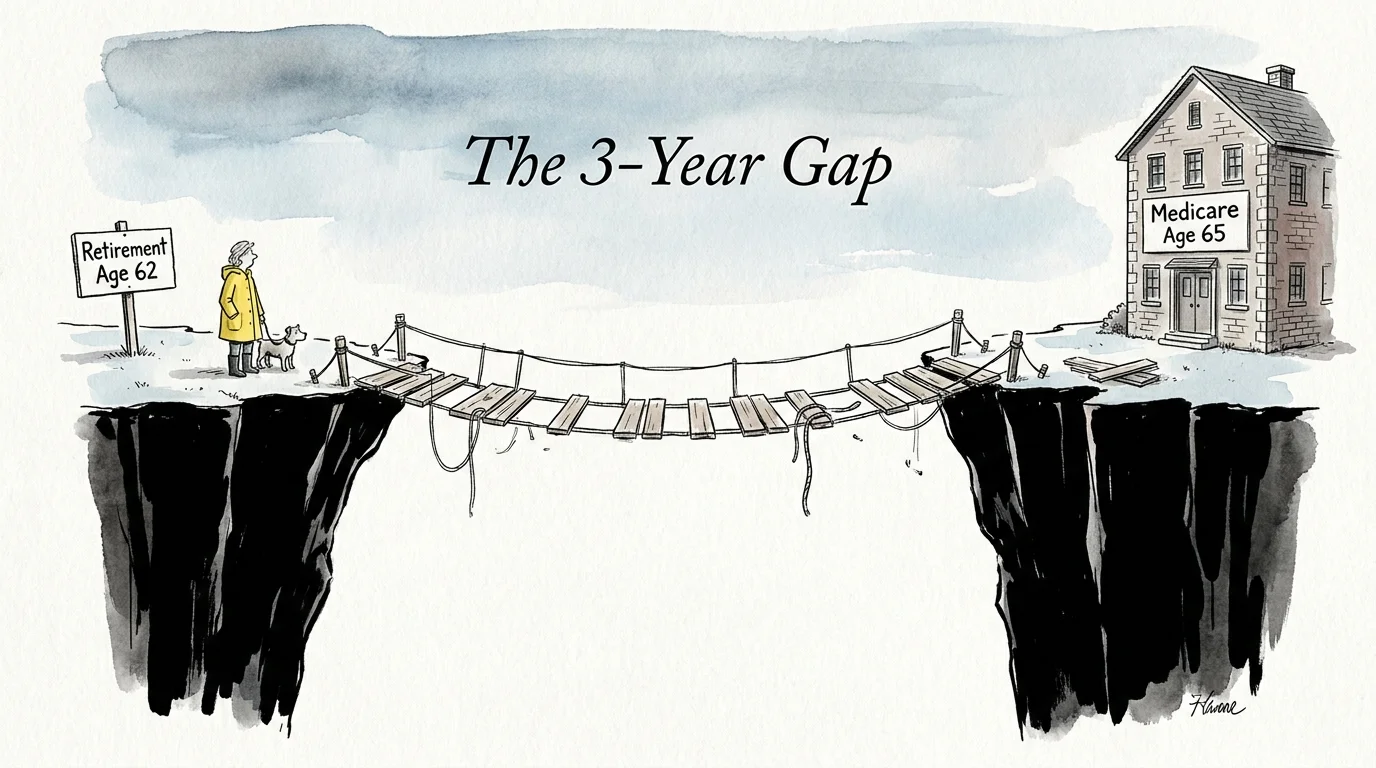

The Pre-Medicare Healthcare Gap

Walking away from your career means walking away from the group health insurance rates negotiated by your employer. For many Americans, this transition is the most expensive shock of early retirement. You become responsible for the full premium, the deductible, and the network management.

A common misconception derails many retirement plans: assuming that claiming early Social Security benefits at age 62 automatically qualifies you for health benefits. It does not. While you can log into the Social Security Administration portal and start collecting a monthly check at 62, Medicare eligibility strictly begins at age 65 for the vast majority of Americans. This leaves a mandatory three-year gap—longer if you retire in your fifties—where you must find private coverage.

“If you want to have a healthy retirement, there’s a big wild card you need to be prepared for: health care expenses. A 65-year-old couple will need an estimated $260,000 to pay for unreimbursed medical expenses through retirement.” — Jean Chatzky, Financial Editor and Author

Healthcare inflation consistently outpaces general inflation. Insurers price their policies based on risk, and older adults naturally require more medical interventions. Federal regulations permit health insurance companies to charge older adults up to three times the premium rate of a 21-year-old. Without proper planning, this age-rating multiplier can easily consume your early retirement budget.

