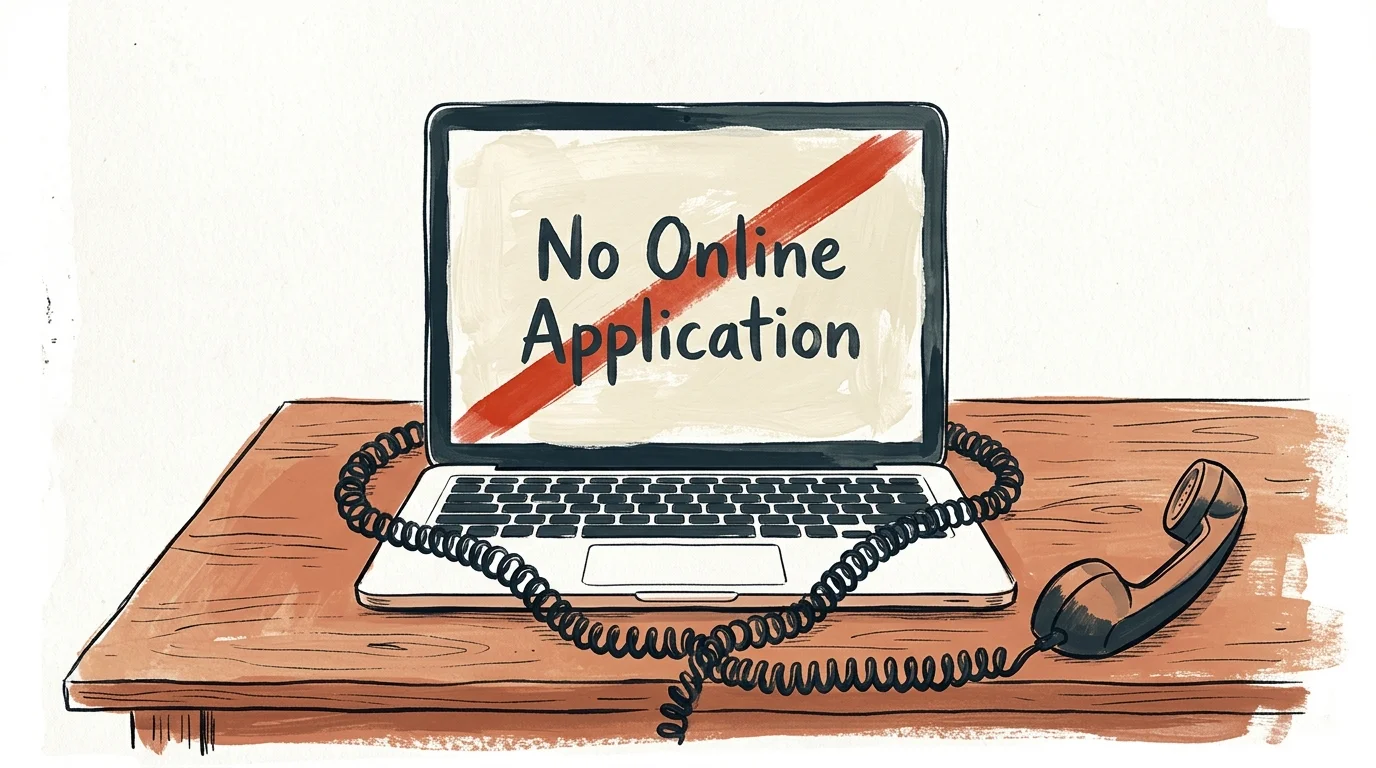

Losing a spouse is a profound emotional blow that instantly alters your financial reality, yet a single procedural hurdle causes thousands of seniors to miss out on critical income when they need it most. Unlike standard retirement claims, you cannot apply for Social Security survivor benefits online. Assuming the process is automatic or entirely digital leads to costly delays that the Social Security Administration will not fully reimburse. To secure your widow or widower benefits, you must manually initiate a telephone or in-person appointment. By understanding the strict timeline, the correct application steps, and how your claiming age affects your payout—ranging from 71.5% to 100% of your late spouse’s benefit—you can protect your financial stability.

