Protecting your hard-earned savings requires choosing a retirement town that actively minimizes your total tax burden rather than just your income tax. For 2026, finding the most affordable places to retire means evaluating the combined impact of property levies, sales taxes, and how a state treats your Social Security and pension withdrawals. A location boasting zero income tax might quietly drain your budget through exorbitant property assessments or high local sales percentages. By analyzing the complete financial picture—including current standard deductions and state-specific exemptions—you can strategically select a destination that stretches your money further. The following guide reveals the U.S. towns offering the absolute lowest combined tax liabilities for retirees this year.

Quick Summary: The 2026 Retirement Tax Landscape

Relocating for retirement is a major financial decision. Before packing your boxes, you need a clear understanding of how state and local governments collect revenue. In 2026, the tax rules have shifted slightly, and knowing the baseline facts will help you evaluate any destination:

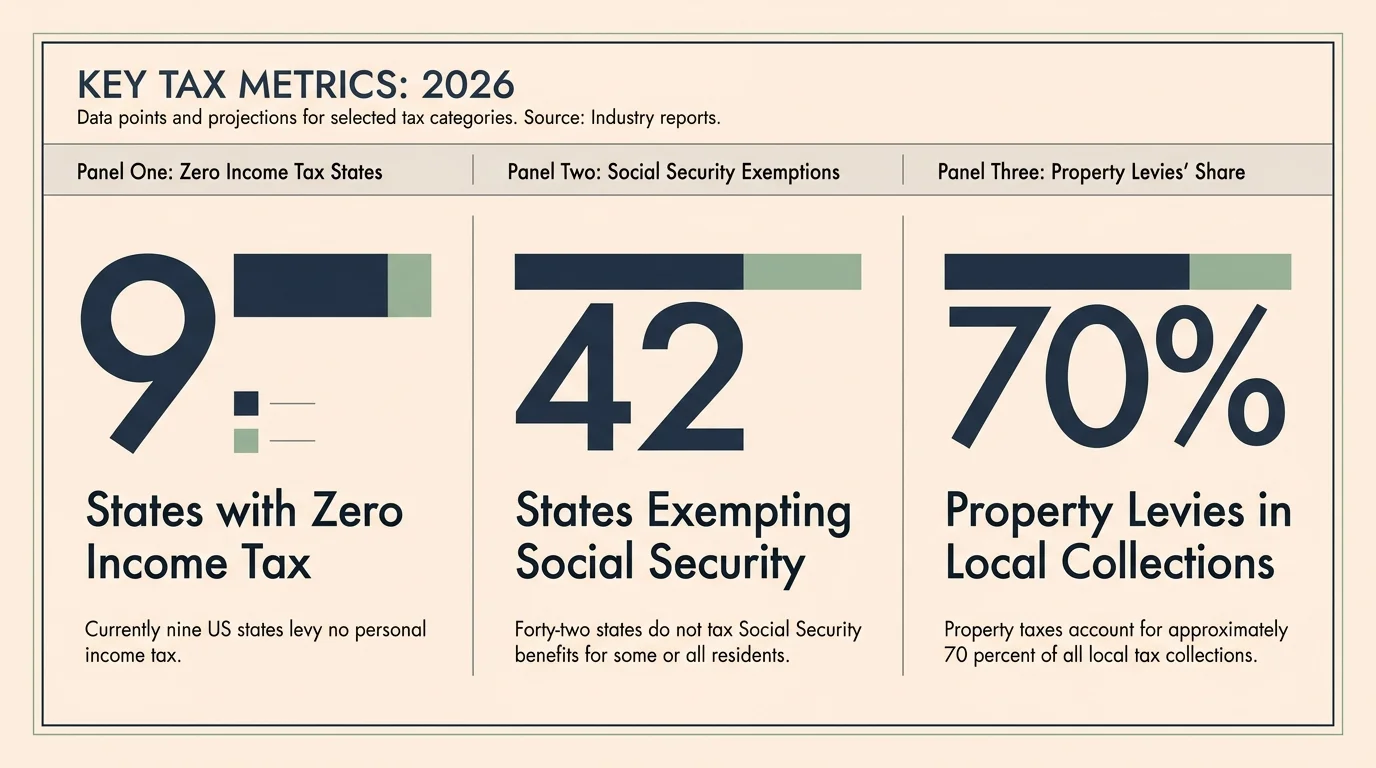

- Nine states charge zero state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

- Social Security is mostly safe: As of 2026, 42 states plus the District of Columbia fully exempt Social Security benefits from state taxation. Only eight states still tax these benefits.