Navigating the Affordable Care Act (ACA) Marketplace

The Affordable Care Act (ACA) remains the primary safety net for early retirees. Available through HealthCare.gov or your specific state exchange, ACA plans guarantee coverage regardless of your medical history. You cannot be denied a policy or charged a higher premium because of a pre-existing condition, making this the safest option for retirees managing chronic health issues.

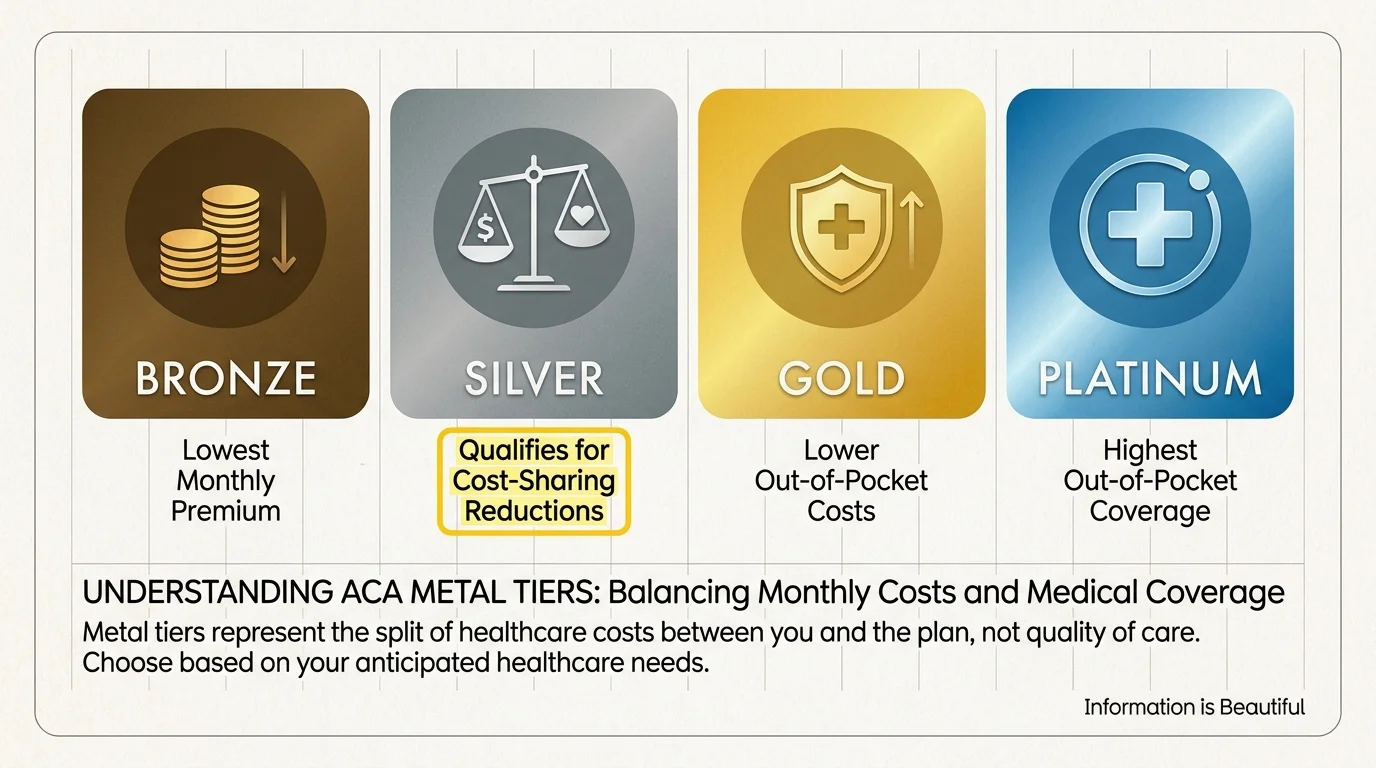

Marketplace plans are categorized into four metal tiers: Bronze, Silver, Gold, and Platinum. Bronze plans carry the lowest monthly premiums but the highest out-of-pocket limits, making them suitable if you rarely visit the doctor. Platinum plans charge steep monthly premiums but cover almost all out-of-pocket costs. Most retirees aim for a Silver plan, which balances moderate premiums with manageable deductibles and qualifies for specific cost-sharing reductions if your income is low enough.

