With new import tariffs pushing everyday consumer prices up by more than 3% in early 2026, protecting your fixed income requires a strategic approach. From the 10% flat tariff on U.S. trading partners to the rising costs of electronics and groceries, this high-price economy demands smarter shopping habits. The good news is that you have powerful tools at your disposal, including massive new tax deductions, little-known Medicare grocery allowances, and targeted store discounts designed exclusively for older Americans. By adjusting where and when you buy essentials, you can effectively offset these hidden import taxes. Here is exactly how to navigate this challenging environment, maximize your cost-of-living adjustments, and secure the daily savings you deserve.

The Real Cost of Tariffs on Your Daily Life

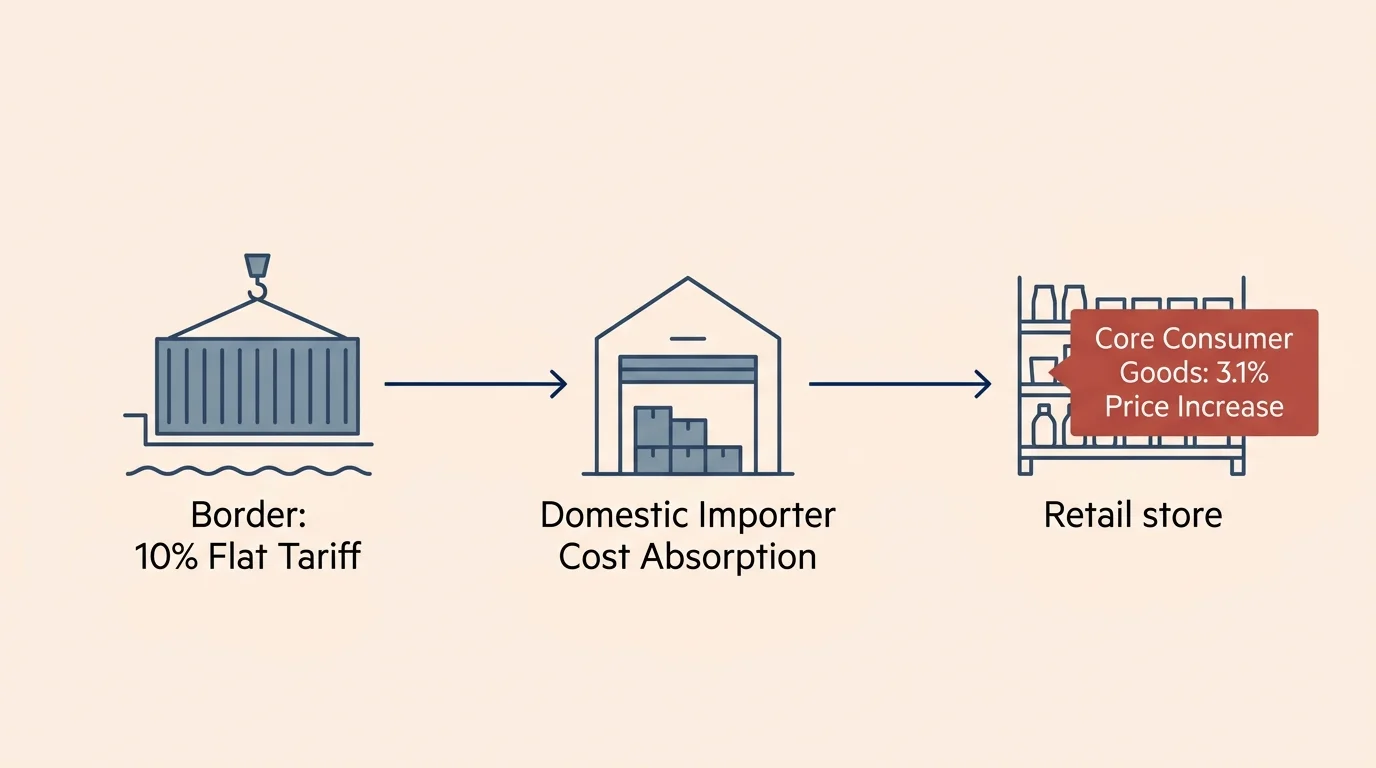

To successfully navigate a high-price economy, you must first understand why prices are climbing. Tariffs operate as a tax on imported goods. When the U.S. government levies a 10% flat tariff on trading partners, the foreign manufacturer does not cover that cost . Instead, the domestic importer pays the tax at the border and immediately passes that expense down the supply chain until it reaches your local retail store.

