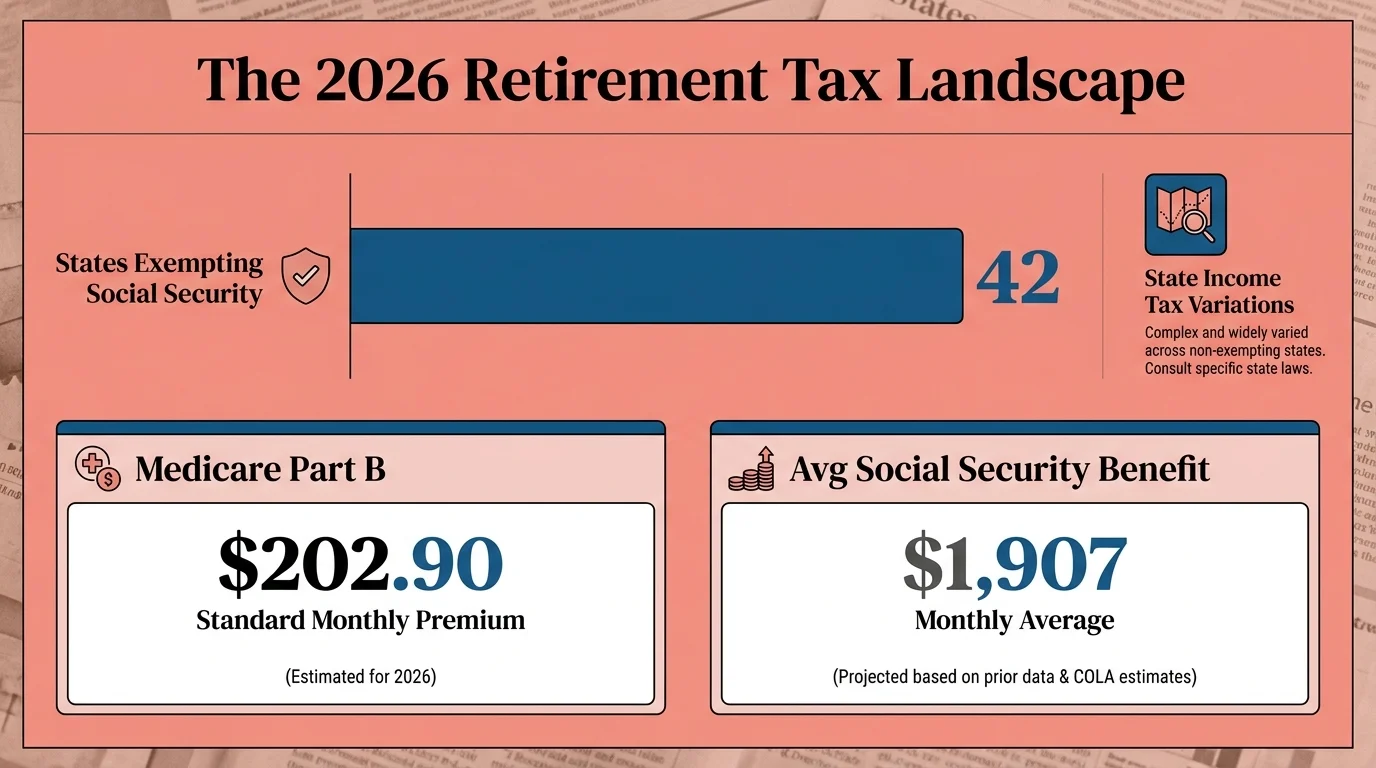

Finding the right place to retire requires balancing your lifestyle goals with the practical realities of a fixed income. When you choose a destination with favorable tax laws, accessible healthcare, and a lower cost of living, your savings stretch significantly further. As of 2026, the standard Medicare Part B premium sits at $202.90 per month, and only 42 states completely exempt Social Security benefits from state income taxes. This makes picking the right location one of the most consequential financial decisions you face. From vibrant desert communities to peaceful Midwestern towns, we have identified eight outstanding U.S. destinations that offer a high quality of life and a stress-free environment without draining your hard-earned nest egg.

1. Midland, Michigan: The Community-Focused Leader

U.S. News & World Report named Midland the absolute best place to retire in the United States for 2026, and the financial fundamentals back up that ranking. Located in the central region of the state, Midland earned the top spot by providing outstanding economic strength, abundant outdoor recreational amenities, and a highly accessible healthcare infrastructure. The city caters specifically to seniors who want an active, community-oriented lifestyle without paying a premium.