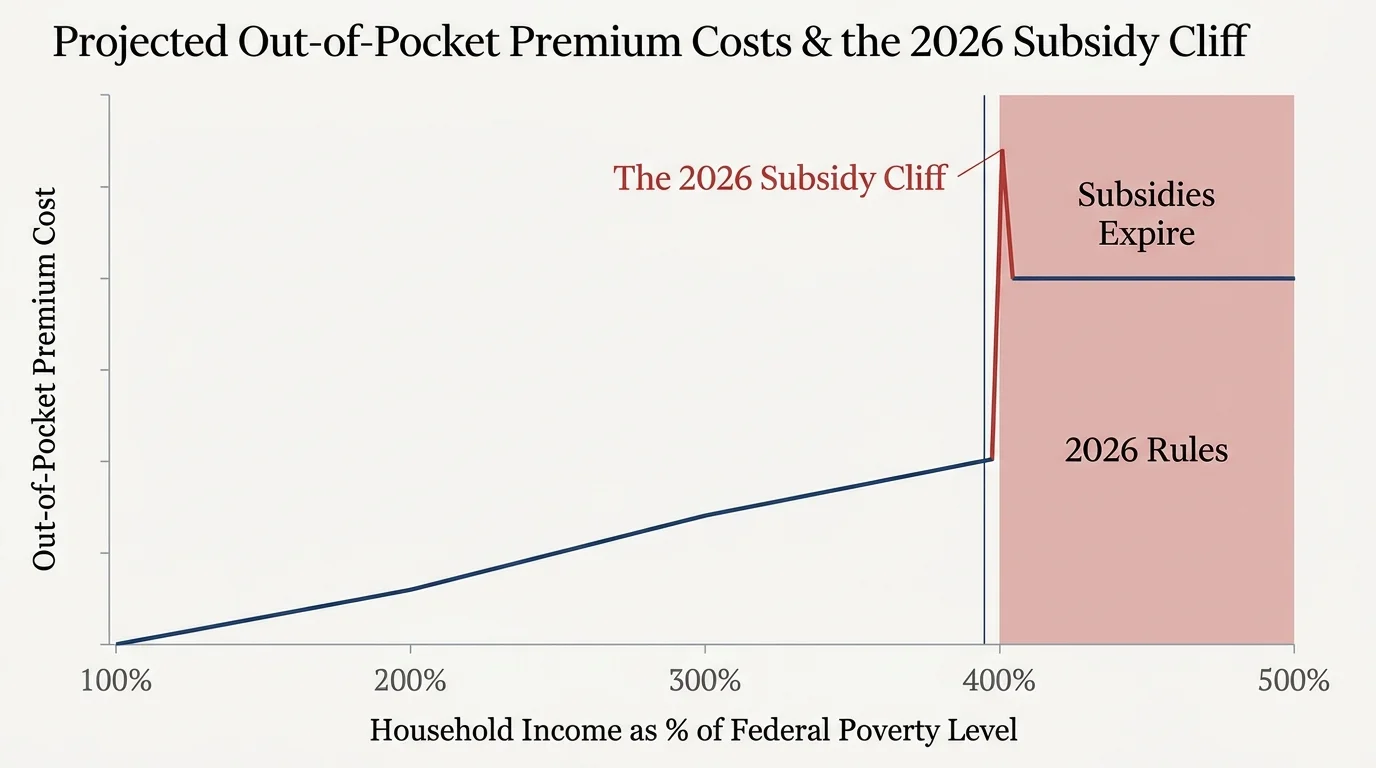

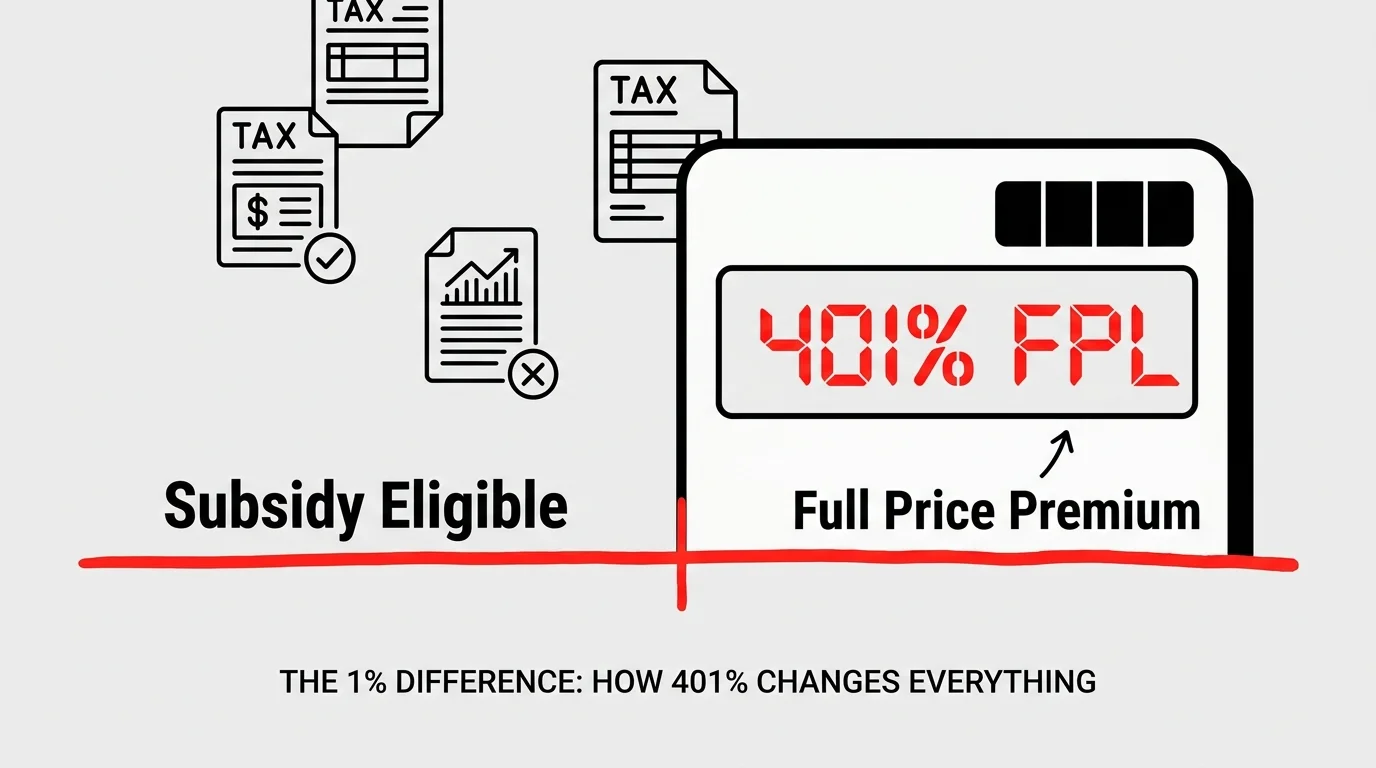

The Return of the ACA Subsidy Cliff in 2026

Understanding ACA premium tax credits is the most critical component of securing affordable insurance. During the pandemic, the federal government temporarily enhanced these tax credits, removing the strict income ceiling. Those temporary enhancements officially expired at the end of 2025.

In 2026, the marketplace has returned to the original ACA rules, bringing back the notorious “subsidy cliff.” Under current law, your household Modified Adjusted Gross Income (MAGI) must stay below 400% of the Federal Poverty Level to qualify for any premium tax credits. For a couple retiring in 2026, this 400% threshold sits roughly around $85,000 (verify exact figures for your state). If your MAGI hits $85,001, you fall off the cliff. You lose every single dollar of financial assistance and must pay the full retail price for your health insurance.

Without subsidies, an ACA policy for a 60-year-old couple can easily exceed $22,000 in annual premiums. Managing your taxable income is no longer just a tax strategy; it is a healthcare necessity.

