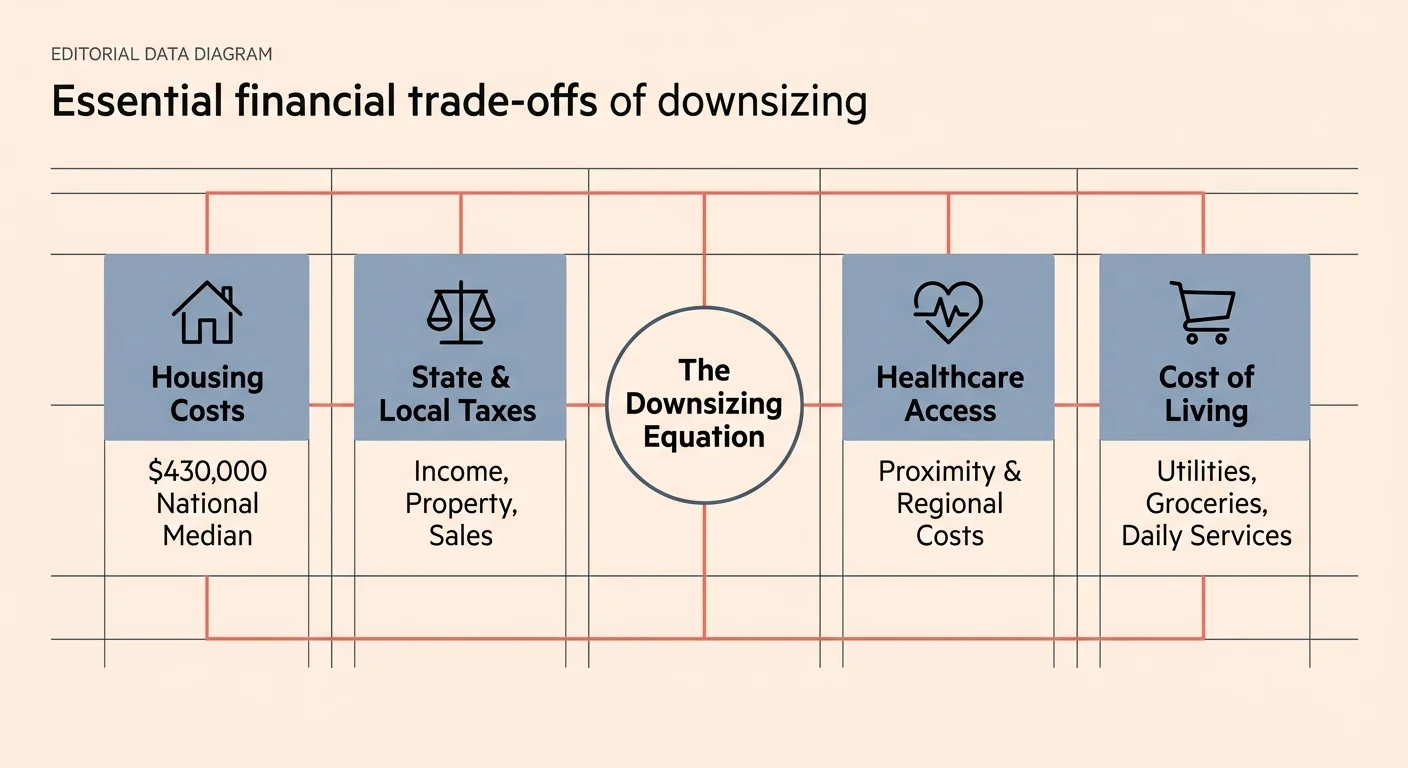

Downsizing in retirement is one of the most effective ways to lower your living expenses and unlock the equity tied up in your current home. By relocating to a tax-friendly or lower-cost area, you can easily add thousands of dollars to your annual retirement budget. The median list price for a U.S. home sat at $430,000 in June 2026, meaning a strategic move could free up significant cash for your future. Whether you want a warmer climate, proximity to top-tier healthcare, or an active community, choosing the right destination requires balancing housing costs with local tax policies. Before packing your boxes, review these 10 distinct locations that offer a superb mix of financial benefits and lifestyle perks for your next chapter.

