Opening your mail to find a $14,000 overpayment demand letter from the Social Security Administration can cause immediate panic, but you have clear legal avenues to fight it or reduce the payments. Under 2026 federal rules, you must take action within 30 days to prevent the government from automatically withholding up to 50 percent of your monthly check. Whether the agency made a calculation error or you unknowingly exceeded an income limit, you do not have to accept a devastating financial blow. By submitting the correct waiver or appeal forms, you can halt the collection process entirely while your case is reviewed or lock in a manageable repayment plan spread over 60 months.

Understanding Why the Government Is Asking for Your Money Back

Social Security overpayments occur when the government determines it paid you more money than you were legally entitled to receive. The sheer size of these letters often leaves retirees in disbelief. A $14,000 demand rarely stems from a single massive mistake; rather, it typically represents years of small monthly miscalculations that quietly compounded before the agency’s computer systems caught the discrepancy.

The rules governing benefit amounts are incredibly complex, and errors can originate from either side. If you claimed early retirement benefits but continued working, you are subject to an annual earnings limit. Earning just a few thousand dollars over that limit can trigger a clawback. For those receiving Supplemental Security Income (SSI), strict asset limits dictate eligibility. A small inheritance, a change in your marital status, or even a well-meaning family member depositing funds into your bank account can push you over the threshold.

With the 2026 Cost-of-Living Adjustment (COLA) set at 2.8 percent, the average monthly retirement benefit sits at $2,026 according to the Social Security Administration (SSA). When benefit amounts rise, the penalty for undetected errors scales up alongside them. Sometimes, the fault lies entirely with the agency. Missing data, delayed processing times, or overlapping records can cause the government to issue payments you never requested. Regardless of who caused the error, federal law requires the agency to attempt to recover the funds.