According to the Federal Reserve, the sweeping tariffs implemented throughout 2025 generated a noticeable ripple effect, raising core consumer goods prices by 3.1% through the first quarter of 2026 . This means a significant portion of the inflation you currently see on store shelves is directly tied to trade policy, not just corporate markups or general inflation.

Certain product categories rely heavily on global supply chains and are bearing the brunt of these price hikes. Furniture, motor vehicle parts, imported apparel, and consumer electronics have seen the sharpest increases . By recognizing which goods are heavily tariffed, you can adjust your purchasing timeline. Delaying non-essential electronics upgrades or opting for domestically manufactured home goods can immediately protect your checking account from these invisible taxes.

“The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures. The inflation tax has a fantastic ability to simply consume capital.” — Warren Buffett, Investor and CEO

Supermarket Strategies for Tariff-Proof Shopping

Grocery shopping remains one of the largest flexible expenses in any retiree budget. While food inflation has moderated slightly from its peak, the compounding effect of higher transportation costs and supply chain tariffs keeps everyday staples expensive. Combatting this requires moving past generic couponing and utilizing specific age-based discounts that grocery chains offer to secure your loyalty.

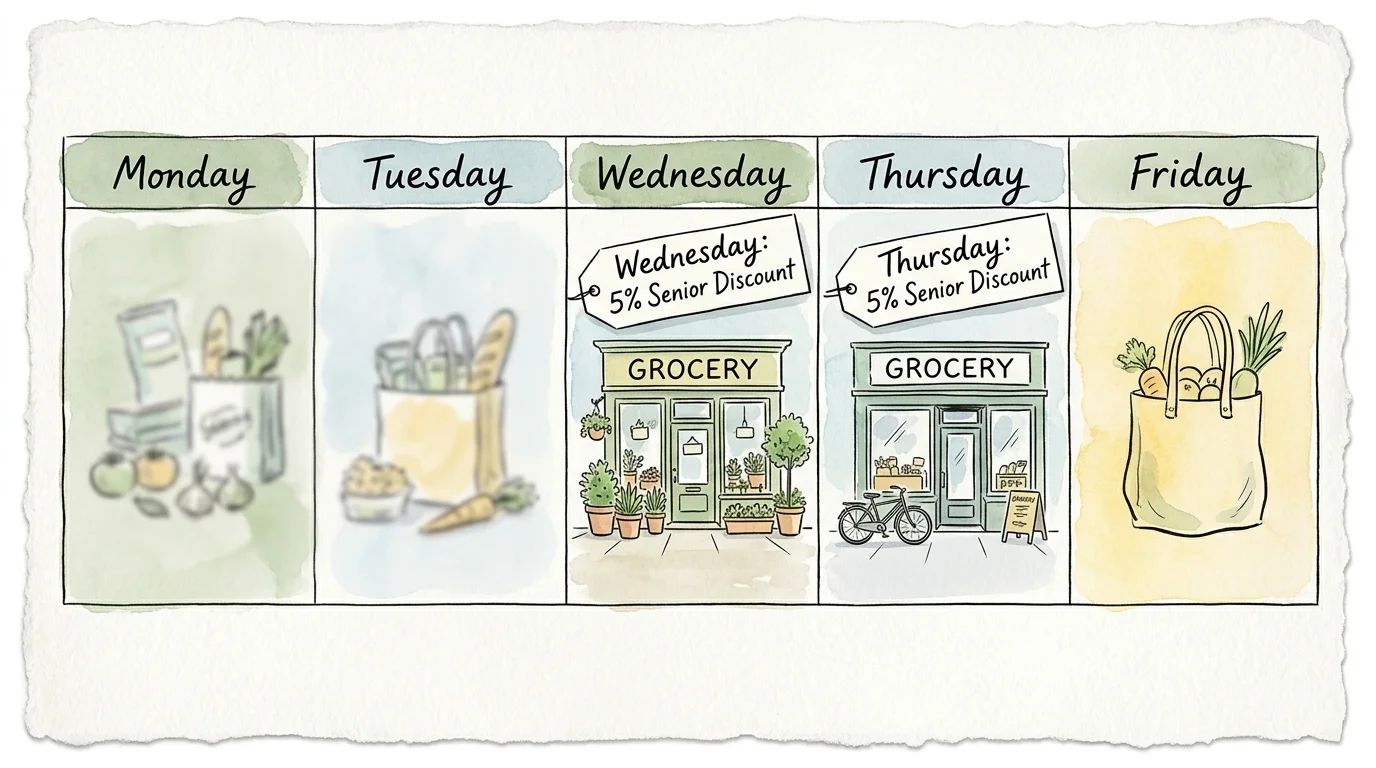

Many regional and national supermarket chains provide dedicated senior discount days. By shifting your primary shopping trip to align with these windows, you can instantly erase the inflationary premium on your groceries.

- Publix: Shoppers aged 55 and older can secure a 5% discount on their total bill every Wednesday in select markets .

- Albertsons: In many locations, customers aged 55 and older receive a 10% discount on the first Wednesday of each month .

- Harris Teeter: Shoppers aged 60 and older can claim a 5% discount every Thursday after linking their loyalty card .

- Kroger: Certain regional Kroger-owned stores provide a 10% discount on select days for older adults, though participation varies heavily by state .

Beyond scheduled discounts, adjusting the specific items in your cart pays massive dividends. Tariff-proof your grocery run by minimizing out-of-season produce imported from South America or specialty goods shipped from Europe. Instead, pivot to domestic store-brand items. Grocery chains negotiate massive, localized contracts for their private-label goods, shielding them from the worst of the international trade tariffs.

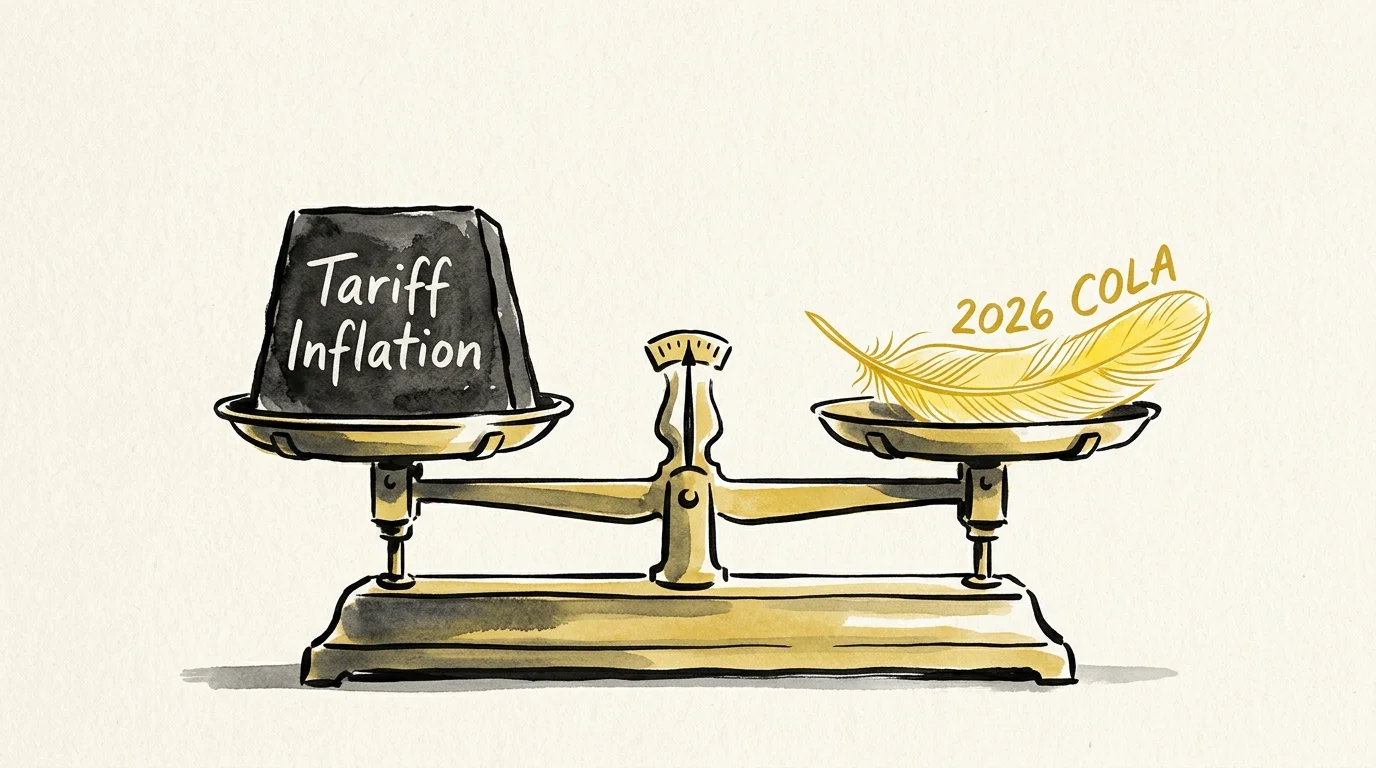

How Your 2026 COLA Factors In

Your Social Security benefits are anchored to inflation through the annual Cost-of-Living Adjustment (COLA). While the COLA provides a critical lifeline, the timing of the adjustment often lags behind the real-time price increases you experience at the register.

In 2025, beneficiaries received a modest 2.5% increase . For 2026, the Social Security Administration enacted a 2.8% COLA . If your monthly benefit hovered around the national average of $2,000, this most recent adjustment added roughly $56 to your monthly check starting in January 2026. While an extra $672 a year provides breathing room, it rarely feels sufficient when utility bills and grocery receipts climb simultaneously.

Understanding the trajectory of your benefits helps with long-term budgeting. Due to the recent tariff-driven price increases on consumer goods, early projections from senior advocacy groups suggest the 2027 COLA could jump higher, potentially landing near 3.8% . Knowing that relief is tied to these inflation metrics allows you to draw down selectively from cash reserves now, anticipating a stronger adjustment in the upcoming year.

Free Up Cash: The Massive 2026 Senior Tax Deductions

The most effective strategy to survive a high-price economy is keeping more of your own income. In 2025, lawmakers passed a sweeping tax package known as the “One Big Beautiful Bill Act” (OBBBA), which dramatically altered the tax landscape for older Americans through 2028 . If you understand how to claim these deductions, you can free up thousands of dollars in cash flow to offset retail inflation.

If you are 65 or older, you now have access to three distinct layers of standard deductions for the 2026 tax year. First, the IRS increased the base standard deduction to $16,100 for single filers and $32,200 for married couples filing jointly . Second, the traditional extra deduction for seniors remains intact, adding $2,050 for singles and $1,650 per spouse for married couples .

The true game-changer is the newly implemented Senior Bonus Deduction. This temporary provision grants an additional $6,000 deduction per eligible person aged 65 or older . For a married couple where both spouses meet the age requirement, this adds a staggering $12,000 in tax-free space to your return. When stacked together, an eligible married couple can shelter $47,500 from federal income tax entirely .

| Deduction Type | Single Filer (Age 65+) | Married Filing Jointly (Both 65+) |

|---|---|---|

| Base Standard Deduction (2026) | $16,100 | $32,200 |

| Additional Senior Deduction | $2,050 | $3,300 ($1,650 x 2) |

| OBBBA Senior Bonus Deduction | $6,000 | $12,000 ($6,000 x 2) |

| Total 2026 Standard Deduction | $24,150 | $47,500 |

You must pay close attention to the income limits attached to this new benefit. The $6,000 Senior Bonus Deduction begins to phase out if your Modified Adjusted Gross Income (MAGI) crosses $75,000 for single filers or $150,000 for married couples filing jointly . Managing your retirement account withdrawals to stay just below this threshold is one of the most lucrative financial moves you can make this year.

Government Assistance and Hidden Health Plan Benefits

If tariffs and inflation have stretched your budget to the breaking point, you should explore assistance programs designed specifically to keep healthy food on your table. Millions of older Americans qualify for these programs but simply never apply, leaving valuable benefits completely unused.

Start by reviewing the Senior Farmers Market Nutrition Program (SFMNP). Administered by the USDA, this program provides low-income seniors with coupons that can be exchanged for fresh, domestic fruits, vegetables, honey, and herbs at local farmers markets . Because you are buying locally grown food, you bypass international tariffs entirely. Similarly, the Commodity Supplemental Food Program (CSFP) delivers monthly packages of healthy, domestically sourced food directly to eligible seniors .

Additionally, check the details of your health insurance coverage. Many modern Medicare Advantage (Part C) plans now include “Flex Cards.” These prepaid debit cards are loaded with a monthly or quarterly allowance specifically earmarked for healthy groceries, over-the-counter pharmacy items, and even utility bills . A flex card allowance of just $50 a month completely neutralizes the average grocery price increases caused by recent tariffs.

What Can Go Wrong

Even with the best intentions, it is easy to make costly errors when navigating a volatile economic landscape. Avoid these common missteps to keep your finances secure:

- Assuming Cashiers Will Apply Your Discount: Most point-of-sale systems require the cashier to manually press a button to apply a senior discount. If you do not ask for it at the beginning of the transaction, you will likely pay full price. Never assume your age or loyalty card triggers the discount automatically .

- Ignoring Tax Phaseout Thresholds: The new $6,000 OBBBA senior deduction is powerful, but it disappears rapidly if your income climbs too high. Pulling too much money out of a traditional IRA for a major purchase could push your MAGI over the $75,000 or $150,000 limit, costing you thousands in lost tax deductions .

- Stockpiling Out of Fear: When news of tariffs hits, the instinct is often to rush out and buy electronics, appliances, or imported goods before prices rise. Hoarding ties up your liquid cash in depreciating assets. Buy what you need, when you need it.

- Letting Flex Card Funds Expire: Medicare Advantage Flex Cards often operate on a “use it or lose it” basis at the end of each month or quarter. Set a calendar reminder to spend your allowance on shelf-stable pantry items before the balance resets to zero.

When to Consult a Professional

While cutting everyday costs is something you can manage on your own, certain financial pivot points require specialized guidance. Consider speaking with a fiduciary financial advisor or a licensed tax professional in the following scenarios:

- You are approaching the OBBBA income thresholds: If your combined income from Social Security, pensions, and required minimum distributions (RMDs) places you near the $150,000 joint or $75,000 single limit, a tax professional can help you utilize Roth conversions or charitable distributions to stay beneath the cap.

- You are evaluating Medicare Advantage plans: Navigating open enrollment is notoriously complex. An independent Medicare broker can review your current prescriptions and compare them against plans offering generous grocery and over-the-counter flex cards.

- You need to restructure your investments for inflation: If your portfolio is too heavy in cash or low-yield bonds, inflation will steadily erode your purchasing power. An advisor can help you properly allocate your assets to generate the growth needed to outpace rising consumer costs.

You have survived turbulent economic cycles before, and you will survive this one. By leveraging your new 2026 tax deductions, claiming the grocery discounts you have earned, and understanding the mechanics behind consumer pricing, you can confidently navigate today’s high-price economy. The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.