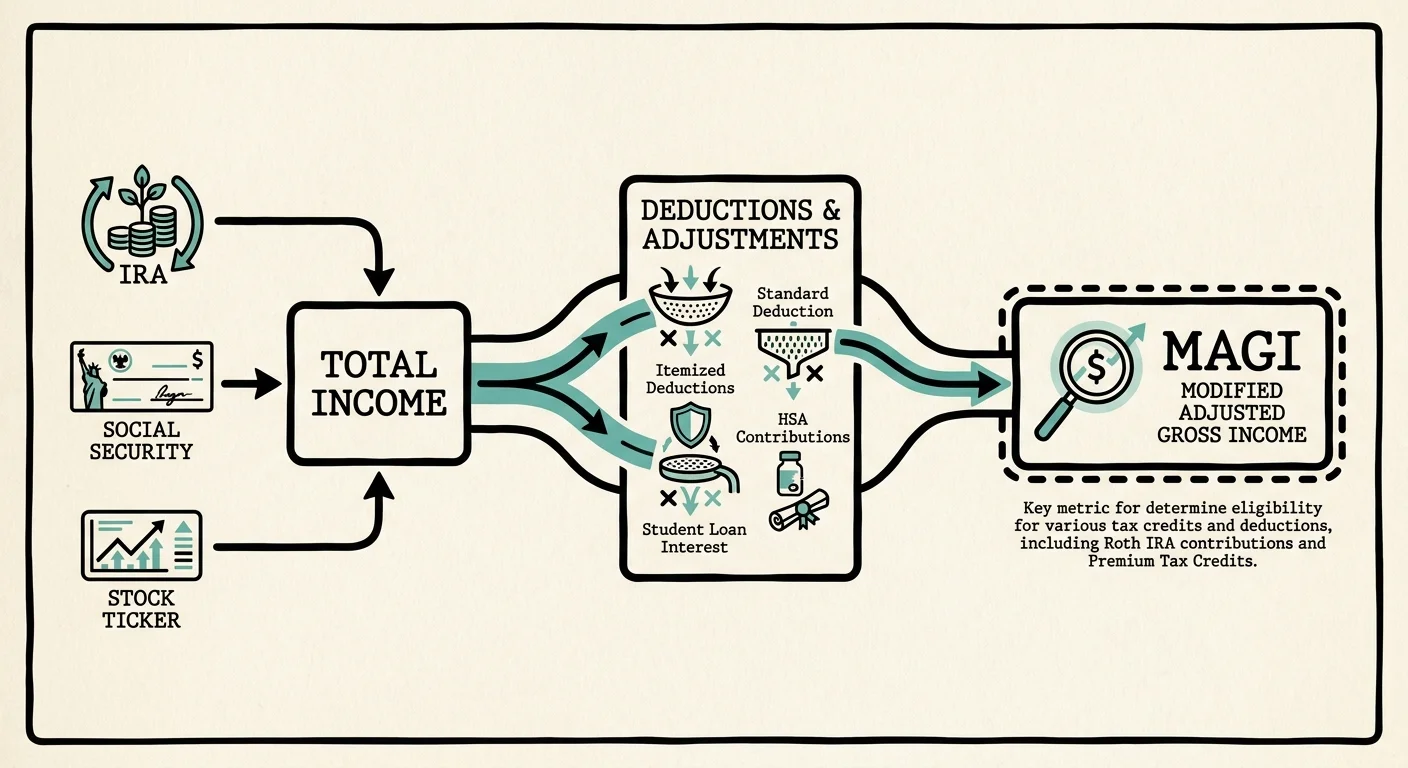

Strategic Income Planning for ACA Subsidies

Because your health insurance costs are directly tied to your MAGI, you must orchestrate your retirement withdrawals meticulously. MAGI includes your wages, taxable pension distributions, traditional IRA withdrawals, dividends, capital gains, and even tax-exempt municipal bond interest.

To stay below the subsidy cliff, consider blending your income sources:

- Draw from Taxable Brokerage Accounts: When you sell stocks in a taxable account, only the capital gains count toward your MAGI, not the principal. You can generate significant cash flow while adding very little to your taxable income.

- Utilize Roth Accounts: Withdrawals from a Roth IRA or Roth 401(k) are completely tax-free and do not count toward your MAGI. Pulling heavily from a Roth account during your pre-Medicare years keeps your income artificially low on paper.

- Delay Social Security: Postponing your Social Security benefits not only increases your future monthly payout, but it also keeps that income off your tax return during the critical years you need ACA subsidies.

- Live on Cash Reserves: Liquidating savings from a standard bank account generates zero taxable income. Building a large cash buffer before you retire early is a proven strategy for securing maximum healthcare subsidies.

COBRA Continuation Coverage: A Short-Term Bridge

If you prefer to keep the exact doctors, network, and deductible you had while working, the Consolidated Omnibus Budget Reconciliation Act (COBRA) allows you to stay on your former employer’s health plan. Most retirees can maintain this coverage for up to 18 months after leaving their job.

The primary drawback to COBRA is the sheer cost. While you were employed, your company likely subsidized 70% to 80% of your health insurance premium. Under COBRA, you are legally responsible for 100% of the premium, plus a 2% administrative fee. A plan that cost you $300 a month out of your paycheck might suddenly cost you $1,500 a month out of your retirement savings.

Despite the high cost, COBRA makes excellent strategic sense in specific scenarios:

- Short Gaps to Medicare: If you retire at age 63 and a half, 18 months of COBRA will carry you exactly to your 65th birthday when you can enroll via the official Medicare website.

- Mid-Year Retirements: If you retire in October and have already met your high deductible and out-of-pocket maximum for the calendar year, switching to an ACA plan means starting your deductible over at zero. Staying on COBRA through December saves you from double-paying your out-of-pocket costs.

- Active Medical Treatments: If you are undergoing chemotherapy, preparing for joint replacement surgery, or managing a complex illness, maintaining your current network of specialists through COBRA provides invaluable peace of mind.

Utilizing a Health Savings Account (HSA) in 2026

A Health Savings Account (HSA) is arguably the most powerful wealth-building tool in the American tax code. It offers a unique triple tax advantage: your contributions are tax-deductible, the money grows tax-free, and withdrawals are completely tax-free when used for qualified medical expenses.

