Where you live in retirement dramatically impacts your bottom line, largely because state taxes can aggressively eat away at your fixed income. Moving just one state over can save or cost you thousands of dollars each year in property, income, and sales taxes. When you understand which states impose the highest overall tax burden, you can make smarter decisions about your golden years. Many retirees assume they are safe in a state with no income tax, only to be surprised by exorbitant property or sales taxes that wipe out those savings. By evaluating the total percentage of personal income paid to state and local governments, you gain a highly accurate picture of your true cost of living.

Understanding “Tax Burden” Versus Simple Tax Rates

When planning your retirement budget, looking at a state’s nominal income tax brackets rarely tells the whole story. A state might boast a staggeringly low income tax rate—or eliminate it entirely—while quietly balancing its budget through aggressive property assessments and steep taxes on everyday goods. This is why financial professionals rely on the concept of “tax burden” rather than simple tax rates.

Your tax burden represents the total proportion of your personal income that flows directly to state and local governments. By examining the three primary tax categories—property taxes, individual income taxes, and sales and excise taxes—analysts can calculate a much more accurate representation of affordability. Evaluating tax burden cuts through the marketing slogans of “low-tax states” and exposes the true cost of funding local schools, road maintenance, and municipal services.

For retirees living on a combination of Social Security, pension payouts, and withdrawals from retirement accounts like IRAs and 401(k)s, this comprehensive view is crucial. If your income remains relatively fixed, a state that extracts 13% of your wealth annually will force you to adopt a vastly different lifestyle than a state that takes only 5%. Understanding how these complex tax systems interact allows you to protect the nest egg you spent decades building.

