Sarasota, Florida, consistently dominates annual “best places to retire” lists, promising sunny beaches and a relaxed lifestyle. But for the average senior, this coastal paradise has transformed into a financial mirage. By mid-2026, the median home price in Sarasota soared past $660,000, while runaway homeowners insurance premiums and escalating healthcare costs have shattered many retirement budgets. If your heart is set on a popular relocation destination, the reality of today’s housing market means you must look far beyond the glossy magazine rankings. We break down the true cost of moving to a top-tier retirement town and provide actionable strategies to protect your savings while finding a destination you can actually afford.

The Financial Reality of Top Retirement Destinations

Florida has long been the gold standard for retirees. Towns like Sarasota, Naples, and even Asheville, North Carolina, built their reputations on offering an exceptional quality of life for older adults. You get walkable downtowns, world-class medical facilities, and communities designed specifically for active seniors. However, popularity comes with a staggering price tag.

During the last few years, a massive influx of out-of-state buyers fundamentally changed the housing landscape. Redfin data from mid-2026 reveals that the median sale price for a home in Sarasota surged to $669,000. If you want a move-in-ready, single-family home near the water or a major cultural hub, you will likely pay significantly more. When you pair a $669,000 mortgage—or even a massive cash outlay—with today’s economic landscape, the math simply stops working for the average retiree. The glossy brochures do not show you the fierce bidding wars, the skyrocketing cost of property maintenance, or the fact that local service providers have had to raise their rates just to survive in the same expensive town.

“Financial security in retirement doesn’t mean you have to be rich. It means you have enough to live the life you want without worrying about running out of money.” — Jean Chatzky, Financial Editor

How Fixed Income Stacks Up Against Rising Costs

To understand why these elite retirement towns are no longer viable for the average senior, you have to look at exactly what money is coming in versus what is going out. Social Security is the bedrock of retirement income for most Americans, but it was never designed to float the cost of luxury coastal real estate.