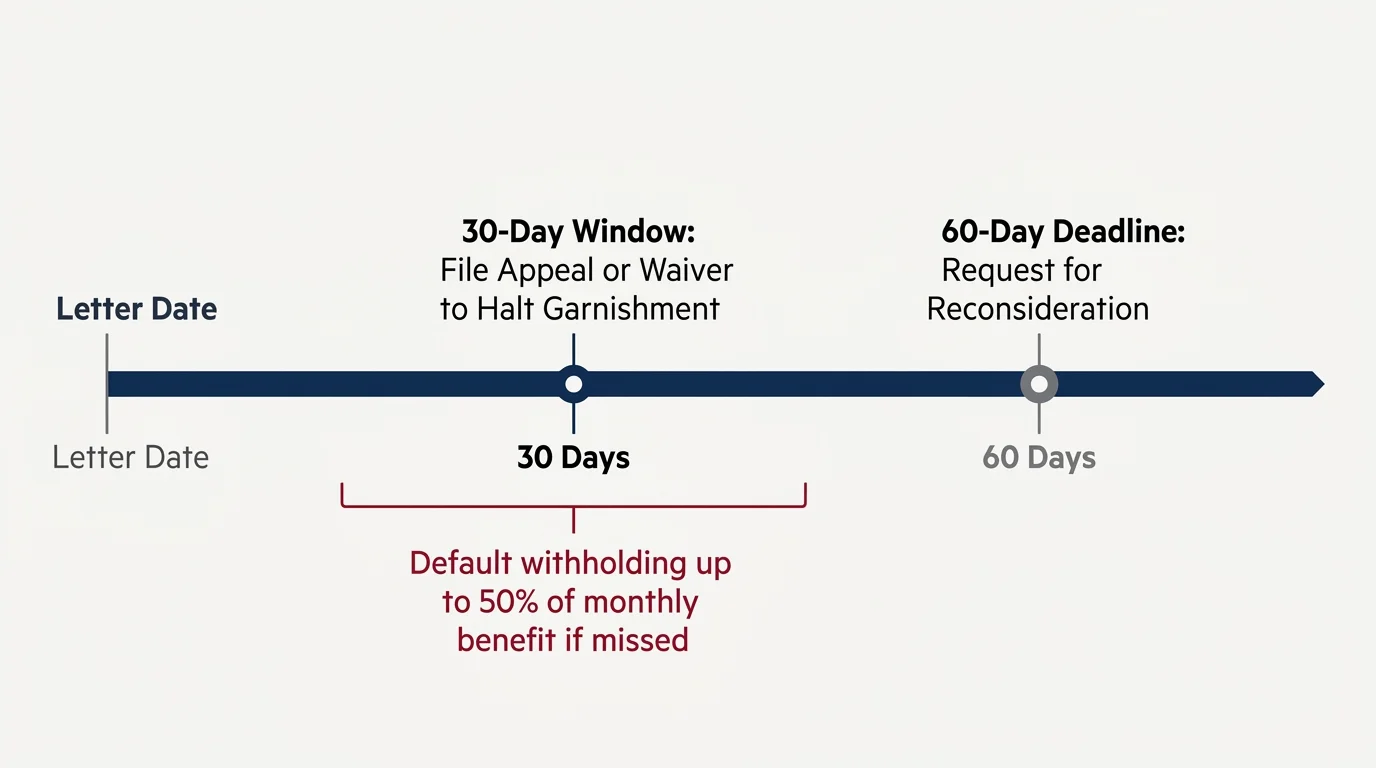

The 30-Day Rule: Your Crucial Window to Stop Garnishment

Time is your most valuable asset when dealing with a federal demand letter. The SSA gives you a specific grace period, but it moves much faster than most retirees realize. Your timeline revolves around two critical deadlines:

- The 30-Day Window: If you file an appeal or a waiver request within 30 days of the date printed on your letter, the SSA cannot start garnishing your checks. Your benefits remain completely untouched while the agency reviews your case.

- The 60-Day Deadline: You have a legal maximum of 60 days to file a formal Request for Reconsideration. If you miss this deadline, you forfeit your right to argue that the debt amount is incorrect.

If you fail to act within the initial 30 days, current 2026 rules dictate that the SSA will automatically default to withholding up to 50 percent of your monthly Title II retirement or disability benefit. For SSI recipients, the default withholding rate is capped at 10 percent of your monthly payment. Do not wait for the mail system to deliver a physical response. Utilize the digital upload tools inside your online “My Social Security” portal to submit your documents. Digital submissions generate an instant, timestamped receipt proving you met the deadline.

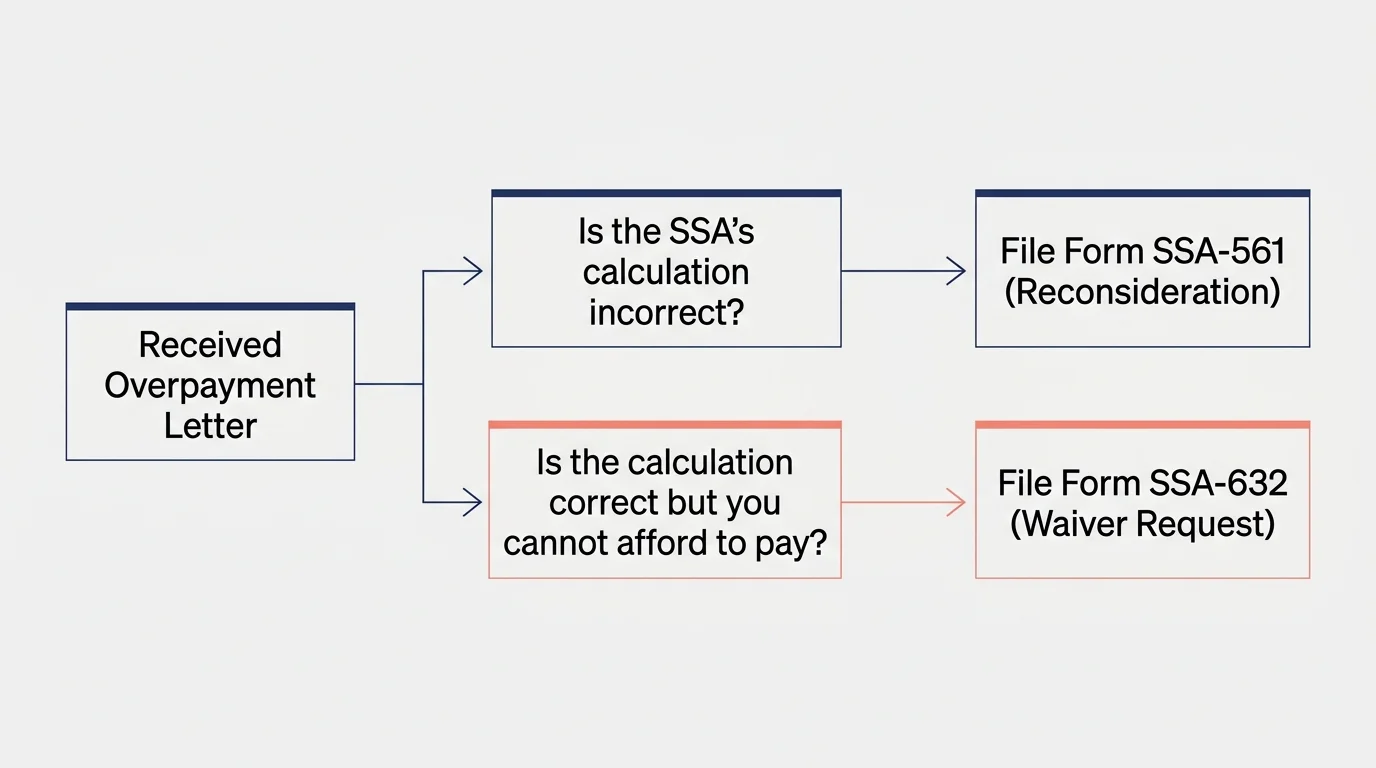

Step 1: File for Reconsideration When the Agency Is Wrong

If you look at the demand letter and immediately realize the government made a factual mistake, you need to file Form SSA-561, the Request for Reconsideration. This form tells the government that you dispute the existence of the debt or the specific dollar amount they are claiming.

Factual errors happen frequently. The agency’s automated systems sometimes flag income that does not actually count toward the earnings limit, such as vacation pay earned in a previous year or a one-time payout from a life insurance policy. In other instances, the SSA might have failed to record a critical life event you reported months ago.

When filling out Form SSA-561, you must be specific. Writing “I do not owe this” will not resolve your case. Instead, provide concrete evidence. For example, you should write, “The SSA claims I earned $4,000 in June 2025, but my attached W-2 and pay stubs prove my earnings were only $1,200.” Gather your bank statements, tax returns from the Internal Revenue Service (IRS), and correspondence from former employers to build an airtight defense. Attach these directly to your appeal.

Step 2: Request a Waiver if You Cannot Afford Repayment

Sometimes, the math on the demand letter is perfectly accurate. You were overpaid, but you had absolutely no idea it was happening. If repaying the debt would destroy your financial security, you must file Form SSA-632, the Request for Waiver of Overpayment Recovery.

To win a waiver, you must successfully prove two distinct things to the government:

- You were “without fault”: You must demonstrate that you did not intentionally hide information, provide false statements, or ignore reporting requirements. If you thought the checks you received were accurate based on the information you provided, you meet this standard.

- Repayment would “defeat the purpose” of the program: You must prove that garnishing your checks would leave you unable to meet your ordinary and necessary living expenses.

Form SSA-632 is exhaustive. It requires a detailed breakdown of your household finances, including your rent or mortgage, utility bills, food costs, and medical out-of-pocket expenses. You must also disclose your assets. If you have substantial funds sitting in a savings account, the SSA will likely deny the waiver, arguing that you have the capacity to repay the debt without facing extreme hardship. Be honest and thorough; leaving out expensive prescription costs or Medicare.gov premiums could result in an unnecessary denial.

“When dealing with a massive bureaucratic error, time is your most valuable asset. Do not wait for the government to fix its own mistakes—you have to be your own loudest advocate.” — Jean Chatzky, Financial Editor and Author

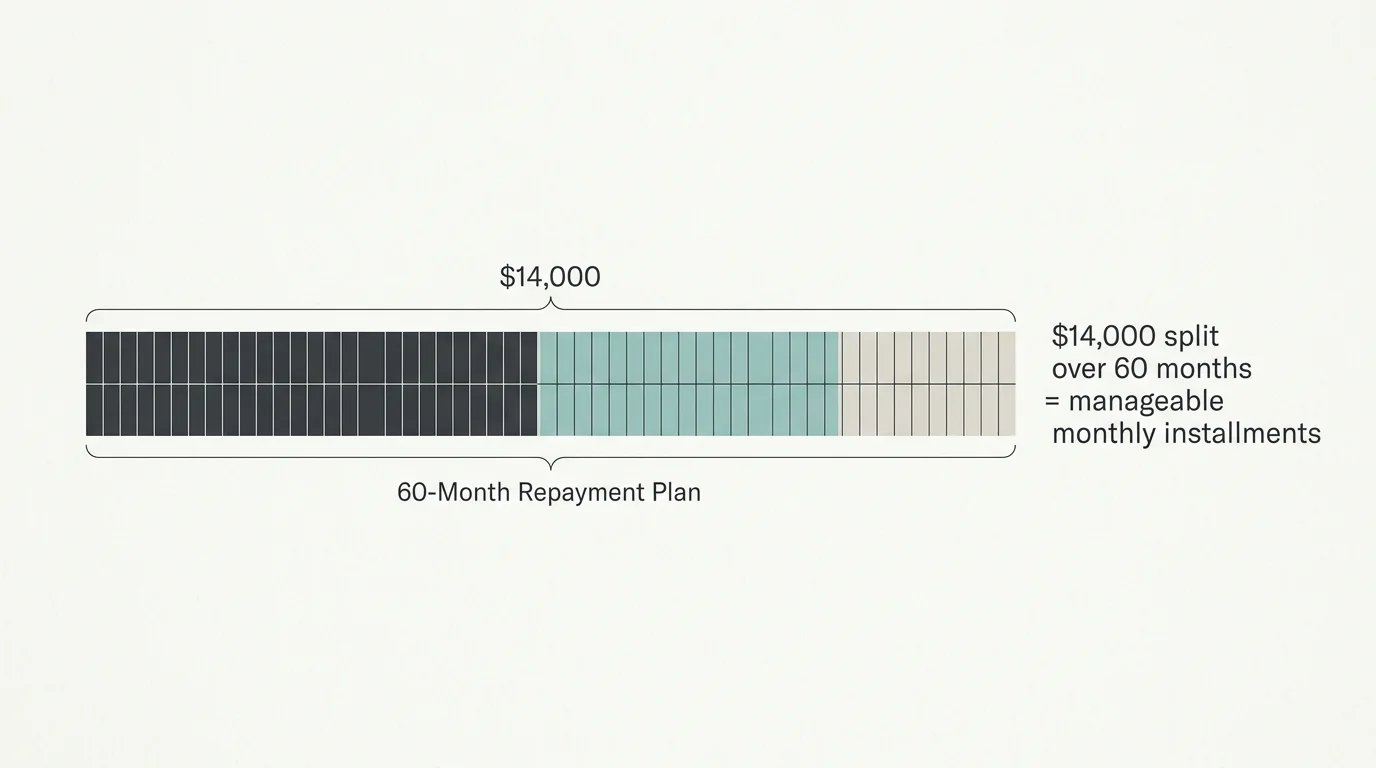

Step 3: Negotiate a Manageable 60-Month Repayment Plan

If you do not qualify for a full waiver—perhaps because you forgot to report a pension change or because your household assets are too high—you still have options. You do not have to accept the default 50 percent garnishment rate that wrecks your monthly cash flow.

You have the legal right to negotiate a repayment plan spread out over 60 months (five years). The agency generally approves these requests without requiring you to fill out the invasive financial hardship forms, provided the math results in a minimum payment of at least $10 per month.

Let us look at a concrete example. If you owe $14,000, dividing that debt over 60 months results in a monthly payment of roughly $233. If you receive the 2026 average retirement benefit of $2,026, paying $233 represents an 11.5 percent reduction in your check. While not ideal, it is infinitely more manageable than the default 50 percent penalty, which would slash your check by $1,013 every single month. To set up this 60-month plan, call the SSA directly at 1-800-772-1213 or visit your local field office.

Action Plan: Which Form Should You File?

Understanding which path to take is half the battle. Use this breakdown to determine your next steps based on your unique situation.

| Your Situation | Appropriate Action | Required Form | Result During Review |

|---|---|---|---|

| You disagree with the debt amount or believe you were not overpaid. | File an appeal to challenge the facts. | Form SSA-561 (Reconsideration) | Collections are paused while the SSA reviews your evidence. |

| You agree you were overpaid, but it was not your fault and you cannot afford repayment. | Request a complete forgiveness of the debt. | Form SSA-632 (Waiver) | Collections are paused while your financial hardship is evaluated. |

| You agree with the debt and have the means to repay it, but need a lower monthly rate. | Negotiate a 60-month repayment schedule. | Call the SSA directly (No long form needed if under 60 months) | Your withholding rate is adjusted to the agreed-upon lower amount. |

Common Mistakes to Avoid

When panic sets in, retirees often make hasty decisions that permanently damage their long-term financial health. Avoid these frequent missteps if you receive a demand letter:

- Ignoring the correspondence: Hoping the government will forget about the debt guarantees the worst possible outcome. Ignoring the letter ensures the SSA will trigger the 50 percent default garnishment after 30 days.

- Draining your retirement accounts: Do not panic and write a $14,000 check from your IRA. Pulling a large lump sum from a traditional retirement account will trigger massive income taxes and deplete the very safety net you need for your future. Always explore waivers and payment plans first.

- Filing the wrong paperwork: Submitting a waiver when you actually need a reconsideration causes massive administrative delays. If the SSA made a math error, a waiver is the wrong tool—you need an appeal.

- Missing the 60-day legal deadline: While the 30-day window stops garnishment, the 60-day window is your absolute final deadline to dispute the facts of the case. Missing it limits your options exclusively to financial hardship waivers.

“Never dip into your essential retirement reserves out of fear. When a surprise bill arrives, exhaust every appeal and payment plan option before you even think about touching your life savings.” — Suze Orman, Personal Finance Expert

How Overpayments Affect Your Taxes

Repaying a massive sum to the government complicates your annual tax filings. Social Security benefits are taxable if your combined income exceeds certain thresholds. If you receive an overpayment and repay it in the exact same calendar year, the SSA will simply issue a Form SSA-1099 reflecting your net benefits, and your tax return will be straightforward.

However, if you repay an overpayment that occurred in previous years, you might have paid taxes on money you are now handing back to the government. You may be eligible to claim a deduction or a tax credit for the repaid amount in the year you pay it back. Additionally, older adults must factor in new tax codes. For tax years 2025 through 2028, seniors age 65 and older are eligible for an additional $6,000 standard deduction bonus. Navigating clawbacks alongside these new tax rules requires precision to ensure you do not overpay the IRS while simultaneously repaying the SSA.

Finding the Right Advisor

While many seniors successfully navigate simple appeals on their own, certain situations demand professional intervention. Consider consulting a licensed fiduciary, a senior advocacy group, or a tax professional if you face any of the following scenarios:

- The clawback threatens your Medicaid eligibility: If you are restructuring assets to repay a massive SSI overpayment, moving money incorrectly could trigger a penalty period for Medicaid or nursing home coverage.

- You owe an exceptionally large sum: If the SSA is demanding $20,000 or more and has already denied your initial waiver request, an elder law attorney can escalate your case to an Administrative Law Judge.

- Your tax situation spans multiple years: If you must amend past tax returns to recover taxes paid on benefits you subsequently returned to the government, a certified public accountant (CPA) will ensure you maximize your legal deductions.

Frequently Asked Questions

Will Social Security take my entire check for an overpayment?

No. While older, harsher policies allowed the agency to withhold 100 percent of your benefits, the default rate for Title II retirement and disability benefits in 2026 is generally up to 50 percent if you take no action. For SSI recipients, it is capped at 10 percent. You can negotiate these figures much lower by acting quickly.

Can I go to jail for a Social Security overpayment?

Overpayments are treated as civil administrative debts. Unless the government can prove you committed intentional, prosecutable fraud—such as using a deceased person’s identity—you will not face criminal charges or jail time for an honest reporting mistake or a bureaucratic calculation error.

What happens if the person who was overpaid passes away?

If a beneficiary dies before repaying the debt, the SSA does not simply forgive the balance. The agency will attempt to recover the overpayment from the deceased individual’s estate. They may also withhold funds from family members who are receiving survivor benefits directly tied to that specific earning record.

Do I need to hire a lawyer to file a waiver?

Legal representation is not required to file Form SSA-561 or Form SSA-632. The forms are designed for the public to complete independently. However, if your case moves past the initial review stages to a formal hearing before a judge, securing an advocate or attorney is highly recommended.

Next Steps for Protecting Your Retirement

Receiving a large demand letter from the federal government is incredibly stressful, but acting with urgency and precision puts you back in the driver’s seat. Secure your 30-day grace period by filing the appropriate paperwork immediately. Gather your financial documents, assess whether you need to fight the facts or request financial mercy, and never agree to a payment plan that jeopardizes your ability to afford housing, food, or medical care.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Last updated: February 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.