- Property taxes are the silent budget killer: Local property levies account for roughly 70% of local government tax collections. A high property tax rate can easily erase the savings you gain from moving to a state with no income tax.

- New federal deductions are available: For tax years 2025 through 2028, seniors age 65 and older benefit from an enhanced federal tax deduction that significantly raises the threshold for taxable income.

Why “No Income Tax” Does Not Tell the Whole Story

Many retirees simply search for states with no income tax and stop their research there. This approach is a common and expensive mistake. State and local governments must fund their roads, schools, and emergency services somehow. If they do not collect revenue through an income tax, they will aggressively collect it through other channels.

Consider Texas as an example. The state proudly advertises zero personal income tax. However, the effective property tax rate in many Texas counties hovers around 1.31% to 1.8% of a home’s assessed value. If you purchase a $400,000 home, you could easily pay $6,000 to $7,200 annually just in property taxes. Over a twenty-year retirement, that single tax liability exceeds $120,000—often costing more than what you would have paid in a state with a moderate income tax and lower property assessments.

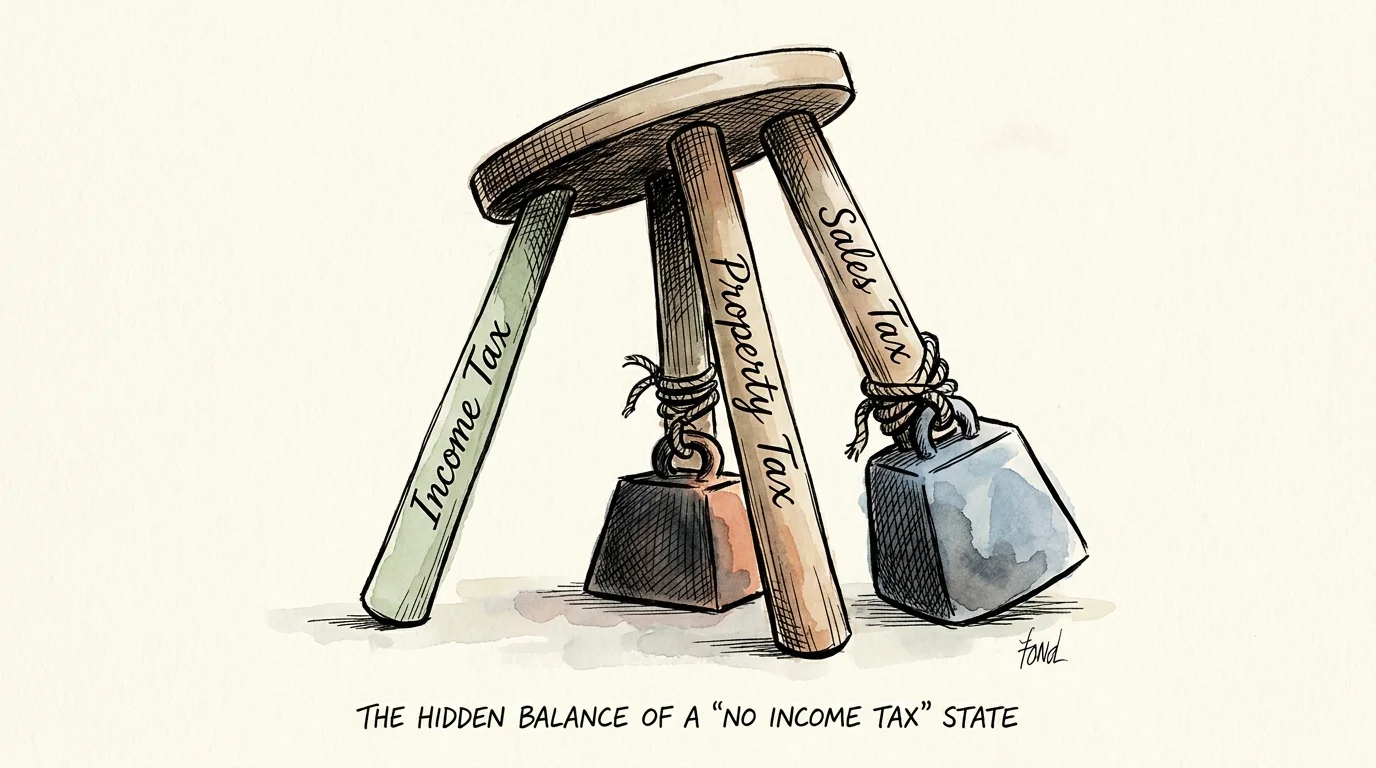

When evaluating a retirement destination, you must analyze the “three-legged stool” of taxation:

- State and Local Income Tax: How does the state tax your pension, 401(k) distributions, and part-time wages?

- Property Tax: What is the effective local rate, and does the state offer a permanent property tax freeze or substantial homestead exemption for residents over age 65?

- Sales and Use Tax: What is the combined state and local sales tax rate, and does it apply to essentials like groceries, clothing, or prescription medications?

Top Retirement Towns With the Lowest Combined Tax Burden

Finding the perfect balance requires pinpointing specific cities that keep all three legs of the tax stool as low as possible. Based on 2026 tax codes, exemptions, and local assessment data, here is the full list of retirement towns offering the lowest overall tax burden for seniors.

