Retiring on a fixed income often means stretching every dollar, but choosing the right location can dramatically protect your savings. Medium-sized cities offer the perfect retirement balance—providing the advanced healthcare networks and cultural amenities of major metropolitan areas while maintaining the lower housing costs and favorable tax structures of smaller towns. With the 2026 Social Security cost-of-living adjustment landing at a modest 2.8 percent and Medicare Part B premiums climbing over $200 per month, relocating to a more affordable region is a practical strategy. By exploring these twelve budget-friendly cities, you can secure lower property taxes, find reasonably priced homes, and ensure your retirement funds last for the long haul.

The Financial Realities of Retiring in 2026

Living comfortably throughout your golden years requires a crystal-clear understanding of the current financial landscape. Inflation and rising healthcare costs easily eat into retirement savings if you fail to plan accordingly. In 2026, the standard Medicare Part B premium sits at $202.90 per month, while the annual deductible is $283. When you pair these medical expenses with the rising costs of utilities, groceries, and home maintenance, finding a tax-friendly state becomes essential.

The good news is that federal tax laws provide substantial relief for seniors. If you are 65 or older, the IRS grants you an additional standard deduction on top of the base amount. Furthermore, special temporary tax provisions currently offer a bonus deduction for seniors, dramatically lowering your taxable income. Before packing your bags, review how these federal numbers apply to your specific tax filing status.

| Filing Status | Base Standard Deduction | Age 65+ Additional Deduction | 2026 Senior Bonus Deduction | Total Potential Deduction |

|---|---|---|---|---|

| Single / Head of Household | $16,100 | $2,050 | $6,000 | $24,150 |

| Married Filing Jointly (Both 65+) | $32,200 | $3,300 ($1,650 each) | $12,000 ($6,000 each) | $47,500 |

While federal tax breaks help everyone, state-level taxation varies wildly. The true affordability of your retirement destination hinges on how the state treats your Social Security benefits, pension payouts, and withdrawals from your 401(k) or IRA.