The Top States with the Highest Overall Tax Burden in 2026

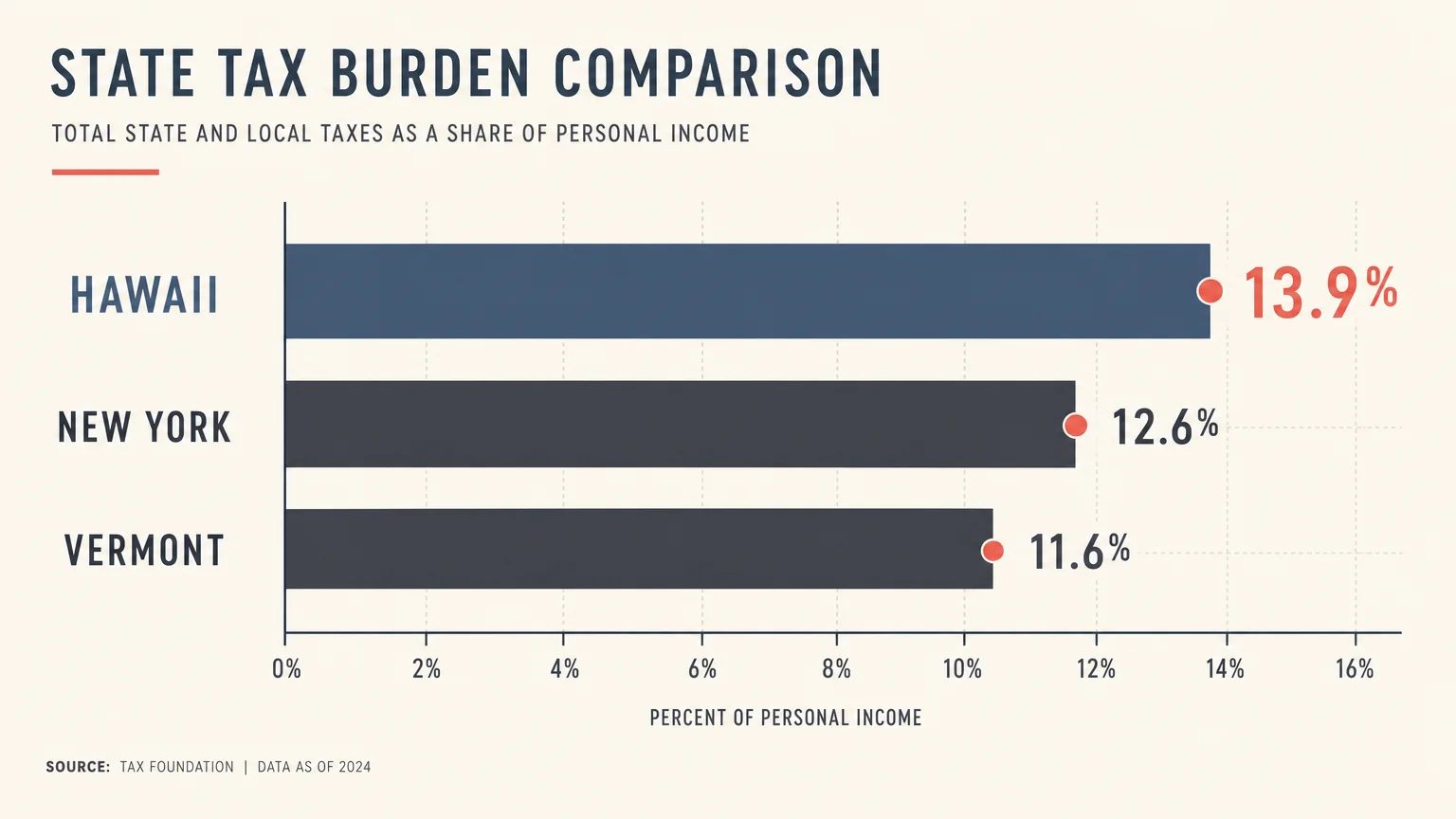

According to the most recent 2026 economic analyses, the tax burden across the United States varies wildly depending on your zip code. Geography plays a massive role in wealth preservation. Based on the 2026 WalletHub methodology mapping personal income to tax revenue, a select group of states consistently demands the most from their residents.

Hawaii leads the nation with the highest overall tax burden. Although its physical beauty is unparalleled, the state extracts nearly 13.9% of total personal income from its residents to fund government operations. This heavy burden is largely driven by exorbitant sales and excise taxes that are passed on to consumers. Following closely behind are New York and Vermont, both known for their robust public services funded by significant property and income tax levies.

| National Rank | State | Overall Tax Burden (%) | Primary Revenue Driver |

|---|---|---|---|

| 1 | Hawaii | 13.9% | Sales and Excise Taxes (7.2%) |

| 2 | New York | 13.6% | Individual Income Taxes |

| 3 | Vermont | 11.5% | Property Taxes |

| 4 | California | 11.0% | Individual Income Taxes |

| 5 | Maine | 10.6% | Property and Income Taxes |

By contrast, residents of Alaska enjoy the lowest overall tax burden in the country at just 4.9%. Because Alaska derives massive revenue from severance taxes on oil and natural gas, it can afford to charge its citizens zero state income tax and incredibly low sales taxes.

The Triad of Taxes: Property, Income, and Sales

To fully grasp how states generate revenue, you must understand the three primary levers they pull. When lawmakers decrease taxes in one category, they almost universally increase them in another. This “triad of taxes” forms the foundation of your annual carrying costs.

The Hidden Weight of Property Taxes

Property taxes are widely considered the most burdensome expense for homeowners, especially seniors whose mortgages are fully paid off. Because property taxes are tied to your home’s assessed value rather than your annual income, a skyrocketing real estate market can dramatically inflate your tax bill even if your retirement income remains unchanged. While 18 states currently implement assessment caps to protect homeowners from runaway tax increases, the baseline rates remain steep in many regions.

For example, New Jersey and Illinois impose the highest effective property tax rates in the nation, both sitting at approximately 1.88% of a home’s value. If you own a $400,000 home in New Jersey, you can expect an annual property tax bill of around $7,520. Conversely, Hawaii features the lowest effective property tax rate at just 0.29%; however, because median home prices in Hawaii are astronomical, the actual dollar amount residents pay remains a significant hurdle.

The Impact of Individual Income Taxes

Your state’s income tax structure dictates how much of your hard-earned pension, IRA distributions, and part-time wages you get to keep. Currently, 42 states levy some form of individual income tax. Many utilize a progressive bracket system—similar to the federal government—where your tax rate increases as your income climbs. For high-income earners, states like California impose top marginal rates exceeding 13%. Other states employ a flat tax system, charging a single universal rate regardless of whether you earn $40,000 or $400,000.

The Regressive Nature of Sales and Excise Taxes

Sales and excise taxes are inherently regressive, meaning they consume a larger percentage of income from lower- and middle-class households than from wealthy ones. When you purchase groceries, clothing, or a new vehicle, the state takes a cut. States that lack an income tax frequently rely on elevated sales taxes to bridge their budgetary gaps. If you are relocating to manage your budget, it is critical to check whether your prospective new state exempts essentials like groceries and prescription medications from its sales tax code. For seniors managing chronic health conditions, a state that taxes prescription drugs can quietly drain thousands of dollars from your accounts.