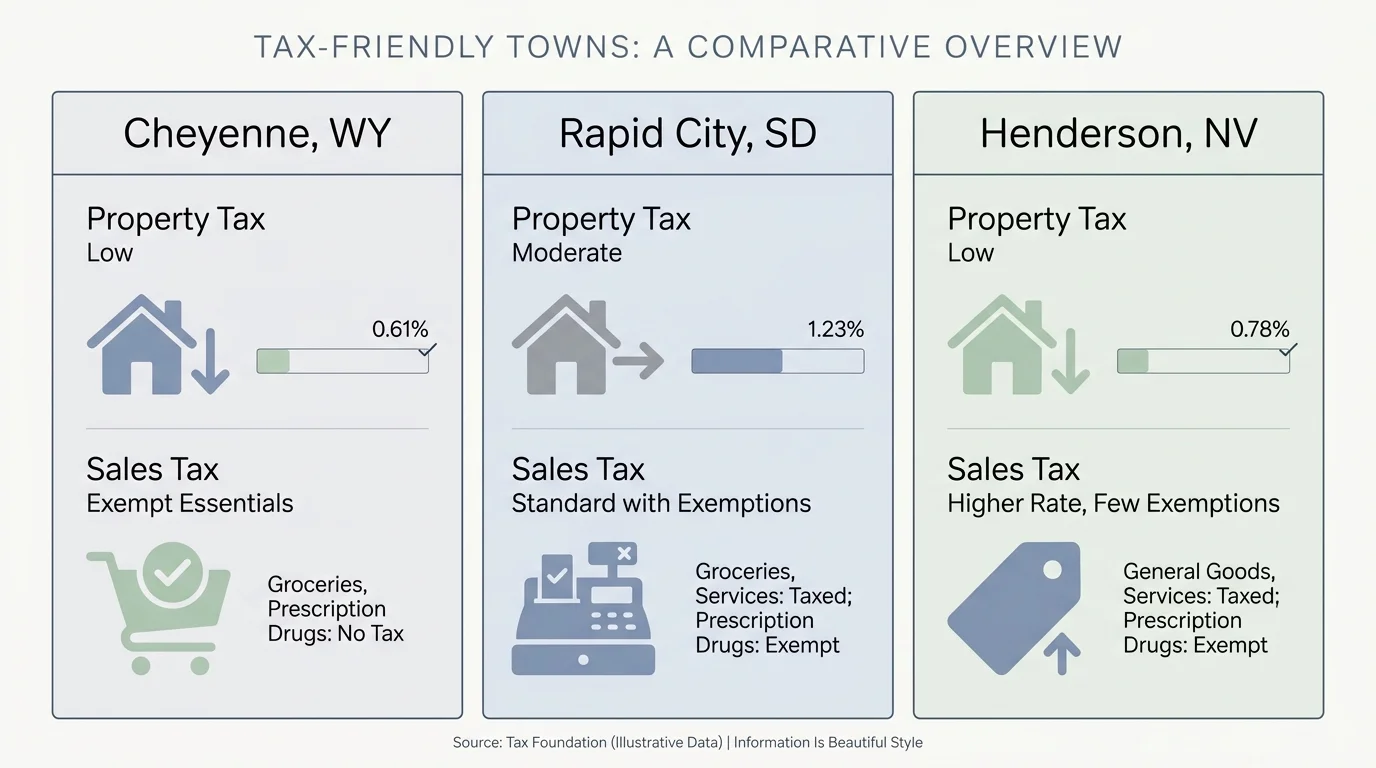

1. Cheyenne, Wyoming

Wyoming consistently ranks as one of the most tax-friendly states for retirees, and its capital, Cheyenne, offers excellent amenities without the heavy financial penalties found in coastal states. Wyoming levies no personal income tax, meaning your Social Security, pensions, and IRA withdrawals are entirely yours to keep. The state sales tax sits at a very manageable 4%, though local municipalities can add a small percentage.

Where Cheyenne truly shines is its approach to property taxes. The statewide effective property tax rate is roughly 0.61%, one of the lowest in the nation. Furthermore, Wyoming offers specific property tax relief programs for seniors that can shield a portion of your home’s assessed value if you meet residency requirements. Cheyenne provides a high quality of life, excellent outdoor recreation, and a cost of living that keeps your retirement budget intact.

2. Henderson, Nevada

Located just outside the hustle and bustle of Las Vegas, Henderson offers a quiet, master-planned community lifestyle with massive tax advantages. Like Wyoming, Nevada has zero state income tax. It also does not tax Social Security or pension income.

Nevada’s property tax structure is exceptionally favorable to retirees. The effective property tax rate averages around 0.50%, and state law strictly caps how much property tax bills can increase year over year, protecting you from sudden spikes if housing prices soar. The trade-off in Henderson is the sales tax, which climbs above 8% when local surcharges are applied. If you plan to spend heavily on retail goods, this will impact you. However, if your budget focuses on services, groceries, and healthcare, Henderson remains a top-tier financial haven.