1. Cheyenne, Wyoming: Wealth Preservation in the West

If maximizing your retirement income is a primary goal, Wyoming deserves your full attention. According to a 2026 WalletHub study evaluating tax rates, living costs, and healthcare access, Wyoming ranks as the overall best state to retire in the United States. The financial appeal is straightforward—Wyoming levies no personal income tax. This means your Social Security benefits, pension payouts, and 401(k) withdrawals remain entirely yours. Cheyenne offers a relatively affordable housing market compared to other western hubs, alongside wide-open spaces and a slower pace of life. However, you must be prepared for harsh winters and potentially longer drives to specialized medical facilities.

2. Midland, Michigan: The Affordable Midwest Gem

Midland claimed the number one spot on the U.S. News & World Report Best Places to Retire list for 2026. Located in the heart of Michigan, this city offers an incredible balance of quality of life and affordability. The median home value in Midland hovers around $206,142, which sits well below the national average. When you downsize here, your home equity stretches significantly further. Michigan also provides favorable tax treatment for retirees, often exempting a large portion of pension income and Social Security benefits from state taxes. Midland is highly regarded for its cultural amenities, safe neighborhoods, and outdoor recreation.

3. The Woodlands, Texas: Premium Living with Zero Income Tax

Texas remains a massive draw for retirees looking to stretch their budgets, primarily because it is one of the nine U.S. states with no personal income tax. The Woodlands, a meticulously planned community just north of Houston, frequently ranks near the top of national retirement lists. While the housing here is more expensive than rural Texas, downsizing from a high-cost coastal city to a smaller property in The Woodlands can still yield substantial savings. You gain immediate access to world-class medical care in the Houston metro area—a vital factor as healthcare needs evolve. Just remember to account for higher property taxes, which Texas uses to offset its lack of an income tax.

4. Altoona, Pennsylvania: Tax-Exempt Pensions and Lower Living Costs

Pennsylvania stands out as a unique financial haven for older adults: it is one of the few states that completely exempts qualifying pension income, 401(k) distributions, and IRA withdrawals from state income tax. Altoona, nestled in the scenic Allegheny Mountains, offers an incredibly low cost of living, allowing retirees to comfortably downsize. Property values are modest, and everyday expenses like groceries and utilities fall below national averages. The city boasts a rich railroad history, numerous parks, and a tight-knit community feel. If you want to experience four distinct seasons while keeping your retirement distributions tax-free, Altoona is a highly practical choice.

5. Palm Coast, Florida: Coastal Living with Financial Advantages

Florida is the traditional gold standard for retirement, driven by its warm climate and absolute lack of state income tax. However, famous retirement hubs like Naples and Miami have become prohibitively expensive for many downsizers. Palm Coast offers a more manageable entry point into the Florida lifestyle. Situated between St. Augustine and Daytona Beach, it provides miles of quiet beaches, numerous golf courses, and a growing network of healthcare providers. By choosing Palm Coast over a larger South Florida metro, you can secure a smaller, manageable home without draining your retirement portfolio.

6. Henderson, Nevada: Sun, Savings, and No State Tax

For those who want desert warmth without the intense cost of living found in southern California, Henderson is a premier contender. Nevada joins Florida and Texas on the list of states with zero personal income tax. Henderson is consistently ranked as one of the safest cities in the country and offers endless amenities, from manicured golf courses to extensive walking trails. Because it borders Las Vegas, you enjoy easy access to an international airport, top-tier entertainment, and expansive dining options. Downsizing to a townhouse or condo in Henderson allows you to lock in a low-maintenance lifestyle while entirely shielding your retirement income from state taxation.