To contribute to an HSA, you must be enrolled in a High Deductible Health Plan (HDHP). For 2026, the Internal Revenue Service (IRS) defines an HDHP as a plan with a minimum deductible of $1,700 for an individual or $3,400 for a family. Furthermore, the maximum out-of-pocket expenses cannot exceed $8,500 for single coverage or $17,000 for family coverage.

The 2026 contribution limits provide massive savings opportunities for early retirees:

- Individual Coverage: Up to $4,400 annually.

- Family Coverage: Up to $8,750 annually.

- Catch-Up Contribution: Individuals age 55 and older can contribute an additional $1,000 per year.

If you retire at 60 and utilize an HDHP through the ACA marketplace, you and your spouse can funnel nearly $10,000 a year into an HSA. You can invest these funds in mutual funds or index funds, allowing the balance to compound. Once you turn 65 and enroll in Medicare, you can no longer contribute new money to an HSA, but you can use your accumulated HSA wealth to pay your Medicare Part B and Part D premiums tax-free for the rest of your life.

Alternative Coverage Strategies

If the ACA marketplace and COBRA do not fit your financial plan, consider these alternative approaches to secure health insurance before age 65.

Spousal Coverage

If you are married and your spouse plans to continue working, joining their employer-sponsored health plan is usually the most cost-effective solution. Losing your job or voluntarily retiring triggers a Special Enrollment Period, allowing your spouse to add you to their workplace plan immediately, without waiting for the company’s annual open enrollment window.

Part-Time Employment with Benefits

Many early retirees pursue “barista FIRE” (Financial Independence, Retire Early). This involves leaving a high-stress corporate career for a low-stress, part-time job that explicitly offers health insurance. Companies like Starbucks, Home Depot, Costco, and Lowe’s are known for extending comprehensive medical benefits to part-time employees who work a minimum number of hours per week. This strategy protects your retirement portfolio while providing structure and social interaction.