3. Lewes, Delaware

Delaware is famously known as a corporate tax haven, but it is equally advantageous for retirees. The coastal town of Lewes offers historic charm, beautiful beaches, and a remarkably low tax footprint. Delaware does levy a progressive state income tax (up to 6.6%), which deters some people who only look at surface-level numbers. However, the state completely exempts Social Security benefits. More importantly, Delaware offers a generous pension and retirement income exclusion up to $12,500 for residents aged 60 and older.

Delaware truly wins with its other taxes. The state has absolutely zero sales tax. The effective property tax rate in Delaware is roughly 0.47%, tying it for one of the lowest property tax burdens in the country. Retirees in Lewes enjoy beachfront living without the crushing property taxes associated with similar towns in New Jersey or Maryland.

4. Sioux Falls, South Dakota

South Dakota is a powerhouse for wealth preservation. Sioux Falls provides world-class healthcare facilities, a vibrant downtown, and four distinct seasons for those who enjoy the Midwest. The state has no income tax, no tax on Social Security, and no inheritance or estate tax.

The effective property tax rate in South Dakota sits around 1.02%. While higher than Delaware or Nevada, the median home price in Sioux Falls is significantly lower than the national average, meaning your actual out-of-pocket tax payment remains quite small. The state sales tax is a low 4.5%, and local municipal rates rarely push the combined total above 6.5%. For retirees focused on legacy planning and stretching fixed incomes, Sioux Falls is incredibly efficient.