7. Decatur, Illinois: Ultra-Affordable Housing

If preserving your nest egg is your highest priority, Decatur offers staggering affordability. In recent data analyzing the cheapest places to retire, Decatur showcased median home values under $100,000. While Illinois is known for higher property taxes, the state offsets this burden for retirees by exempting most retirement income—including Social Security, pensions, and 401(k) withdrawals—from state income tax. If you sell a large family home in a high-cost area, buying a smaller home outright in Decatur could leave you with hundreds of thousands of dollars in surplus equity to invest for your future.

8. Homosassa Springs, Florida: Budget-Friendly Sunshine State Alternative

Homosassa Springs routinely earns high marks on national retirement rankings, emerging as a top destination for those prioritizing affordability without sacrificing the Florida climate. Known for its natural springs, manatee populations, and relaxed Gulf Coast vibe, this area allows you to escape the heavy traffic and inflated housing prices of urban Florida. The cost of living here remains accessible, and you still reap the benefits of Florida’s retiree-friendly tax code. Downsizing to a modest ranch home in Homosassa Springs gives you a quiet, nature-focused retirement with excellent financial stability.

9. Chattanooga, Tennessee: High-Tech Infrastructure Meets Natural Beauty

Tennessee features no state income tax, making it a highly attractive destination for retirees eager to protect their monthly cash flow. Chattanooga, affectionately known as the “Scenic City,” is nestled along the Tennessee River and surrounded by mountains. It offers an incredibly vibrant downtown area, excellent healthcare facilities, and a cost of living that remains below the national average. Furthermore, Chattanooga is famous for its municipal broadband network, offering some of the fastest and most reliable internet in the country—perfect for retirees who want to stay connected with distant family members via video calls.

10. Rio Rancho, New Mexico: Sunny Desert Charm for Less

New Mexico provides a rich cultural environment and a lower cost of living compared to neighboring Arizona and Colorado. Rio Rancho, located just north of Albuquerque, frequently appears on lists of top U.S. retirement cities due to its affordable housing and strong quality of life. The dry, sunny climate is ideal for seniors who suffer from joint pain or simply loathe shoveling snow. While New Mexico does tax some retirement income, recent legislative changes have made the state much friendlier to middle-income retirees. Rio Rancho offers stunning views of the Sandia Mountains and access to Albuquerque’s robust healthcare system.

Key Financial Factors to Evaluate Before Relocating

Finding a beautiful town is only half the battle. Before committing to a move, you must run the numbers on your specific situation. A destination that looks cheap on paper can quickly become expensive if you ignore localized costs. Consider these critical variables:

- Medicare and Healthcare Costs: While federal Medicare premiums apply nationwide—such as the standard Medicare Part B premium of $202.90 per month and the $283 annual deductible for 2026, according to the Centers for Medicare & Medicaid Services—the cost of supplemental insurance (Medigap) or Medicare Advantage plans varies heavily by zip code. Always price out your specific healthcare plans in your target city.

- State Taxation of Retirement Income: As outlined above, state tax laws differ wildly. Nine states have no income tax, while others fully tax 401(k) distributions but exempt Social Security. Review exactly how your target state will treat your specific mix of income streams.

- Property Taxes and Insurance: A state with no income tax often compensates by charging higher property taxes. Additionally, homeowners insurance has skyrocketed in coastal states; a smaller home in a hurricane-prone area might cost more to insure than a large home in the Midwest.

- Cost of Living Adjustments (COLA): Your Social Security benefits are protected by annual COLA increases. For example, if your monthly benefit is $1,800, a 2.5% COLA would add $45 to your monthly check. However, inflation hits different regions unevenly. Ensure your target city’s cost of living isn’t rising faster than your fixed income.