The Online Trap That Costs Widows and Widowers Months of Income

When dealing with the aftermath of a spouse’s passing, you likely turn to the internet for answers. The Social Security Administration (SSA) offers a robust online portal for standard retirement and disability applications. Because of this, many surviving spouses naturally assume they can log into their “my Social Security” account, click a button, and convert their spouse’s benefit into a survivor benefit.

This is a costly misconception. The SSA explicitly prohibits online applications for survivor benefits. If you spend weeks waiting for a digital portal to update or assuming your funeral director handled the entire benefit transfer, you lose precious time. While funeral homes report the death to the SSA using the deceased’s Social Security number, this action merely stops the deceased spouse’s monthly checks. It does not automatically start your survivor benefit.

If you delay applying, you lose money. Social Security limits retroactive pay. If you wait six months to realize your benefits did not automatically start, you may forfeit thousands of dollars in lost income. You must actively claim what belongs to you by calling the SSA at 1-800-772-1213 to schedule a phone interview or an in-person appointment at your local office.

How Social Security Survivor Benefits Are Calculated

To make informed decisions about your financial future, you need to understand how the SSA calculates your monthly check. Survivor benefits are based on the earnings of the person who died. The more they paid into Social Security, the higher your survivor benefit will be.

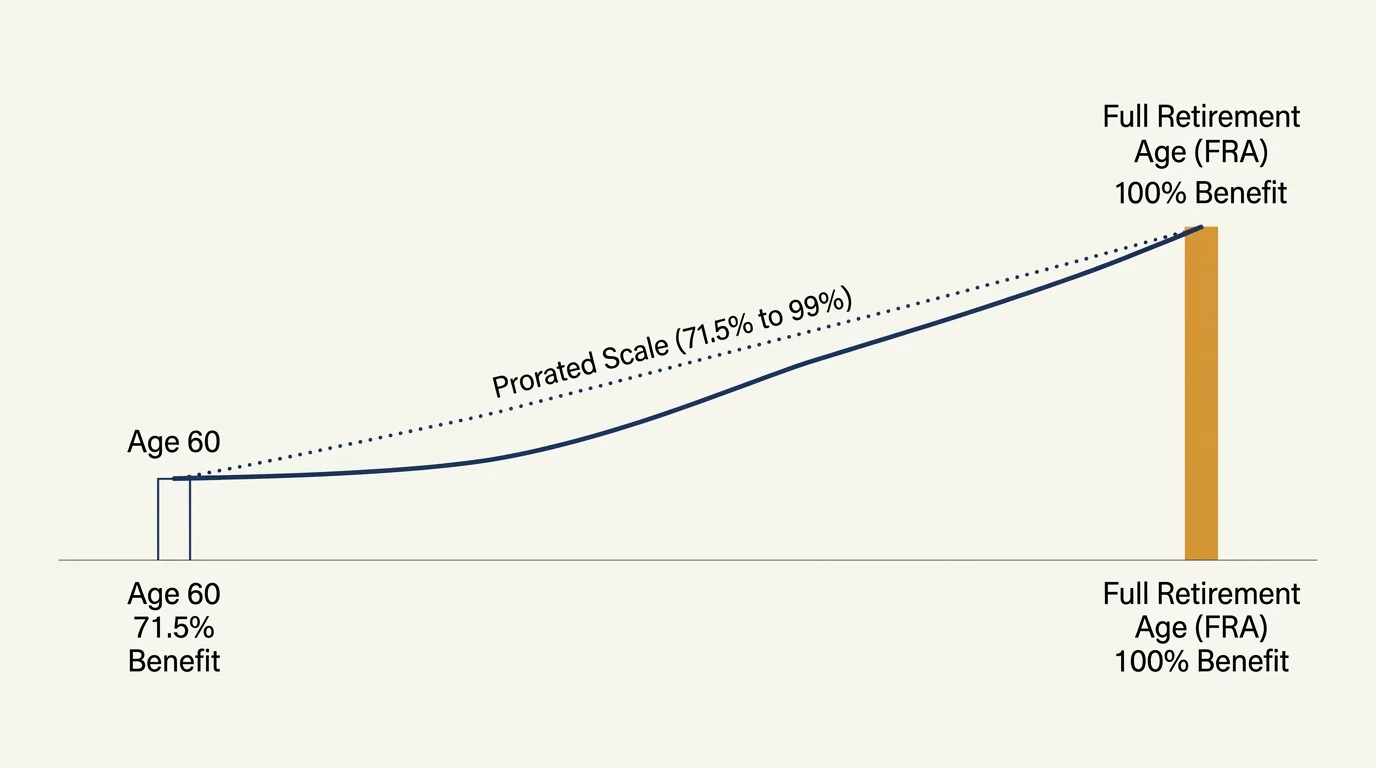

Your claiming age dictates the exact percentage of your late spouse’s Primary Insurance Amount (PIA) you receive. For example, the 2026 Cost-of-Living Adjustment (COLA) increased standard benefits by approximately 2.8%. This increase is permanently baked into your late spouse’s baseline benefit, which directly inflates the survivor payout you receive.

Here is how your age affects your monthly compensation:

| Your Claiming Age | Percentage of Survivor Benefit Received | Who It Makes Sense For |

|---|---|---|

| Age 50 to 59 (Disabled) | 71.5% | Disabled widows or widowers who cannot work and require immediate financial assistance. |

| Age 60 | 71.5% | Surviving spouses who have stopped working and need cash flow to cover daily living expenses. |

| Between Age 60 and FRA | 71.5% to 99% (prorated) | Those balancing part-time work with the need for supplemental income before reaching full retirement age. |

| Full Retirement Age (FRA)* | 100% | Seniors who can afford to wait, allowing them to capture the maximum possible monthly survivor benefit. |

*Note: Full Retirement Age is 67 for anyone born in 1960 or later. If you were born earlier, your FRA may be 66 and a certain number of months. Check with the SSA for your exact FRA.