From a tax perspective, Michigan provides excellent stability for retirees. The state completely exempts Social Security benefits from state income tax. According to the Social Security Administration, the average monthly benefit in 2026 sits around $1,907, meaning most retirees receive nearly $23,000 annually. Keeping those funds safe from state-level taxation provides an immediate boost to your monthly cash flow. Furthermore, Michigan offers a tiered deduction system for private and public pensions based on your birth year, which shields even more of your income.

2. Green Valley, Arizona: Affordable Desert Living

If shoveling snow no longer appeals to you, Green Valley deserves your attention. Recognized heavily on the 2026 Forbes Best Places to Retire list, this unincorporated area rests comfortably in the foothills of the Santa Rita mountains, roughly 20 miles south of Tucson. Green Valley is unique because it consists of more than 130 age-restricted developments designed explicitly around the needs of older adults.

Housing affordability remains a massive draw. While the national median home price surpassed $400,000 in recent years, Forbes data for 2026 shows the median home price in Green Valley hovering around an incredibly accessible $282,000. Arizona also operates under a simplified flat income tax rate of 2.5% and completely exempts your Social Security checks from taxation. You can enjoy a culturally rich, sun-drenched environment while keeping your housing costs strictly controlled.

3. Lancaster, Pennsylvania: The Tax-Friendly Haven

Lancaster consistently ranks as a premier retirement destination due to its rare blend of rural, rolling farmland and immediate access to top-tier medical facilities. However, the true beauty of retiring in Lancaster lies within Pennsylvania’s highly advantageous tax code. The state goes far beyond simply exempting Social Security benefits.

Pennsylvania is one of the few states in the country that does not tax distributions from 401(k) plans, traditional IRAs, or pensions once you reach age 59 and a half. If your retirement strategy involves drawing down heavily on your traditional IRA to cover living expenses, residing in Pennsylvania acts as an automatic discount on your tax bill. This robust protection of retirement income allows you to dedicate more of your budget to enjoying local farmers’ markets, historical sites, and the thriving arts scene rather than worrying about the IRS.