“It’s not what you make, it’s what you keep. The impact of taxes on your retirement income cannot be overstated.” — Ed Slott, Retirement Tax Expert

Which States Still Tax Social Security Benefits in 2026?

One of the most common questions seniors ask when mapping out their retirement is whether their hard-earned Social Security benefits will be taxed. The answer involves both federal and state-level rules.

At the federal level, the Social Security Administration (SSA) and the IRS determine the taxability of your benefits based on your “provisional income”. This figure is calculated by taking your Adjusted Gross Income (AGI), adding any non-taxable interest you earn, and then adding 50% of your Social Security benefits. If your provisional income exceeds certain thresholds, up to 85% of your benefits may be subject to federal income tax.

State-level taxation, however, is a rapidly changing landscape. Advocacy groups like AARP have spent years lobbying state legislatures to abolish taxes on Social Security, and those efforts have generated massive recent successes. For example, Missouri and Kansas successfully eliminated their Social Security taxes in 2024. More recently, West Virginia completely phased out its taxation on Social Security benefits starting in the 2026 tax year.

As of 2026, only eight states still impose income taxes on Social Security benefits:

- Colorado: Taxes higher earners but offers substantial income deductions for residents aged 65 and older.

- Connecticut: Imposes taxes based on specific Adjusted Gross Income (AGI) caps.

- Minnesota: Still taxes benefits, though legislative discussions regarding phase-outs continue.

- Montana: Uses federal taxable income as its starting point but offers a $5,500 deduction for seniors over 65.

- New Mexico: Imposes taxes on upper-income earners.

- Rhode Island: Taxes benefits for higher-income brackets.

- Utah: Applies taxes but provides retirement tax credits to offset the burden for middle-income filers.

- Vermont: Continues to tax benefits, heavily contributing to its high overall tax burden.

Even if you live in one of these eight states, your benefits might still escape taxation if your overall income falls below state-specific exemption thresholds. When the SSA announces its annual Cost-of-Living Adjustment (COLA)—which is set at 2.8% for 2026—it increases your monthly cash flow. However, that extra income could simultaneously push you into a taxable bracket, making proactive tax planning more important than ever.

States That Do Not Tax Personal Income

For many retirees, moving to a state with no individual income tax sounds like an immediate ticket to financial freedom. Escaping the annual burden of filing complex state returns and keeping 100% of your pension and IRA withdrawals is an undeniably attractive proposition.

In 2026, nine states officially levy zero individual income tax:

- Alaska: The only state to boast no income tax and no state-level sales tax.

- Florida: A perennial favorite for retirees due to its warm climate and lack of income tax.

- Nevada: Funds its operations largely through tourism, gaming, and high sales taxes.

- New Hampshire: Officially became a pure no-income-tax state after fully repealing its interest and dividends tax as of 2025.

- South Dakota: Offers a highly favorable tax environment for retirees and trusts.

- Tennessee: Levies zero income tax but relies heavily on elevated sales taxes.

- Texas: Offsets its lack of income tax with some of the highest property tax rates in the country.

- Washington: Levies no traditional income tax but recently implemented a targeted tax on high-yield capital gains.

- Wyoming: Boasts one of the lowest overall tax burdens, driven by mineral severance taxes rather than resident income.

While this list is enticing, you must weigh the hidden costs. A retiree moving from California to Texas will undoubtedly save massive amounts on income tax, but they might suffer serious sticker shock when their property tax bill arrives. Always evaluate the full tax triad before calling a moving company.