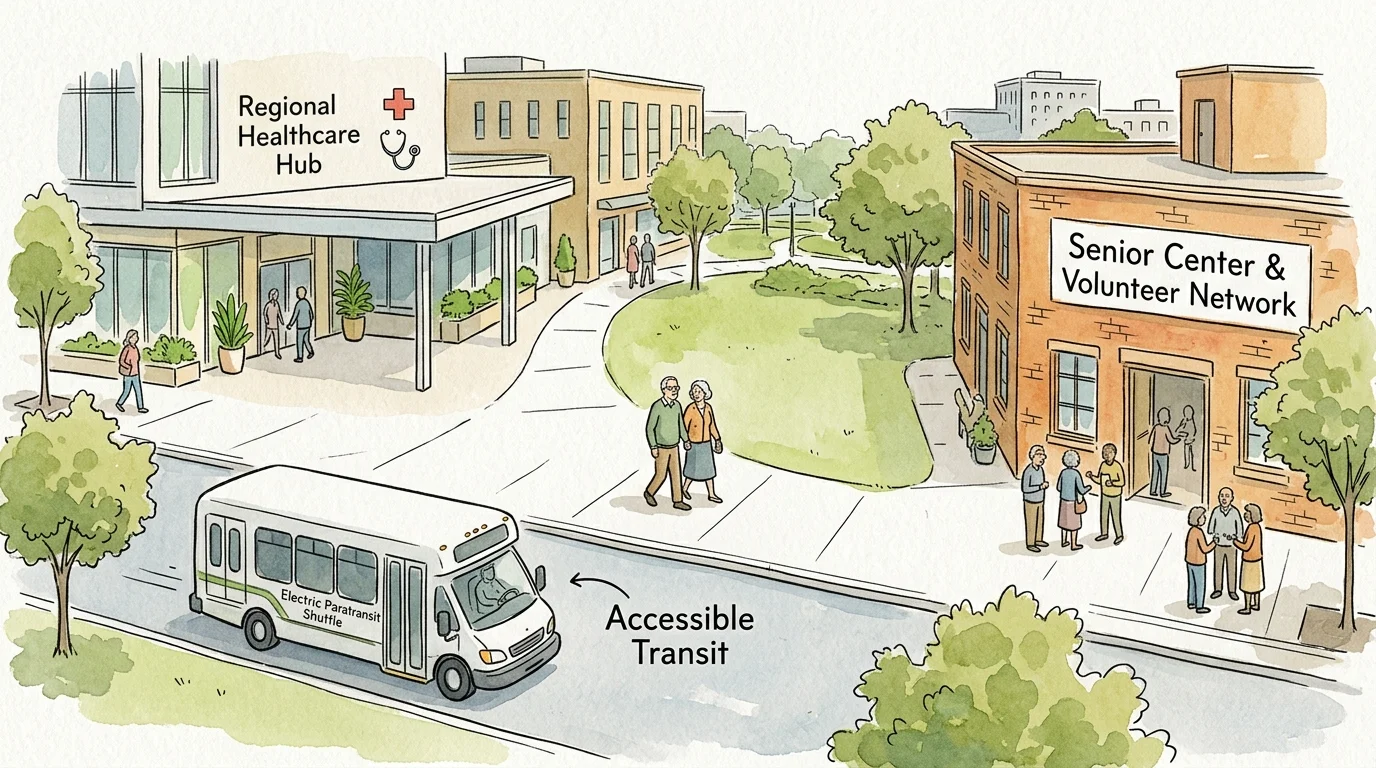

What Makes a Medium-Sized City Ideal for Aging at Home?

Medium-sized cities—typically defined as having a population between 100,000 and 500,000—hit the “Goldilocks” zone for retirees. Major cities often come with exorbitant property taxes, heavy traffic, and sky-high costs of living. On the flip side, rural areas might be cheap, but they often lack immediate access to specialists and comprehensive Medicare networks.

Relocating to a mid-sized city provides several structural advantages for aging in place:

- Robust Healthcare: These cities typically host regional medical hubs, meaning you do not have to travel hours to see a cardiologist or physical therapist.

- Manageable Cost of Living: Housing prices generally sit below the national average, allowing you to downsize and pocket the equity from your previous home.

- Community Engagement: Mid-sized communities often feature strong senior centers, volunteer networks, and local universities that offer continuing education for older adults.

- Accessible Transit: Many of these locations offer paratransit services and walkable neighborhoods, which become crucial if you eventually decide to stop driving.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