“You have to manage your money in retirement just as carefully—if not more carefully—than you did while you were working.” — Jean Chatzky, Financial Editor

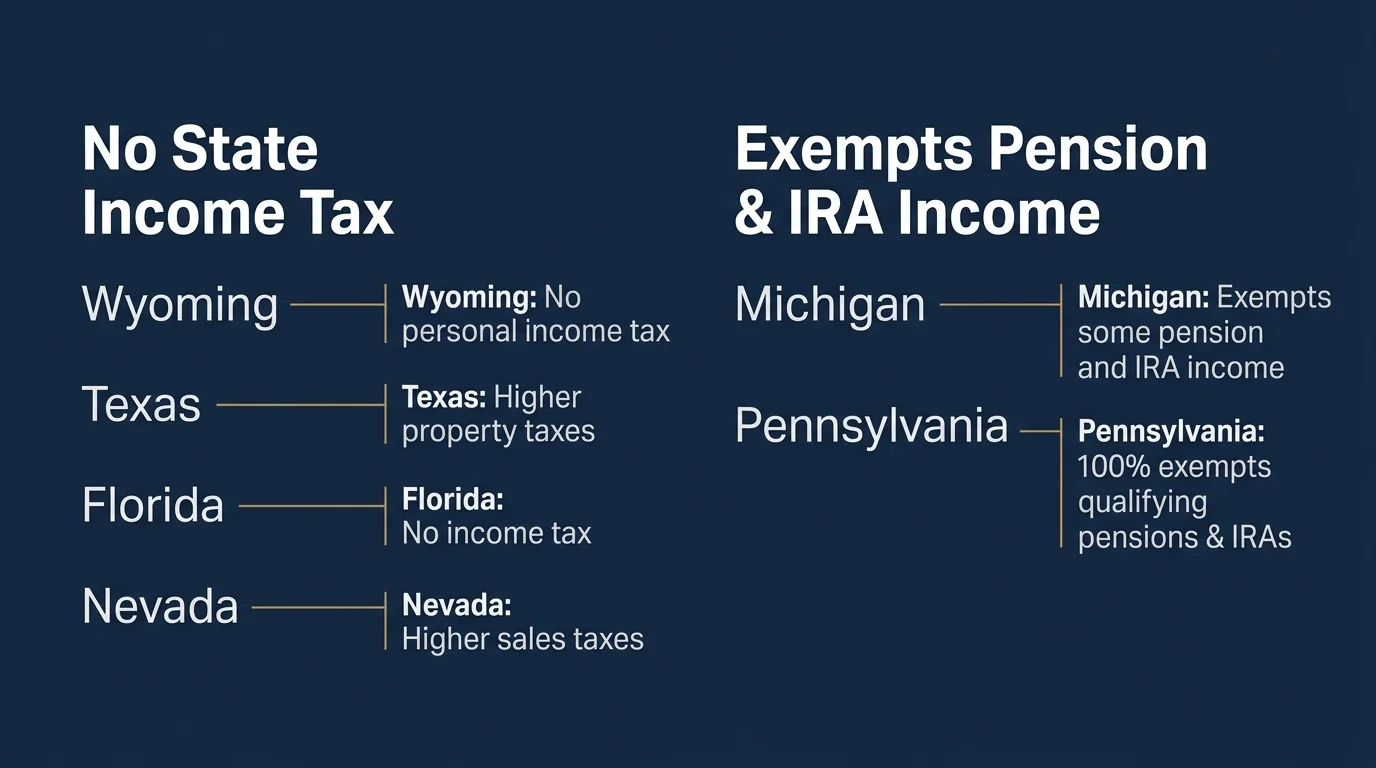

State Tax Treatment Comparison for Retirees

To help you visualize how different states approach retirement taxes, here is a quick comparison of a few popular downsizing destinations based on 2026 tax structures:

| State | State Income Tax Rate | Are Social Security Benefits Taxed? | Are Pensions & 401(k)s Taxed? |

|---|---|---|---|

| Florida | None | No | No (Fully Exempt) |

| Pennsylvania | 3.07% (Flat Rate) | No | No (Qualifying distributions are exempt) |

| Texas | None | No | No (Fully Exempt) |

| Michigan | 4.25% (Flat Rate) | No | Partially Exempt (Depends on age and source) |

| Nevada | None | No | No (Fully Exempt) |

Common Mistakes to Avoid When Downsizing

Downsizing is a major logistical and financial maneuver. Even careful planners can fall into traps that erode their projected savings. Be mindful of these common errors:

- Ignoring Hidden Homeownership Costs: You might find a townhome that costs half the price of your current house, but if it comes with a $600 monthly Homeowners Association (HOA) fee, your monthly savings could vanish. Always factor in HOA dues, special assessments, and local utility rates.