5. Lancaster, Pennsylvania

Pennsylvania might seem like a strange addition to a low-tax list because it carries a flat state income tax of 3.07%. However, the state treats seniors exceptionally well. Pennsylvania completely exempts all eligible retirement income from state taxes. This means your Social Security, 401(k) distributions, pensions, and IRA withdrawals are 100% tax-free at the state level. If you stop working entirely in retirement, your effective state income tax rate in Pennsylvania is zero.

Lancaster offers rolling farmland, a low cost of living, and proximity to major East Coast cities. Property taxes in Pennsylvania are slightly higher than average, but Lancaster’s affordable housing market balances the equation. The state also exempts necessities like clothing and groceries from its 6% sales tax, keeping your daily living expenses remarkably low.

6. Sarasota, Florida

Florida is the traditional capital of American retirement for good reason. It features no state income tax, meaning your retirement distributions and Social Security are completely untouched. Sarasota provides unmatched cultural amenities, pristine beaches, and a massive community of fellow seniors.

The effective property tax rate in Florida is about 0.89%. The state also offers the famous “Save Our Homes” cap, which limits the annual increase in the assessed value of a primary residence to 3% or the inflation rate, whichever is lower. This provides excellent long-term budget predictability. However, when moving to Sarasota, you must factor in the rapidly rising cost of homeowner’s insurance, which has become a significant financial burden that offsets some of the state’s tax advantages.

At a Glance: Comparing the Top Tax-Friendly Towns

Use the table below to compare the baseline tax data for our top recommended retirement towns in 2026. Remember, local municipalities may add small percentages to property and sales taxes.

| Town & State | State Income Tax | Avg. Property Tax Rate | State Sales Tax | Taxes Social Security? |

|---|---|---|---|---|

| Cheyenne, WY | 0% | ~0.61% | 4.0% | No |

| Henderson, NV | 0% | ~0.50% | 6.85% | No |

| Lewes, DE | Up to 6.6% | ~0.47% | 0% | No |

| Sioux Falls, SD | 0% | ~1.02% | 4.5% | No |

| Lancaster, PA | 3.07% | ~1.3% | 6.0% | No |

| Sarasota, FL | 0% | ~0.89% | 6.0% | No |

The 2026 Senior Tax Deductions You Cannot Afford to Miss

Before worrying entirely about state taxes, you must ensure you are maximizing your federal tax efficiency. For 2026, the federal government offers several stacked deductions that can drastically reduce the taxes you pay on your retirement withdrawals.

First, the baseline standard deduction for a married couple filing jointly in 2026 is $32,200. However, if you and your spouse are 65 or older, you qualify for an additional standard deduction that adds roughly $1,600 per person to that total.

Furthermore, under recent tax legislation extending through 2028, eligible seniors can claim an enhanced bonus deduction of up to $6,000 per person ($12,000 for a married couple filing jointly). When combined, a married couple over the age of 65 can shield over $46,000 of their income from federal income taxes entirely. You should verify current tax brackets and deduction limits directly with the Internal Revenue Service (IRS) each spring.

“It is a ticking time bomb. It is the tax in your IRAs and 401(k)s. That money has not yet been taxed. It is tax-deferred, not tax-free. And with taxes probably going up very soon, a lot of that could be lost when you need the money the most in retirement.” — Ed Slott, CPA and Retirement Tax Expert

As Slott warns, deferring taxes during your working years creates a liability in retirement. By combining federal deductions with a move to a tax-friendly state, you can defuse this tax bomb and keep more of your wealth.

State-by-State Breakdown: Social Security Taxation in 2026

For decades, many states taxed Social Security benefits, adding a painful secondary tax on top of federal obligations. Fortunately, advocacy efforts have led to widespread tax reform. In 2026, 42 states—including recent additions like West Virginia, Kansas, and Missouri—no longer tax your Social Security benefits.

If you rely heavily on your monthly benefits, you should completely avoid the eight states that still tax Social Security in 2026. They are:

- Colorado: Taxes benefits, but offers an exemption up to $24,000 for those 65 and older.