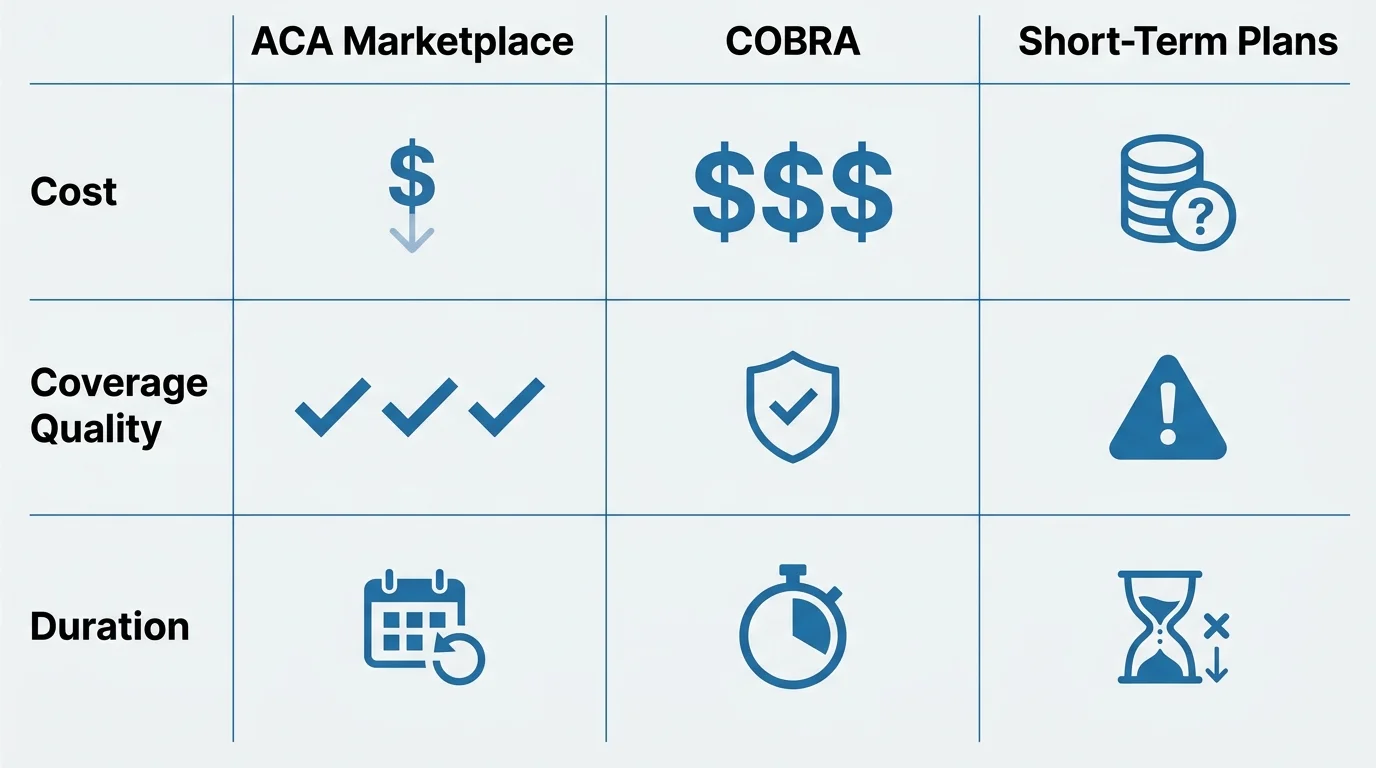

Comparing Your Primary Options

Evaluating your choices requires balancing monthly cash flow against your medical risk tolerance. Use this breakdown to compare the three most common paths.

| Coverage Option | Best For | Primary Advantage | Major Drawback |

|---|---|---|---|

| ACA Marketplace Plan | Retirees who can strictly control their taxable income. | Potential for massive government subsidies; guarantees coverage for pre-existing conditions. | Subject to the 2026 income subsidy cliff; narrow provider networks. |

| COBRA Continuation | Retirees with less than 18 months until Medicare, or those in active treatment. | Zero disruption in care; keeps your current doctors and progress toward deductibles. | Extremely expensive; you pay 102% of the full premium. |

| ACA HDHP with HSA | Healthy retirees wanting to build tax-free wealth for later life. | Triple tax advantage; lowers taxable income to help qualify for ACA subsidies. | High out-of-pocket costs if a sudden medical emergency occurs. |

Pitfalls to Watch For

Early retirees frequently mishandle their health insurance transitions. These errors can cost thousands of dollars and leave you dangerously exposed to medical debt. Avoid these common missteps as you navigate the pre-Medicare landscape.