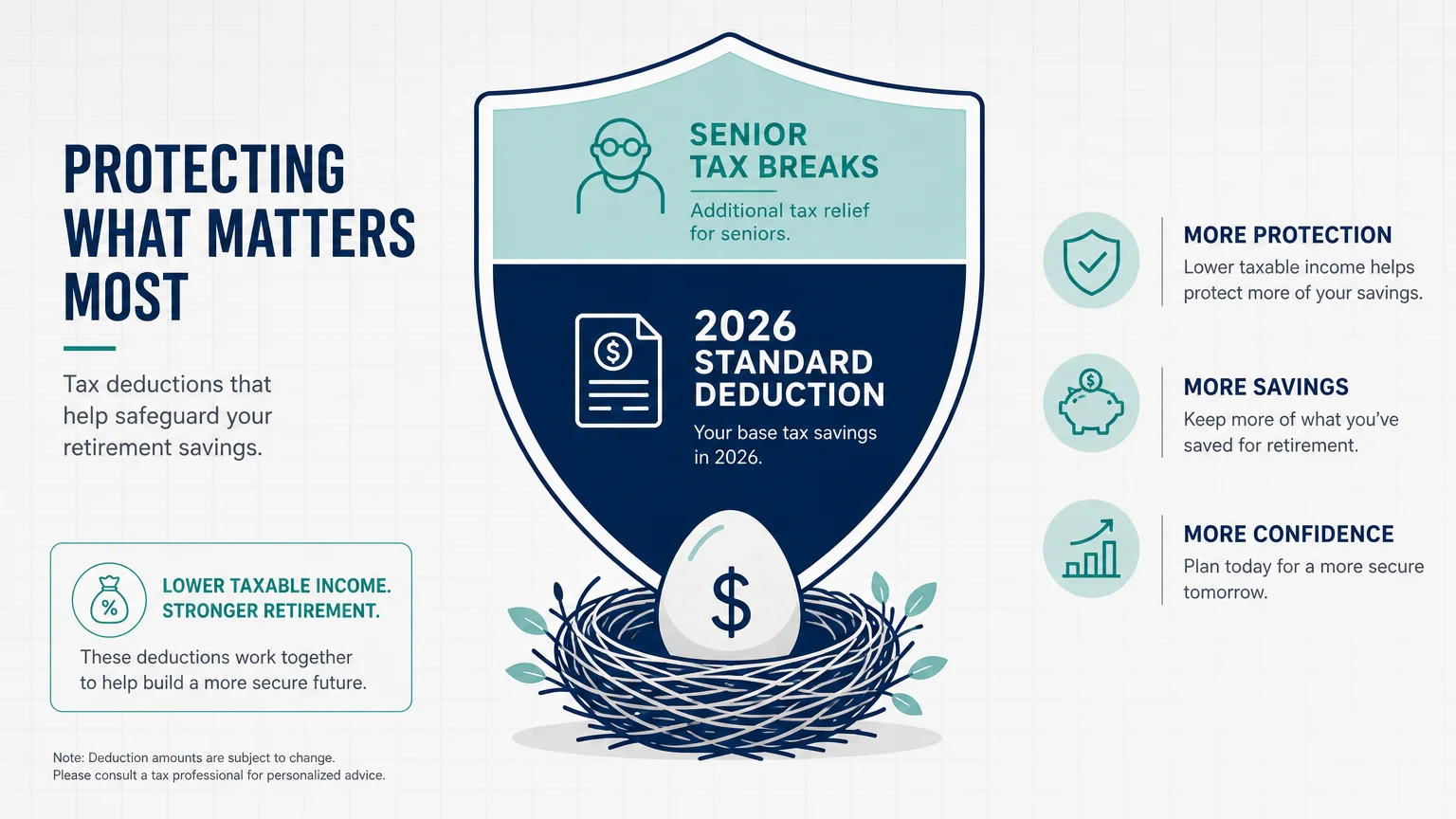

Navigating the 2026 Standard Deduction and New Senior Tax Breaks

While managing your state tax burden is vital, minimizing your federal tax liability provides the most immediate boost to your retirement budget. The IRS updates its tax brackets and standard deductions annually to combat inflation, and the figures for the 2026 tax year offer significant relief.

For the 2026 tax year, the baseline federal standard deduction rises to $16,100 for single filers and $32,200 for married couples filing jointly. If you file as head of household, the deduction increases to $24,150.

However, the tax landscape for seniors has dramatically improved thanks to recently enacted legislation. The highly publicized “One Big Beautiful Bill Act” (OBBBA) introduced massive, temporary tax relief specifically targeting older Americans. For tax years 2025 through 2028, eligible taxpayers aged 65 or older can claim an enhanced bonus deduction of $6,000 per person.

To qualify for this lucrative break in 2026, you must meet the following criteria:

- You must be 65 years of age on or before the last day of the tax year.

- The deduction phases out for single taxpayers with a modified adjusted gross income (MAGI) over $75,000.

- For married couples filing jointly, the phase-out begins when MAGI exceeds $150,000.