- Forgetting About Transaction Costs: Selling a home and buying a new one is expensive. You must account for real estate agent commissions, closing costs, moving company fees, and potential repairs to get your current home market-ready. These costs can easily consume 8% to 10% of your home’s sale price.

- Downsizing the House but Upgrading the Lifestyle: It is remarkably easy to sell a large, older home and buy a smaller, ultra-luxury condo. If the smaller home features high-end finishes, premium appliances, and resort-style amenities, you might end up spending exactly what you made on the sale, defeating the purpose of freeing up equity.

- Moving Too Far From Support Networks: Relocating halfway across the country for lower taxes sounds great on a spreadsheet, but social isolation is a real risk in retirement. Ensure your new location allows for easy travel back to family or offers a welcoming community where you can build new support systems.

Finding the Right Advisor When Relocating

Moving across state lines in retirement involves complex tax and investment decisions. Finding the right professional guidance is crucial depending on your specific scenario:

- Scenario 1: You are selling a highly appreciated home. If you have lived in your home for decades, you might face substantial capital gains upon sale. You need a Certified Public Accountant (CPA) to help you navigate the IRS primary residence exclusion and minimize your tax burden.

- Scenario 2: You are moving across state lines. Establishing a new tax domicile isn’t as simple as changing your mailing address. A fee-only financial planner can help you execute a “domicile checklist”—ensuring you properly switch your driver’s license, voter registration, and bank accounts so your former high-tax state doesn’t audit you.

- Scenario 3: You have a large cash windfall from your home sale. If downsizing frees up $200,000 in cash, leaving it in a standard checking account exposes it to inflation. A fiduciary investment advisor can help you integrate that cash into an income-producing portfolio to support your monthly living expenses.

Frequently Asked Questions

Do I have to pay capital gains taxes when I sell my home to downsize?

It depends on your profit. According to the IRS, single filers can typically exclude up to $250,000 of capital gains on the sale of a primary residence, while married couples filing jointly can exclude up to $500,000, provided they have owned and lived in the home for at least two of the past five years. Any profit beyond those thresholds is subject to capital gains tax.

Will my Medicare coverage work if I move to a different state?

Original Medicare (Parts A and B) is a federal program, so it travels with you anywhere in the U.S. that accepts Medicare. However, if you have a Medicare Advantage plan (Part C) or a standalone Part D prescription drug plan, you will likely need to enroll in a new plan specific to your new zip code. Moving triggers a Special Enrollment Period, allowing you to switch plans without penalty.

Are 55+ active adult communities actually cheaper than standard neighborhoods?

Not always. While the homes themselves might be smaller and easier to maintain, 55+ communities often feature extensive amenities like clubhouses, pools, and organized activities. These perks require substantial monthly HOA fees. You are paying for the lifestyle and community just as much as the real estate.

Downsizing your home is one of the most empowering financial choices you can make in retirement. By thoughtfully selecting a location that aligns with your tax situation, healthcare needs, and lifestyle preferences, you can protect your hard-earned savings while enjoying a vibrant, lower-stress daily life. Take your time researching these areas, visit them during different seasons, and consult with a tax professional before making your final leap.

This is educational content based on general financial principles for seniors. Individual results vary based on your situation. Always verify current benefit amounts, tax rules, and program eligibility with official government sources.

Last updated: July 2026. Benefit amounts, tax rules, and program details change annually—verify current figures with official government sources such as the Social Security Administration, Medicare.gov, and the Internal Revenue Service (IRS).