The Exact Step-by-Step Application Process

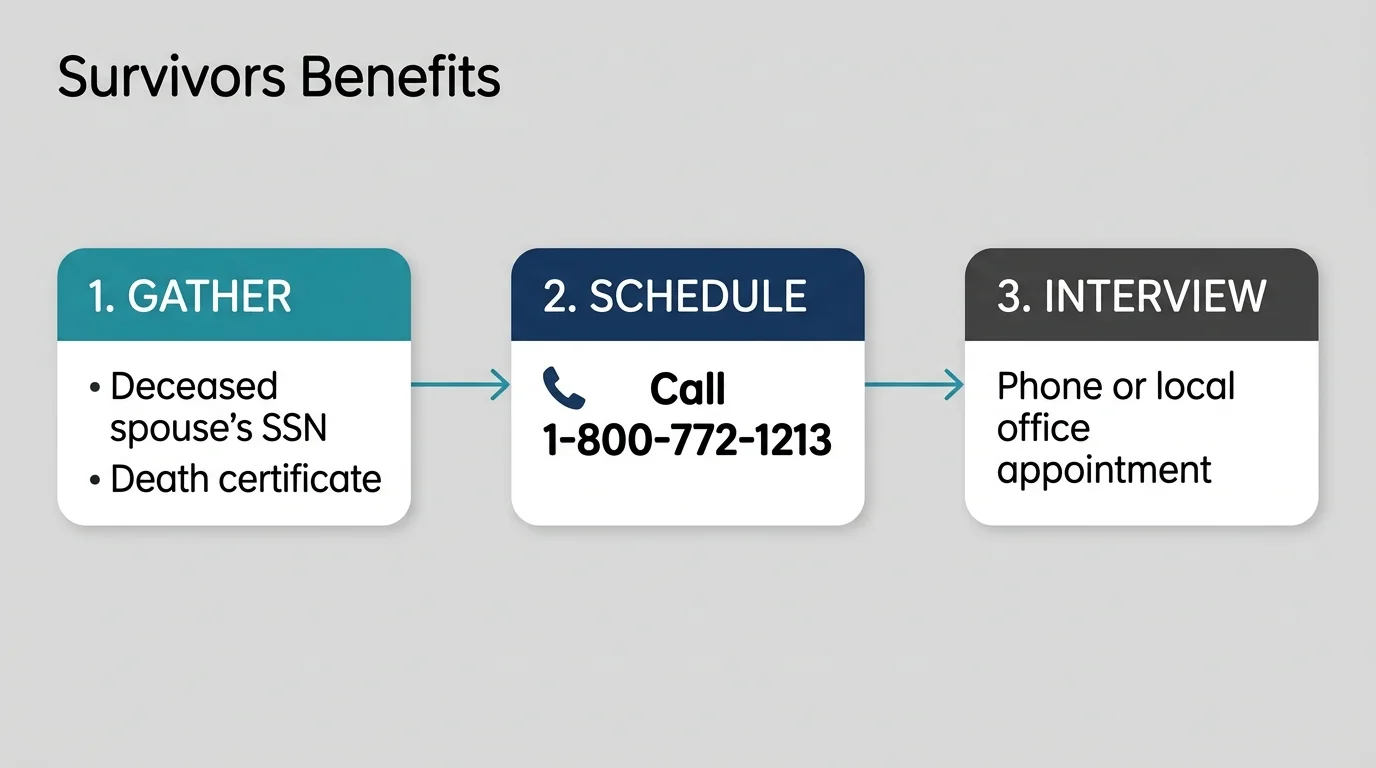

Knowing you must call the SSA is only the first step. Navigating the actual bureaucracy requires preparation. Gathering your documentation before you make the call prevents administrative delays and ensures your claim is processed rapidly.

- Verify the Death Has Been Reported: Usually, the funeral home handles this by providing the deceased’s Social Security number to the SSA. However, you should still call the SSA directly to confirm they have the record of death. This stops any overpayments that you would otherwise have to pay back.

- Schedule Your Appointment: Call 1-800-772-1213. Do not walk into a local SSA office without an appointment, as wait times can span several hours. The representative will schedule a dedicated time for a claims specialist to call you or meet with you.

- Gather Your Core Documents: The SSA requires proof of identity, marriage, and death. Assemble original copies (or certified copies from the issuing agency) of the following:

- Your birth certificate or other proof of birth

- Proof of U.S. citizenship or lawful alien status

- The deceased worker’s death certificate

- Your marriage certificate

- The deceased’s W-2 forms or federal self-employment tax return for the most recent year

- Final divorce decree, if you are applying as a surviving divorced spouse

- Claim the $255 Lump-Sum Death Payment: In addition to monthly survivor benefits, the SSA provides a one-time death payment of $255 to the surviving spouse who lived with the deceased. You must apply for this payment within two years of the date of death. Even if you were already receiving spousal benefits and your monthly check automatically converted to a survivor check, you still must contact the SSA to claim this $255 payment.

What Can Go Wrong: Avoiding Common Mistakes

Navigating the transition to a single-income household leaves little room for financial error. When applying for survivor benefits, widows and widowers frequently make administrative and strategic mistakes that permanently lower their lifelong income.

Failing the Social Security Earnings Test

If you claim survivor benefits before your Full Retirement Age and continue to work, your income is subject to the Social Security earnings limit. In 2026, the SSA withholds $1 in benefits for every $2 you earn above the strict $24,480 annual limit. Many younger widows claim at age 60, continue working full-time, and are shocked when the SSA temporarily freezes their checks. Once you reach your FRA, this earnings limit disappears completely, and you can earn unlimited income without penalty.

Mishandling the “Switching Strategy”

You cannot receive both your own retirement benefit and a survivor benefit simultaneously; the SSA pays you the higher of the two amounts. However, you have the right to sequence them. A common mistake is claiming whichever benefit is currently higher right away, without looking at the long-term math.