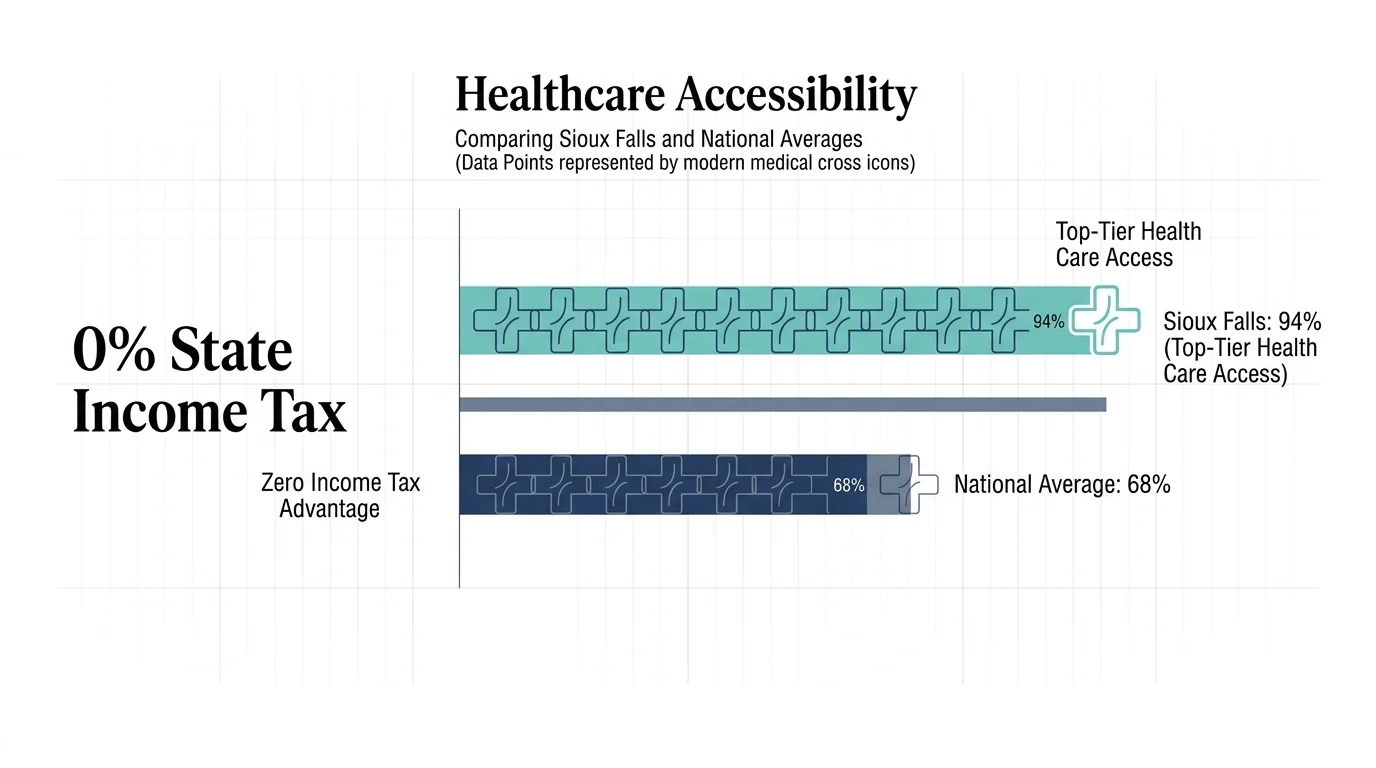

4. Sioux Falls, South Dakota: Zero Income Tax and Top-Tier Health Care

Consistently highlighted by WalletHub as a top retirement destination for 2026, South Dakota proves that you do not need to head to the coasts to find an exceptional retirement lifestyle. Sioux Falls anchors the state’s appeal by offering a safe, highly walkable downtown and access to massive medical networks like Sanford Health and Avera Health. As you age, proximity to specialized medical care becomes a paramount financial and logistical concern.

South Dakota levies absolutely zero state income tax. When the Social Security Administration applied the 2.8% cost-of-living adjustment (COLA) for 2026, residents in Sioux Falls kept the entire raise without worrying about a state tax bite. Your pension payouts, IRA distributions, and part-time employment wages all remain untouched by the state, giving you immense flexibility when structuring your retirement withdrawals.

5. Cheyenne, Wyoming: Wide Open Spaces and Tax Relief

For active seniors who prioritize outdoor recreation and personal privacy, Cheyenne delivers a remarkably peaceful retirement experience. Wyoming boasts wide open spaces, majestic mountain views, and a quiet, relaxed pace of life. It also happens to be one of the most structurally sound states for protecting your wealth.

Like South Dakota, Wyoming collects no state income tax. Furthermore, Wyoming imposes no estate or inheritance tax, making it a brilliant location for retirees focused on legacy planning and leaving assets to their children. Property taxes in Cheyenne remain well below the national average. Because housing costs and property taxes are minimal, your fixed income stretches much further, allowing you to invest in hobbies, travel, or simply building a more robust emergency fund.

6. San Antonio, Texas: Sun, Culture, and Affordability

Texas has long been a magnet for retirees, but San Antonio strikes the perfect balance between big-city amenities and small-town affordability. Earning a spot on the 2026 Forbes list, San Antonio offers a rich cultural history, spectacular food, and a warm climate. Crucially, the median home price in many of its senior-friendly neighborhoods remains comfortably under $300,000.

Texas does not charge a state income tax, which shields your Social Security, pensions, and investment income completely. You must factor in property taxes, as Texas relies heavily on them to fund local services. However, Texas offers significant homestead exemptions and property tax deferrals for residents over age 65. If you manage your housing costs wisely, San Antonio provides a dynamic, culturally immersive retirement without the financial stress associated with other major metropolitan areas.

7. The Villages, Florida: The Ultimate Active Adult Lifestyle

No list of stress-free retirement destinations is complete without mentioning The Villages in Central Florida. This massive, master-planned community practically invented the modern active adult lifestyle. From hundreds of golf courses to sprawling town squares featuring nightly live entertainment, the infrastructure exists entirely to keep seniors active, social, and engaged.

Florida remains a financial haven because it lacks a state income tax. This is particularly valuable if you rely heavily on taxable investment portfolios or massive IRA distributions to fund your lifestyle. While the income tax benefits are profound, you must budget carefully for the region’s elevated property insurance premiums. By prioritizing a newer home built to current hurricane codes, you can mitigate some of these insurance costs while enjoying everything the Sunshine State offers.

8. Fargo, North Dakota: A Hidden Gem for Healthcare and Value

Fargo holds a remarkable distinction in the retirement planning space—it is the only city to appear on the Forbes Best Places to Retire list for 16 consecutive years. While the upper Midwestern winters require a sturdy coat, the economic climate is exceptionally warm and welcoming for seniors.