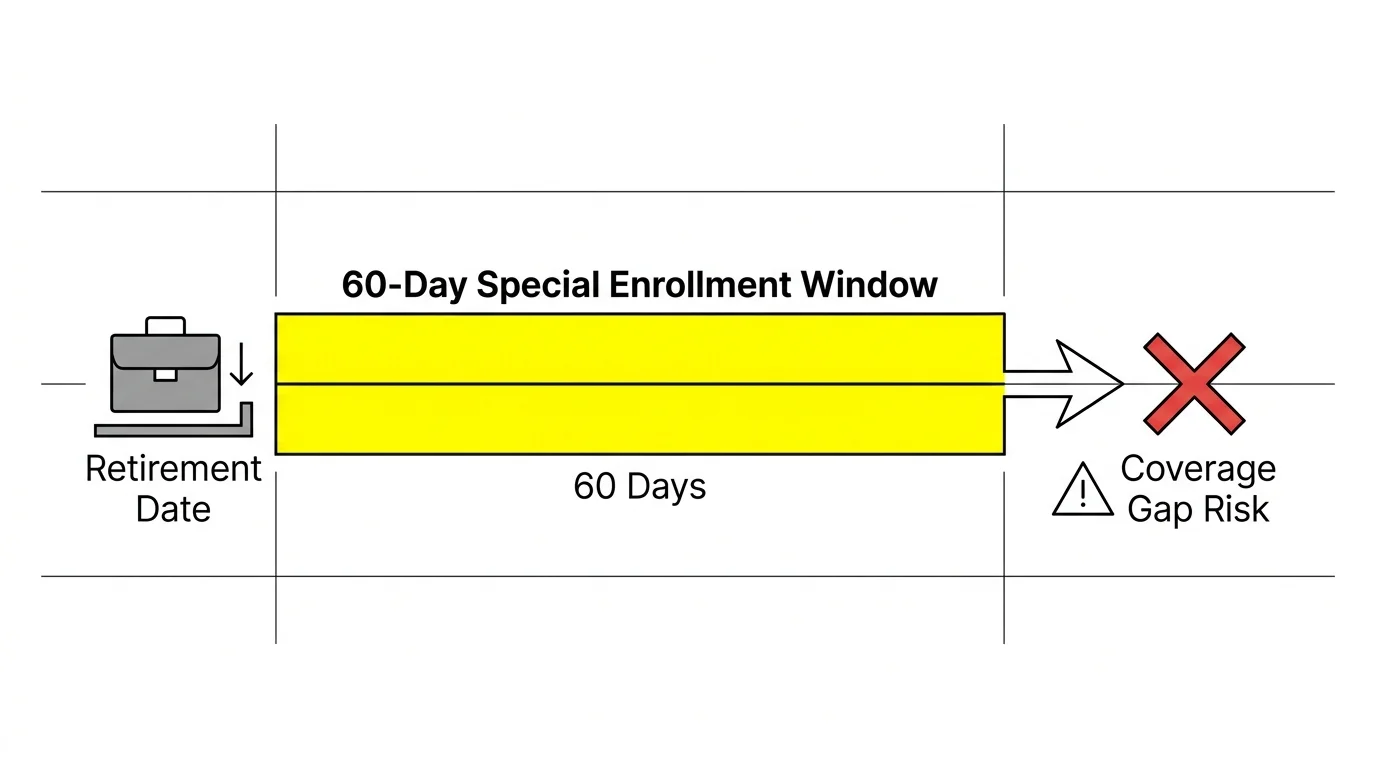

1. Missing Your Special Enrollment Window

Leaving your job and losing your workplace coverage qualifies you for a Special Enrollment Period (SEP) on the ACA marketplace. You have exactly 60 days from the date your coverage ends to select a new plan. If you let this 60-day window expire while debating your options, you will be locked out of the marketplace until the next annual Open Enrollment period in November. Do not procrastinate.

2. Miscalculating MAGI for ACA Subsidies

Guessing your income on an ACA application is a costly mistake. If you underestimate your income, receive heavy subsidies all year, and then take a massive year-end IRA distribution that pushes you over the 400% cliff, the IRS will notice. When you file your taxes the following spring, you will be forced to repay every single dollar of the premium tax credits you received. Always err on the side of overestimating your income slightly, or work with a CPA to project your exact distributions.

3. Draining Traditional IRAs to Pay Premiums

Paying a $1,500 monthly COBRA premium out of a traditional IRA creates a vicious tax cycle. Because traditional IRA withdrawals are taxed as ordinary income, pulling out $18,000 to pay for healthcare actually increases your taxable income. This higher income pushes you further away from ACA subsidies and increases your overall tax burden. Always pay health premiums from cash reserves, taxable accounts, or Roth accounts whenever possible.

4. Assuming Short-Term Plans Provide True Protection

You will see aggressive online advertisements for “Short-Term Medical” or “Health Care Sharing Ministries.” These are not ACA-compliant health insurance policies. They frequently exclude pre-existing conditions, cap the total amount they will pay out, and drop you if you receive a severe diagnosis like cancer. They provide an illusion of safety but fail spectacularly when you actually need catastrophic care.

Getting Expert Help

Securing health insurance in your early sixties involves moving targets: tax brackets, subsidy cliffs, and fluctuating premiums. You do not have to make these decisions in a vacuum.

- Health Insurance Brokers: A licensed independent health insurance broker can show you every ACA plan and COBRA alternative in your zip code. Best of all, using a broker costs you nothing. They are paid commissions directly by the insurance companies, and your premium remains exactly the same whether you use a broker or apply alone.

- Fiduciary Financial Planners: If you hold substantial assets in 401(k)s and traditional IRAs, hire a fee-only fiduciary planner. They run sophisticated software to map out exactly which accounts to draw from in which years, ensuring you stay below the ACA subsidy cliff while maximizing your portfolio’s longevity.

- ACA Navigators: The federal government funds impartial Navigators to help consumers fill out marketplace applications accurately. You can find a local Navigator through HealthCare.gov to guide you through the complex income projection forms.

For additional guidance on aging, financial wellness, and senior support programs, organizations like the National Council on Aging (NCOA) offer excellent, unbiased resources designed specifically to protect older adults.

Frequently Asked Questions

Can I get Medicare if I retire at 62?

No. While you can claim early Social Security benefits at age 62, Medicare eligibility does not begin until age 65 for most Americans. The only exceptions are for individuals who have received Social Security Disability Insurance (SSDI) for 24 months, or those with End-Stage Renal Disease (ESRD) or ALS.

Do Roth IRA withdrawals count toward my ACA income limit?

No. Qualified withdrawals from a Roth IRA are entirely tax-free and do not count toward your Modified Adjusted Gross Income (MAGI). This makes Roth accounts incredibly valuable for early retirees trying to qualify for premium tax credits.

Can I use my HSA funds to pay for COBRA premiums?

Yes. By law, you can use tax-free HSA funds to pay for COBRA continuation coverage premiums, health care coverage while receiving unemployment compensation, and eventually, Medicare premiums.

Preparing for a Healthy Early Retirement

Retiring before 65 requires confronting the reality of American healthcare costs head-on. By understanding the return of the ACA subsidy cliff in 2026, leveraging the short-term power of COBRA, and maximizing the tax advantages of an HSA, you can build a customized bridge to Medicare. Take control of your taxable income, map out your withdrawal strategy, and lean on licensed professionals to verify your numbers. Your early retirement should be defined by the freedom to pursue your passions, not by the stress of unmanageable medical bills.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.