- Connecticut: Fully taxes benefits unless your income falls below a strict threshold.

- Minnesota: Offers a partial subtraction, but high earners will pay state tax on their benefits.

- Montana: Taxes benefits based on federal taxable thresholds.

- New Mexico: Provides exemptions for lower-income seniors, but upper-middle-class retirees will face taxation.

- Rhode Island: Exempts benefits only for those with adjusted gross incomes below specific state caps.

- Utah: Offers a non-refundable retirement tax credit, but still taxes benefits for many residents.

- Vermont: Fully exempts benefits only if your income falls below certain thresholds; taxes phase in quickly for middle earners.

Always review your specific benefit structure directly through the Social Security Administration (SSA) to understand how federal and state taxes will impact your net monthly check.

What Can Go Wrong: Costly Mistakes Seniors Make When Relocating

Moving across the country to save money requires meticulous planning. Far too many seniors make emotional decisions based on surface-level tax rates, only to discover hidden costs that destroy their budgets. Avoid these four common blunders:

1. Ignoring the IRMAA Surcharge

Moving to a state with zero income tax does not protect you from federal healthcare surcharges. The Income-Related Monthly Adjustment Amount (IRMAA) is a federal surcharge added to your Medicare Part B and Part D premiums if your income crosses certain thresholds. The government calculates IRMAA based on your tax return from two years prior. If you liquidate a large taxable portfolio or sell an expensive home in a high-tax state to fund your move, the resulting income spike could trigger massive IRMAA penalties two years later. You can review current premium thresholds at Medicare.gov.

2. Buying Before Renting

Never buy a home in a new state without living there first. You might fall in love with a low-tax town on paper, only to discover you hate the summer humidity, the local traffic, or the distance from major airports. Renting for six to twelve months allows you to establish residency, enjoy the tax benefits immediately, and take your time finding the perfect neighborhood without locking up your liquidity.

3. Forgetting About Homeowner’s Insurance and HOAs

A state might have low property taxes, but environmental risks can make up the difference. Florida and Texas both offer excellent tax benefits, but both states are experiencing severe homeowner’s insurance crises. If you save $3,000 a year in property taxes but your insurance premium jumps by $4,500, you have lost money on the move. Similarly, many low-tax towns rely on massive Homeowner Associations (HOAs) to fund local infrastructure. High HOA fees act exactly like a localized tax.

4. Overlooking Healthcare Access

Many hyper-affordable, low-tax towns are located in rural areas. While the cost of living is fantastic, the proximity to specialized medical care is not. As you age, access to top-tier cardiologists, orthopedic surgeons, and comprehensive hospital systems becomes your most valuable asset. Do not move to a low-tax county if it puts you an hour away from the nearest emergency room. You can use resources like Benefits.gov to explore local senior assistance programs before committing to a zip code.

When to Consult a Professional

You should not navigate interstate tax strategy alone if you have complex assets. Consider hiring a fee-only fiduciary financial advisor or a Certified Public Accountant (CPA) if you encounter any of the following scenarios:

- You own a business or real estate in your previous state: Simply moving your primary residence does not stop your old state from taxing the income generated by assets left behind. A CPA can help you restructure your portfolio to avoid double taxation.

- You plan to execute large Roth conversions: Shifting funds from a traditional IRA to a Roth IRA generates immediate taxable income. A professional can help you time these conversions strategically after you establish residency in a low-tax state, maximizing your savings.

- You have a large, highly appreciated taxable brokerage account: Capital gains taxes vary wildly by state. Washington, for example, has no personal income tax but imposes a 7% tax on capital gains exceeding a quarter of a million dollars. An advisor can sequence your sell-offs to minimize this burden.

Relocating to a tax-friendly town is one of the most effective ways to preserve your wealth and reduce financial stress in your golden years. By carefully evaluating property taxes, sales taxes, and retirement income exemptions, you can confidently choose a destination that supports the lifestyle you have spent decades building. Take your time, run the numbers on your specific income streams, and build a retirement plan that keeps your money in your pocket.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.