When you combine these deductions, the math becomes incredibly favorable. A married couple who are both over 65 and fall below the income thresholds could claim the $32,200 standard deduction alongside a combined $12,000 OBBBA bonus deduction. When factoring in the traditional age-based add-on for seniors (which typically hovers around $1,500 to $1,950 per qualifying individual), a retired couple could potentially shield nearly $48,000 of their income from federal taxes entirely. Review these current limits carefully at the Internal Revenue Service (IRS) website to ensure you do not leave money on the table.

Common Mistakes to Avoid When Planning Your Relocation

Even the most careful planners can stumble when trying to optimize their state taxes. Navigating the legal web of interstate residency requires precision. Avoid these common missteps if you want to successfully lower your tax burden.

- Focusing Solely on Income Tax: As demonstrated by states like Texas and New Hampshire, moving to a state with zero income tax does not automatically equal savings. High property taxes and vehicle excise taxes can quickly negate your increased monthly cash flow.

- Failing to Properly Establish Legal Domicile: Simply buying a condominium in Florida and staying there for the winter does not free you from New York or California taxes. High-tax states are notoriously aggressive about auditing wealthy retirees who claim to have moved. To legally sever ties, you must establish a new “domicile” by changing your driver’s license, registering to vote in your new state, updating your estate documents, and physically residing in the new state for more than 183 days a year.

- Overlooking Taxes on Retirement Accounts: Just because a state exempts Social Security benefits from taxation does not mean your 401(k) withdrawals or private pensions are safe. Many states that protect Social Security fully tax traditional IRA distributions as ordinary income. Always verify exactly which types of retirement income are protected.

- Ignoring Estate and Inheritance Taxes: Sometimes referred to as “death taxes,” state-level estate and inheritance taxes can drastically reduce the wealth you pass on to your heirs. Even if a state has a low overall income tax burden during your life, it might levy heavy taxes on your assets upon your passing. Ensure your estate plan accounts for the specific laws of your chosen state.

Finding the Right Advisor

Given the complexities of state tax codes, standard deductions, and shifting federal legislation, consulting with a fiduciary financial advisor or a Certified Public Accountant (CPA) is often the safest route. Consider seeking professional guidance if you find yourself in any of the following scenarios:

Relocating Across State Lines: If you are selling your primary residence and moving to a state with a vastly different tax structure, an advisor can help you time the sale of your home to minimize capital gains exposure and ensure your change of domicile is legally bulletproof.

Executing Strategic Roth Conversions: If you plan to move from a high-tax state to a low-tax state, an advisor can help you map out a timeline for converting your traditional IRA funds into a Roth IRA. Delaying conversions until you become a resident of a no-income-tax state can save you tens of thousands of dollars.

Managing Multi-State Income Sources: If you retire to Florida but continue to earn rental income from a property you own in New Jersey, you will still owe taxes to New Jersey on that specific income. Tax professionals excel at untangling multi-state tax returns and ensuring you claim the correct credits to avoid double taxation.

Frequently Asked Questions (FAQ)

Is it worth moving to a state with no income tax?

It can be highly beneficial, but it depends entirely on your broader financial picture. If your income relies heavily on taxable IRA distributions or pensions, a zero-income-tax state offers massive savings. However, if your primary wealth is tied up in a high-value home, the elevated property taxes in states like Texas or New Hampshire might outweigh the income tax benefits. Always calculate your specific “tax burden” rather than looking at income tax in a vacuum.

At what age do seniors stop paying property taxes?

You never entirely stop paying property taxes; however, many local jurisdictions offer targeted relief for seniors. Depending on your state and county, you may qualify for “senior freezes” that lock your property’s assessed value at a certain age, or homestead exemptions that shield a portion of your home’s value from taxation. You typically must apply for these programs directly through your county assessor’s office.

Does moving to a new state trigger a tax audit?

If you are moving away from an aggressive, high-tax state (such as New York, California, or Illinois) and you maintain property, business ties, or bank accounts in that state, your risk of a residency audit increases significantly. These states employ specialized audit teams to verify that you have genuinely abandoned your old domicile and successfully established a new one.

Which state has the absolute lowest tax burden?

According to 2026 economic data, Alaska holds the title for the lowest overall tax burden in the United States at just 4.9%. Because the state generates immense revenue from the energy sector, it imposes no state income tax and incredibly low sales and property taxes on its residents.

Taking control of your retirement finances means looking past the surface-level marketing of “tax-friendly” states and doing the hard math on your actual carrying costs. Whether you decide to stay close to family in a high-tax region or embark on a new adventure in a tax-free haven, making an informed decision protects your financial independence.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: June 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.