Fargo shines in two critical areas: extreme affordability and world-class healthcare availability. Your housing dollars buy significantly more square footage here than in almost any other top-rated retirement hub. North Dakota also exempts Social Security benefits from state income taxation for most residents. The combination of minimal housing debt, low crime rates, and heavily protected retirement income makes Fargo a uniquely stress-free place to spend your golden years.

How State Taxes Impact Your Retirement Destination

Understanding the interplay of different tax systems is critical before you pack your moving boxes. While 42 states exempt Social Security benefits, the way they handle other forms of income varies wildly. For instance, West Virginia recently completed a three-year phase-out and officially eliminated its Social Security tax on January 1, 2026. This leaves only eight states that still tax your benefits in some capacity: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont.

When evaluating a new city, you must look beyond the income tax rate and examine the total tax burden. A state with zero income tax might charge aggressive sales taxes on groceries or impose exorbitant property taxes on your primary residence.

| Retirement State | Social Security Taxed? | State Income Tax? | Notable Financial Perk for Seniors |

|---|---|---|---|

| Michigan | No | Yes (Flat rate) | Generous tiered pension deductions based on birth year. |

| Arizona | No | Yes (Flat rate) | Low flat income tax of 2.5% provides high predictability. |

| Pennsylvania | No | Yes (Flat rate) | Completely exempts 401(k) and IRA withdrawals after age 59½. |

| South Dakota | No | No | Zero state income tax on all forms of retirement earnings. |

| Wyoming | No | No | No estate tax and highly favorable property tax rates. |

| Texas | No | No | Robust property tax exemptions for residents over age 65. |

| Florida | No | No | No state income tax; strong asset protection laws. |

| North Dakota | No | Yes | Exceptional cost-of-living value offsets moderate state taxes. |

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, CEO of Berkshire Hathaway

Pitfalls to Watch For

Relocating for retirement can unlock massive financial benefits, but it also introduces unique risks. Avoid these common mistakes when planning your move:

- Ignoring Healthcare Network Changes: While Original Medicare (Parts A and B) travels with you anywhere in the United States, Medicare Advantage (Part C) and Prescription Drug Plans (Part D) are tied strictly to your county of residence. Moving across state lines—or even just to a neighboring county—forces you to select a new plan. Verify your coverage options on Medicare.gov before finalizing any relocation.

- Triggering IRMAA Surcharges: The standard Medicare Part B premium sits at $202.90 per month in 2026, with an annual deductible of $283. However, if you sell a highly appreciated home in your old state to fund your move, that massive capital gain could temporarily push your income high enough to trigger the Income-Related Monthly Adjustment Amount (IRMAA). This can dramatically spike your Medicare premiums two years down the line.

- Overlooking Property Insurance Realities: Moving to a state with no income tax often feels like an instant raise. However, if you move to a coastal region like Florida or a wildfire-prone area out west, soaring property insurance premiums can quickly erase your tax savings. Always secure insurance quotes on a specific property before making an offer.

- Underestimating the Cost of Travel: Moving to a peaceful, remote town in Wyoming or North Dakota sounds idyllic, but consider the cost of flying back to see your grandchildren. If you locate too far from a major airport, the logistical and financial strain of travel can slowly erode your quality of life.

Getting Expert Help

You do not have to navigate a major cross-country retirement move alone. Engaging the right professionals ensures that your relocation actually results in the financial peace you seek.

- Consult a Tax Professional: A Certified Public Accountant (CPA) can run a localized tax projection. They will compare your exact combination of Social Security, pension, and IRA income under your current state’s tax laws versus your proposed destination.

- Work with a Medicare Broker: Because Medicare Advantage and Part D plans are localized, a licensed independent broker can help you transition your healthcare coverage seamlessly. You generally qualify for a Special Enrollment Period when you move outside your current plan’s service area.

- Update Your Estate Plan: Estate laws, probate processes, and power of attorney documents vary heavily by state. Once you establish residency in your new home, have a local estate planning attorney review your will or trust to ensure it remains valid and optimal under local statutes.

Moving Forward with Confidence

Choosing your retirement destination should be an exciting chapter rather than a source of anxiety. By carefully analyzing housing costs, healthcare accessibility, and local tax policies, you can design a lifestyle that perfectly aligns with your financial reality. Whether you prefer the sunny golf courses of Florida, the peaceful plains of South Dakota, or the tax-friendly environment of Pennsylvania, the right community is out there waiting for you. Take your time, crunch the numbers, and plan your next adventure with absolute confidence.

This article provides general financial education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice tailored to your retirement needs, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.