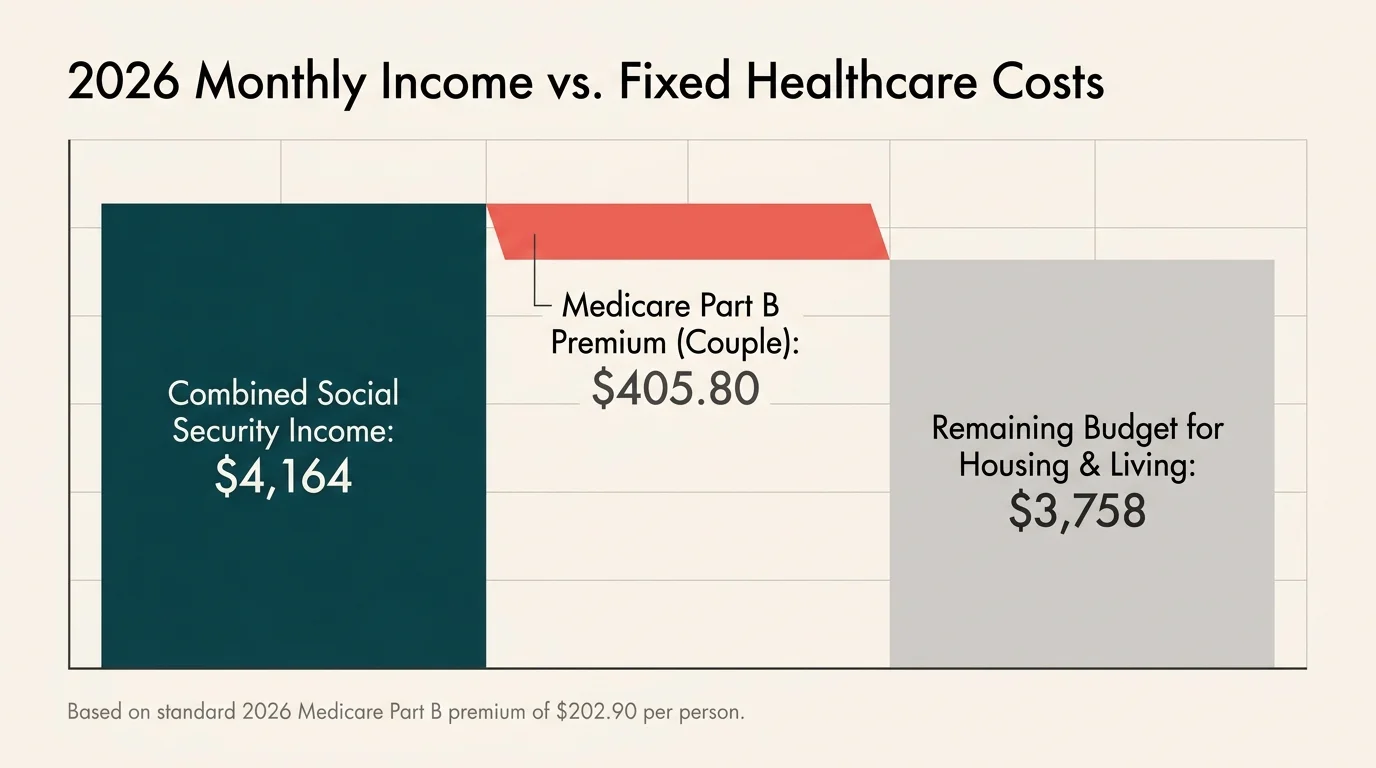

According to the Social Security Administration, the average monthly benefit for a retired worker reached $2,082 in May 2026. If you are part of a married couple where both spouses receive this average benefit, your combined household income from Social Security sits at roughly $4,164 per month. Next, you must deduct your baseline healthcare costs before you spend a single dollar on housing. For 2026, the standard Medicare Part B premium is $202.90 per month, per person. That instantly removes over $405 from a couple’s monthly budget.

This leaves you with about $3,758 per month to cover housing, food, transportation, taxes, and discretionary spending. If you hold a mortgage on a $660,000 home, your monthly payment—including principal, interest, taxes, and insurance—will completely consume, and likely exceed, your remaining Social Security income. Even if you sell your current home and pay cash for your new retirement property, the localized cost of living in a premium destination will drain your investment portfolios much faster than a standard financial plan anticipates.

| 2026 Core Retirement & Healthcare Costs at a Glance | |

|---|---|

| Average Social Security Benefit (Retired Worker) | $2,082 per month |

| Medicare Part B Standard Premium | $202.90 per month |

| Medicare Part B Annual Deductible | $283 per year |

| Medicare Part A Inpatient Deductible | $1,736 per benefit period |

| Medicare Part A Hospital Coinsurance (Days 61-90) | $434 per day |

The Hidden Expenses of Relocating

The purchase price of a home is only the opening act of your financial commitment. When you move to a highly sought-after retirement town, you immediately face a gauntlet of hidden expenses that can destabilize your fixed income.

Property Tax Reassessments

In many states, property taxes are capped for existing homeowners but reset to the current market value the moment a house is sold. You might look at a real estate listing and see that the previous owner paid $2,500 a year in property taxes. Once you purchase that same home for top dollar, the local appraiser will reassess the property, and your tax bill could easily double or triple overnight. Always budget based on the purchase price, not the historical tax record.

Escalating Insurance Premiums

Coastal towns in Florida and mountain towns in the West are grappling with an insurance crisis. Homeowners insurance premiums in places like Sarasota have skyrocketed in recent years. Furthermore, if your home is in a designated flood zone, you are required to purchase separate flood insurance. You must budget for continuous, aggressive rate hikes every single year.

HOA Assessments and Reserves

Many retirees move into managed communities to avoid yard work and exterior maintenance. However, homeowner associations (HOAs) across the country are facing massive funding shortfalls. Due to new state laws regarding structural integrity and reserve funding, HOAs are levying substantial special assessments. A sudden $15,000 bill to repair a community roof or resurface the private roads can instantly derail your annual budget.

What Can Go Wrong

Relocating in retirement is a major life event. When you mix high-cost housing markets with fixed incomes, the margin for error shrinks to zero. Here are the most common mistakes seniors make when chasing a spot on a “best of” list.

- Triggering the IRMAA Cliff: If you sell a highly appreciated family home to fund your move, you might generate a substantial capital gain. While the IRS gives you a primary home exclusion, any gain above that limit increases your Modified Adjusted Gross Income (MAGI). Medicare uses your MAGI from two years prior to determine your Part B and Part D premiums. A massive spike in income from a home sale could trigger the Income-Related Monthly Adjustment Amount (IRMAA), forcing you to pay hundreds of dollars more per month for your medical coverage.

- Buying Before You Rent: Visiting a town for two weeks in the winter is entirely different from living there year-round. Many retirees purchase an expensive home, move all their belongings, and realize six months later that the summer heat is unbearable, the traffic is atrocious, or they simply miss their grandchildren. If you decide to reverse course, the closing costs and real estate commissions will consume a massive chunk of your wealth.

- Misunderstanding Medicare Networks: If you rely on a Medicare Advantage plan, your coverage is heavily tied to your local geographic network. When you move to a new county or state, you trigger a Special Enrollment Period. You must choose a new plan, and the premier doctors or hospital systems in your new expensive town might not be in-network for the affordable plans.

- Falling Victim to Lifestyle Creep: When you move to a wealthy retirement enclave, everything around you is priced for high-net-worth individuals. The local restaurants are pricier, the golf club initiation fees are exorbitant, and the grocery stores cater to luxury tastes. It is incredibly easy to spend an extra $1,000 a month simply by participating in the local culture.

The Silver Lining: 2026 Tax Deductions That Help

While housing and insurance costs are brutal, the federal tax code actually offers some remarkable relief for seniors in 2026. If you manage your location strategy correctly, you can use these deductions to offset the pain of rising living expenses.

The Internal Revenue Service (IRS) adjusted the standard deductions for 2026, and a new piece of legislation has created a massive shelter for retiree income.

For the 2026 tax year, the baseline standard deduction for a married couple filing jointly is $32,200. Because you and your spouse are 65 or older, you each get an additional standard deduction of $1,650, bringing your total to $35,500.

But the biggest news for 2026 is the implementation of a new senior tax deduction. Qualifying taxpayers age 65 and older can claim an additional $6,000 deduction per person. For a married couple filing jointly, that is an extra $12,000.

If your income falls beneath the phase-out limits ($150,000 for joint filers), your total federal deduction before you even need to itemize could reach a staggering $47,500. This means you can pull heavily from your traditional IRAs or 401(k)s to fund your retirement lifestyle without losing a massive percentage to federal income taxes. Properly planning your asset drawdowns around these deductions can free up thousands of dollars a year to help offset the rising costs of housing and healthcare.

“Predicting rain doesn’t count. Building arks does.” — Warren Buffett, Investor and Philanthropist

Practical Strategies for Finding an Affordable Alternative

You do not have to give up your dream of a warm, culturally rich retirement. You simply have to adjust your geographic targeting. Instead of buying into the town printed on the front of the magazine, look for the hidden gems just outside the blast radius of high prices.

Move One County Over

Real estate operates on boundary lines. If you cannot afford Sarasota, look 30 minutes north to Bradenton, or drive further inland. You still get the exact same Florida sunshine, you can still drive to the same beaches, and you have access to the same regional airports. The only difference is your housing cost drops by 20% to 30%. The same rule applies to the Carolinas and the Mountain West.

Follow the Healthcare Footprint

Before you fall in love with a cheaper adjacent town, investigate the healthcare infrastructure. Go to Medicare.gov and research the quality of the local hospitals and the availability of specialists. A town is only a good deal if you can get exceptional medical care within a 30-minute drive. Consider utilizing the Eldercare Locator to find area agencies on aging that can provide insights into local senior services before you move.

Analyze State and Local Taxes

Federal taxes are only one part of the equation. State taxation varies wildly. Nine states have no income tax at all, while others completely exempt Social Security benefits but heavily tax your IRA withdrawals. Make sure your affordable alternative is not secretly clawing back your money through vehicle registration fees, high sales taxes, or steep property taxes. You can often check state-specific benefits through AARP to see how a specific region ranks for retirees.

When to Consult a Professional

Managing a multi-state move while navigating Social Security, Medicare, and investment drawdowns is a complex puzzle. You should reach out to a certified professional if you encounter the following situations:

- You are selling a highly appreciated asset: A tax professional can help you structure the sale of your primary residence to minimize the impact on your Medicare IRMAA calculations.

- You need to transition health coverage: An independent Medicare broker can evaluate the specific medical networks in your new zip code and ensure your prescriptions remain affordable.

- You are considering a new mortgage: A fee-only financial planner can stress-test your portfolio to ensure a new mortgage payment will not deplete your assets if the stock market experiences a prolonged downturn.

Your Next Steps

Relocating in retirement is one of the most exciting decisions you will ever make. While the premier towns on every “best of” list may have priced themselves out of reach, true financial peace of mind comes from living well within your means. By expanding your search radius, managing your tax liabilities, and carefully evaluating hidden costs, you can find a beautiful, vibrant community that protects your wealth and enriches your daily life.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.