A smarter strategy often involves claiming the reduced survivor benefit at age 60 (or 62) while letting your own personal retirement benefit grow at 8% per year up until age 70. At age 70, you switch to your own maxed-out benefit. Conversely, if your late spouse was the higher earner, you might claim your own reduced benefit early, and switch to their 100% survivor benefit when you reach your FRA. Discussing these timing options with a professional ensures you do not leave money on the table.

Remarrying Before Age 60

Remarriage directly impacts your eligibility for survivor benefits. If you remarry before you turn 60 (or 50 if you are disabled), you forfeit your right to collect benefits on your deceased spouse’s record. However, if you remarry after age 60, your survivor benefits remain completely intact. Understanding this timeline is crucial for widows and widowers planning to rebuild their lives with a new partner.

When to Consult a Professional

While the actual application process is free and straightforward once you secure an appointment, deciding when to apply requires strategic financial planning. Consider consulting a fiduciary financial advisor or a Social Security specialist in the following scenarios:

- You are a Surviving Divorced Spouse: If your marriage lasted 10 years or longer, you are entitled to the same survivor benefits as a current spouse, provided you meet the other age and remarriage requirements. A professional can help you navigate the specific documentation required to prove the length of the marriage.

- You Have a Complex Tax Situation: Survivor benefits can push you into a higher tax bracket, especially when combined with required minimum distributions (RMDs) from inherited IRAs. The “Tax Torpedo” is a real threat where a larger Social Security check causes a higher percentage of your benefits to become taxable.

- You Need to Coordinate Medicare Premiums: Medicare Part B premiums are deducted directly from your Social Security check. If your overall household income spikes due to life insurance payouts or inherited account withdrawals, you could face the Income-Related Monthly Adjustment Amount (IRMAA) surcharge, which significantly reduces your net survivor check.

“If you’re winging your retirement spending… that’s a big mistake. You need a concrete plan for how you’ll use that money.” — Jean Chatzky, Financial Editor and Author

Frequently Asked Questions

Can I apply for survivor benefits online if I am already receiving retirement benefits?

No. Regardless of your current benefit status, you cannot apply for survivor benefits online. You must call the SSA at 1-800-772-1213 to schedule a specialized appointment.

Are Social Security survivor benefits taxable?

Yes. Just like standard retirement benefits, up to 85% of your survivor benefits may be subject to federal income tax if your combined income exceeds the IRS thresholds ($25,000 for a single filer). Check current tax guidelines at IRS.gov to calculate your specific liability.

Does the 2026 COLA apply to my survivor benefits?

Yes. The annual Cost-of-Living Adjustment (COLA), which sits around 2.8% for 2026, applies to the deceased worker’s primary insurance amount. This permanently raises the baseline figure used to calculate your percentage payout.

What if I am already receiving spousal benefits when my spouse dies?

If you are already receiving spousal benefits on your partner’s record, the SSA will automatically convert your spousal benefit into a survivor benefit once they process the death report. However, you still must contact the SSA to manually apply for the $255 one-time death payment.

Securing Your Financial Future

Losing your spouse forces you to navigate overwhelming grief while simultaneously managing complex financial transitions. Taking immediate, decisive action to secure your survivor benefits protects your household income and gives you the breathing room to plan your next steps.

Remember that the system will not optimize your payout for you. Pick up the phone, schedule your appointment, and bring the necessary documentation. By taking control of the process, you honor the hard work your spouse put into building that safety net for you.

“After suffering the loss of a loved one, do nothing but keep your money safe and sound for at least one year. If you want to find the best financial advisor, look in the mirror—for no one will care about your money more than you do.” — Suze Orman, Personal Finance Expert

Disclaimer: This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Helpful Resources

- Social Security Administration: Official Survivor Benefits Guide

- Medicare.gov: Managing Your Health Coverage

- Internal Revenue Service (IRS): Tax Information for Seniors & Retirees

- National Council on Aging (NCOA): Financial Security Resources