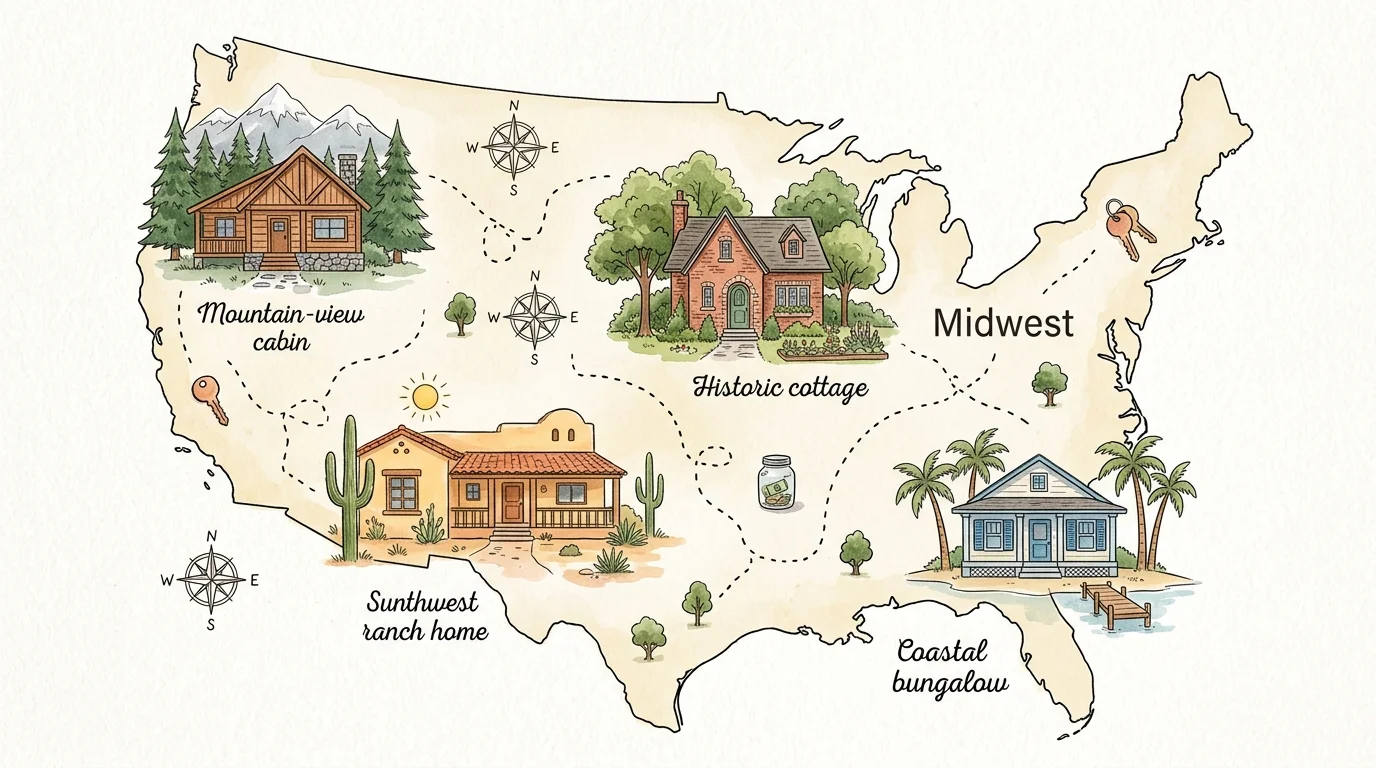

12 Affordable Cities for Your Retirement

To help you narrow down your search, we compiled a list of twelve exceptionally affordable medium-sized cities. These locations offer a blend of favorable tax environments, reasonable housing markets, and high-quality healthcare networks.

1. Green Valley, Arizona

Located just south of Tucson, Green Valley is a sprawling, scenic area comprising dozens of age-restricted retirement developments. While the national median home price has soared past $400,000, properties in Green Valley average around $282,000. The desert climate eliminates the physical strain of shoveling snow, and Arizona does not tax your Social Security benefits. You get the peace of a quiet community with immediate access to Tucson’s premier medical facilities.

2. Midland, Michigan

Midland consistently ranks at the top of national retirement lists, including taking the number one spot in the U.S. News 2026 rankings. It boasts abundant green spaces, a 110-acre botanical garden, and highly walkable neighborhoods. Best of all, Michigan is incredibly tax-friendly for seniors, offering generous exemptions on retirement income. The housing costs here fall well below the national average, making it an excellent place to stretch a fixed income.

3. Augusta, Georgia

Georgia is a haven for retirees looking to lower their tax burdens. If you are 65 or older, Georgia allows you to exclude up to $65,000 of retirement income per person from your state taxes. Augusta pairs this incredible tax advantage with mild winters, beautiful golf courses, and a remarkably low cost of living. Homebuyers will find that their dollars buy significantly more square footage here than in coastal retirement hotspots.

4. Des Moines, Iowa

Iowa recently revolutionized its tax code, transforming it into one of the most retiree-friendly states in the Midwest. As of 2023, Iowa completely exempts retirement income—including pensions, IRAs, and 401(k) distributions—from state income tax for residents age 55 and older. Des Moines offers a vibrant cultural scene, excellent hospitals, and a remarkably affordable housing market.

5. Sioux Falls, South Dakota

If you prefer to avoid state income tax entirely, South Dakota deserves a spot on your shortlist. Sioux Falls is a thriving mid-sized city known for its safety, cleanliness, and the magnificent Falls Park. It is also home to the Sanford Health system, providing top-tier medical care. While the winters are cold, the lack of state income tax leaves more money in your pocket to travel or invest.

6. Winston-Salem, North Carolina

North Carolina appeals to retirees who want a moderate climate with four distinct seasons. Winston-Salem offers an affordable alternative to pricier cities like Asheville or Charlotte. The city is renowned for its healthcare, anchored by the Wake Forest Baptist Medical Center. North Carolina does not tax Social Security, and everyday expenses like groceries and utilities remain budget-friendly.

7. Lancaster, Pennsylvania

Pennsylvania offers a massive financial perk for retirees: it does not tax Social Security benefits or eligible pension income. Lancaster blends historic charm with a rolling, scenic countryside. The area features numerous high-quality healthcare networks and a cost of living that makes aging in place highly sustainable. It frequently ranks in the top ten retirement destinations nationwide for its overall quality of life.

8. Fort Wayne, Indiana

When it comes to pure housing affordability, Fort Wayne is tough to beat. Your retirement savings can stretch incredibly far here, allowing you to easily purchase a single-story home suitable for aging in place. Indiana exempts Social Security from state taxes, and Fort Wayne provides ample community amenities, including an extensive parks system and a revitalized downtown area.

9. Spokane, Washington

For retirees who love the great outdoors but want to escape the astronomical housing prices of Seattle, Spokane is a brilliant alternative. Washington state levies no personal income tax, protecting your retirement distributions from state-level cuts. Spokane features a stunning riverfront, excellent hospitals, and a drier, sunnier climate than the western half of the state.

10. Knoxville, Tennessee

Tennessee is another state with no personal income tax, and Knoxville provides a beautiful, affordable gateway to the Smoky Mountains. The city maintains a low cost of living while offering the amenities of a college town, thanks to the University of Tennessee. You will find endless opportunities for outdoor recreation, continuing education, and cultural events.

11. Lexington, Kentucky

Lexington blends Southern charm with a highly favorable tax environment. Kentucky exempts all Social Security benefits and allows a generous exclusion of up to $31,110 of additional retirement income per person. Known as the “Horse Capital of the World,” Lexington features beautiful rolling landscapes, top-rated healthcare facilities, and a cost of living that respects a fixed budget.

12. Kansas City, Missouri

Straddling the border of Missouri and Kansas, this vibrant metro area offers big-city amenities at mid-sized prices. Missouri fully eliminated state income tax on Social Security benefits in 2024, making it much more attractive for retirees. Kansas City provides world-class barbecue, a legendary jazz scene, and incredibly affordable attractions for when the grandchildren visit.

What Can Go Wrong: Common Mistakes When Relocating

Relocating for retirement is a massive life event, and simple oversights can lead to financial headaches. Avoid these common missteps to ensure your move is successful:

- Underestimating Healthcare Network Changes: If you use a Medicare Advantage plan, your network is localized. Moving to a new state or even a new county means you must enroll in a new plan. Check if your preferred doctors and hospitals are covered in your new city before buying a house.

- Ignoring Property Tax Reassessments: Some states have low housing prices but extremely high property taxes. Additionally, buying a new home often triggers a tax reassessment based on the current market value, which might result in a higher tax bill than the previous owner paid.

- Failing to Consider Long-Term Mobility: A two-story home on a steep hill might be fine at age 65, but it could become a hazard at age 85. Always prioritize single-story living, walk-in showers, and minimal stairs when purchasing a home for retirement.

- Moving Too Far from Support Networks: Moving purely for financial reasons can backfire if it leaves you isolated. Factor in the cost of flights or long drives to visit family, as isolation can negatively impact both your mental and physical health.

When to Consult a Professional

While researching cities online is a great starting point, certain situations require expert guidance to protect your assets. Consider hiring a professional if you face any of the following scenarios:

You Are Planning a Roth Conversion: Moving from a high-tax state to a low-tax state changes the math on Roth conversions. A tax advisor can help you time your conversions to minimize your lifetime tax burden.

You Have Complex Pension Income: State laws governing pension taxation are notoriously complex. Some states tax government pensions differently than private pensions. A certified financial planner can project your exact net income based on your new state’s laws.

You Are Selling a Highly Appreciated Home: If you are selling a home you have owned for decades, you might face capital gains taxes. A tax professional can help you navigate the primary residence exclusion rules to shield up to $500,000 of profit (for married couples) from federal taxes.

Frequently Asked Questions

Does Medicare cover me if I move to another state?

Original Medicare (Part A and Part B) is a federal program and covers you anywhere in the United States. However, if you have a Medicare Advantage plan (Part C) or a standalone Prescription Drug Plan (Part D), you will likely need to choose a new plan specific to your new zip code using a Special Enrollment Period.

How do state taxes impact my Social Security benefits?

As of 2026, the vast majority of states—42 in total—do not tax Social Security benefits at the state level. However, if you move to one of the few states that still tax these benefits, your net monthly income could drop. Always verify the current tax laws of your destination state before relocating.

Should I rent or buy when relocating for retirement?

Renting for six months to a year is a highly recommended strategy when moving to a new city. It allows you to test the climate, explore different neighborhoods, and establish a healthcare team without committing hundreds of thousands of dollars to a home purchase.

Making Your Final Choice

Choosing where to spend your retirement is about much more than just crunching numbers; it is about finding a community where you feel safe, supported, and engaged. The twelve cities outlined above offer a fantastic starting point for retirees looking to balance their checkbooks without sacrificing their quality of life. Take the time to visit your top choices during different seasons, review the local medical facilities, and consult with professionals to ensure the tax advantages align with your specific income sources.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, benefits, tax situation, and health needs—may require different approaches. When in doubt, consult a licensed financial advisor or tax professional.

Helpful Resources:

- Social Security Administration (SSA)

- Medicare.gov

- Internal Revenue Service (IRS)

- National Council on Aging (NCOA)

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources.